July 15, 2026

The Commodity Cycle That Never Fully Repeats Itself

Every major commodity supercycle carries a fingerprint unique to its era. The copper booms of the 1970s were shaped by Cold War industrialisation. The iron ore surge of the 2000s was written in China's urbanisation story. The lithium frenzy of 2022 was, in hindsight, partly speculative. What is unfolding across China's lithium sector in the first half of 2026 is something structurally different, and investors who mistake it for a replay of prior cycles may be misreading the market entirely.

The scale of the earnings recovery now being reported by China's largest lithium producers is difficult to overstate. However, the more significant question is not how large the profits are, but why they are happening now, and whether the conditions underpinning them are durable. Understanding that requires looking beyond the headline figures and into the mechanics of supply, demand, technology adoption, and China's unique position in the global battery materials chain.

When big ASX news breaks, our subscribers know first

How Large Is the Profit Surge? A Sector-Wide Performance Breakdown

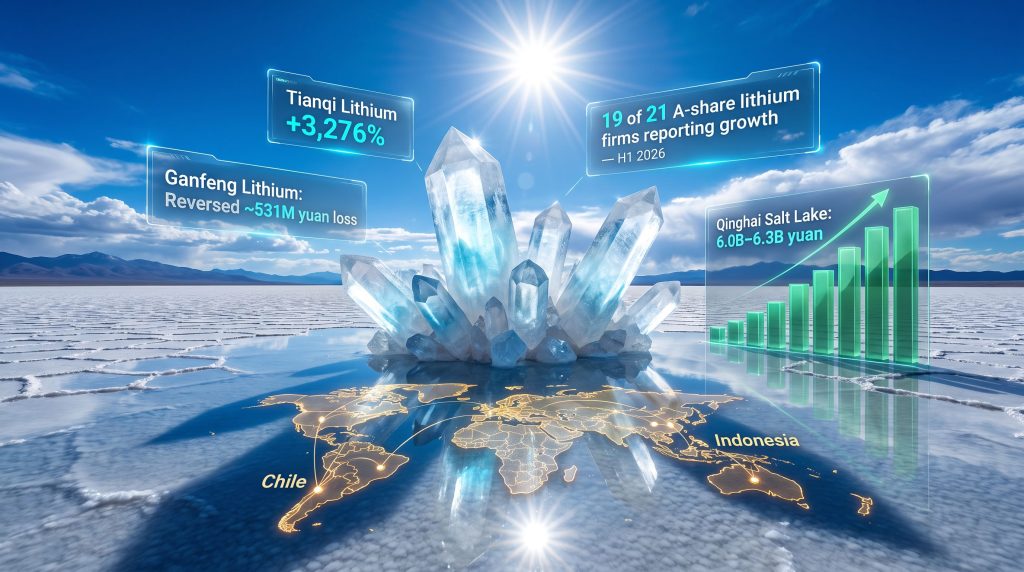

The H1 2026 earnings disclosures represent some of the most dramatic year-on-year profit recoveries seen in any commodity sector in recent memory. Tianqi Lithium, the Sichuan-based producer with assets spanning Chile and Australia, reported an estimated net profit range of 2.85 billion yuan to 4.25 billion yuan (approximately US$420 million to US$625 million) for the six months ended 30 June 2026. That figure represents a year-on-year increase of between 3,276% and 4,935%, reflecting the scale of destruction that the prior downturn inflicted and the speed at which conditions have reversed.

Ganfeng Lithium, recognised globally as the world's largest producer of metal lithium and lithium compounds, disclosed a projected net profit range of 3.65 billion yuan to 4.6 billion yuan for the same period, swinging from a net loss of 531 million yuan in H1 2025. This reversal ends two consecutive years of interim losses for the company, a milestone carrying significant strategic weight beyond the arithmetic.

H1 2026 Earnings Snapshot Across Major Chinese Lithium Producers

| Company | H1 2026 Net Profit (CNY) | Approximate USD Value | Year-on-Year Change |

|---|---|---|---|

| Tianqi Lithium | 2.85B – 4.25B yuan | ~US$420M – US$625M | +3,276% to +4,935% |

| Ganfeng Lithium | 3.65B – 4.6B yuan | ~US$537M – US$677M | Reversed ~531M yuan loss |

| Yahua Industrial | 1.1B – 1.3B yuan | ~US$162M – US$191M | +710% to +857% |

| Qinghai Salt Lake | 6.0B – 6.3B yuan | ~US$882M – US$927M | +131% to +143% |

| Zangge Mining | 3.55B – 3.75B yuan | ~US$522M – US$551M | +97% to +108% |

Qinghai Salt Lake's comparatively moderate growth rate is not a sign of weakness. It reflects the inherently more stable cost profile of brine-based lithium extraction, where production costs are structurally lower and less volatile than hard-rock operations. When prices were depressed, brine producers suffered less. When prices recover, their percentage gain appears smaller, even as absolute profits remain enormous.

The current earnings surge is not isolated to one or two companies. Of 21 A-share listed lithium battery firms that disclosed H1 2026 earnings outlooks, 19 reported growth, confirming this is a sector-wide recovery driven by structural forces rather than company-specific execution.

The distinction between returning to profit and achieving record earnings is also meaningful. Yahua Industrial's growth figures of 710% to 857% suggest a company recovering from near-zero profitability, while Qinghai Salt Lake's numbers reflect a business that never fully collapsed but is now operating at a materially higher earnings level than its already-profitable prior-year base.

What Is Driving the China Lithium Profit Surge in 2026?

Driver 1: Lithium Price Recovery and the End of the Destocking Cycle

The lithium market downturn of 2024 to mid-2025 represented one of the most severe price corrections in the mineral's commercial history. Prices for lithium carbonate and lithium hydroxide fell by more than 80% from their 2022 peaks as oversupply collided with a slowdown in downstream demand growth. Battery manufacturers worked through bloated inventories rather than procuring fresh material, compressing both volumes and prices simultaneously for upstream producers.

What distinguishes the current recovery from the 2022 price spike is its demand foundation. The 2022 surge was partly driven by procurement panic and inventory accumulation across the battery supply chain. Furthermore, the 2026 recovery is occurring as those inventories are exhausted and genuine end-user demand is driving restocking. Average selling prices for major lithium products rose markedly year-on-year in H1 2026, as confirmed in Tianqi Lithium's exchange filings, and this reflects real consumption growth rather than speculative positioning.

Driver 2: Structural Supply Constraints and Project Pipeline Gaps

New lithium supply is not appearing fast enough to satisfy demand growth. Across Western mining jurisdictions, capital discipline imposed during the 2024 price downturn caused widespread project deferrals. Permitting timelines in jurisdictions including the United States, Canada, and parts of Europe routinely extend beyond five years from discovery to production, meaning projects shelved in 2024 cannot contribute meaningfully to supply before 2029 or 2030 at the earliest.

This creates an asymmetry that benefits producers already in operation. Chinese lithium companies, many of which maintained production continuity through the downturn by absorbing losses or drawing on balance sheet strength, are consequently positioned to capture the full margin expansion of the recovery cycle while competitors are still in development mode.

Driver 3: New Energy Vehicle Demand as the Primary Consumption Engine

Global NEV adoption continues to accelerate across multiple geographies simultaneously. China, Europe, and Southeast Asia are all registering record EV sales volumes, and each new vehicle sold represents a direct and ongoing demand commitment for lithium-ion battery chemistry. The compounding effect of a growing vehicle fleet, combined with increasing battery pack sizes per vehicle to extend driving range, means the lithium demand curve from the automotive sector alone is steep and durable.

The simultaneous rise in both volume and price, often described in the industry as a dual-growth dynamic, creates a compounding effect on margins that is more powerful than either factor operating independently. When a producer is selling more units and selling each unit at a higher price, the operating leverage effect on profitability can produce earnings multiples that appear extraordinary but are mathematically straightforward.

Driver 4: Energy Storage Systems Emerging as a Demand Multiplier

Beyond EVs, battery storage expansion is becoming an increasingly significant consumer of lithium chemicals. The rapid deployment of solar and wind generation capacity globally creates a structural need for storage to manage intermittency, and lithium-ion batteries are the dominant technology for this application at current cost and performance levels.

An underappreciated secondary driver of energy storage demand is the growth of AI infrastructure. Data centres require highly reliable power with minimal interruption, and large-scale battery storage systems are being deployed alongside data centre campuses to ensure power quality and continuity. This creates a demand channel for lithium that is entirely separate from the transportation sector and is growing rapidly.

Ganfeng's vertical integration into battery manufacturing allows it to capture value from both the upstream chemical production and the downstream ESS sales cycle, positioning it differently from pure-play mining companies that are purely price-takers on the commodity side.

How Do China's Lithium Giants Maintain Their Competitive Edge?

Vertical Integration as a Structural Moat

The business models of China's leading lithium producers have evolved well beyond simple mineral extraction. The most sophisticated players now operate across the full value chain:

- Raw material extraction from owned or controlled brine and hard-rock operations

- Chemical refining converting spodumene concentrate or brine into battery-grade lithium carbonate or hydroxide

- Battery cell manufacturing supplying finished energy storage products to automotive and grid-storage customers

- Recycling operations recovering lithium from end-of-life batteries to reduce raw material dependency

This vertical depth insulates integrated producers from single-point price volatility and allows them to shift margin capture up or down the value chain depending on where pricing conditions are most favourable. During periods of low lithium chemical prices, downstream battery margins may still be healthy. During periods of high chemical prices, upstream mining operations generate excess returns.

Tianqi Lithium's asset base illustrates a different but complementary form of competitive advantage: geographic diversification across the world's highest-quality lithium resources. Its operational presence across Chilean brines and hard-rock operations in Australia represents access to two of the three largest lithium reserve concentrations on the planet. The geological quality of these assets, particularly the high lithium grade and low impurity profiles of the Chilean brines, underpins cost structures that are difficult for newer entrants to replicate regardless of capital investment.

The geographic diversification of Chinese lithium producers across South America, Australia, and Southeast Asia provides meaningful insulation from single-jurisdiction supply disruptions, a structural advantage that Western competitors are only beginning to address seriously.

In addition, Ganfeng's strategic identity rests on its position as the world's largest producer of both metal lithium and lithium compounds, combined with an international project diversification strategy spanning multiple continents. The Argentina lithium brine market and Southeast Asian processing assets both feature in this broader Chinese lithium supply architecture, offering cost and logistical advantages for serving regional battery manufacturing clusters.

Is This Profit Surge Sustainable? Risks and Scenarios to Watch

No commodity recovery is without limits, and intellectual honesty requires examining the scenarios under which the current China lithium firms profit surge could moderate or reverse.

Scenario Analysis: Three Possible Trajectories Through 2027

Scenario A: Continued Tightening (Bull Case)

NEV adoption accelerates beyond current consensus forecasts. ESS deployments compound lithium demand at rates the supply pipeline cannot match. Lithium prices stabilise at elevated levels, and margin durability extends well into 2027. Integrated Chinese producers capture the largest share of value creation.

Scenario B: Managed Equilibrium (Base Case)

New project pipelines from Australia, Africa, and South America gradually restore supply balance through late 2026 and into 2027. Prices moderate from peak levels but do not return to the 2024 trough. Profitability across the Chinese lithium sector persists at levels that are healthy but below H1 2026 peaks. This remains the most probable outcome under current conditions.

Scenario C: Renewed Oversupply (Bear Case)

Accelerated project completions across multiple geographies flood the market faster than demand growth absorbs them. Macroeconomic headwinds or the rollback of EV incentive programmes in key markets slows demand. Margins compress again, though vertically integrated producers with low-cost assets prove more resilient than pure-play upstream miners.

Key Risk Factors to Monitor

- Geopolitical tensions affecting cross-border lithium trade agreements and processing partnerships

- Regulatory changes in lithium-rich jurisdictions, particularly Chile's ongoing debate around state involvement in lithium development, Argentina's fiscal instability, and Australia's evolving critical minerals framework

- Technology substitution risk from sodium-ion battery chemistry, which is advancing faster than many Western analysts acknowledge and could displace lithium in lower-cost, shorter-range applications

- Currency fluctuation impacts on yuan-denominated earnings from offshore assets, particularly as US dollar strength can mask or amplify reported profitability in domestic reporting terms

China's Processing Dominance and the Global Energy Transition

One frequently overlooked dimension of the China lithium firms profit surge is what it reveals about the structure of the global battery materials industry. China does not simply mine lithium; it refines the overwhelming majority of the world's lithium chemicals regardless of where the raw ore originates. Australian spodumene, Chilean brine, and African lepidolite all pass through Chinese processing infrastructure at significant scale.

This processing dominance means that the profitability of Chinese lithium producers is partially insulated from geographic shifts in raw material production. Innovations such as direct lithium extraction may eventually alter this dynamic, but the refining bottleneck remains concentrated in China for the foreseeable future, even as Western nations invest in developing domestic lithium mining capacity through frameworks such as the US Inflation Reduction Act and the EU Critical Raw Materials Act.

The shift in how governments classify lithium — moving from an ordinary industrial commodity to a strategic industrial input essential for energy security — is creating a demand floor that has no parallel in earlier commodity cycles. Policy-driven procurement, national stockpiling programmes, and mandated domestic content requirements in battery manufacturing are all layering structural demand onto the cyclical demand that already exists from private sector EV and ESS deployment.

This does not mean lithium is immune to price cycles. It means the floor of those cycles is likely higher than historical averages would suggest, because governments are now participants in the demand side of the market in ways they were not during previous commodity downturns. Furthermore, the China battery recycling outlook adds another layer of supply resilience, as recovered material increasingly supplements primary production.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: China Lithium Firms Profit Surge

Why are Chinese lithium companies reporting such large profit increases in 2026?

The convergence of three forces — a sharp rebound in lithium chemical prices from multi-year lows, accelerating demand from NEV and ESS markets, and constrained new supply from competing jurisdictions — has produced a simultaneous volume and price growth environment that generates outsized profitability for producers with low-cost, vertically integrated operations.

Which Chinese lithium company posted the highest profit growth percentage in H1 2026?

On a percentage basis, Tianqi Lithium's reported range of 3,276% to 4,935% year-on-year growth is the most dramatic, though this reflects the extreme depth of its prior-year losses rather than necessarily superior operational performance relative to peers.

Is the lithium market recovery expected to continue beyond 2026?

The base case among market observers is a gradual moderation as new supply comes online. However, prices are expected to remain above the 2024 trough given structural demand growth from EVs, grid storage, and policy-driven procurement programmes. The timing and scale of new project completions will be the primary variable to watch. For instance, current lithium price data continues to reflect a markedly improved environment compared to the depths of the prior downturn.

How does Ganfeng Lithium differ from Tianqi Lithium in its business model?

Tianqi's model is anchored in controlling world-class upstream assets in Chile and Australia, making it primarily a lithium chemicals producer. Ganfeng, in contrast, operates further down the value chain, combining upstream mining and chemical production with lithium-ion battery manufacturing, giving it exposure to downstream ESS and EV battery demand in ways that Tianqi currently does not replicate at the same scale.

What role does energy storage play in driving lithium demand growth?

Grid-scale ESS deployment is growing rapidly as renewable energy penetration increases globally, requiring storage to manage supply intermittency. Combined with AI data centre power resilience requirements, ESS represents a demand channel that is growing independently of EV adoption and adds meaningful volume to overall lithium consumption forecasts.

Are smaller Chinese lithium producers also benefiting from the recovery?

Yes. Of 21 A-share listed lithium battery companies that disclosed H1 2026 earnings outlooks, 19 reported growth, confirming the recovery is broad-based across the sector rather than concentrated in the two largest players.

Key Takeaways: The Strategic Significance of China's 2026 Lithium Earnings Boom

The profit environment Chinese lithium producers are reporting in the first half of 2026 is the product of structural forces that have been accumulating for several years, not a short-term commodity spike. Five converging dynamics underpin the current China lithium firms profit surge:

- Lithium price normalisation following one of the deepest corrections in the mineral's commercial history

- Supply pipeline gaps created by capital discipline and permitting delays in Western jurisdictions

- Accelerating NEV adoption across multiple major markets simultaneously

- Emerging ESS demand from grid storage and AI infrastructure buildout

- Vertical integration advantages that allow Chinese producers to capture value across multiple points in the supply chain

Unlike the 2022 price spike, which was partly fuelled by inventory accumulation and procurement panic, the current recovery is underpinned by genuine end-user consumption growth and structural supply constraints. This distinction matters enormously for assessing sustainability.

The competitive positioning of Chinese lithium producers relative to global peers remains strong, anchored in geological asset quality, processing infrastructure scale, and vertical integration depth that Western competitors are years away from replicating. Investors and analysts tracking this sector should monitor new project completion timelines, sodium-ion battery adoption curves, and the evolving regulatory environment in lithium-rich jurisdictions as the primary indicators of when and how the current cycle matures.

This article contains forward-looking analysis and scenario projections based on publicly available information. It does not constitute financial advice. Commodity markets are inherently volatile, and actual outcomes may differ materially from scenarios described.

Want to Capitalise on the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex commodity data into actionable insights for both short-term traders and long-term investors — explore historic discoveries and their exceptional returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next major move in critical minerals.