July 15, 2026

The Quiet Transformation Hiding Inside a 3% Headline Number

When a mining company the size of Rio Tinto Ltd (ASX: RIO) reports a 3% rise in copper equivalent production, the temptation is to dismiss it as modest. But inside that aggregate figure lies something far more consequential: Rio Tinto production growth and lithium output are both in active transition, where iron ore cash flows are quietly funding one of the most ambitious lithium build-outs in the history of the resources sector.

Understanding Rio Tinto's H1 2026 results requires looking past the headline and into the mechanics of how a diversified major manages simultaneous commodity cycles, capital-intensive ramp-ups, and geopolitical friction without losing operational footing.

When big ASX news breaks, our subscribers know first

Copper Equivalent Production: What the Composite Metric Actually Tells You

Mining majors use copper equivalent (CuEq) production as a normalised benchmark precisely because their commodity portfolios are too diverse to summarise with a single volume number. CuEq converts each commodity's output into a copper-referenced unit using price ratios, allowing investors and analysts to assess overall production performance across iron ore, copper, aluminium, and lithium within a single comparable figure.

A 3% year-on-year rise in CuEq production across an operation of Rio Tinto's scale is not trivial. When you account for the capital intensity required to sustain production across multiple jurisdictions simultaneously, absorbing a 7% decline in bauxite output while still generating a net-positive aggregate result signals genuine operational breadth.

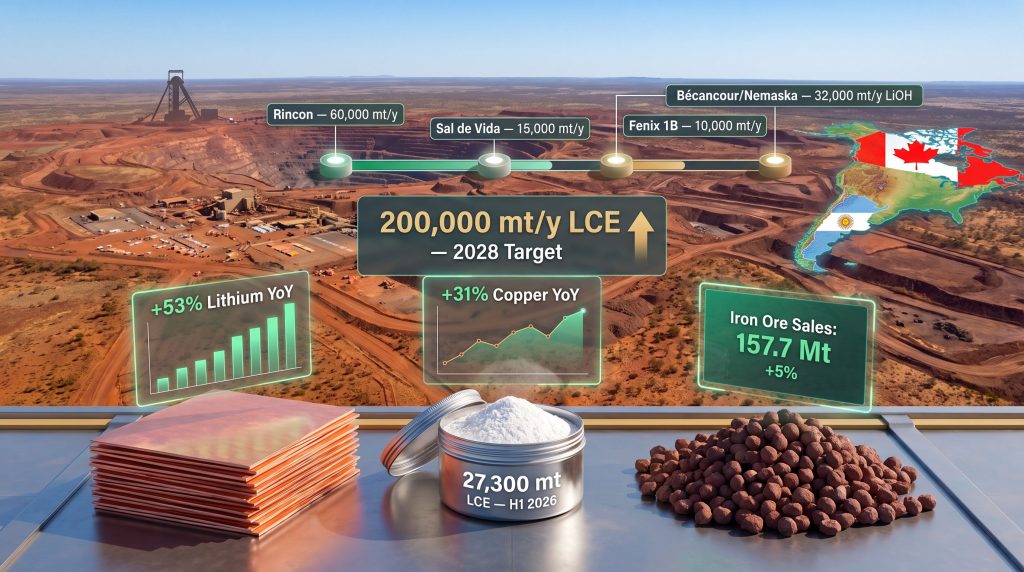

Key Insight: The 3% CuEq increase masked significant internal divergence. Lithium production rose 53% year-on-year in H1 2026, copper output at Oyu Tolgoi surged 31%, and iron ore sales climbed 5%, while bauxite fell 7%. The headline figure reflects disciplined portfolio management, not uniform performance.

The four structural pillars underpinning Rio Tinto's production base each moved at different speeds in H1 2026. That the group maintained full-year guidance across all four divisions simultaneously, despite weather events in Argentina, higher diesel costs in the Pilbara, and ongoing geopolitical uncertainty, reflects the operational discipline that scale and diversification enable.

Iron Ore: The Pilbara's Strongest First-Half Performance Since 2018

What Drove the Volume Uplift

Pilbara iron ore sales reached 157.7 million tonnes (Mt) in H1 2026, a 5% increase year-on-year and the strongest first-half result since 2018. The second quarter alone delivered 85.3 Mt in Pilbara sales, representing a 7% improvement over Q2 2025 levels. The driver was not a step-change in installed capacity but rather sustained productivity investment improving throughput efficiency across existing infrastructure.

This distinction matters for investors. Productivity-driven volume gains typically come with a more favourable cost profile than capacity-driven gains, because they leverage existing sunk infrastructure rather than requiring equivalent increases in capital expenditure.

Near-Term Friction Points to Monitor

Not all indicators were uniformly positive. Management flagged two headwinds for H2 2026:

- Port outload capacity reductions linked to ongoing capital works at Pilbara port facilities, which create a temporary throughput ceiling

- Higher diesel costs applying modest upward pressure on cash unit costs for Pilbara iron ore operations

These are operational realities of large-scale infrastructure investment cycles rather than structural impairments, but they are worth monitoring through the second half. Furthermore, the China steel and iron ore outlook remains a key variable shaping demand for Pilbara volumes over the medium term.

Simandou: The Long-Horizon Iron Ore Catalyst

Beyond the Pilbara, the Simandou iron ore development in Guinea represents a significant long-term addition to Rio Tinto's iron ore market position. Simandou contains some of the highest-grade iron ore deposits in the world, with grades reportedly exceeding 65% Fe content, which compares favourably to Pilbara grades that typically range from 56% to 62% Fe.

Higher-grade ore commands a price premium in the seaborne market because it reduces processing costs for steel mills, making it particularly attractive to customers seeking lower carbon intensity in their steel production processes. The Simandou project is approaching major completion milestones and represents a qualitative shift in Rio Tinto's iron ore portfolio, not just a volume addition.

Copper Growth: Oyu Tolgoi's Underground Ramp-Up and What Comes Next

Why Underground Block Cave Ramp-Ups Are Non-Linear

Copper output at the Oyu Tolgoi mine in Mongolia rose 31% year-on-year in H1 2026, driven by the ongoing ramp-up of underground block cave operations. The Oyu Tolgoi ramp-up is structurally significant and requires a brief explanation of block cave mining itself.

In block cave operations, a large mass of ore is undercut, causing it to cave under gravity into collection points below. Unlike open-pit mining, which produces relatively predictable volumes as benches are progressively excavated, underground block cave operations go through extended ramp-up phases before reaching steady-state production. Output growth during this phase is inherently non-linear, meaning volume gains can be outsized in percentage terms as the cave propagates and more drawpoints become active.

This structural dynamic means Oyu Tolgoi's 31% copper growth in H1 2026 is likely the beginning of a multi-year production expansion rather than a one-off event. As a direct consequence of higher volumes, C1 net unit costs at Oyu Tolgoi declined, demonstrating the classic relationship between throughput scale and cost efficiency in bulk mining operations.

The Next Wave: Resolution and Winu

Beyond Oyu Tolgoi, Rio Tinto copper expansion across two development assets represents the next phase of the growth pipeline:

- Resolution (Arizona, USA): A large porphyry copper deposit advancing through regulatory and permitting processes. The deposit is estimated to contain approximately 1.8 billion tonnes of ore, potentially making it one of the largest undeveloped copper deposits in North America.

- Winu (Western Australia): An emerging copper-gold deposit advancing toward development. Its Western Australian location offers proximity to established infrastructure and a well-understood regulatory environment.

Both projects remain subject to development timelines that are partially governed by permitting and regulatory approval processes, and investors should treat timelines as indicative rather than fixed.

Rio Tinto's Lithium Strategy: Building Toward 200,000 Tonnes Per Year

The Arcadium Acquisition as a Platform, Not a Destination

Rio Tinto's lithium ambitions are anchored by the $6.7 billion acquisition of Arcadium Lithium, which closed in March 2025. The transaction secured the world's third-largest lithium reserves and an operational footprint spanning Argentina and Canada, transforming lithium from a peripheral exposure into a designated fastest-growing divisional priority. The Rio Tinto lithium strategy has consequently become a central pillar of the group's long-term investment thesis.

What is less widely understood is that the acquisition also brought with it a proprietary direct lithium extraction (DLE) technology platform, which was a decisive factor in the acquisition rationale. DLE differs fundamentally from conventional evaporation pond extraction in three critical ways:

- Recovery rates: DLE can recover a significantly higher proportion of lithium from brine compared to evaporation ponds, which can leave substantial lithium in solution

- Water consumption: DLE processes return brine to the aquifer after lithium extraction, reducing net water consumption in water-stressed environments like the Argentine Puna plateau

- Production cycle times: Evaporation ponds require 12 to 24 months of solar evaporation before lithium can be recovered. DLE compresses this to hours or days, enabling more responsive production

Rio Tinto has indicated it is targeting a 50% EBITDA margin at scale across its lithium division, a figure that would be difficult to achieve with conventional evaporation technology at current lithium prices but becomes more plausible with DLE's superior recovery and lower operating cost profile.

H1 2026 Lithium Output: Reading the Numbers Correctly

| Period | LCE Output | Year-on-Year Change | Notes |

|---|---|---|---|

| Q1 2026 | 12,700 mt | -26% YoY | Weather disruption at Olaroz and Fenix |

| Q2 2026 | ~14,600 mt | +20% QoQ | Recovery trajectory underway |

| H1 2026 Total | 27,300 mt | +53% YoY | Reflects Arcadium baseline in prior year |

| Full-Year 2026 Guidance | 61,000–64,000 mt | Maintained | H2 front-loaded with new project contributions |

The Q1 shortfall deserves contextualisation. Weather-related disruptions at the Olaroz and Fenix operations in the Argentine Andes created a temporary production gap, not a structural impairment. The Olaroz operation sits at approximately 3,900 metres above sea level on the Puna plateau, an environment where extreme weather events can disrupt brine pumping and evaporation processes. Q2's recovery trajectory confirmed the transient nature of the Q1 disruption.

The more important arithmetic is what H1's 27,300 mt implies for H2. To meet the full-year guidance midpoint of approximately 62,500 mt, Rio Tinto needs to produce roughly 35,200 mt in H2 2026, a 29% step-up from H1 volumes. That requirement is not aggressive given that both Sal de Vida and Fenix 1B are expected to deliver first production in H2 2026.

The Four Projects Driving the 2028 Capacity Target

Strategic Target: Rio Tinto is targeting 200,000 metric tonnes per year (mt/y) of lithium carbonate equivalent capacity by 2028, representing more than a 2.5-fold increase from the approximately 75,000 mt/y baseline inherited through the Arcadium acquisition.

| Project | Location | Capacity Target | Status (H1 2026) | First Production |

|---|---|---|---|---|

| Rincon Expansion | Argentina | 60,000 mt/y LCE | Starter plant commissioning | 2028 (post ramp-up) |

| Sal de Vida | Argentina | 15,000 mt/y LCE | Commissioning 40% complete | H2 2026 |

| Fenix 1B | Argentina | 10,000 mt/y LCE | Commissioning 60% complete | H2 2026 |

| Bécancour/Nemaska | Canada | 32,000 mt/y LiOH | Construction 60% complete | 2028 |

| Group Target | Multi-jurisdiction | 200,000 mt/y LCE | On track | 2028 |

The Rincon project warrants particular attention. With $2.5 billion in committed capital investment, it represents the largest single-project commitment within the lithium expansion programme. A 3,000-tonne starter plant was in commissioning as of H1 2026, serving a dual purpose: generating early cash flow and validating the DLE process at commercial scale before the full 60,000 mt/y expansion is commissioned.

The Bécancour/Nemaska facility in Quebec introduces an important product differentiation. While the Argentine operations produce lithium carbonate, Bécancour will produce lithium hydroxide, the form preferred by battery manufacturers using high-nickel cathode chemistries such as NMC 811 and NCA. Having production capacity across both product forms gives Rio Tinto greater commercial flexibility to serve different segments of the battery supply chain.

Capital Allocation Sequencing Across Four Simultaneous Projects

Running four major lithium projects simultaneously creates genuine execution risk, and Rio Tinto's approach to managing it is worth examining. The group has structured capital deployment at approximately $1 billion per year in lithium-specific investment across 2026 to 2028, with project sequencing designed to stagger commissioning milestones rather than creating simultaneous ramp-up demands on management bandwidth.

Sal de Vida and Fenix 1B are designed to reach first production before Rincon's full ramp-up and Bécancour's commissioning begin in earnest, creating a phased progression of operational complexity rather than a single point of maximum execution risk.

Aluminium: Bauxite Disruption in Context

Why a 7% Bauxite Decline Does Not Translate Directly to Aluminium

Bauxite production fell 7% year-on-year in H1 2026 to 28.5 Mt, with Q2 showing a partial recovery. This figure requires careful interpretation. Aluminium production operates through a processing chain: bauxite is refined into alumina, which is then smelted into aluminium metal. Inventory buffers and processing flexibility at intermediate stages mean that a bauxite volume shortfall does not automatically translate into equivalent reductions in finished aluminium output within the same reporting period.

Full-year aluminium guidance remains unchanged, which suggests management has sufficient alumina inventory or processing flexibility to absorb the H1 bauxite shortfall without compromising the annual production target.

AP60 Smelter: Low-Carbon Aluminium Positioning

The Canadian AP60 aluminium smelter expansion represents a significant near-term catalyst for Rio Tinto's aluminium division. AP60 technology is one of the most energy-efficient aluminium smelting processes commercially available, and its Canadian location provides access to hydroelectric power, enabling the production of aluminium with a substantially lower carbon footprint than coal-powered smelters.

This positions Rio Tinto to serve the growing market segment of manufacturers requiring lower-carbon aluminium for automotive and aerospace applications, where supply chain emissions are increasingly subject to customer scrutiny and regulatory frameworks.

The next major ASX story will hit our subscribers first

Guidance Stability as a Credibility Signal

Rio Tinto reaffirmed production and cost guidance across iron ore, copper, aluminium, and lithium following H1 2026 results. In isolation, unchanged guidance is unremarkable. However, in the context of weather disruptions in Argentina, geopolitical uncertainty affecting global supply chains, elevated diesel costs in the Pilbara, and ongoing capital works constraining near-term port capacity, maintaining guidance across all four commodity divisions simultaneously carries a stronger signal.

According to Rio Tinto's first quarter 2026 production results, the group reported only limited operational impacts from broader supply chain disruptions, underscoring its multi-jurisdictional resilience. This structure reduces single-point-of-failure risk in ways that smaller, single-commodity or single-jurisdiction operators cannot replicate.

Portfolio Construction and the Energy Transition Thesis

H1 2026 Commodity Performance at a Glance

| Commodity | H1 2026 Volume | YoY Change | Guidance Status |

|---|---|---|---|

| Iron Ore (sales) | 157.7 Mt | +5% | Unchanged |

| Copper (Oyu Tolgoi) | Significant uplift | +31% | Unchanged |

| Bauxite | 28.5 Mt | -7% | Unchanged |

| Lithium (LCE) | 27,300 mt | +53% | Unchanged (61,000–64,000 mt FY) |

| CuEq (Group) | Composite measure | +3% | Unchanged |

Iron Ore as the Cash Engine Funding Growth

Iron ore remains the dominant earnings contributor, and 157.7 Mt in H1 2026 sales underscores the scale of this position. The strategic function of the Pilbara operation is not simply to grow; it is to generate the free cash flow that funds copper and lithium expansion without excessive balance sheet leverage. This internal capital recycling model is central to Rio Tinto production growth and lithium output, and represents a deliberate portfolio construction choice.

A critical and often underappreciated dynamic is that Oyu Tolgoi's ramp-up, Rincon's commissioning, and Sal de Vida's first production are all expected to converge within the same 24-month window. If copper and lithium pricing conditions remain constructive during this period, the compounding effect of simultaneous volume growth across both future-facing commodities could materially amplify free cash flow generation beyond what the current production trajectory alone would suggest.

Speculative Considerations for Long-Term Investors

Several forward-looking dynamics are worth monitoring, though they involve inherent uncertainty:

- DLE technology scalability: If Rio Tinto's DLE technology performs at commercial scale as it has in pilot phases, it could establish a meaningful cost advantage over competitors relying on conventional evaporation pond production in the Argentine lithium triangle

- Lithium price timing: The 200,000 mt/y target arriving in 2028 coincides with widely anticipated acceleration in battery electric vehicle penetration in major markets. Whether lithium prices recover from current cyclical lows by the time full capacity is online remains a key contingent variable

- Simandou's market impact: The addition of high-grade Simandou iron ore to the seaborne market could alter pricing dynamics for standard-grade Pilbara ore, introducing a nuanced internal competitive tension that investors in Rio Tinto as a pure iron ore story should consider carefully

Furthermore, as noted by market analysts covering the period, Rio Tinto's simultaneous delivery of record iron ore volumes and soaring copper production signals a breadth of operational execution that few global mining peers can match.

Over the 12 months to July 2026, Rio Tinto shares (ASX: RIO) rose approximately 48%, significantly outperforming the S&P/ASX 200 Index, which returned approximately 2% over the same period. Whether this re-rating reflects the market beginning to price in the full value of Rio Tinto production growth and lithium output, or simply responds to commodity price tailwinds, is a question investors should weigh carefully before assuming further multiple expansion.

This article contains general information only and does not constitute financial advice. Past performance is not indicative of future returns. Investors should consider their own circumstances and consult a licensed financial adviser before making investment decisions. Forward-looking statements, production targets, and financial projections referenced in this article are subject to risks, uncertainties, and assumptions that may cause actual outcomes to differ materially from those described.

Want to Catch the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — transforming complex geological data into actionable investment insights for traders and long-term investors alike. Explore how historic discoveries have generated extraordinary returns on the Discovery Alert discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.