June 16, 2026

When One Mine Explosion Reshapes a Global Commodity Market

The global thermal coal market has never operated in isolation from geopolitical shocks, weather cycles, or regulatory upheaval. However, the convergence of events striking simultaneously in mid-2026 is unusual even by historical standards. The China mine disaster and Indonesia coal export policy changes, combined with a war-driven LNG supply crisis and an approaching El Niño weather pattern, have collided to create what analysts describe as the tightest seaborne coal supply environment in years. Understanding how these forces interact requires looking beyond individual headlines and examining the structural fault lines running beneath the global energy supply chain.

When big ASX news breaks, our subscribers know first

The Shanxi Mine Disaster: Local Tragedy, Global Consequences

Shanxi province sits at the geographic and economic heart of China's coal industry. As the country's single largest coal-producing region, disruptions there reverberate through energy markets with a speed and scale that few other geographies can match.

A fatal explosion at a Shanxi mine last month triggered an immediate regulatory response from central authorities, mandating province-wide safety inspections across operating facilities. The pattern is well-established in Chinese mining governance: a high-casualty incident triggers sweeping audit orders, operational suspensions accumulate across the region, and domestic spot availability tightens before the inspection cycle concludes.

How Post-Disaster Safety Inspections Translate Into Supply Tightening

The mechanism connecting a single mine incident to national import demand follows a recognisable sequence:

- Central authorities issue mandatory safety review orders following a confirmed fatality event

- Provincial regulators suspend or restrict output at mines pending compliance audits

- Regional coal production volumes decline during the inspection window

- Domestic spot prices rise as utility buyers compete for reduced available supply

- State-owned power operators and industrial buyers pivot to seaborne imports to compensate

- International benchmark prices respond to the incremental demand signal

This sequence has historical precedent. The February 2023 collapse at the Xinjing Coal Industry open-pit mine in Inner Mongolia's Alxa Left Banner killed 53 people and injured 6 others. Post-incident investigations identified illegal construction practices, reckless subcontracting, and systemic regulatory failures at the local authority level. China's emergency management authorities responded with sector-wide safety inspections and mandatory rectification programs that materially constrained output for months.

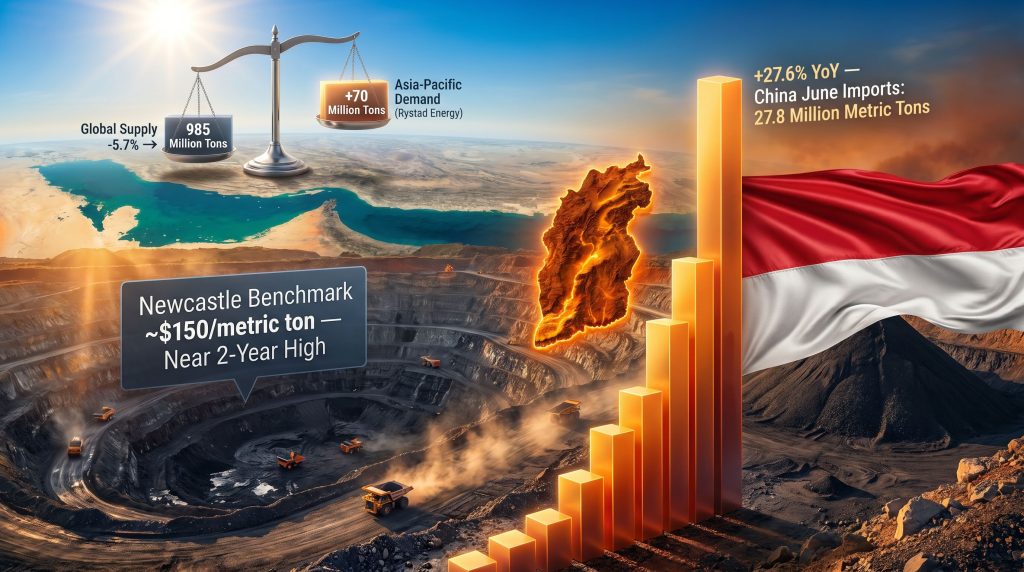

The 2026 Shanxi incident is following the same institutional pattern, but the market context is significantly tighter. According to DBX Commodities CEO Alexandre Claude, China's June 2026 thermal coal imports are forecast to reach 27.8 million metric tons, representing a 27.6% year-on-year increase. That acceleration reflects the exhaustion of the inventory buffer that had previously kept China's import appetite subdued through the first five months of the year.

Key Market Insight: Until May 2026, Chinese utilities were drawing on sufficient domestic inventories and renewable generation output to moderate seaborne purchase volumes. The Shanxi safety-driven output curtailments have effectively depleted that cushion in a matter of weeks, not months.

Indonesia's Export Policy Overhaul: Structural Disruption, Not a Temporary Blip

While the China mine disaster and Indonesia coal export policy changes are being discussed together, the Indonesian side of this equation carries longer-duration structural implications. This is not a short-term administrative adjustment. Furthermore, it represents a fundamental reorientation of how the world's largest thermal coal exporter manages its commodity supply chain. These coal supply challenges are reshaping buyer strategies across the entire Asia-Pacific region.

The Danantara Transition and What It Means for Spot Markets

Indonesia is routing all coal exports through a new state-controlled intermediary, Danantara Sumber Daya Indonesia (DSI). The phased rollout commenced on 1 June 2026, with fuller implementation scheduled progressively through the remainder of the year. Market participants have raised concerns about the lack of operational clarity surrounding the transition, counterparty execution risk, and the impact on the liquidity of spot-market transactions that Asian buyers depend on for baseload power procurement.

Inserting a state entity between private miners and international buyers introduces a layer of bureaucratic friction that spot markets are structurally ill-equipped to absorb. Asian utility buyers, particularly in China and the Indian coal market, have historically relied on the responsiveness of Indonesian spot trading to manage near-term fuel inventory requirements.

The RKAB Quota Reversal: Compressing Planning Horizons

Indonesia previously allowed coal miners to operate under a three-year RKAB (Rencana Kerja dan Anggaran Biaya) quota approval system. This provided medium-term production certainty, enabling investment decisions and export contract commitments on multi-year horizons. The government has reverted to annual approval cycles, consequently altering the planning environment for producers in a fundamental way.

The market impact of this shift is potentially severe. Analysis from McCloskey's executive director Scott Dendy indicates Indonesian thermal coal production was already down 7% year-on-year through the first four months of 2026. If this pace is maintained, full-year exports could fall by approximately 11% to 446 million tons. The shift from three-year to annual RKAB approvals may reduce output by up to 100 million tonnes relative to prior multi-year production targets.

The Full Policy Stack: A Comparative Overview

| Policy Change | Previous Framework | New Framework | Market Impact |

|---|---|---|---|

| Production quotas | 3-year RKAB approvals | Annual approvals | ~100Mt output reduction risk |

| Export routing | Direct private miner exports | State DSI intermediary | Execution uncertainty, delays |

| Export pricing | Spot market / bilateral | HBA domestic benchmark | Pricing friction for Asian buyers |

| Export tax | No price-linked tax | Proposed threshold-triggered tax | Margin compression for producers |

The HBA (Harga Batubara Acuan) domestic reference price, now being applied as an export pricing benchmark, creates particular friction. International spot buyers in China and India typically operate on exchange-based or bilateral pricing mechanisms. Mandating HBA as a price anchor effectively forces foreign buyers to accept an Indonesian domestic price construct rather than market-clearing international prices, a shift that may accelerate procurement diversification toward alternative origins.

Warning for Buyers: The Danantara transition introduces meaningful counterparty uncertainty into what has historically been a relatively fluid spot-market export process. Buyers relying on Indonesian coal for baseload generation face potential delays and pricing unpredictability throughout the transition period.

The Iran War's Cascading Impact on Asian Energy Demand

The disruption of LNG shipping through the Strait of Hormuz by the US-Israeli military campaign against Iran has added a demand shock to what was already a supply-constrained market. Under normal operating conditions, the strait carries approximately one-fifth of global oil and LNG supplies. The broader energy market disruptions caused by this conflict have also intensified interest in the LNG supply implications for long-term contract structures across Northeast Asia.

Japan and South Korea, both structurally dependent on LNG imports for power generation, pivoted rapidly to high-grade thermal coal as a fuel substitute when those LNG flows were interrupted. This demand surge pushed the Newcastle benchmark to near two-year highs above $150 per metric ton, a price level that reflects premium coal purchasing, not the lower-grade Indonesian thermal coal that underpins most regional baseload generation.

Consultancy Rystad Energy estimates the Iran war fallout will drive an additional 70 million metric tons of coal consumption across the Asia-Pacific region in 2026 alone. That demand addition is arriving simultaneously with a projected 5.7% decline in global coal supply to 985 million tons (Argus), creating a supply-demand gap that is arithmetically bullish for prices through the remainder of the year.

A framework agreement between the US and Iran to reopen the Strait of Hormuz has been reached, but officials note that restoring normal shipping volumes will take weeks, and returning to pre-war LNG production levels could take years given infrastructure damage and operational restart timelines.

El Niño: The Demand Amplifier That Could Tip the Balance Further

Peng Qihua, associate professor at Nanjing University's School of Atmospheric Sciences, has highlighted the risk that drought-like conditions in northern China could curtail hydropower output while simultaneously driving higher air-conditioning demand. In Chinese power system economics, reduced hydropower output has a direct substitution effect, pushing coal-fired generation higher to compensate for reduced renewable baseload.

Across Southeast Asia, above-normal temperatures are already driving elevated coal consumption in Vietnam and the Philippines. Thailand faces tighter domestic gas supplies, which market participants including Vasudev Pamnani, director at India-based I-Energy Resources, expect to translate into higher coal import volumes through 2026.

The dual effect of El Niño is particularly difficult for markets to absorb in the current environment. It simultaneously raises demand through heat-driven electricity consumption and suppresses one of the key alternatives to thermal coal by reducing hydroelectric availability.

Alternative Suppliers: Can Anyone Fill the Indonesian Gap?

The structural constraints facing every meaningful alternative supplier suggest there is no straightforward substitution path for the volumes Indonesia is failing to deliver. For a more detailed look at the latest coal price update trends, the broader pricing dynamics across competing origins are worth examining alongside supply availability.

| Origin | Export Trend | Key Constraint | Primary Buyer Markets |

|---|---|---|---|

| Indonesia | Declining (~-11% in 2026) | Policy uncertainty, DSI transition | China, India, Southeast Asia |

| Russia | Declining | Loss-making producers, rouble strength | Asia, Europe |

| Australia | Rising (modest) | Higher costs, diesel restrictions | Japan, South Korea, India |

| South Africa | Rising interest | Vessel clearance timing volatility | India |

Russia, the world's third-largest coal exporter, is facing an acute economics problem. Approximately two-thirds of Russian coal producers are currently operating at a loss, driven by a strengthened rouble and rising domestic transportation costs. Output is declining, not growing.

Australia offers more promise, with exports expected to increase modestly in 2026, but higher mining costs and restricted diesel supply are constraining the pace of that growth. South Africa is drawing increasing interest from Indian buyers diversifying away from uncertain Indonesian supply, but irregular vessel clearances and shipment timing volatility limit near-term reliability.

The next major ASX story will hit our subscribers first

Near-Term Price Outlook: Three Scenarios for the Second Half of 2026

The convergence of the China mine disaster and Indonesia coal export policy changes, alongside Iran war demand additions and El Niño risk, creates a market environment where upside price scenarios appear more probable than downside ones in the near term. DBX Commodities has noted that with demand firm and supply constrained, near-term price risk is skewed to the upside.

| Scenario | Key Assumption | Price Implication |

|---|---|---|

| Base Case | Hormuz partially reopens; Shanxi inspections wind down in Q3 | Prices moderate from peak but remain elevated above $130/t |

| Bull Case | El Niño intensifies; DSI transition causes prolonged export delays | Newcastle benchmark tests $170-$180/t range |

| Bear Case | LNG supply fully restored; China demand softens on economic slowdown | Prices retreat toward $110-$120/t by Q4 2026 |

Disclaimer: The above scenarios are analytical projections based on publicly available market data and analyst commentary. They do not constitute financial advice. Commodity price forecasts carry significant inherent uncertainty and may differ materially from actual outcomes.

Key Market Metrics at a Glance

| Metric | Value / Estimate | Source |

|---|---|---|

| Newcastle benchmark price | ~$150/metric ton (near 2-year high) | Iran war LNG tightness |

| China June thermal coal imports (forecast) | 27.8 million metric tons | DBX Commodities |

| China June import growth (year-on-year) | +27.6% | DBX Commodities |

| Indonesia thermal coal production decline (Jan-Apr 2026) | -7% year-on-year | McCloskey |

| Projected Indonesian export decline (full year 2026) | ~11% to 446 million tons | McCloskey |

| Global coal supply decline forecast (2026) | -5.7% to 985 million tons | Argus |

| Additional Asia-Pacific coal consumption (Iran war impact) | +70 million tons in 2026 | Rystad Energy |

Frequently Asked Questions

What caused the coal supply disruption in Shanxi province?

A fatal explosion at a Shanxi coal mine triggered mandatory province-wide safety inspections ordered by central authorities. The resulting operational suspensions and output restrictions tightened domestic coal supply, pushing Chinese utilities and industrial buyers toward seaborne imports to compensate.

What is Danantara and how does it affect Indonesia's coal exports?

Danantara Sumber Daya Indonesia (DSI) is a new state-controlled entity through which the Indonesian government intends to route all coal exports. The phased rollout began in June 2026. Traders have raised concerns about operational clarity, counterparty risk, and the impact on spot market liquidity for Asian buyers.

How much could Indonesian coal exports decline in 2026?

Based on production tracking through April 2026, exports could fall by approximately 11% to 446 million tons for the full year, according to McCloskey analysis. The shift from three-year RKAB quotas to annual approvals may further reduce output by up to 100 million tonnes relative to prior planning targets.

How does El Niño affect coal demand?

An approaching El Niño is expected to reduce hydropower output in northern China through drought conditions while simultaneously driving higher air-conditioning electricity demand. Across Southeast Asia, elevated temperatures are already increasing coal-fired generation. Both effects add further demand pressure to an already constrained seaborne market.

Could South Africa replace Indonesian coal supply for Indian buyers?

South Africa is attracting growing procurement interest from Indian buyers seeking alternatives to uncertain Indonesian supply. However, analysts flag irregular vessel clearances and shipment timing volatility as near-term constraints on the reliability and scale of South African exports as a genuine substitute.

Want To Capitalise on the Next Major Commodity Supply Shock?

Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements to identify high-potential mineral discoveries across 30+ commodities — including coal and energy — delivering real-time, actionable alerts to subscribers before the broader market reacts. Explore historic discovery returns on Discovery Alert's discoveries page and begin your 14-day free trial to position yourself ahead of the next major market-moving event.