June 24, 2026

The Hidden Architecture of Mineral Power: How Critical Resources Became Geopolitical Leverage

For decades, the assumption underpinning global industrial supply chains was relatively straightforward: commodities flow where economics dictate, and trade partners with mutual dependencies rarely weaponise those relationships. That assumption has now been systematically dismantled. The China mineral export curbs to Japan that have unfolded since late 2025 represent something more consequential than a bilateral trade dispute. They reveal a structural shift in how resource-rich nations exercise geopolitical influence in a world increasingly defined by the materials that power advanced technology.

Understanding this shift requires looking beyond the immediate diplomatic friction between Beijing and Tokyo and examining the deeper architecture of mineral dependency that makes such leverage possible in the first place. Indeed, rare earth supply chains have long been more fragile than most policymakers were willing to acknowledge.

When big ASX news breaks, our subscribers know first

Beyond Tariffs: Why Export Controls Have Become Beijing's Preferred Instrument

Traditional trade conflict relied on tariffs and import restrictions. The new paradigm operates differently. Export controls on critical minerals are surgical where tariffs are blunt. They can be tightened or loosened with precision, applied selectively to intermediate processing forms while allowing refined metals to continue flowing, and calibrated to inflict industrial pain without triggering the kind of broad economic rupture that draws international condemnation or military responses.

China's approach to Japan follows this logic almost perfectly. Rather than announcing a sweeping embargo, Beijing has engineered a slowdown that is measurable, damaging, and yet technically deniable as anything other than routine regulatory administration. The dual-use licensing framework, which now covers approximately 1,100 categories of items requiring export permits for international shipment from China, provides the legal scaffolding for precisely this kind of selective pressure.

What makes this instrument particularly powerful is its scalability. The same architecture that is currently being applied to Japan can, in principle, be directed at any trading partner that challenges Beijing's core interests. South Korea, Germany, and the United States are all observing this situation with considerable attention. Furthermore, China's rare earth export restrictions have already demonstrated their capacity to reshape entire industrial ecosystems far beyond the bilateral relationship in which they originate.

What Minerals Are Being Restricted, and Why Does It Matter?

The specific materials targeted by China's export restrictions are not arbitrary. Each one occupies a structurally irreplaceable position in Japan's industrial ecosystem.

| Mineral | Primary Industrial Use in Japan | Export Status (2026) | China's Global Market Share |

|---|---|---|---|

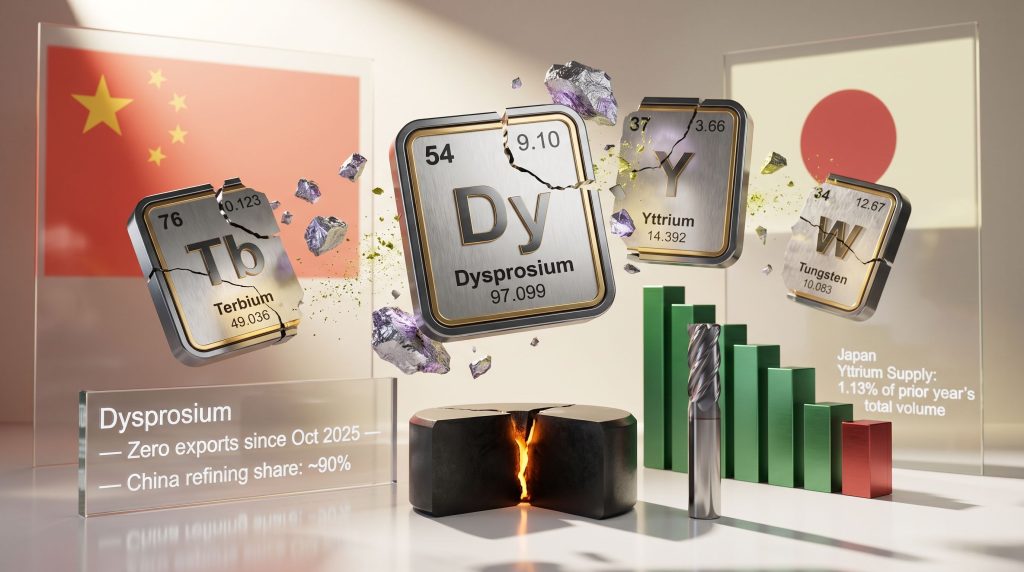

| Dysprosium | High-performance EV magnets | Zero since October 2025 | ~90% of refining |

| Terbium | High-performance EV magnets | Zero since October 2025 | ~90% of refining |

| Yttrium | LED screens, semiconductor equipment | 1.13% of prior year's volume | Dominant supplier |

| Tungsten (intermediate) | Precision automotive tooling | Zero since January 2026 | Major global producer |

| Heavy Rare Earth Chemicals | Military-grade manufacturing | Lowest 3-month volume since 2023 | ~95% of magnet production |

| Samarium | Defence and industrial magnets | Subject to dual-use controls | Significant share |

| Gallium and Germanium | Semiconductors, electronics | Dropped to zero in early 2026 | Leading global producer |

Tungsten: The Quiet Threat to Automotive Manufacturing

Tungsten rarely attracts the same headlines as lithium or cobalt, but its industrial role is foundational. Tungsten carbide is the material of choice for precision cutting tools used throughout automotive manufacturing. There is no near-term commercial substitute that matches its hardness and thermal resistance properties at scale.

Intermediate tungsten exports from China to Japan fell to zero in January 2026 and have not recovered. This matters enormously because Japan's automotive sector contributes approximately 10% of total national GDP, according to reporting in the Japan Times. A sustained interruption to tungsten supply is not an abstraction. It is a direct constraint on the physical capacity of Japanese factories to produce vehicle components.

The NdFeB Magnet Problem and EV Supply Chain Exposure

Dysprosium and terbium occupy a uniquely critical position in the electric vehicle transition. Both elements are essential additives in neodymium-iron-boron (NdFeB) permanent magnets, the technology that powers electric motors in virtually every modern EV platform. Without dysprosium in particular, NdFeB magnets lose their thermal stability at operating temperatures, making them unsuitable for automotive applications.

China controls approximately 95% of global permanent magnet production, according to the International Energy Agency. Exports of both dysprosium and terbium to Japan have been at zero since October 2025. The timing is notable: the final recorded shipments occurred just before Japanese Prime Minister Sanae Takaichi made her remarks on Taiwan in November 2025.

A lesser-known dimension of this vulnerability is that NdFeB magnet grades are not uniform. The dysprosium content in a magnet designed for EV traction motors, which must operate across extreme temperature ranges, is significantly higher than in consumer electronics applications. Japan's automotive magnet manufacturers require the highest-grade heavy rare earth inputs, and these are precisely the materials for which alternative sourcing is most difficult to establish quickly.

Yttrium and the Semiconductor Equipment Dimension

Yttrium's role extends into a sector that is often overlooked in discussions of rare earth dependency: semiconductor fabrication equipment. Yttrium-based ceramics are used in plasma-resistant chamber components inside the advanced equipment that manufactures chips. With yttrium exports to Japan currently running at just 1.13% of the prior year's total volume, the implications extend well beyond LED screens into the core infrastructure of chip production itself.

The Political Trigger: A Timeline of Diplomatic Deterioration

The sequence of events that produced the current China mineral export curbs to Japan follows a traceable escalation path.

| Date | Event |

|---|---|

| November 2025 | PM Takaichi makes public remarks suggesting potential Japanese military involvement in a hypothetical Taiwan conflict |

| October 2025 | Final recorded exports of dysprosium and terbium to Japan |

| January 2026 | China tightens dual-use export controls; intermediate tungsten flows to Japan reach zero |

| Early 2026 | Gallium and germanium exports to Japan drop to zero |

| May 2026 | Magnet-related exports hit their lowest monthly level since May 2025 |

| June 2026 | 20 Japanese entities formally banned from dual-use exports; 20 more placed on a secondary watch list |

Beijing's Commerce Ministry framed the restrictions in terms of concerns about Japan's alleged remilitarisation and what it characterised as nuclear aspirations, providing a legal basis under the dual-use licensing regime. The targeted Japanese entities include divisions of Mitsubishi Heavy Industries in aerospace and shipbuilding, with Subaru Corp and Mitsubishi Materials Corp appearing on a secondary watch list.

The Calibration Logic: Pain Without Escalation

One of the more analytically important features of the current restrictions is what they deliberately exclude. Light rare earths, which are not subject to China's export control regime, continue to flow to Japan without significant disruption. Tungsten in refined metal form has continued at reduced but non-zero levels. This selective architecture is not accidental.

By targeting intermediate processing forms rather than imposing a total embargo, Beijing is able to maximise industrial disruption for Japanese manufacturers who depend on specific feedstock forms, while maintaining plausible deniability about the intent and avoiding the kind of categorical action that triggered significant international backlash in 2010. The restrictions are calibrated, in the assessment of Bloomberg News reporting, to inflict targeted pain without reaching the threshold that would provoke a direct US response.

How Exposed Is Japan? The Depth of Structural Dependency

Japan's vulnerability to these restrictions is real, but it exists within a historical context that is often misrepresented. The 2010 rare earth embargo prompted more than a decade of diversification efforts. Those efforts were meaningful but insufficient.

| Dimension | 2010 Crisis | 2026 Restrictions |

|---|---|---|

| Trigger | Territorial dispute (Senkaku/Diaoyu Islands) | Taiwan-related political remarks |

| Scope | Near-total rare earth embargo | Targeted intermediate forms and dual-use items |

| China's Refining Share | ~95% | ~90-95% |

| Japan's China Dependency | ~90% of imports | ~60-70% of imports |

| Japan's Recycling Capacity | Early-stage | Significantly more advanced |

| Diplomatic Channel Status | Eventually resolved | Currently near-standstill |

The reduction in China dependency from roughly 90% to 60-70% of imports represents genuine progress. However, the IEA's data reveals why this progress is structurally insufficient: China's dominance is not primarily a function of mining output. It derives from control of refining and processing capacity. Even minerals extracted in Australia, Canada, or Africa frequently require Chinese processing before they can be used in advanced manufacturing. Geographic diversification of mining sources alone does not solve this problem. This reality has fundamentally reshaped how nations think about critical minerals demand and the long-term infrastructure investments required to address it.

How Japanese Companies Are Responding

Japanese industrial firms are not passive recipients of this supply shock. Several adaptive strategies are being deployed simultaneously, though each carries significant limitations.

The Recycling Pivot

The most structurally significant corporate response has been an accelerated pivot toward recycled feedstock. Mitsubishi Materials Corp has raised its reliance on recycled material to approximately 70%, with a publicly stated goal of reaching 100% by 2030. This trajectory was first established in the wake of the 2010 crisis and has since evolved from a contingency measure into a core strategic commitment.

Sumitomo Electric Industries, one of Japan's largest tungsten buyers, has similarly advanced its recycling infrastructure. The company's chairman and CEO Masayoshi Matsumoto communicated clearly at an industry exhibition in Beijing in June 2026 that the firm currently operates two dedicated recycling facilities globally and has substantially improved its recycling technology over recent years. His comments also underscored the severity of the situation, noting that a prolonged shutout from Chinese supply would create serious problems for Japanese manufacturing broadly.

Stockpile Management: A Buffer With an Unknown Horizon

Firms across affected sectors have been drawing down existing mineral inventories to maintain production continuity. This is a rational short-term response but carries an inherent limitation: stockpiles are finite. The duration of current reserves across affected industries has not been publicly disclosed, which represents one of the most significant uncertainties in assessing how much time Japan's industrial base actually has before production constraints become acute.

The opacity around stockpile duration is itself a strategic variable. Companies have limited incentive to disclose remaining inventory levels publicly, as doing so could accelerate price movements in substitute materials or signal vulnerability to trading partners.

Industry Diplomacy at the Commercial Level

With formal government-to-government channels frozen, Japanese industry has been pursuing parallel commercial dialogue. The Japan Chamber of Commerce and Industry dispatched a delegation to the China International Supply Chain Expo in Beijing in June 2026. Liberal Democratic Party member Gaku Hashimoto attended the same event through a separate group. These missions represent an attempt to maintain supplier relationships and gather intelligence on the direction of Chinese policy through back-channel commercial contact.

The next major ASX story will hit our subscribers first

Japan's Government Response: Policy Frameworks and Diplomatic Dead Ends

At the policy level, Japan's response has centred on alignment with multilateral frameworks rather than unilateral action. Tokyo has joined a Group of Seven commitment to ensure no single country supplies more than 60% of rare earth inputs to member economies by 2030. Japanese Finance Minister Satsuki Katayama has confirmed that recycling incentives, price floor mechanisms, and trade diversification measures are all under active consideration.

The diplomatic picture is considerably more constrained. Japan's ambassador to China has made repeated requests for meetings with Chinese Foreign Ministry officials throughout 2026, all without success. Prime Minister Takaichi has publicly signalled openness to dialogue at multiple levels, but has been unwilling to retract her Taiwan remarks, which Beijing has made a precondition for substantive engagement.

A potential bilateral meeting between Prime Minister Takaichi and President Xi at the Asia-Pacific Economic Cooperation forum in Shenzhen in November 2026 has been discussed. However, reporting from Reuters indicates that Takaichi has been reluctant to pursue such a meeting due to frustrations over personal attacks directed at her by China. Whether Beijing would agree to such a meeting is also uncertain. This potential APEC encounter represents the most credible near-term diplomatic off-ramp currently visible.

The Broader Geopolitical Signal: What the Rest of the World Is Reading

The implications of China mineral export curbs to Japan extend far beyond the bilateral relationship. Several dynamics are worth examining carefully.

The Dual-Use Architecture as a Scalable Template

China's export licensing regime for dual-use items provides a replicable framework that can be applied to any trading partner at any level of intensity. The ~1,100 item category list creates enormous administrative flexibility. Flows can be tightened through licence denial rates, slowed through extended processing times, or suspended selectively for specific industrial categories. This is a more sophisticated instrument than either tariffs or embargoes, and its scalability makes it a persistent structural risk for any nation dependent on Chinese mineral processing.

The Processing Bottleneck Problem

Nations accelerating diversification away from Chinese mineral supply are confronting a consistent structural barrier: the absence of sufficient refining and processing capacity outside China. The IEA has assessed that China controls above 90% of the global rare earth refining process. Building alternative processing infrastructure requires capital, permitting timelines, technical expertise, and feedstock access, none of which can be assembled quickly.

This is why investment in allied-nation processing capacity across Australia, Canada, and Europe is increasingly framed not as a commercial opportunity but as a national security imperative. Moreover, a coherent critical minerals strategy at the national level must address processing infrastructure, not merely mining output. Mining diversification without processing diversification is an incomplete solution that leaves supply chains structurally exposed at the midstream stage.

Industries Facing the Most Acute Risk

- Automotive manufacturing: Simultaneous exposure to tungsten-dependent precision tooling shortfalls and EV magnet supply interruptions

- Electronics and displays: Yttrium shortfall cascading into LED production and semiconductor fabrication equipment supply

- Defence and aerospace: Heavy rare earth restrictions directly constraining military-critical minerals manufacturing capacity

- Clean energy: Permanent magnet shortages feeding through into wind turbine and EV drivetrain supply chains

Key Takeaways for Investors and Industry Observers

The situation unfolding between China and Japan contains several insights that apply well beyond this specific bilateral relationship.

-

Processing capacity is the critical chokepoint. Nations and companies that control refining infrastructure hold strategic leverage that raw material access alone cannot replicate.

-

Recycling is not a short-term fix. It is a multi-year infrastructure investment with genuine long-term value, but it cannot bridge immediate supply gaps at the speed current disruptions demand.

-

Diplomatic timelines are unpredictable. The APEC November 2026 window is the clearest near-term resolution pathway, but its outcome is genuinely uncertain and should not be assumed in any supply planning scenario.

-

Light rare earths and heavy rare earths carry different risk profiles. The current restrictions are concentrated on heavy rare earths and specific intermediate processing forms. This distinction matters significantly for downstream manufacturers and investors assessing exposure.

-

The precedent effect is real. Every nation with significant Chinese mineral processing dependency is stress-testing its own supply chain resilience against the Japan scenario. The investments and policy frameworks that follow will reshape global mineral markets over the next decade.

Disclaimer: This article contains forward-looking assessments, diplomatic projections, and market analysis that involve inherent uncertainty. Information is drawn from publicly available sources including Bloomberg News reporting dated June 23, 2026, and International Energy Agency assessments on rare earth supply chain risks. Nothing in this article constitutes investment advice. Readers should conduct independent research before making any investment or commercial decisions based on the information presented here.

Want to Track the ASX Companies Positioned at the Forefront of Critical Minerals Processing?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX, turning complex geological data into actionable investment insights — precisely the kind of early intelligence that matters as global supply chains scramble to build processing capacity outside China. Start your 14-day free trial at Discovery Alert today, or explore how historic mineral discoveries have generated substantial returns for those positioned ahead of the market.