June 23, 2026

The Global Zinc Market Is Being Redrawn From the Inside Out

Commodity markets rarely shift direction without warning. In zinc, the signals have been building for more than a year: a widening divergence between international and domestic Chinese prices, a rapid compression of net import volumes, and a wave of new smelting capacity entering production at exactly the moment when downstream demand in China has stalled. Together, these forces are pointing toward something that has happened only once in the past fourteen years: China transitioning from the world's largest net importer of refined zinc to a China net refined zinc exporter.

Understanding why this matters requires more than reading the trade statistics. It demands an appreciation of how zinc moves through the global supply chain, what drives the arbitrage calculus between the London Metal Exchange and the Shanghai Futures Exchange, and why the structure of Chinese smelting investment has created a supply-push dynamic that domestic consumption alone cannot resolve. Furthermore, these commodity price impacts extend well beyond China's borders.

When big ASX news breaks, our subscribers know first

From Dominant Consumer to Potential Supplier: China's Shifting Zinc Trade Identity

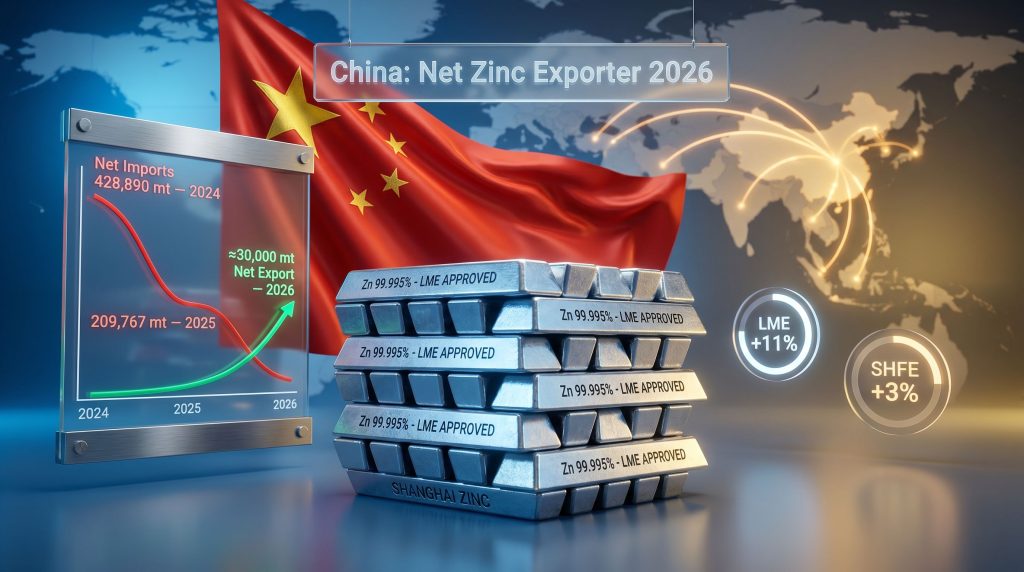

For the better part of two decades, China's role in global zinc markets followed a consistent logic. The country accounts for roughly half of annual global refined zinc production, yet its voracious domestic appetite, anchored in the galvanized steel requirements of its construction and infrastructure sectors, reliably absorbed that output and then some. The result was a persistent net import position that peaked at 428,890 metric tons in 2024 before declining sharply to 209,767 metric tons in 2025.

That two-year decline in net import volumes is not noise. It reflects a fundamental recalibration of the supply-demand balance within China's zinc economy. New smelting capacity, much of it commissioned in late 2025 and continuing into 2026, is adding refined output at a rate that domestic consumption growth simply cannot match.

| Year | China Net Zinc Trade Position | Volume (metric tons) |

|---|---|---|

| 2024 | Net Importer | 428,890 |

| 2025 | Net Importer | 209,767 |

| Jan–Apr 2026 | Net Importer (Cumulative) | 34,500 |

| 2026 Full Year (Forecast) | Net Exporter (Projected) | ~30,000 |

Alice Fox, commodities strategist at Macquarie Group, projects that China will record net refined zinc exports of approximately 30,000 metric tons across 2026 as a whole, marking the first such shift in four years. The directional momentum is already visible in the monthly trade data: net imports for the January to April 2026 period fell approximately 62% compared with the same interval in 2025, based on Reuters calculations of Chinese customs data.

The 2022 Episode: A Precedent Worth Studying Carefully

China's brief transition to net exporter status in 2022 offers a critical reference point, though one that demands careful interpretation. That episode was triggered primarily by an external shock: mass smelter curtailments across Europe, driven by an unprecedented surge in energy costs that made zinc smelting in many Western facilities economically unviable. Chinese producers, insulated from those energy cost pressures and sitting on adequate domestic supply, stepped into the gap.

The window closed relatively quickly. As European energy costs moderated and demand conditions normalised, the arbitrage opportunity evaporated and Chinese exports tapered back toward zero. By mid-2024, China was once again a substantial net importer.

The 2026 scenario differs in an important structural respect. The current domestic surplus is not primarily a function of temporarily weak demand, as was partly the case in 2022. It is being driven by new installed smelting capacity that will not disappear when demand recovers. This distinction matters for assessing the durability of any export window that opens in the second half of 2026.

"The 2022 episode demonstrated that China has the latent export capacity to supply international markets at scale. The 2026 dynamic, built on new infrastructure rather than temporary demand suppression, has a more structural foundation, though it remains vulnerable to the same self-correcting arbitrage forces that closed the previous window."

Supply Growth Outpacing Demand: The Arithmetic Behind the Surplus

The core mechanism driving China's emerging zinc surplus is straightforward in arithmetic terms, even if its implications are far-reaching. Macquarie Group's analysis forecasts domestic refined zinc supply growth of 4.2% in 2026, against demand growth of only 1%. This differential, sustained across a market of China's scale, translates into a meaningful and growing inventory overhang within the domestic system.

Several interconnected factors explain why demand growth has been so constrained:

-

Property sector stagnation: Galvanized steel, which consumes the largest share of refined zinc through the hot-dip galvanizing process used to protect structural steel from corrosion, is directly tied to construction activity. China's property sector has been in a prolonged contraction since 2021, with residential construction starts and completions well below pre-downturn levels.

-

Infrastructure spending limitations: While public infrastructure investment has partially offset the property sector drag, it has not been sufficient to absorb the additional zinc supply entering the market from new smelter capacity.

-

Consumer durables softness: Beyond construction, zinc is also consumed in die-casting applications for the automotive and consumer electronics sectors. Both have faced headwinds from subdued domestic consumption confidence.

The galvanizing industry deserves particular attention here. Hot-dip galvanizing involves immersing steel components in a bath of molten zinc at approximately 450 degrees Celsius, bonding a protective zinc-iron alloy layer to the surface. The process is highly zinc-intensive, and its demand profile tracks construction starts with a lag of roughly six to eighteen months. Consequently, the China steel market outlook for this period directly shapes galvanizing demand flowing through that lag. With Chinese property starts having contracted sharply, the pipeline of demand is structurally reduced.

Geopolitical Disruption and the Ex-China Supply Squeeze

The domestic Chinese surplus alone would not be sufficient to generate an export flow if international markets were adequately supplied. What has created the export opportunity is a simultaneous tightening on the ex-China supply side, arising from a convergence of industrial accidents, concentrate supply constraints, and elevated energy costs.

Production suspensions and operational scale-downs at zinc smelting facilities in Peru and Kazakhstan, both attributable to industrial accidents, have removed meaningful refined zinc tonnage from the non-Chinese supply pool. These are not minor disruptions: Peru and Kazakhstan are both significant contributors to global zinc smelting capacity, and unplanned outages in either country register in global inventory and price dynamics.

Compounding the smelter-level disruptions, the broader geopolitical environment — including elevated energy costs stemming from conflict in the Middle East — has raised the operating cost base for energy-intensive smelters in affected regions. Higher energy input costs either reduce output margins to the point where curtailment becomes rational, or they feed through directly into production cost structures that constrain new investment. Indeed, supply chain disruptions of this nature have become an increasingly persistent feature of commodity markets in recent years.

Zinc concentrate supply, the raw material feedstock from which refined metal is smelted, has also tightened in global markets. The treatment charge — which is the fee that mine operators pay smelters to process concentrate into refined zinc — has been under sustained downward pressure, reflecting the competitive environment for feedstock. For smelters outside China operating with already-elevated energy costs, tighter concentrate supply and lower treatment charges create a dual margin squeeze.

The LME-SHFE Price Spread: Reading the Arbitrage Signal

For zinc traders and market analysts, the divergence between LME and SHFE zinc prices is the most immediate indicator of whether the conditions for Chinese exports are genuinely present. As of late May 2026, the LME global benchmark had gained approximately 11% year-to-date, while the most-traded SHFE zinc contract had risen only around 3% over the same period.

| Exchange | YTD Price Performance (to May 2026) |

|---|---|

| London Metal Exchange (LME) | +11% |

| Shanghai Futures Exchange (SHFE) | +3% |

| Implied Arbitrage Spread | ~8 percentage points |

This roughly 8 percentage point divergence is the price signal that incentivises Chinese smelters and trading houses to redirect metal toward export markets. When international prices rise significantly faster than domestic benchmarks, the economics of exporting become increasingly attractive relative to selling into the domestic market, even after accounting for shipping costs, export logistics, and any applicable trade frictions.

The arbitrage is inherently self-correcting. If Chinese exports materialise at scale, additional supply entering international markets will exert downward pressure on the LME price, while simultaneous domestic inventory reduction in China may support the SHFE price. The spread compresses, and the export incentive diminishes. This dynamic is a characteristic feature of commodity market volatility and is why the timing and volume of any export surge will be constrained by market feedback mechanisms.

The next major ASX story will hit our subscribers first

Current Trade Data: Transition Still in Progress

Through the first four months of 2026, China remained a net importer of refined zinc, recording cumulative net imports of approximately 34,500 metric tons. In April specifically, refined zinc exports reached 3,900 metric tons while imports maintained the country's net import position at roughly 2,000 metric tons for the month. The gap is narrowing rapidly.

CRU Group's principal zinc analyst has indicated that China likely reached near self-sufficiency in refined metal by the end of 2025 and is expected to remain in surplus while the rest of the world operates in deficit throughout 2026. The transition to net exporter status is considered most likely to occur in the third or fourth quarter of 2026, when seasonal smelter output patterns and the cumulative effect of capacity ramp-up align with the sustained international price premium.

Risk Factors That Could Alter the Trajectory

Any forecast of this nature carries material uncertainty. Several scenarios could delay, reduce, or reverse the projected transition:

| Risk Factor | Direction of Impact | Probability Assessment |

|---|---|---|

| Prolonged Middle East conflict | Suppresses global demand; narrows export window | Moderate |

| China property sector recovery | Absorbs domestic surplus; reduces exports | Low-to-Moderate (near term) |

| Ex-China smelter restarts | Reduces international price premium | Moderate |

| New Chinese capacity commissioning delays | Slows surplus accumulation | Low |

CRU Group analysis notes that if the conflict in the Middle East extends further, the resulting global demand destruction from persistently high energy prices could erode the very international price premium that makes Chinese exports economically viable. This is a particularly nuanced risk: the same geopolitical forces that have tightened ex-China supply could, if they escalate further, undermine the demand side of the equation sufficiently to close the arbitrage window from the opposite direction.

A faster-than-anticipated recovery in Chinese real estate activity would also fundamentally alter the calculus. Even a partial restoration of pre-2022 construction momentum would accelerate domestic zinc absorption, potentially consuming the projected surplus before it can be directed toward international markets. Given the scale of China's property sector relative to total zinc demand, even modest upside in construction activity carries significant implications for the domestic supply balance.

What a Net Export Position Means for Global Zinc Markets

If China does transition to a China net refined zinc exporter in the second half of 2026, the consequences for global market dynamics would extend beyond the headline trade flow statistics:

-

LME pricing pressure: Incremental Chinese supply entering international markets would apply downward pressure on the LME benchmark, compressing the arbitrage spread that triggered the export flow and potentially capping the current price rally.

-

Regional supply relief: Steel galvanizers and zinc-consuming manufacturers in Southeast Asia, South Asia, and potentially parts of Europe would likely see improved metal availability. Given logistics economics, Southeast and South Asian markets are the natural primary destinations for Chinese refined zinc exports.

-

Smelting economics outside China: A sustained period of Chinese export competition would intensify margin pressure for non-Chinese smelters, particularly those already operating with elevated energy costs. This could paradoxically lead to further curtailments in ex-China smelting capacity, partially offsetting the supply relief that Chinese exports provide.

-

LME warehouse inventory dynamics: Any meaningful increase in Chinese zinc exports directed at LME warrant metal would show up as rising LME warehouse stocks, a metric that commodity traders monitor closely as a leading indicator of forward price direction.

Frequently Asked Questions

Has China ever held net refined zinc exporter status before?

China briefly became a net refined zinc exporter in 2022, the only occurrence in approximately the previous fourteen years. Prior to that episode, China had been a consistent net importer since roughly 2008, a reflection of the scale of its domestic construction and galvanized steel industries relative to smelting output. For broader context on how these dynamics have evolved, global zinc production trends over recent years illustrate the underlying structural shifts at play.

What is the 2026 net zinc trade forecast for China?

Macquarie Group's commodities strategy team projects China will record net refined zinc exports of approximately 30,000 metric tons in 2026, compared with net imports of 209,767 metric tons in 2025 and 428,890 metric tons in 2024. However, as Reuters reports on China's zinc trade shifts note, this transition remains subject to significant market variables.

Why is supply growing faster than demand within China?

New smelting capacity commissioned across 2025 and 2026 is expanding domestic refined zinc output at approximately 4.2% annually, while demand growth is constrained to around 1% by persistent weakness in the property construction sector, the dominant end-use market for galvanized steel.

What is behind the higher zinc prices outside China?

A combination of unplanned smelter curtailments in Peru and Kazakhstan, tightening zinc concentrate availability, and elevated energy costs in key producing regions has created a supply deficit in ex-China markets. Furthermore, analysis from SMM on China's refined zinc export momentum highlights how these dynamics have been building across successive months, pushing the LME zinc benchmark up approximately 11% year-to-date as of late May 2026.

When is the net exporter transition expected to occur?

Market analysts point to the third or fourth quarter of 2026 as the most likely window for the transition, contingent on the continued persistence of the LME-SHFE price spread and the absence of significant disruptions to China's domestic surplus trajectory.

Structural Inflection or Temporary Window: The Verdict Is Still Open

The convergence of domestic oversupply, subdued Chinese consumption growth, international smelter disruptions, and a widening price arbitrage spread creates a more structurally grounded basis for a Chinese zinc export episode in 2026 than the 2022 precedent. The critical difference is that the current surplus originates from new installed capacity rather than a temporary demand suppression, giving it a longer potential duration.

However, the transition remains conditional. The self-correcting nature of commodity arbitrage, the ever-present possibility of a Chinese property sector recovery, and the geopolitical risks that simultaneously tighten supply and threaten demand all represent live variables that could alter the outcome materially.

For commodity market participants, the Q3 2026 trade data will serve as the first definitive test of whether China's emergence as a China net refined zinc exporter is materialising as forecast, or whether this structural inflection point will, like 2022 before it, prove more fleeting than the underlying fundamentals suggest.

This article draws on publicly available analysis from Macquarie Group and CRU Group as reported by Reuters on 25 May 2026, and Chinese customs data as compiled by Reuters. Forecasts and projections referenced herein are those of third-party analysts and do not constitute financial advice. Commodity markets involve significant uncertainty, and actual outcomes may differ materially from any projection discussed.

Want to Position Yourself Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex commodity data across more than 30 minerals into clear, actionable insights — so subscribers can identify high-potential opportunities the moment they emerge. Explore how major mineral discoveries have historically generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to gain a market-leading edge.