May 22, 2026

China Northern Rare Earth strategic control represents a fundamental shift in how nations approach resource security within the rare earth sector. The transformation of global supply chain architectures reveals operational frameworks that increasingly reflect geopolitical priorities rather than pure market mechanisms. These developments signal a departure from traditional commodity trading models toward integrated control systems designed for sustained competitive advantage. Strategic positioning within critical mineral markets now requires understanding both technical capabilities and institutional frameworks that govern access, processing, and distribution.

The evolution of China Northern Rare Earth strategic control represents a comprehensive approach to market dominance that extends far beyond conventional business operations. Furthermore, these strategic developments intersect with broader China export controls that impact global supply chains and market dynamics.

What Defines China Northern Rare Earth's Strategic Market Position?

Corporate Structure and Ownership Framework

The institutional architecture of China Northern Rare Earth Group reflects deliberate design choices that prioritize strategic control over short-term profitability maximisation. As a state-owned enterprise, the organisation operates within governance structures that enable rapid resource allocation and coordinated decision-making across multiple operational domains.

This ownership model facilitates vertical integration spanning extraction, processing, and downstream manufacturing capabilities. The centralised control mechanisms enable synchronised responses to market conditions while maintaining operational security protocols that protect proprietary methodologies and customer relationships.

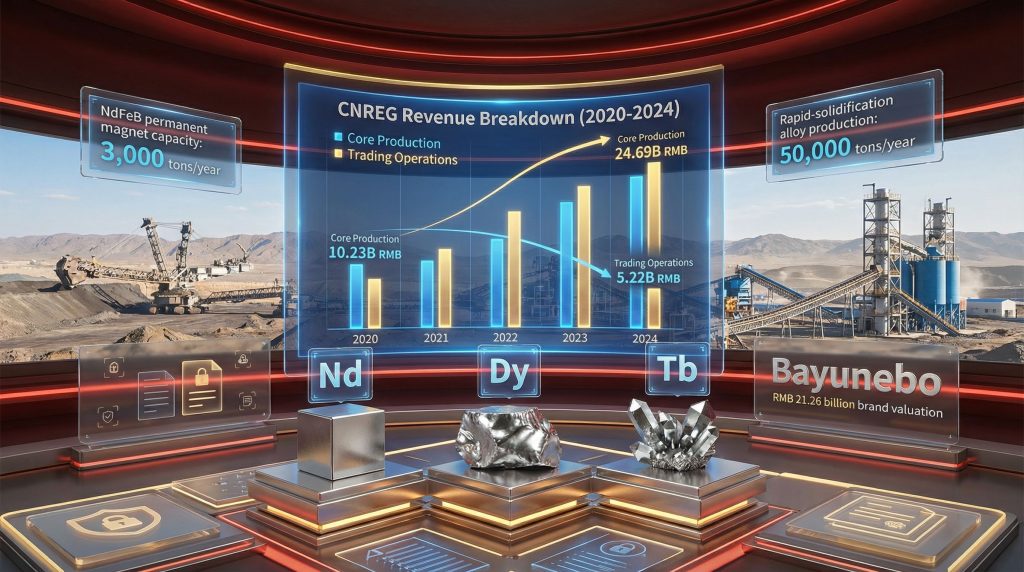

Through Q3 2025, the company reported revenues of RMB 30.29 billion (approximately $4.2 billion USD) with profits reaching RMB 2.58 billion ($360 million USD), demonstrating maintained industry leadership across output, profit, and market value metrics. These financial indicators reflect successful execution of strategic initiatives rather than merely representing commercial outcomes.

Board-level governance structures emphasise operational security through dedicated committees that oversee information dissemination protocols and personnel management. This elevation of confidentiality to executive governance levels indicates organisational recognition that operational data constitutes strategic national assets requiring protection equivalent to security infrastructure.

Market Share Dynamics and Competitive Positioning

The competitive landscape within rare earth markets demonstrates concentrated control patterns that reflect deliberate consolidation strategies. China Northern Rare Earth strategic control extends across multiple value chain segments, creating integrated supply networks that competitors struggle to replicate.

Market positioning advantages derive from scale economies in both upstream and downstream operations. The company maintains processing capabilities that enable transformation of raw materials into high-value products, capturing margin opportunities throughout the value chain rather than depending solely on commodity pricing.

Vertical integration creates barriers to entry for potential competitors while providing operational flexibility during market volatility. This structural advantage enables strategic responses to changing demand patterns without dependence on external suppliers or processing partners.

The establishment of comprehensive information security measures, including dedicated Confidentiality Committees and classified IT system isolation, signals recognition that competitive advantages require active protection. In addition, these protocols treat operational knowledge as strategic assets equivalent to national security information.

When big ASX news breaks, our subscribers know first

How Does CNREG's Financial Performance Reflect Strategic Intent?

Revenue Distribution Analysis by Business Segment

Financial performance patterns reveal strategic resource allocation priorities that extend beyond short-term revenue optimisation. The company's profit margin of approximately 8.5% based on Q3 2025 figures demonstrates operational efficiency while maintaining investment capacity for expansion initiatives.

Revenue concentration within domestic markets reflects deliberate strategic positioning that prioritises supply security for Chinese manufacturers over export revenue maximisation. This approach creates dependency relationships within China's industrial ecosystem while limiting exposure to international trade disruptions.

The financial structure enables sustained investment in capacity expansion projects, including 3,000 tons per year of NdFeB permanent magnet production and 50,000 tons per year of rapid-solidification alloy capacity. These investments represent strategic positioning for future demand growth rather than responses to current market conditions.

Key Financial Metrics (Q3 2025):

- Total Revenue: RMB 30.29 billion ($4.2 billion USD)

- Net Profit: RMB 2.58 billion ($360 million USD)

- Profit Margin: 8.5%

- NdFeB Capacity: 3,000 tons/year

- Alloy Production: 50,000 tons/year

Geographic Revenue Concentration Patterns

Market allocation strategies demonstrate prioritisation of domestic consumption over export revenue generation. This approach creates strategic advantages through supply security while reducing dependence on international market conditions that may be influenced by geopolitical tensions.

The concentration of revenue within domestic markets enables long-term relationship development with Chinese manufacturers across multiple industries. These relationships create switching costs and dependency patterns that strengthen market positioning beyond pure pricing competition.

Limited export exposure provides flexibility during international trade disputes while maintaining the option to leverage supply access as a strategic tool. This positioning enables selective market engagement rather than dependence on global commodity pricing mechanisms.

What Production Capabilities Drive China's Rare Earth Dominance?

Upstream Mining and Processing Infrastructure

The Bayan Obo mine complex represents a flagship operation within China Northern Rare Earth strategic control architecture. This facility provides integrated extraction and initial processing capabilities that form the foundation for downstream value-added operations.

Processing technology advancement initiatives focus on continuous improvement of extraction efficiency and environmental performance. These developments create competitive advantages through lower production costs while meeting increasingly stringent environmental requirements that may become barriers for competitors.

Rare earth concentrate production methodologies incorporate proprietary techniques developed through decades of operational experience. Furthermore, the protection of these methodologies through information security protocols prevents technology transfer to international competitors.

Downstream Manufacturing Expansion Programs

Strategic capacity additions demonstrate commitment to value chain integration that captures higher margins while creating customer dependency relationships. The 3,000 tons per year NdFeB permanent magnet capacity targets high-value applications in electric vehicles, wind turbines, and defence systems.

Rapid-solidification alloy production lines with 50,000 tons per year capacity represent specialised processing capabilities requiring precise composition control and cooling rate management. These technical requirements create barriers to entry for potential competitors lacking specialised knowledge and equipment.

Value-added product development priorities focus on applications requiring specific performance characteristics that command premium pricing. This strategy moves beyond commodity production toward engineered materials that require technical collaboration with customers.

The commissioning of major production expansions occurs under intensive oversight protocols including on-site political supervision, 24-hour leadership rotations, and mandatory monthly accountability measures. Consequently, this approach treats capacity additions as strategic national priorities rather than routine commercial investments.

Technology Innovation and Process Optimisation

Breakthrough technologies in continuous rare earth carbonate production enable improved process efficiency while reducing environmental impact. These advances create competitive advantages through lower operating costs and enhanced regulatory compliance.

Ammonia recycling system implementations demonstrate commitment to environmental efficiency that may become regulatory requirements in international markets. Early adoption of these technologies provides competitive positioning as environmental standards tighten globally.

Energy efficiency improvement protocols reduce operational costs while improving environmental performance metrics. These developments enable competitive pricing while maintaining profitability margins necessary for continued investment in expansion projects.

Recognition programmes for technical personnel, including regional skills awards for process continuity and emissions reduction contributions, demonstrate organisational emphasis on internal capability development rather than dependence on external expertise.

How Do Information Security Measures Reflect Strategic Priorities?

Board-Level Confidentiality Framework Implementation

The establishment of a dedicated Confidentiality Committee at board level represents formal institutionalisation of information security as a governance priority competing with financial and operational objectives for executive attention and resource allocation.

Data dissemination control protocols govern access to operational information, processing methodologies, and customer relationship data. These measures treat industrial knowledge as strategic assets requiring security equivalent to national defence information.

Personnel tracking systems monitor employees with sensitive data access, including post-departure surveillance to prevent knowledge transfer to competitors. However, this approach recognises that human capital represents a potential vulnerability requiring active management.

Ongoing inspection programmes ensure compliance with confidentiality protocols while identifying potential security gaps. These measures create organisational culture that prioritises information protection alongside operational efficiency.

Technology Transfer Prevention Mechanisms

Classified IT system isolation procedures maintain physical separation between sensitive operational data and external networks. This air-gapped architecture prevents digital access while enabling internal data sharing necessary for operational coordination.

Foreign visitor restriction policies limit exposure of sensitive facilities and information to international personnel who might transfer knowledge to competing organisations. These protocols balance commercial relationship requirements with security priorities.

Overseas travel monitoring for key personnel ensures that technical knowledge remains within organisational boundaries while enabling necessary business activities. This approach recognises that informal knowledge transfer represents ongoing security concerns.

The elevation of information security to board-level governance indicates recognition that competitive advantages require active protection rather than reliance on trade secret protections or contractual agreements alone.

What Role Does Brand Development Play in Global Strategy?

"Bayunebo" Brand Valuation and Market Positioning

The Bayunebo brand achieved a valuation of RMB 21.26 billion with 26% year-over-year growth, demonstrating successful transition from commodity supplier to branded materials provider. This transformation enables premium pricing power while creating customer loyalty that transcends pure cost competition.

Portfolio expansion includes 174 domestic trademark registrations and 14 international trademark applications, indicating strategic intent to protect brand recognition across multiple markets and product categories. This intellectual property protection creates legal barriers to competitive branding efforts.

Brand development at this scale represents strategic investment in market positioning that extends beyond immediate revenue generation. Furthermore, the focus on brand recognition enables differentiation within markets that might otherwise treat rare earth materials as undifferentiated commodities.

Market Perception and Customer Relationship Management

The transformation from supplier to branded materials provider requires customer education regarding product differentiation and quality assurance. This approach creates switching costs through technical certification processes and quality validation requirements.

Customer loyalty development through brand recognition enables pricing power that extends beyond raw material cost considerations. Customers willing to pay premium pricing for branded materials provide revenue stability during market volatility.

Premium pricing power through brand recognition creates financial capacity for continued investment in capacity expansion and technology development. This self-reinforcing cycle strengthens competitive positioning over time.

Brand-based customer relationships enable information gathering regarding market trends and competitor activities through routine commercial interactions. This intelligence provides strategic advantages in capacity planning and product development priorities.

How Do Export Controls Impact China's Rare Earth Strategy?

Regulatory Environment and Trade Policy Alignment

Strategic alignment between corporate operations and national trade policy creates coordination advantages that individual companies cannot achieve independently. This integration enables synchronised responses to international trade disputes while maintaining supply security for domestic manufacturers.

Domestic consumption prioritisation mandates reduce export dependency while creating leverage opportunities during international negotiations. This approach treats rare earth exports as strategic tools rather than purely commercial activities.

Strategic stockpiling and reserve management capabilities provide flexibility during supply disruptions while enabling tactical market interventions. For instance, these resources create options for responding to international pressure without compromising domestic supply security.

Export quota and licensing framework evolution reflects changing geopolitical priorities that may restrict international access to Chinese rare earth materials. These mechanisms enable selective market engagement based on strategic considerations.

Geopolitical Leverage Through Supply Chain Control

Critical mineral dependency creation in Western markets provides strategic leverage that extends beyond commercial relationships. This dependency creates vulnerabilities that may influence policy decisions regarding trade relationships and technology access, as discussed in recent China's new rare earth and magnet restrictions analysis.

Technology transfer requirements for market access enable knowledge acquisition while limiting competitor capabilities. This approach uses market dominance to accelerate domestic technological advancement while constraining international competition.

Strategic timing of supply restrictions can create market disruptions that impact competitor profitability and investment capacity. These tactics enable market share protection without direct competitive engagement.

Supply chain control mechanisms create systemic vulnerabilities in Western manufacturing that require strategic responses extending beyond individual company procurement decisions. Consequently, this systemic impact amplifies the strategic value of rare earth dominance.

The next major ASX story will hit our subscribers first

What Are the Implications for Global Rare Earth Markets?

Western Supply Chain Vulnerability Assessment

Dependency ratios across key rare earth elements reveal systemic vulnerabilities within Western manufacturing supply chains. These dependencies create strategic risks that extend beyond normal commercial supply disruption scenarios.

Alternative supplier development faces significant challenges including capital requirements, technical expertise gaps, and regulatory approval timelines. These barriers create time-sensitive vulnerabilities during transition periods toward supply chain diversification, particularly relevant as the European CRM facility initiative demonstrates.

Strategic mineral reserve adequacy analysis reveals insufficient stockpile levels relative to potential supply disruption scenarios. This gap creates immediate vulnerabilities while alternative supply sources undergo development and certification processes.

The concentration of processing capabilities within China creates bottlenecks that cannot be rapidly replaced through alternative suppliers lacking equivalent technical expertise and processing capacity.

Investment Opportunities in Non-Chinese Rare Earth Projects

Western supply chain development initiatives require substantial capital investment and technical expertise that may exceed individual company capabilities. These requirements suggest need for coordinated investment approaches involving government support and risk sharing mechanisms.

Processing technology development remains a critical bottleneck that requires dedicated research investment and technical personnel training. These capabilities cannot be rapidly acquired through commercial transactions or licensing agreements.

Timeline challenges for alternative supply development extend beyond typical project development cycles due to regulatory requirements and technical complexity. However, these delays create extended periods of continued dependency on Chinese sources.

Market development for non-Chinese rare earth producers requires customer certification processes and quality validation that may take years to complete. These requirements create barriers to rapid market entry even after production capability establishment.

Technology Competition and Innovation Gaps

Processing technology knowledge transfer restrictions limit Western access to proven methodologies while requiring independent development of equivalent capabilities. This technological gap creates both cost disadvantages and extended development timelines.

Research and development investment requirements for competitive processing technologies exceed normal commercial development budgets. These investments require strategic commitment over multiple years without guaranteed commercial success.

Innovation gaps in environmental processing technologies create additional barriers as regulatory requirements tighten globally. In addition, meeting environmental standards while maintaining cost competitiveness requires technical advances that may not be commercially available.

Substitution material research offers potential long-term alternatives to rare earth dependency, but breakthrough timelines remain uncertain. These research programmes require sustained investment without assured commercial viability.

How Can Western Markets Respond to Strategic Resource Control?

Alternative Supply Chain Development

Western governments and industry leaders are increasingly recognising the need for diversified rare earth supply chains. The development of alternative sources requires coordinated investment strategies that address both technical and commercial challenges.

Mining projects in countries such as Australia, Canada, and the United States are receiving increased attention and funding. However, establishing competitive processing capabilities remains a significant challenge requiring specialised expertise and substantial capital investment.

The mining industry evolution demonstrates how technological advances are enabling more efficient extraction and processing methods. These innovations may help reduce cost disadvantages compared to Chinese operations.

Strategic partnerships between Western companies and governments are essential for overcoming barriers to market entry. Risk-sharing mechanisms and government support can help accelerate development timelines while ensuring commercial viability.

Critical Minerals Security Initiatives

The importance of critical minerals energy security cannot be overstated as Western nations seek energy transition independence. Recent policy developments, including the Executive order on minerals in the United States, demonstrate growing government recognition of these vulnerabilities.

Strategic stockpiling initiatives provide short-term security while alternative supply sources undergo development. However, stockpile management requires careful planning to ensure adequate reserves without excessive carrying costs.

Research and development funding for substitution materials and recycling technologies offers potential long-term solutions. These investments require sustained commitment over multiple years with uncertain commercial outcomes.

International cooperation frameworks enable coordinated responses among allied nations, preventing competitive disadvantages while developing alternative capabilities. Shared research initiatives and technology transfer agreements can accelerate development timelines, as highlighted in China's strategic control over supply chains.

Future Scenarios for China's Rare Earth Strategic Control

Scenario 1: Continued Market Consolidation

Further vertical integration possibilities include expansion into end-use manufacturing sectors that currently represent customer segments. This development would create direct competition with current customers while capturing additional value chain margins.

Enhanced downstream manufacturing capabilities could enable complete product solutions rather than materials supply relationships. This transformation would fundamentally alter customer relationships while increasing market control.

Increased barriers to entry for competitors through continued capacity expansion and technology development would solidify market dominance while reducing competitive pressure on pricing and service levels.

Market consolidation through acquisition or partnership with remaining independent producers could eliminate competitive alternatives while creating unified strategic control over global supply chains.

Scenario 2: Geopolitical Tension Escalation

Complete export restriction implementation would force Western manufacturers to develop alternative supply sources under emergency conditions, potentially creating market opportunities for non-Chinese producers despite higher costs and lower quality.

Strategic stockpile utilisation for leverage during international negotiations could create temporary supply disruptions while demonstrating the strategic value of rare earth control for broader geopolitical objectives.

Technology transfer prohibition enforcement would limit Western access to proven processing methodologies while accelerating independent technology development efforts. However, this scenario could ultimately reduce Chinese technological advantages over extended periods.

Escalating restrictions might trigger coordinated Western responses including strategic stockpiling, alternative supplier development, and substitution material research that could reduce Chinese leverage over multi-year timeframes.

Scenario 3: Market Diversification Pressure

Western alternative supply development acceleration through government support and strategic investment could reduce dependency over 5-10 year timeframes, creating competitive pressure on Chinese pricing and service levels.

Recycling technology advancement impacts could reduce demand for primary rare earth materials while enabling Western supply security through domestic waste stream processing. These developments would alter supply-demand dynamics fundamentally.

Substitution material research breakthrough potential could eliminate demand for specific rare earth elements while reducing strategic leverage from supply control. These technological changes represent long-term threats to current market structures.

Market diversification success would require coordinated policy responses including investment incentives, research funding, and regulatory support that may exceed current Western government commitment levels.

Key Takeaways for Investors and Policymakers

Investment Risk Assessment Framework

Supply chain concentration risk evaluation requires understanding both immediate disruption potential and long-term strategic implications of rare earth dependency. These risks extend beyond normal commercial supply chain management considerations.

Geopolitical exposure measurement tools must account for scenarios involving strategic resource restriction rather than purely commercial supply disruptions. Traditional risk assessment methodologies may underestimate potential impact severity and duration.

Alternative investment opportunity identification should consider both direct rare earth supply alternatives and substitution technologies that could eliminate dependency entirely. These options represent different risk-return profiles requiring distinct evaluation approaches.

Portfolio diversification strategies must account for systemic vulnerabilities affecting entire industry segments simultaneously. Consequently, geographic diversification alone may be insufficient protection against strategic supply restrictions.

Strategic Response Options for Western Markets

Critical mineral reserve establishment priorities require coordinated government and industry action to create strategic stockpiles sufficient for extended supply disruption scenarios. These reserves must balance storage costs against strategic security benefits.

Technology development funding requirements exceed normal commercial research budgets, necessitating government support or risk-sharing mechanisms to enable private sector investment in alternative processing technologies and substitution materials research.

International cooperation framework necessities include coordination among Western allies to avoid competitive disadvantages while developing alternative supply sources and processing capabilities. Furthermore, uncoordinated responses may create market distortions reducing overall effectiveness.

Strategic response timelines must account for extended development periods required for alternative supply source establishment and customer certification processes. Immediate responses must bridge gaps while long-term solutions undergo development.

Investment Disclaimer: The analysis presented reflects current market conditions and strategic positioning based on available information. Rare earth markets involve complex geopolitical factors that may change rapidly, affecting investment outcomes. All investment decisions should consider comprehensive risk assessment including supply chain, regulatory, and geopolitical factors that may impact returns.

China Northern Rare Earth strategic control represents a comprehensive approach to market dominance that extends far beyond conventional business operations. The integration of operational discipline, information security, and brand development creates competitive advantages that require coordinated strategic responses from Western markets seeking supply chain security and independence.

Looking to Navigate Critical Mineral Market Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across the ASX, helping investors identify actionable opportunities in the rapidly evolving critical minerals sector. With China's strategic control over rare earth supply chains creating unprecedented market dynamics, explore Discovery Alert's discoveries page to understand how historic mineral discoveries have generated substantial returns and begin your 30-day free trial to position yourself ahead of critical market developments.