May 22, 2026

The Architecture of Optionality: Why Latin American Miners Are Engineering Multi-Polar Buyer Relationships

Commodity export history is littered with cautionary tales about single-buyer dependence. From the era when the United States absorbed the vast majority of Latin American raw material exports, to the dramatic pivot toward China during the commodity supercycle of the 2000s and 2010s, the region has repeatedly demonstrated a tendency to over-concentrate its external trade relationships. That pattern delivered enormous short-term revenue gains but embedded structural vulnerabilities that only become visible when the dominant buyer changes its terms. Today, a new chapter is being written, and mining companies in Latin America are betting on India without abandoning China as the foundational logic of a deliberate risk-management architecture.

This is not a story of geopolitical alignment or ideological realignment. It is a story of portfolio construction applied to commodity relationships, and understanding the mechanics of that strategy requires looking closely at where power actually resides in the current mineral supply chain.

When big ASX news breaks, our subscribers know first

From Single Buyer Dependence to Strategic Optionality

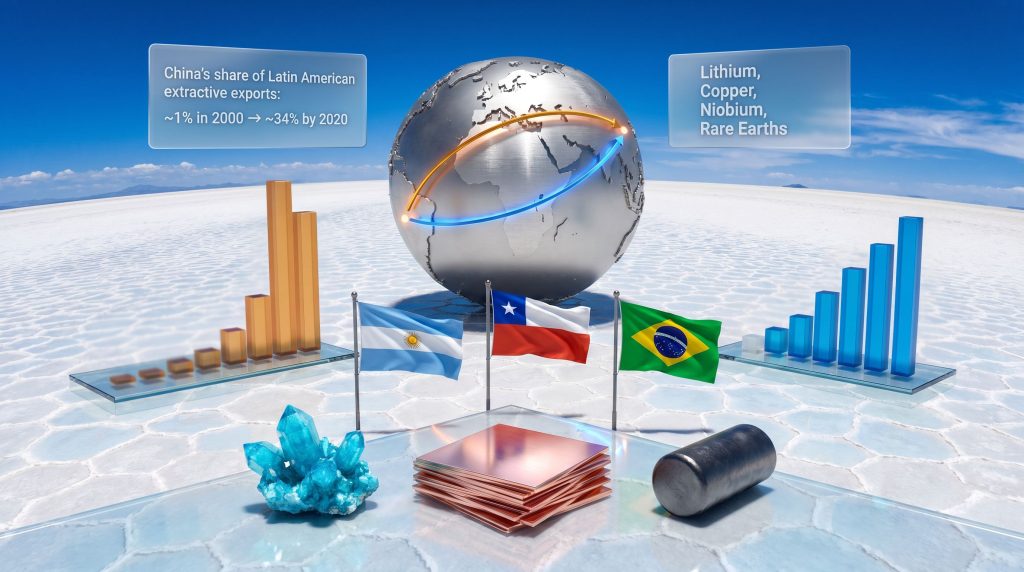

The scale of China's penetration into Latin American extractive trade over the past two decades is difficult to overstate. According to data compiled by the UN Economic Commission for Latin America and the Caribbean (ECLAC) and trade databases including UN Comtrade, China's share of Latin American exports climbed from low single digits in 2000 to become the dominant trade destination for key mineral-exporting economies by the late 2010s.

For countries such as Chile and Peru, China now absorbs well over one-third of mineral and metals exports when copper, lithium, and iron ore are considered together. Brazil's iron ore trade tells a similar story, with China representing the dominant destination for its seaborne shipments across the last decade.

ECLAC's trade outlook publications have consistently flagged that this level of destination concentration amplifies vulnerability to external demand shocks, price pressure campaigns, and unilateral policy changes by the dominant buyer. The current strategic rethinking among Latin American operators is a direct response to that documented vulnerability.

The critical distinction analysts must understand is the difference between market diversification and geopolitical realignment. Latin American governments are almost universally resistant to being drawn into the U.S.-China rivalry as a declared participant. The diversification toward India is being framed not as a rejection of China but as a commercial risk-management exercise, one that also happens to generate negotiating leverage with Beijing.

This is the "both/and" framework in action: maintain and even deepen Chinese relationships while simultaneously cultivating India as a credible alternative buyer whose growing demand creates genuine competitive tension. Furthermore, the broader surge in critical minerals demand is accelerating this strategic rebalancing across the region.

What India Brings to the Table: Scale, Urgency, and Political Neutrality

India's mineral import agenda is being driven by a combination of domestic industrial ambition and structural supply-chain vulnerability. The country's battery manufacturing sector, electric vehicle transition targets, and infrastructure investment pipeline collectively generate demand projections for lithium, copper, and rare earth elements that are among the fastest-growing in the world.

India currently imports the overwhelming majority of its critical mineral requirements, and its domestic processing and refining capacity remains far below what its industrial ambitions require. India's lithium supply strategy is consequently driving increasingly assertive procurement engagement across multiple supply regions, including Latin America.

The minerals most central to India's Latin American procurement strategy fall into four primary categories:

- Lithium carbonate and lithium hydroxide: Essential for battery cell manufacturing, with Argentina and Chile holding the most advanced extraction projects

- Copper cathodes: Driven by India's infrastructure investment pipeline and power grid expansion, with Chile and Peru as primary source countries

- Niobium: Brazil controls the vast majority of global identified niobium supply, making it uniquely positioned as a supplier with limited Chinese substitutability

- Rare earth elements: Brazil and Peru hold significant deposits, relevant to India's stated goal of diversifying away from Chinese-dominated REE processing

Beyond raw demand volumes, India offers something that Chinese state-backed buyers structurally cannot: perceived political neutrality. Latin American governments navigating U.S.-China pressure find that Indian procurement partnerships carry far less geopolitical baggage than deepening Chinese equity relationships. India's "friend-shoring" narrative, while not yet backed by the financing scale that China can deploy, provides a diplomatic framing that appeals to governments seeking leverage without formal alignment. Indeed, as reported by Stratnews Global, India is actively betting on Latin America's mineral wealth as a cornerstone of its long-term supply security.

| Mineral | Primary Latin American Sources | India's Strategic Interest | China's Current Position |

|---|---|---|---|

| Lithium Carbonate | Argentina, Chile, Bolivia | High: battery supply chain | Dominant: refining control |

| Lithium Hydroxide | Chile, Argentina | High: EV manufacturing | Dominant: processing share |

| Copper Cathodes | Chile, Peru | Growing: infrastructure demand | Major buyer and investor |

| Niobium | Brazil | Emerging strategic interest | Significant existing presence |

| Rare Earth Elements | Brazil, Peru | Strategic priority | Near-monopoly in processing |

The Processing Chokepoint: Why Buyer Diversification Is Not the Same as Power Diversification

Here is the insight that most surface-level analysis of the India-Latin America mineral story misses entirely. China's influence over Latin American mining cannot be reduced to trade volumes or even direct investment. Its most durable leverage point is processing and refining infrastructure.

Chinese firms hold significant equity stakes in lithium projects across the Lithium Triangle, the lithium-rich salt flat regions spanning Argentina, Chile, and Bolivia that collectively host the world's largest identified lithium reserves. More importantly, China dominates global lithium refining capacity. This means that even when Latin American producers sell raw material to a non-Chinese buyer, the intermediate processing step may still route through Chinese infrastructure.

The critical distinction here is between export diversification, which is achievable within a relatively short timeframe through new offtake agreements, and processing independence, which requires a decade-scale investment in domestic or partner-country refining infrastructure. Confusing the two leads to a fundamental overestimation of how quickly India can reduce China's structural leverage.

These rare earth processing challenges are not unique to Latin America; however, the region's geographic distance from established refining hubs makes them particularly acute. For India to become a genuine Tier-1 partner rather than a secondary buyer relationship, it would need to commit capital to joint processing ventures within Latin America itself.

Three Scenarios for the Next Five Years

Strategic scenario analysis offers the most rigorous framework for evaluating how the China-India-Latin America mineral triangle might evolve. Three distinct pathways emerge from current evidence:

Scenario A: Incremental Diversification (Highest Probability, 2026-2030)

Mining operators maintain primary Chinese offtake agreements while negotiating parallel long-term supply contracts with Indian buyers. India gradually captures a 10-20% share of offtake volumes across key minerals without displacing Chinese purchasing dominance. The outcome is improved negotiating leverage with Beijing and modest revenue diversification, but limited progress on processing independence.

Scenario B: Accelerated India Pivot (Conditional on Infrastructure Commitment)

India commits capital to joint processing ventures in Chile or Argentina, directly addressing the refining bottleneck. Latin American governments offer preferential terms to Indian partners as part of structured mineral diplomacy frameworks. The outcome is meaningful supply-chain bifurcation, with India becoming a genuine second-tier anchor buyer and Chinese negotiating leverage declining materially.

Scenario C: Forced Realignment (Tail Risk)

Escalating U.S.-China trade tensions or direct external pressure accelerates decoupling beyond what Latin American operators have planned for. Chinese investment in the region faces political restrictions, forcing operators to rapidly scale Indian and Western procurement partnerships. The outcome involves short-term revenue disruption and a significant processing infrastructure gap that takes years to fill.

Country-by-Country Positioning: Who Benefits Most?

The India diversification opportunity is not evenly distributed across Latin America. Geography, mineral profile, and existing Chinese contractual entanglements all affect each country's strategic positioning.

Argentina

Argentina sits at the centre of the Lithium Triangle and is a primary target for Indian offtake discussions. The Argentina lithium brine market presents particularly compelling opportunities, given the country's vast salt flat reserves and evolving investment frameworks. The complication is that Chinese firms already hold significant equity positions in multiple lithium projects, creating a dual-relationship dynamic where the same asset may be simultaneously subject to Chinese equity influence and Indian offtake interest.

Chile

Chile, as the world's largest copper producer and a major lithium source, offers dual-commodity relevance for India's infrastructure and battery manufacturing agendas. Its more advanced regulatory and contractual frameworks make it an easier entry point for Indian institutional investors. The complexity lies in existing relationships between state entities and their Chinese partners; consequently, Codelco's copper strategy will be central to determining how much flexibility exists for redirecting offtake toward new buyer relationships.

Peru

Peru's copper-dominant export profile aligns well with India's infrastructure-driven demand growth, but persistent political instability has historically constrained long-term offtake agreement structures. This represents a genuine risk factor for Indian procurement planners seeking contractual certainty.

Brazil

Brazil occupies a uniquely strong position for a reason most commentators overlook: it controls the vast majority of the world's identified niobium supply. Niobium is used as a strengthening additive in high-strength low-alloy steel and is increasingly relevant to battery chemistry research. China cannot easily substitute Brazilian niobium, which gives Brazil a rare form of commodity leverage. Brazil's already-established iron ore trade relationships with both China and India provide a proven template for dual-buyer management.

Bolivia

Bolivia holds the world's largest identified lithium reserves but remains the most constrained by nationalisation policy and infrastructure limitations. Chinese state entities have been the primary engagement partners, and India faces a steeper entry challenge here than anywhere else in the region. Bolivia's lithium sector represents the single largest wildcard in regional mineral diplomacy, and any liberalisation of its investment framework would immediately trigger intense India-China competition.

The next major ASX story will hit our subscribers first

Structural Barriers That the India Narrative Often Underestimates

A candid assessment of the India-Latin America mineral integration story must acknowledge the friction points that optimistic analyses tend to gloss over. Moreover, as CSIS has noted, the structural complexities of Latin American mining resist straightforward geopolitical narratives:

- Processing infrastructure gap: India's domestic refining capacity cannot yet absorb Latin American raw materials at scale without Chinese intermediaries in the value chain

- Logistics and freight costs: The geographic distance between South America and India adds meaningful freight cost layers relative to established trans-Pacific routes to China, affecting delivered-cost competitiveness

- Financing capacity asymmetry: Chinese state-backed financing mechanisms operate at a scale and deployment speed that Indian institutional capital cannot currently match, creating a structural disadvantage when competing for project equity

- Contractual lock-in: Existing Chinese equity stakes and long-term offtake agreements in many Latin American projects create legal and commercial barriers to redirecting supply, even when both the Latin American operator and Indian buyer are willing

For India to close these gaps, a sequence of specific developments would need to materialise: Indian-funded processing joint ventures within Latin America; formalised government-to-government mineral security frameworks with binding commitments; Indian investment vehicles capable of competing at the project development stage; and logistics infrastructure that reduces the freight cost penalty of the India route.

Investment Implications: Reading the Signal Correctly

For investors, the India diversification narrative is best understood as a medium-to-long-term structural theme rather than a near-term catalyst. The risk of mispricing this theme lies in treating incremental diplomatic engagement as evidence of imminent offtake volume shifts.

The companies best positioned to capture value from this evolving dynamic share several characteristics:

- Flexible offtake structures with no exclusive Chinese contractual lock-in

- Mineral exposure to lithium, copper, or niobium, the three commodity categories where Indian demand growth is most structurally driven

- Assets located in Argentina, Chile, or Brazil, where regulatory frameworks and existing diplomatic engagement are most advanced

- Processing assets within Latin America that are not Chinese-owned, which become strategically valuable if Indian-funded joint ventures materialise

Key risk factors to monitor include the pace of India's domestic battery manufacturing scale-up, which determines whether projected import demand actually materialises; the Chinese response to Latin American diversification efforts, including potential retaliatory financing withdrawal or price pressure campaigns; and the competitive dynamic from U.S.-aligned mineral security frameworks, which may compete with India for supply-chain alignment from Latin American producers.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. All scenario analysis and forward-looking statements involve inherent uncertainty. Readers should conduct independent due diligence before making investment decisions.

The Longer Arc: Portfolio-Based Commodity Relationships as the New Normal

The China-dominant model served Latin American mining operators exceptionally well during the commodity supercycle, delivering sustained demand growth, competitive pricing, and substantial project financing. The asymmetric risk that model now represents in a fragmented geopolitical environment is the central reason why mining companies in Latin America are betting on India without abandoning China as they actively redesign their buyer architecture.

The emerging template is portfolio-based buyer relationships, where no single nation controls a dominant share of offtake volumes from any given asset or country. India is the first serious challenger to Chinese buyer dominance in the region, but it is unlikely to be the last. European Union critical mineral frameworks and U.S. supply-chain initiatives are both generating procurement interest in Latin American resources, creating a multi-polar buyer environment that, once fully developed, would structurally reduce the leverage of any single actor.

What the next five years will reveal is whether India's processing infrastructure commitments translate into operational capacity, whether Latin American governments can renegotiate Chinese equity positions without triggering capital withdrawal, and whether Bolivia's lithium sector opens to competitive international investment. The answers to those questions will ultimately determine whether mining companies in Latin America are betting on India without abandoning China remains a pragmatic commercial strategy, or whether it evolves into something far more structurally transformative for the region's mineral diplomacy.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including those across critical commodities like lithium, copper, and rare earths that sit at the centre of Latin America's evolving buyer relationships — instantly translating complex mineral data into actionable investment insights. Explore how historic discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the broader market.