June 30, 2026

China Northern Rare Earth's strategic positioning within Beijing's quinquennial planning framework represents a fundamental shift toward integrated resource control that could reshape global manufacturing dependencies through 2030. The China Northern Rare Earth Five-Year Plan demonstrates how state-directed coordination enables rapid deployment of capital and technology across entire value networks, creating competitive dynamics that transcend traditional market mechanisms.

Understanding how centralised quinquennial planning translates into sectoral dominance reveals critical insights for investors, manufacturers, and policymakers navigating an increasingly fragmented global economy. Furthermore, recent export control measures amplify these strategic advantages by introducing regulatory uncertainty into alternative supply chain planning.

Understanding China's Rare Earth Industrial Dominance Framework

The Architecture of China's 15th Five-Year Plan (2026-2030)

China's quinquennial planning system operates through standardised five-year cycles that align state resources with strategic objectives. The 15th Five-Year Plan covering 2026-2030 represents a critical transition phase where Beijing shifts from volume expansion to value-chain integration across critical materials sectors.

The National Development and Reform Commission (NDRC) coordinates these planning cycles through mandatory targets for state-owned enterprises, creating direct pathways between central policy and operational execution. Unlike market-driven economies where corporate strategy responds to competitive pressures, China's planning framework enables:

- Synchronised capacity deployment across mining, processing, and manufacturing stages

- Coordinated pricing strategies that prioritise market control over profit maximisation

- Technology development timelines aligned with geopolitical objectives

- Export control mechanisms integrated into production planning

The transition from the 14th to 15th Five-Year Plan marks a fundamental shift in approach. Where previous cycles emphasised production scale and cost competitiveness, the current framework prioritises vertical integration and downstream value capture. This evolution reflects Beijing's recognition that controlling raw material extraction without commanding finished product manufacturing leaves substantial value creation to international competitors.

State-owned enterprise alignment within this system creates execution capabilities unavailable to private competitors. Corporate strategies automatically synchronise with national objectives, eliminating coordination delays typical of market-based resource allocation. This structural advantage becomes particularly pronounced in capital-intensive industries requiring long development timelines and complex technology integration.

China Northern Rare Earth Group's Market Position

China Northern Rare Earth Group operates as the world's largest rare earth producer under Baogang Group ownership, commanding unprecedented scale across global markets. The company's 2025 performance metrics reportedly achieved first-place rankings in revenues, profits, output, and market capitalisation within the rare earth sector, according to recent industry analysis.

This market leadership extends beyond simple production volumes. The company's integration within the broader Baogang Group industrial ecosystem provides access to steel production infrastructure, metallurgical expertise, and diversified revenue streams that create competitive moats unavailable to single-focus rare earth enterprises.

| Performance Metric | 2025 Status | Strategic Significance |

|---|---|---|

| Global Production Share | Market Leader | Price-setting capability |

| Revenue Ranking | First Globally | Capital allocation advantage |

| Supply Chain Integration | Vertical Control | Technology protection |

| State Coordination | SOE Alignment | Policy execution speed |

The company's explicit mission to safeguard China's rare earth supply-chain security demonstrates how commercial operations serve broader strategic purposes. Management's commitment to expanding production whilst stabilising pricing reveals deliberate market intervention designed to maintain competitive advantage over Western alternative supply chains.

This positioning enables the company to operate according to strategic rather than purely commercial logic. Where private enterprises must optimise for shareholder returns, state-owned rare earth producers can prioritise market share, technology protection, and geopolitical leverage within their operational frameworks.

The Baogang Group parent entity, established in 1978, represents one of China's largest state-owned steel and materials enterprises. This relationship ensures rare earth operations benefit from accumulated industrial expertise, established supply chains, and coordinated investment strategies spanning multiple industrial sectors.

When big ASX news breaks, our subscribers know first

How Will China's "Full-Element, Full-Product" Strategy Reshape Global Markets?

Vertical Integration Across the Rare Earth Value Chain

China's full-element, full-product industrial system represents a comprehensive strategy spanning extraction, separation, processing, and downstream manufacturing within integrated state-controlled networks. This approach eliminates intermediate profit margins whilst concentrating technological capabilities within protected industrial clusters.

Mining operations leverage China's geological advantages in both carbonatite deposits and ion-adsorption clays. The Baotou region contains the world's largest single rare earth resource, whilst southern Chinese provinces provide access to heavy rare earth elements critical for advanced applications. This geological diversity enables comprehensive element portfolio control unavailable to single-deposit competitors.

Separation and processing technology represents the critical bottleneck in global rare earth supply chains. China controls approximately 90% of global separation capacity through facilities that require decades of process optimisation and substantial capital investment to replicate. The technical complexity of achieving >99.99% purity for high-technology applications creates significant barriers for alternative producers.

Key technological advantages include:

- Solvent extraction expertise developed over 40+ years of industrial operation

- Precipitation chemistry optimisation for individual rare earth element isolation

- Quality control systems meeting aerospace and defence specifications

- Environmental compliance frameworks balancing production efficiency with regulatory requirements

Downstream applications integration extends China's control into permanent magnet manufacturing, phosphor production, catalytic materials, and specialised alloys. This vertical structure captures 40-60% of total value-chain margins compared to 10-15% available to raw material suppliers operating in isolation.

The strategic implications become apparent when examining supply chain vulnerabilities. Western manufacturers requiring rare earth inputs face limited alternatives to Chinese processing, even when sourcing raw materials from non-Chinese mines. MP Materials' Mountain Pass facility exemplifies this challenge, continuing to ship concentrate to China for separation despite operating the largest rare earth mine outside China.

Technology Transfer and Innovation Acceleration

China's research and development acceleration strategy focuses on converting technological capabilities into commercial production faster than international competitors can establish alternative supply chains. This approach leverages accumulated expertise whilst targeting emerging applications before Western companies achieve market entry.

Proprietary separation technologies represent closely guarded intellectual property developed through decades of state-supported research. These methodologies enable China to maintain processing cost advantages whilst creating substantial catch-up costs for competitors attempting to develop equivalent capabilities.

The commercialisation acceleration objective targets several critical application areas:

- Advanced permanent magnets for electric vehicle propulsion systems

- Rare earth-in-glass optical materials for telecommunications infrastructure

- Metallurgical additives for high-performance steel and aluminium alloys

- Next-generation catalysts for chemical processing and environmental applications

International technology acquisition complements internal development through targeted partnerships, equity investments, and strategic collaborations. However, the evolving mining industry evolution suggests that maintaining control over core separation technologies whilst seeking access to downstream application expertise represents a key competitive strategy.

The timeline advantage proves particularly significant in emerging markets where technological leadership translates into sustained competitive positions. By accelerating movement from research to commercial production, Chinese producers can establish manufacturing scale and cost structures that discourage new market entrants.

Capital efficiency in technology development benefits from state coordination across research institutions, universities, and industrial enterprises. This integrated approach eliminates duplication whilst concentrating resources on breakthrough technologies with commercial potential.

What Are the Implications of China's Capacity Expansion Plans?

Production Scale and Global Supply Impact

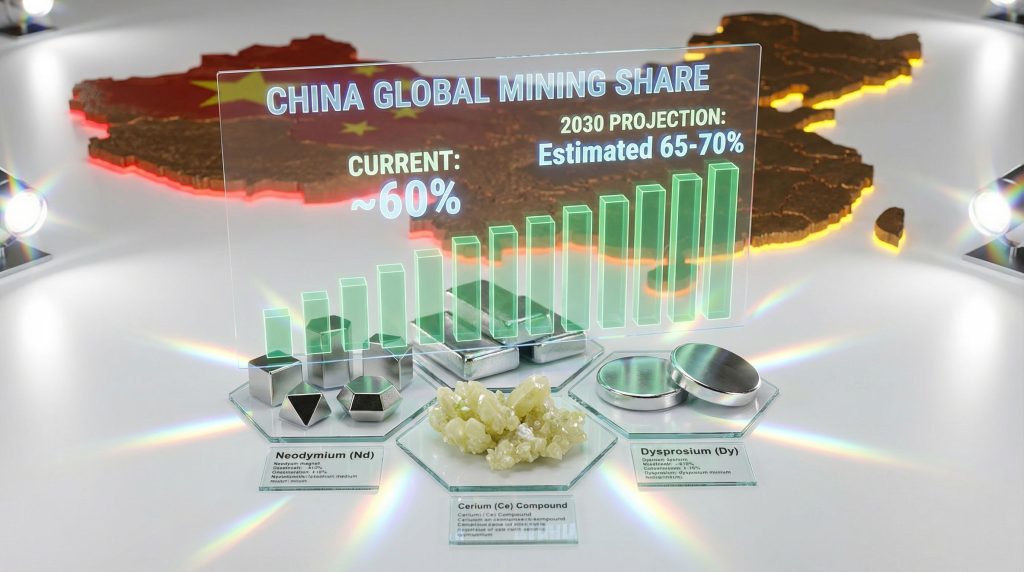

China's capacity expansion trajectory through 2030 reinforces existing supply chain dependencies whilst creating additional barriers for alternative producers seeking market entry. Current production metrics demonstrate the scale advantages that enable strategic pricing and supply management.

| Supply Chain Metric | Current Status (2025) | 2030 Projections |

|---|---|---|

| Global Mining Share | ~60% | Estimated 65-70% |

| Separation Capacity | ~90% | Projected 85-95% |

| Processing Infrastructure | Dominant | Near-monopolistic |

| Downstream Integration | Market Leader | Comprehensive Control |

China's 2024 production reached approximately 880,000 tonnes of rare earth oxide equivalent, representing the majority of global supply according to U.S. Geological Survey data. This scale enables significant economies of scope across mining, processing, and manufacturing operations.

The global rare earth market, valued at approximately $6-7 billion annually, remains concentrated within Chinese industrial networks despite growing international demand for electric vehicles, renewable energy systems, and defence applications. This concentration creates strategic leverage that extends beyond simple commercial considerations.

Separation capacity constraints represent the primary bottleneck limiting alternative supply chain development. Building greenfield separation facilities requires $500 million to $1 billion in capital investment with 3-7 year construction timelines, creating substantial barriers for competitive entry.

Western alternative capacity remains limited compared to Chinese scale. Lynas Rare Elements operates separation capacity of approximately 20,000-30,000 tonnes annually across Australian and Malaysian facilities, representing less than 5% of Chinese capacity. This scale differential enables China to influence global pricing through production adjustments.

The price stabilisation strategy announced for the China Northern Rare Earth Five-Year Plan suggests Beijing will use scale advantages to maintain competitive pressure on alternative producers. By coordinating capacity expansion with pricing objectives, Chinese producers can prevent Western competitors from achieving the profitability levels necessary for sustained operations.

Market Control and Supply Chain Security

Export control mechanisms amplify China's strategic leverage by creating additional uncertainty for international manufacturers dependent on Chinese supply chains. Recent regulatory implementations demonstrate how administrative measures can complement production advantages.

Technology transfer restrictions prevent foreign entities from accessing Chinese separation expertise whilst maintaining dependence on Chinese processing capabilities. This approach preserves technological advantages whilst generating export revenues from value-added products.

The dual-use applications framework enables selective supply management for defence and high-technology sectors. In this context, critical minerals energy security considerations become paramount for national economic planning.

Buffer stock management provides additional tools for supply chain influence. State-owned enterprises can coordinate inventory management to smooth market fluctuations or create strategic pressure during geopolitical tensions.

Critical Risk Assessment:

Single-source dependency for critical materials creates systemic vulnerabilities across Western manufacturing sectors, with particular exposure in defence, renewable energy, and electric vehicle supply chains.

Why Does China's Rare Earth Strategy Challenge Western Localisation Efforts?

Competitive Cost Structure Advantages

Labour cost differentials provide Chinese producers with substantial operational advantages that extend beyond simple wage comparisons. Integrated industrial clusters enable shared infrastructure, specialised workforce development, and coordinated logistics that reduce total production costs.

Economies of scale in processing facilities create fixed-cost advantages unavailable to smaller alternative producers. Chinese separation plants process volumes that justify sophisticated automation, environmental control systems, and quality management infrastructure requiring substantial throughput to achieve cost efficiency.

Environmental compliance costs vary significantly across jurisdictions, with Chinese producers operating within established regulatory frameworks optimised for industrial efficiency. Western alternative projects face more stringent environmental requirements that increase capital costs and operational complexity.

Capital allocation efficiency benefits from state-directed investment strategies that prioritise strategic objectives over short-term returns. This approach enables sustained investment in capacity expansion and technology development despite market volatility.

Technology and Infrastructure Barriers

Separation technology complexity creates significant barriers for new market entrants attempting to establish competitive processing capabilities. The rare earth-to-rare earth selectivity problem requires sophisticated chemistry and process control that takes years to optimise.

Intellectual property constraints limit access to proven separation methodologies, forcing alternative producers to develop proprietary technologies or licence incomplete solutions. Chinese producers benefit from accumulated process knowledge protected through state secrecy rather than patent disclosure.

Timeline challenges for establishing alternative supply chains exceed political and investment planning horizons in Western economies. The 3-7 year development periods for greenfield projects create coordination problems across multiple stakeholder groups with different risk tolerances and time preferences.

Capital investment requirements for competitive facilities exceed the risk appetite of many private investors, particularly given uncertainty about long-term Chinese competitive responses. The scale of investment needed approaches levels requiring government support or strategic partnerships.

How Do Export Controls Amplify China's Strategic Leverage?

Regulatory Framework Evolution

Export control implementations create additional uncertainty layers for international manufacturers planning long-term supply strategies. These administrative measures complement production advantages by introducing regulatory risk into alternative supply chain planning.

Technology transfer restrictions prevent foreign entities from accessing Chinese processing expertise whilst maintaining market dependencies. This approach preserves competitive advantages whilst generating revenue from value-added exports.

Dual-use application categories enable selective enforcement targeting specific end-users or applications. Defence contractors, aerospace manufacturers, and advanced technology companies face particular exposure to supply disruptions through targeted export limitations.

Licensing requirement systems create administrative barriers that can be adjusted according to bilateral relationships and strategic priorities. These mechanisms provide diplomatic leverage whilst maintaining plausible commercial rationales.

Geopolitical Risk Assessment

Supply disruption scenarios create cascading effects across Western industrial sectors dependent on Chinese rare earth inputs. Electric vehicle manufacturers, wind turbine producers, and defence contractors face potential production shutdowns during supply interruptions.

Price volatility risks increase during periods of geopolitical tension, with Chinese producers capable of coordinating pricing strategies across state-owned enterprises. This coordination capability enables strategic market pressure unavailable to disaggregated private competitors.

Furthermore, escalating US‑China trade tensions compound these vulnerabilities by introducing additional layers of regulatory uncertainty into already concentrated supply chains.

Technology access limitations prevent Western companies from developing competitive processing capabilities, creating sustained dependencies on Chinese supply chains. These restrictions compound over time as technological gaps widen.

Investment uncertainty discourages private capital allocation toward alternative supply chain development when regulatory risks create unpredictable operating environments. This dynamic reinforces existing market concentrations.

What Alternative Scenarios Could Emerge by 2030?

Western Supply Chain Diversification Pathways

Australian rare earth development represents the most viable alternative to Chinese supply, with Lynas Rare Elements demonstrating operational separation capabilities outside China. However, scale limitations and capital constraints prevent comprehensive market diversification within projected timelines.

North American processing initiatives face significant technological and regulatory barriers. Recent developments illustrate the ongoing challenges in establishing viable alternative supply chains, as MP Materials continues shipping concentrate to China despite operating the largest non-Chinese mine.

European Union critical materials strategies emphasise recycling and demand reduction rather than alternative primary production. These approaches may reduce import dependencies but cannot eliminate them within current technological frameworks.

Strategic partnership models could enable technology sharing and risk distribution across allied nations, but require unprecedented coordination between government and private sector stakeholders with different risk tolerances and investment horizons.

Market Fragmentation vs. Chinese Consolidation

Probability assessment for successful non-Chinese rare earth ecosystems remains limited by technological barriers, capital requirements, and Chinese competitive responses. Alternative supply chains may achieve niche market positions but struggle to compete across comprehensive product portfolios.

Investment requirements for competitive alternative capacity exceed private market capabilities in most scenarios. Government support mechanisms become necessary but create political sustainability challenges during economic downturns or policy transitions.

Technology development timelines favour incumbents with established capabilities and accumulated expertise. Breakthrough technologies could alter competitive dynamics, but development risks and commercialisation challenges create significant uncertainty.

International cooperation frameworks could enable shared development costs and coordinated market entry strategies, but require sustained political commitment across multiple election cycles and changing strategic priorities.

The next major ASX story will hit our subscribers first

How Should Investors and Industries Prepare for This New Reality?

Investment Strategy Considerations

Portfolio exposure assessment should evaluate direct and indirect dependencies on Chinese rare earth supply chains across equity holdings. Manufacturing companies, technology firms, and defence contractors face varying levels of supply chain risk requiring different hedging strategies.

Alternative supply chain investments carry significant execution risk but offer potential strategic value during supply disruptions. Investors should evaluate technology development timelines, regulatory support levels, and competitive response scenarios when assessing alternative producers.

Commodity price hedging becomes increasingly complex when supply chains concentrate within state-controlled entities capable of coordinated market management. Traditional hedging mechanisms may prove insufficient during strategic supply disruptions.

Geographic diversification considerations should account for supply chain dependencies that transcend simple revenue exposure metrics. Companies operating outside China may remain vulnerable to Chinese supply chain control.

Corporate Risk Management Frameworks

Supply chain auditing should map rare earth dependencies across multiple product tiers, identifying both direct inputs and embedded components sourced through complex supply networks. Many manufacturers lack visibility into rare earth exposure through component suppliers.

Strategic inventory management requires balancing carrying costs against supply disruption risks. Critical applications may justify substantial buffer stocks despite working capital implications.

Supplier diversification strategies face practical limitations when alternative sources lack comparable quality, scale, or reliability. Diversification efforts must account for realistic alternative capacity constraints and development timelines.

Contractual risk allocation becomes critical when suppliers face force majeure risks related to export controls or regulatory changes. Contract terms should address supply interruption scenarios and alternative source requirements.

What Does This Mean for Global Technology Leadership?

Downstream Industry Impact Assessment

Electric vehicle manufacturing faces particular vulnerability to rare earth supply disruptions given permanent magnet motor requirements. Leading EV producers must balance performance optimisation with supply chain security considerations.

Renewable energy systems depend heavily on rare earth permanent magnets for wind turbine generators and various component applications. Grid-scale renewable deployment could face constraints during supply interruptions.

Defence applications require rare earth materials for guidance systems, communications equipment, and advanced weapons platforms. Consequently, implementing a comprehensive defence‑critical materials strategy becomes essential for national security considerations that extend beyond commercial supply chain concerns.

Technology innovation cycles may slow in sectors requiring rare earth inputs when supply uncertainty discourages long-term product development investments. This dynamic could impact competitive positioning across multiple industries.

Innovation Ecosystem Implications

Research and development priorities should emphasise material substitution and recycling technologies that reduce primary rare earth demand. These approaches offer potential competitive advantages whilst addressing supply security concerns.

International collaboration mechanisms could enable shared technology development and risk distribution across allied nations. However, intellectual property sharing and competitive dynamics create coordination challenges.

Talent acquisition strategies must account for specialised expertise requirements in rare earth processing and application development. Technical workforce limitations constrain alternative supply chain development in many jurisdictions.

Knowledge transfer dynamics between academic research and commercial application face barriers when processing technologies remain closely guarded industrial secrets. Open research initiatives may prove necessary for alternative technology development.

Strategic Recommendations for Navigating Supply Chain Dependencies

Government Policy Coordination

Critical materials stockpiling programmes should coordinate across allied nations to maximise strategic impact whilst minimising duplicate costs. Shared reserves could provide collective security against supply disruptions.

Research and development funding mechanisms require sustained commitment across political cycles to achieve meaningful technological breakthroughs. Public-private partnership models may optimise resource allocation whilst sharing development risks.

Trade policy coordination among allied nations could create sufficient market scale to justify alternative supply chain investments. Coordinated procurement policies may provide demand certainty for non-Chinese producers.

Regulatory harmonisation for environmental and safety standards could reduce development costs for alternative supply chains whilst maintaining appropriate protection levels.

Long-term Outlook and Scenario Planning

2030 market structure projections suggest continued Chinese dominance across most rare earth value chain segments. Alternative supply chains may achieve niche positions but remain unable to provide comprehensive supply security.

Technological disruption scenarios could alter competitive dynamics through breakthrough separation technologies, material substitution, or recycling innovations. However, development timelines and commercialisation risks create significant uncertainty.

Geopolitical stability assumptions underlying current supply chain strategies may prove optimistic given evolving international relationships. Contingency planning should account for various cooperation and conflict scenarios.

Success metrics for alternative supply chain development should balance supply security objectives with economic efficiency considerations. Pure cost competitiveness may prove insufficient if strategic resilience requires sustained subsidisation.

The China Northern Rare Earth Five-Year Plan represents a comprehensive strategy for maintaining and extending global market control through integrated capacity expansion, technological advancement, and strategic coordination. Western responses require sustained commitment, unprecedented international cooperation, and realistic assessment of competitive challenges that extend far beyond simple market dynamics.

This analysis contains forward-looking assessments based on publicly available information and industry analysis. Geopolitical developments, technological breakthroughs, and policy changes could significantly alter projected outcomes. Investors and stakeholders should conduct independent due diligence appropriate to their specific risk tolerance and strategic objectives.

Ready to Discover the Next Major Mineral Find?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page, showcasing exceptional market outcomes, and begin your 30-day free trial today to position yourself ahead of the market.