June 29, 2026

The Quiet Revolution in Mining Services: Why Long-Term Performance Contracts Are Reshaping Asia-Pacific Grinding Operations

The economics of mineral processing have never been straightforward, but a structural shift is underway that is changing how mine operators in Asia-Pacific think about one of their most critical cost centres. Rather than treating grinding circuit consumables as a transactional procurement exercise, a growing number of high-throughput operations are binding their liner supply to performance outcomes, sharing accountability with equipment suppliers in ways that were largely unheard of a decade ago.

This transition is visible in the accumulation of long-term service contracts across the region, with Metso Life Cycle Services agreements in Asia-Pacific representing one of the clearest examples of how the mining industry evolution is moving from product delivery toward performance partnership.

When big ASX news breaks, our subscribers know first

Defining the LCS Model: More Than a Supply Contract

At its core, a Life Cycle Services agreement is a fundamentally different commercial instrument compared to conventional equipment procurement. Under a standard supply arrangement, the supplier's obligation ends when goods are delivered and accepted. What happens to performance after that point, whether liners wear faster than expected or throughput targets are missed, falls entirely on the mine operator.

LCS structures invert this logic. The supplier retains meaningful accountability for outcomes after delivery, creating a shared interest in how the equipment performs over the duration of the contract. This is not simply a warranty extension; it is a reorganisation of who bears the financial consequences of performance shortfalls.

Two distinct LCS structures have emerged as the dominant formats deployed across Asia-Pacific operations:

- Performance-based agreements that link liner wear life and throughput benchmarks directly to contractual obligations, giving suppliers a financial stake in optimising material selection, profile design, and installation quality

- Site-adapted agreements that combine consignment stock management, pre-scheduled delivery logistics, and embedded on-site technical support tailored to the specific operational rhythms and ore characteristics of individual sites

Both structures can scale to cover the full mill liner supply across multiple grinding circuits within a single operation, making them applicable to some of the region's largest processing facilities.

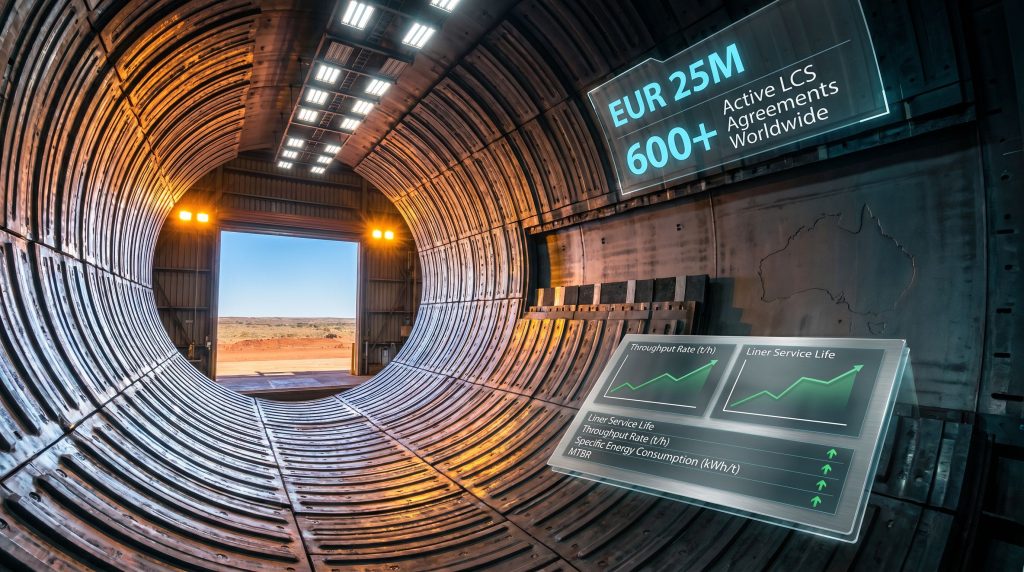

EUR 25 Million in New Deals: Breaking Down Metso's Asia-Pacific LCS Expansion

In mid-2026, Metso confirmed the signing of four new mill lining LCS agreements with unnamed operators across Asia-Pacific, with a combined value exceeding EUR 25 million. Two of the agreements were executed during 2025, with the remaining two completed in the first half of 2026. Each contract carries a duration of up to three years.

Notably, two of the four agreements incorporate performance-based guarantees, meaning that defined throughput and liner service life targets form part of the binding contractual framework rather than existing as aspirational guidance.

| Agreement Batch | Period Signed | Contract Duration | Combined Value |

|---|---|---|---|

| Two mill lining LCS deals | 2025 | Up to 3 years | Part of EUR 25M total |

| Two mill lining LCS deals | H1 2026 | Up to 3 years | Part of EUR 25M total |

| Filtration LCS (lead/zinc producer) | 2025-2026 | 4 years | Part of EUR 60M (two agreements) |

These four agreements arrive on the back of two separate multi-year LCS deals worth a combined EUR 60 million, one covering filtration services for a lead/zinc producer, announced in close proximity to the mill lining cluster. Taken together, the accumulated LCS contract value secured in the Asia-Pacific region within a twelve-month window approaches EUR 85 million, a figure that speaks to the accelerating pace of long-term service contracting adoption in the region.

Metso currently maintains more than 600 active LCS agreements globally and operates six dedicated service centres across Asia-Pacific, including what the company describes as its largest global service hub, situated in Karratha, Western Australia. In 2025 alone, Metso secured more than 100 new LCS contracts worldwide, with the Minerals segment accounting for a substantial share of that total.

The scale of service infrastructure supporting these agreements matters: embedded local capability, particularly in remote Western Australian locations, reduces the response time for liner inspections, reline scheduling, and technical advisory visits that are critical to keeping performance guarantees on track.

What Mill Liners Actually Do, and Why Performance Matters So Much

For those outside the mineral processing world, the strategic significance of grinding mill liners is not immediately obvious. Understanding why these components are the subject of multi-million euro, multi-year contracts requires a brief look at the physics involved.

Grinding mills, whether semi-autogenous (SAG), ball, or autogenous (AG) configurations, reduce ore particle size through a process of continuous impact and abrasion. The liner forms the internal protective layer of the steel mill shell, absorbing these forces and preventing catastrophic shell wear. Furthermore, as the liner erodes over time, its geometry changes, which affects the trajectory of grinding media, altering energy transfer efficiency and ultimately influencing how fine the product grind becomes.

This creates a cascade of operational consequences:

- Worn liner profiles increase energy consumption per tonne of ore processed, raising operating costs

- Unpredictable liner failure forces unplanned mill shutdowns, which in large-throughput operations can cost tens of thousands of dollars per hour in lost production

- Incorrect liner material specification for a given ore type accelerates wear cycles, compressing the window between relines and increasing maintenance labour demand

The performance indicators that LCS agreements are built around reflect exactly these sensitivities:

| Performance Indicator | Why It Matters |

|---|---|

| Liner service life (hours/tonnes processed) | Determines reline frequency and planned downtime windows |

| Throughput rate (t/h) | Core production KPI directly affected by liner condition |

| Specific energy consumption (kWh/t) | Efficiency benchmark linked to liner profile integrity |

| Mean time between relines (MTBR) | Operational planning metric for maintenance scheduling |

A less widely appreciated technical point is that liner profile geometry is not static across a liner's service life. The lifting bars that project inward from the liner surface gradually flatten as wear progresses, meaning the effective grinding action changes continuously between relines. Sophisticated liner suppliers use wear simulation modelling to design profiles that maintain acceptable grinding performance across the full wear cycle, a capability that becomes a genuine differentiator under performance-based contracts.

Risk Reallocation: How Performance Guarantees Change Commercial Dynamics

The introduction of performance guarantees into liner supply contracts represents a meaningful reallocation of commercial risk, and understanding who benefits requires looking at both sides of the arrangement.

For mine operators, the primary benefit is the conversion of a historically volatile cost centre into something more predictable. Emergency liner procurement, unplanned reline events, and the associated production losses carry substantial financial exposure. When the supplier holds contractual accountability for liner service life, the operator's exposure to these events is structurally reduced.

For suppliers like Metso, the performance-based model creates a strong internal incentive to invest in the technical disciplines that drive better outcomes: advanced wear-resistant alloy development, computational fluid dynamics modelling of liner geometry, and real-time monitoring of liner condition. Suppliers that cannot actually deliver on performance guarantees will find these contracts financially punishing, meaning the model naturally filters toward technically capable vendors.

For the broader relationship, performance follow-up obligations require ongoing data sharing between operator and supplier. Wear rate data, throughput records, and energy consumption logs become shared inputs into continuous improvement cycles. Over multi-year contract durations, this depth of operational transparency builds a collaborative dynamic that is difficult for competing suppliers to disrupt at renewal time.

Performance-based LCS agreements effectively create switching costs that are not financial but informational: the incumbent supplier accumulates site-specific wear data and operational knowledge that a new entrant cannot instantly replicate.

The Macro Forces Behind Asia-Pacific LCS Adoption

The regional appetite for Metso Life Cycle Services agreements in Asia-Pacific is not driven by a single factor but by a convergence of operational, geological, and labour market pressures that have intensified over the past several years.

Ore grade decline and increasing hardness across many of the region's established mining districts is a structural driver that receives insufficient attention in mainstream discussions of mining services demand. As open-pit operations shift toward primary sulphide processing, the copper leaching process and related comminution requirements intensify substantially. Higher Bond Work Index values translate directly into faster liner wear rates and more frequent reline cycles, making predictable liner supply and performance guarantees more commercially valuable.

Labour constraints in remote processing locations, particularly across inland and northwestern Australia, have made the embedded technical support component of LCS agreements increasingly attractive. Recruiting and retaining qualified metallurgists and maintenance specialists in fly-in, fly-out environments is expensive and unreliable. Supplier-embedded expertise effectively supplements site capability without adding to the operator's permanent headcount.

Capital discipline following the cost inflation cycle of 2021-2023 has pushed operators toward fixed-scope, predictable service contracts as a budgeting preference over variable spot procurement. The ability to model liner costs forward across a two-to-three-year horizon aligns with the cash flow discipline that equity markets have been demanding from mining companies in recent years.

The commodity mix across Asia-Pacific also shapes LCS demand in ways that are worth examining:

| Commodity Sector | Grinding Intensity | LCS Relevance |

|---|---|---|

| Copper (porphyry deposits) | Very high | High – large SAG/ball mill circuits with intensive liner wear |

| Gold (hard rock) | High | High – frequent reline cycles in high-tonnage operations |

| Lead/Zinc | Moderate-High | Moderate – filtration and grinding LCS both applicable |

| Iron Ore | Moderate | Moderate – AG mill applications with site-specific liner needs |

The next major ASX story will hit our subscribers first

Digital Infrastructure: The Enabling Layer That Makes LCS Scalable

A structural feature of LCS agreements that is rarely examined in depth is the role that digital monitoring and data infrastructure play in making performance guarantees commercially viable at scale. Indeed, data-driven mining operations are proving essential to the successful delivery of these long-term performance commitments.

Liner wear is not a linear process, nor is it uniform across a mill's internal surface. Impact zones near the feed end of a SAG mill, for example, experience dramatically different wear profiles from the discharge end liners. Without granular wear tracking, a supplier operating under a performance guarantee faces significant uncertainty about when to recommend a reline.

Remote condition monitoring, now increasingly deployed across major Asia-Pacific grinding circuits, addresses this uncertainty by enabling wear progression tracking between physical inspections. Acoustic monitoring systems can detect changes in mill charge behaviour that correlate with liner wear state, while periodic laser scanning during planned maintenance windows provides precise three-dimensional wear mapping of the liner surface.

The aggregate dataset generated across a supplier's LCS portfolio has strategic value that extends beyond individual sites. Wear rate data collected across dozens of sites processing similar ore types creates a proprietary knowledge base for predictive liner design. This accumulated knowledge represents a competitive moat that deepens over time as the LCS portfolio grows.

How Technology Is Amplifying LCS Performance

The mining efficiency gains made possible through artificial intelligence and advanced modelling are increasingly integrated into LCS delivery frameworks. Suppliers can now simulate liner wear trajectories with far greater precision than was achievable even five years ago, enabling more confident performance commitments and tighter reline scheduling. In addition, the mining technology benefits emerging from sensor innovation are translating directly into improved wear monitoring capabilities across active LCS sites.

How LCS Structures Compare Across the Contracting Spectrum

Situating LCS agreements within the broader landscape of mining services contracting helps clarify what they are and what they are not.

| Contract Model | Supplier Accountability | Duration | Performance Linkage |

|---|---|---|---|

| Spot supply | Delivery only | Single transaction | None |

| Frame agreement | Pricing certainty | 1-2 years | Minimal |

| LCS (site-adapted) | Supply + technical support | 2-3 years | Indirect |

| LCS (performance-based) | Supply + outcomes | 2-3 years | Direct – throughput/wear life |

| Full outsourcing | End-to-end operations | 5+ years | Comprehensive |

The performance-based LCS position on this spectrum is significant. It goes substantially further than the pricing certainty of a frame agreement but stops short of the comprehensive operational integration of full outsourcing arrangements. For most mine operators, this middle position offers the optimal balance between maintaining internal control of grinding circuit management and accessing the technical depth that a specialist supplier can provide.

This mirrors a transition visible across other capital-intensive industries. In commercial aviation, engine manufacturers moved toward power-by-the-hour contracts that bill airlines per hour of engine operation rather than per engine sold, retaining maintenance responsibility and internalising the financial consequences of reliability shortfalls. The mineral processing sector is following a structurally similar path, as detailed in Metso's Asia-Pacific service offering documentation.

Frequently Asked Questions: Metso Life Cycle Services in Asia-Pacific

What is a Metso Life Cycle Services agreement?

A Metso Life Cycle Services agreement bundles equipment supply, typically mill liners or filtration systems, with ongoing technical support, scheduled deliveries, and in some cases, performance guarantees tied to measurable production outcomes including throughput rates and liner service life.

How many LCS agreements does Metso currently hold globally?

Metso manages more than 600 active LCS agreements worldwide across its Minerals and Flow Control segments, with a meaningful concentration in Asia-Pacific.

What is the value of Metso's recent Asia-Pacific mill lining LCS deals?

Four mill lining LCS agreements signed across 2025 and the first half of 2026 carry a combined value exceeding EUR 25 million, with individual contract durations of up to three years.

What does a performance-based mill lining guarantee involve?

Under a performance-based structure, the liner supplier commits to defined throughput and wear life benchmarks. If targets are not met, the contractual terms may include remediation obligations or financial adjustments, creating a shared accountability framework between supplier and operator.

How does LCS differ from a standard maintenance contract?

Standard maintenance contracts typically cover reactive or scheduled servicing of existing equipment. LCS agreements are broader in scope, integrating supply chain management, technical advisory services, performance monitoring, and in some cases outcome guarantees, making them a more comprehensive operational partnership rather than a service call arrangement.

Why is Asia-Pacific a priority region for LCS expansion?

The region hosts some of the world's highest-throughput grinding operations, particularly in copper and gold processing. Combined with labour constraints in remote locations, increasing ore hardness across ageing deposits, and capital discipline preferences among publicly listed operators, the structural case for long-term performance-linked service agreements is compelling. Consequently, the Australian mining industry's deal activity illustrates how rapidly this model is being adopted across the region.

Key Takeaways: What the LCS Expansion Signals for Mining Services

The accumulation of more than EUR 85 million in LCS contract value across Asia-Pacific within approximately twelve months, combining the EUR 25 million mill lining cluster with the EUR 60 million filtration and grinding agreements, reflects a structural acceleration in long-term service contracting that goes beyond a single supplier's commercial strategy.

Several broader signals are embedded in this activity:

- Performance-based contract structures are transitioning from niche arrangements used by technically sophisticated operators to mainstream procurement instruments across high-throughput mineral processing environments

- The integration of digital wear monitoring with physical liner supply is redefining what equipment supply means in the context of modern grinding circuit management, adding a data services layer that did not exist in earlier contracting generations

- For mine operators, Metso Life Cycle Services agreements in Asia-Pacific convert a historically variable cost centre into a more predictable, performance-anchored operational expense that is easier to model and defend within capital allocation frameworks

- The switching costs embedded in long-running performance partnerships, particularly the site-specific operational knowledge accumulated by the supplier, create durable commercial relationships that extend naturally across multiple contract renewal cycles

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Figures referenced, including contract values and portfolio sizes, are sourced from publicly available company announcements and industry reporting. Readers should conduct independent research before making any investment or procurement decisions.

Want to Know Which ASX Mining Discoveries Could Deliver Outsized Returns?

As the mining services sector evolves toward performance-driven partnerships, the biggest investment opportunities often lie in the underlying discoveries powering these operations — and Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts the moment significant mineral discoveries are announced, turning complex data into actionable insights. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial to position yourself ahead of the broader market.