July 15, 2026

When the Buffer Runs Out: China's Strategic Oil Stockpile and the Coming Market Reckoning

Energy markets rarely move in straight lines. History consistently shows that the most severe price dislocations are not caused by the initial shock itself, but by the delayed unravelling of buffers that temporarily absorbed it. The 1973 Arab Oil Embargo, the 1990 Gulf War supply disruption, and the 2022 European energy crisis all followed this pattern: a supply event occurs, strategic reserves or alternative flows cushion the immediate blow, and then the true market repricing arrives weeks or months later, when those buffers are exhausted.

That delayed reckoning dynamic is precisely what China draws down billion-barrel stockpile reserves have introduced into the current global oil market. Understanding how that buffer was built, how fast it is being consumed, and what happens when Beijing decides to reverse course is essential context for anyone trying to interpret oil price signals in the second half of 2026.

When big ASX news breaks, our subscribers know first

The Architecture of China's Pre-Positioned Crude Buffer

Why China Spent More Than a Year Buying More Oil Than It Could Use

For well over a year before the U.S.-Israel military campaign against Iran began, China's crude oil import volumes consistently exceeded its refinery processing capacity by a substantial margin. This was not an accident of logistics or demand forecasting. It reflected a deliberate, sustained effort to pre-position crude inventories at scale, taking advantage of two structural advantages: globally stable oil prices and access to heavily discounted sanctioned crude from both Russia and Iran.

Tanker tracking firms and commodity analysts, who derive China's inventory levels by comparing gross import flows against reported refinery throughput rates, estimated that China was accumulating surplus crude at a pace of between 900,000 and 1.1 million barrels per day throughout much of 2024 and 2025. Over a sustained accumulation period, that rate compounds into a reserve position of extraordinary size.

Key Methodology Note: Because China treats its strategic petroleum reserve data as sensitive national security information, no direct inventory figures are officially published. Unlike the United States, which releases weekly Energy Information Administration (EIA) inventory reports, China provides no equivalent public disclosure. Analysts must therefore infer stockpile levels by measuring the differential between crude import volumes and refinery throughput statistics. When imports persistently exceed processing capacity, the surplus is attributed to inventory accumulation. This methodology, used by firms including Kpler and Vortexa, represents the primary analytical lens through which China's oil buffer is assessed.

How Sanctioned Crude From Russia and Iran Fuelled the Inventory Build

The economics of China's stockpile campaign were materially enhanced by access to discounted crude from sanctioned producers. Russian Urals crude and Iranian heavy grades, both trading at substantial discounts to Brent benchmarks throughout this period, provided China's state refiners and independent teapot refineries with a cost advantage unavailable to European or Japanese buyers. Furthermore, China oil market dynamics created an arbitrage opportunity that Beijing exploited systematically, importing volumes well above its operational requirements and directing the surplus into storage infrastructure.

The geopolitical dimension of this strategy extends beyond pure economics. China's willingness to absorb sanctioned crude at scale served dual purposes: reducing its effective import cost per barrel while simultaneously building the strategic reserve depth that would later allow it to weather a major supply disruption without catastrophic economic damage.

Storage Infrastructure Expansion: The 11 New Facilities and 169 Million Barrel Capacity Target

The scale of China's inventory ambitions is reflected in its infrastructure investment programme. As reported by Reuters, China was actively constructing 11 new oil storage facilities, targeting 169 million barrels of additional storage capacity, with completion targeted by the end of 2026. This new build adds to the 180 to 190 million barrels of additional storage capacity that had already come online between 2020 and 2024, according to data from Kpler and Vortexa.

Taken together, this infrastructure expansion programme reflects a strategic decision made at the highest levels of Chinese economic planning: that physical crude inventory, held domestically and insulated from external supply chain disruptions, represents a core element of national energy security. The 169 million barrel target for new capacity alone equates to roughly two weeks of China's pre-war import volumes, providing meaningful additional runway in precisely the kind of supply shock scenario that subsequently materialised.

How Severe Is the Import Collapse? A Data-Driven Breakdown

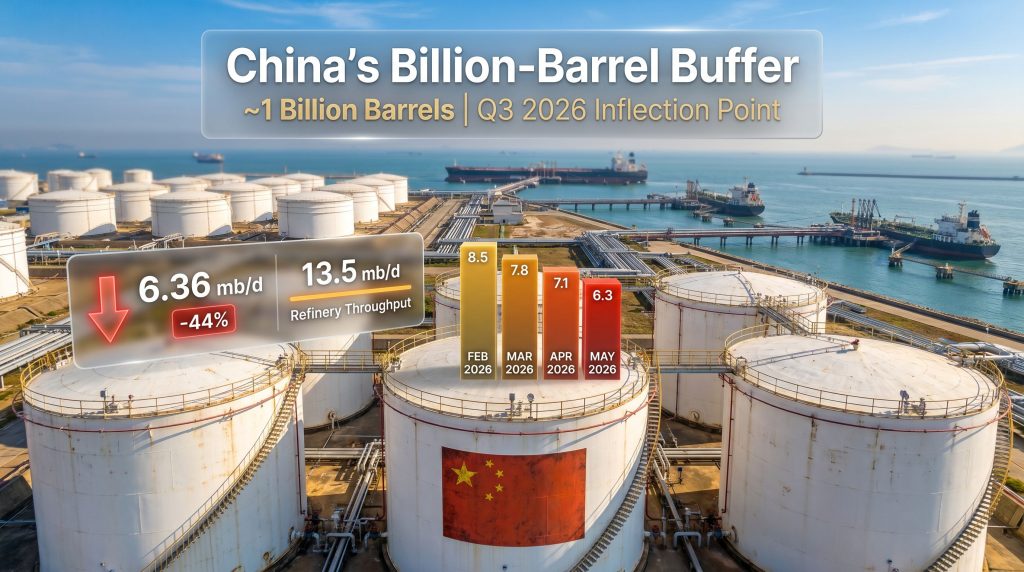

China's Crude Import Trajectory: February to May 2026

The speed and scale of China's import contraction following the outbreak of hostilities is among the most dramatic demand shifts in modern oil market history. Kpler data cited by Reuters analyst Clyde Russell illustrates the progression:

| Month | Estimated Daily Imports (mb/d) | Change vs. February |

|---|---|---|

| February 2026 (pre-conflict) | 11.39 | Baseline |

| March 2026 | ~10.5 (est.) | ~-8% |

| April 2026 | 8.10 | -29% |

| May 2026 | 6.36 | -44% |

Within three months of the conflict's onset, China's daily crude imports had fallen by more than 5 million barrels per day, representing a contraction of over 44% from the pre-war baseline. For context, 5 million barrels per day is roughly equivalent to the total daily crude production of Iraq, one of OPEC's largest producers.

The Refinery Throughput Paradox: Processing 13.5 mb/d While Importing Just 6.36 mb/d

The import collapse takes on its most analytically significant dimension when placed against China's concurrent refinery throughput data. According to Kpler, Chinese refineries processed approximately 13.5 million barrels of crude per day in May 2026, even as imports fell to just 6.36 million barrels per day.

Featured Snippet: China's refineries processed approximately 13.5 million barrels of crude per day in May 2026, while importing only 6.36 million barrels per day. The gap of more than 7 million barrels daily is being bridged entirely by strategic inventory drawdowns, representing one of the largest single-nation stockpile deployment events in oil market history.

This means that for every barrel of crude China imported in May 2026, its refineries were processing more than two. The arithmetic gap of over 7 million barrels per day between processing rates and import volumes reveals the true scale of the inventory drawdown underway. Refinery throughput did decline modestly, by an estimated 154,000 barrels per day from April and by 1.9 million barrels per day compared to May 2025 levels. However, those declines are fractional relative to the import contraction, confirming that China's refining sector has remained operationally robust by drawing on pre-positioned stockpiles.

What Is Driving the Import Collapse? Supply Shock vs. Demand Destruction

Separating Geopolitical Supply Disruption From Genuine Demand Weakness

One of the most consequential analytical errors in oil market commentary during supply shock events is conflating import weakness with demand destruction. When a country deploys domestic stockpiles to substitute for imported crude, its import volumes fall sharply even as industrial consumption and refinery output hold steady. The surface-level data pattern looks identical to a demand collapse, but the underlying economic reality is fundamentally different.

Critical Distinction: A sharp decline in crude imports does not necessarily signal weakening industrial demand. When pre-positioned inventories absorb the supply shortfall, refinery throughput can remain elevated while import volumes fall dramatically. Analysts and investors who treat China's May 2026 import figures as evidence of an economic slowdown risk significantly misjudging both the current market equilibrium and the future demand trajectory.

China's continued refinery throughput of 13.5 mb/d in May 2026 is the definitive evidence that domestic energy demand has not collapsed commensurately with the import decline. The country's industrial base continues to process crude at broadly comparable rates to prior periods, sustained entirely by inventory deployment rather than import recovery.

How the U.S.-Israel-Iran Conflict Restructured Middle Eastern Crude Flow Patterns

The conflict has fundamentally disrupted the routing of Middle Eastern crude to Asian markets. The broader consequences of US-China oil tensions have compounded the disruption of Iranian supply availability, whilst heightened risks to Strait of Hormuz transit have compressed the pool of accessible barrels for all Asian importers.

Chevron's chief executive confirmed that multiple ships had been attacked in the Strait of Hormuz, a development that has materially elevated war risk insurance premiums for tankers transiting the waterway. The Hormuz chokepoint, through which approximately 20% of global oil trade transits daily, has consequently become a variable that compounds the underlying supply shock with logistical uncertainty.

Asia's Disproportionate Exposure: Why the Gulf Supply Disruption Hits Eastern Markets Hardest

Asia's dependence on Middle Eastern crude is structurally higher than that of any other major importing region. European importers have access to North Sea, West African, and Caspian alternatives; North American refiners benefit from proximity to Western Hemisphere production. Asian importers, by contrast, are geographically and economically oriented toward Gulf barrels, making any sustained disruption to Middle Eastern flows disproportionately consequential for the region.

| Country | Response Mechanism | Import Impact |

|---|---|---|

| Japan | Crude imports fell approximately 66% in April 2026 | Severe disruption |

| India | Exploring alternative supply sources; LNG push accelerated | Partial substitution underway |

| Philippines | Received first non-Iranian cargo following the Hormuz disruption | Supply rerouting initiated |

| China | Drawing down estimated 1 billion barrel strategic stockpile | Imports halved; throughput maintained |

Japan's import collapse of approximately 66% in April 2026 is particularly striking, given that Japan holds far smaller strategic reserve buffers relative to its consumption than China does. India's central bank has formally warned that the oil price shock poses a meaningful threat to the country's growth trajectory, with analysts estimating that oil at $90 per barrel could push Indian inflation to 4.8% and constrain GDP expansion.

Scenario Modelling: How Long Can China's Stockpile Absorb the Shortfall?

Three Scenarios for the Drawdown Trajectory

The duration of China's inventory buffer depends critically on the rate at which it is being consumed and whether Beijing elects to modulate refinery throughput as a conservation mechanism. Three scenarios frame the plausible range of outcomes:

Scenario 1: Rapid Depletion (High Drawdown Rate Sustained)

- Daily drawdown of approximately 7 mb/d continues through Q3 2026

- Operational buffer approaches depletion within 140 to 150 days from conflict onset

- China compelled to re-enter global crude markets aggressively by August or September 2026

- Highest risk of abrupt demand reversal and associated price spike

Scenario 2: Managed Drawdown (Refinery Throughput Moderated)

- China reduces refinery utilisation by 10 to 15% to conserve inventory

- Daily drawdown pressure reduced to approximately 5.5 to 6 mb/d

- Buffer extended through Q4 2026, allowing more orderly market re-entry

- Gives Beijing greater flexibility to time replenishment when geopolitical conditions stabilise

Scenario 3: Partial Supply Restoration (Alternative Crude Routes Activated)

- Partial restoration of non-Iranian Gulf flows or accelerated Russian pipeline volumes

- Import recovery to approximately 8 to 9 mb/d reduces the drawdown burden

- Strategic stockpile preserved near minimum operational thresholds into early 2027

- Lowest near-term price shock risk, but still implies eventual replenishment demand

Key Variable: What Constitutes China's Minimum Operational Reserve Threshold?

A critical and underappreciated variable in the depletion timeline is Beijing's internal definition of the minimum acceptable strategic inventory level. China's decision to begin reversing its import decline will almost certainly be triggered not by actual depletion, but by the approach of some internally defined reserve floor below which Beijing considers national energy security to be at risk.

Strategic Parallel: The U.S. Strategic Petroleum Reserve drawdown following the 2022 energy crisis demonstrated the operational and political risks of depleting national crude buffers below threshold levels. The SPR fell to its lowest level in approximately four decades before the release programme was curtailed. Beijing, having observed this experience and built its own reserve architecture with considerably greater deliberateness, is widely expected to act well before reaching a comparable depletion point.

The Price Suppression Effect: China's Stockpile as Phantom Supply

Why Brent Has Not Yet Reached $150 Per Barrel Despite a Major Supply Shock

From a pure supply-demand arithmetic standpoint, the removal of Iranian crude volumes from accessible global supply, combined with the Hormuz transit risk premium and the broader Gulf disruption, should have produced a far more severe Brent crude price spike than markets have actually experienced. The reason that Brent has not yet breached $150 per barrel lies almost entirely with China's inventory deployment strategy.

By substituting approximately 7 million barrels per day of domestic stockpile for imported crude, China has effectively removed that volume from global spot market demand. This functions as phantom supply from the perspective of international benchmarks: refinery demand is satisfied, but no incremental buying pressure is placed on global markets. The dampening effect is substantial enough that Goldman Sachs has maintained a view that near-term demand destruction dynamics are partially offsetting supply shock risks, whilst HSBC has flagged what it characterises as a potential super-squeeze in oil markets if the current equilibrium breaks down.

In addition, monitoring crude oil price trends has become increasingly important for analysts trying to gauge the true trajectory of Brent benchmarks amid this dynamic. Rystad Energy has taken a more aggressive stance, projecting that a re-escalation of the U.S.-Iran conflict could drive oil prices to $180 per barrel by August 2026 if supply constraints intensify.

Historical Comparison: China's Role vs. IEA Coordinated Reserve Releases

| Mechanism | Volume Released | Duration | Price Impact |

|---|---|---|---|

| IEA Coordinated Release (2022) | ~180 million barrels total | ~6 months | Limited short-term dampening |

| China Inventory Drawdown (2026 est.) | ~1 billion barrels total buffer | Ongoing through 2026 | Significant Brent price ceiling effect |

The scale differential between the IEA's 2022 coordinated release and China's current unilateral drawdown is instructive. The IEA mobilised approximately 180 million barrels across its member states, an effort that was broadly acknowledged to have provided only temporary and limited price relief. China's estimated billion-barrel buffer is roughly five times larger and is being deployed by a single actor with no multilateral coordination requirements, making it a structurally more powerful market intervention.

The next major ASX story will hit our subscribers first

What Happens When China Returns to the Market?

The Inventory Replenishment Imperative

The central forward-looking question for global oil markets is not whether China will return to international crude markets, but precisely when that reversal will occur and at what volume. A country that has built strategic petroleum infrastructure with the deliberateness and scale that China has demonstrated is not going to allow those reserves to remain depleted. The replenishment imperative is essentially certain; only the timing is variable.

Featured Insight: Once China's strategic crude stockpiles approach operational minimums, estimated by analysts to occur sometime in Q3 2026, Beijing will face a binary choice: accept the economic exposure of chronically low reserves, or return to global markets as an aggressive buyer. History and policy logic both strongly favour the latter. A return to pre-conflict import volumes of approximately 11 mb/d would inject roughly 5 million barrels per day of incremental demand into an already supply-constrained global market.

The July 2026 Inflection Point: Why Q3 Is the Critical Window

A growing number of energy analysts have identified July 2026 as the inflection point at which the deferred price impact of the Iran war supply shock is likely to become fully palpable in international benchmarks. The convergence of several factors makes Q3 2026 the highest-risk period for an upward price dislocation:

- China's drawdown clock advances toward the estimated operational reserve floor

- Summer peak demand season amplifies global consumption in the Northern Hemisphere

- The IEA has warned that global oil stocks are tracking toward historical lows ahead of this peak demand period

- OPEC's market influence through production surges from Iraq, the UAE, and Saudi Arabia are not expected to fully materialise until 2027

- Shipping insurance and tanker availability constraints persist around the Strait of Hormuz

New Storage Capacity: How 169 Million Barrels of Infrastructure Changes the Calculus

The 11 new storage facilities under construction, targeting 169 million barrels of additional capacity by end-2026, introduce an important strategic dimension to China's re-entry calculus. If geopolitical conditions stabilise sufficiently to allow Gulf crude flows to partially recover, China will not merely replenish its existing reserves. It will have the physical infrastructure to continue expanding its strategic buffer beyond pre-war levels, potentially using a period of price normalisation as an opportunity to buy aggressively into new storage at scale.

This possibility — that China's re-entry into global markets could be motivated not only by operational necessity but by opportunistic long-term accumulation — represents a scenario with more sustained bullish price implications than a simple replenishment cycle would suggest. Furthermore, the trade war oil impact on Beijing's broader energy strategy means that replenishment decisions are unlikely to be taken in isolation from wider geopolitical considerations.

Russia's Dual Role and the Dependency Risk

China's Energy Lifeline and Its Structural Vulnerability

Russia has functioned as a critical alternative crude source for China throughout the conflict period, with pipeline volumes and arctic tanker flows providing a partial substitute for disrupted Gulf barrels. However, this reliance introduces its own strategic vulnerability. Russia's ability to sustain elevated export volumes is constrained by domestic refinery prioritisation, the impact of Ukrainian drone strikes on Russian refining infrastructure, and the finite capacity of Eastern pipeline routes.

Russian pipeline capacity to China via the Eastern Siberia-Pacific Ocean (ESPO) pipeline runs at approximately 1.6 million barrels per day, a meaningful volume but insufficient on its own to bridge a gap of 5 million barrels per day created by the import collapse. According to analysis from Columbia University's Energy Policy programme, China's Russia dependency therefore provides partial offset but not full supply restoration, reinforcing the strategic stockpile's indispensable role in the current equilibrium.

Frequently Asked Questions: China's Oil Stockpile and the Iran Supply Shock

How much crude oil has China stockpiled?

Analysts estimate China accumulated approximately 1 billion barrels of surplus crude above operational requirements during a sustained pre-conflict buying campaign in 2024 and 2025, accumulating at a rate of approximately 900,000 to 1.1 million barrels per day throughout that period.

Why did China's crude imports fall by more than 44%?

The conflict between the U.S.-Israel alliance and Iran severely disrupted Middle Eastern crude supply chains, restricting the availability of Iranian and Gulf-origin barrels that China had been importing at high volumes. The import decline reflects both constrained supply availability and China's deliberate substitution of domestic stockpiles for imported crude.

Is China's reduced oil import level permanent or temporary?

The import reduction is assessed as temporary by virtually all major energy analysts. China's refinery throughput has remained elevated relative to imports, confirming that domestic consumption has not declined commensurately. Once stockpiles approach minimum operational thresholds, import volumes are expected to recover sharply.

What would happen to oil prices if China re-enters the market at full volume?

A return to pre-conflict import levels of approximately 11 mb/d would add roughly 5 million barrels per day of incremental demand to an already supply-constrained global market. Analysts have flagged this as a potential catalyst for significant upward repricing, with Rystad projecting prices as high as $180 per barrel under sustained re-escalation scenarios.

Why doesn't China report its strategic oil inventory levels?

China treats strategic petroleum reserve data as sensitive national security information, with no public disclosure equivalent to the U.S. weekly EIA inventory reports. Analysts must infer stockpile levels from the differential between import data and refinery throughput statistics, a methodology that introduces inherent estimation uncertainty.

Key Takeaways: The Deferred Price Shock and What It Means for Markets

China draws down billion-barrel stockpile reserves in a manner that has functioned as one of the most powerful single-actor price stabilisation mechanisms in modern oil market history. By substituting domestic inventory for imported crude at a rate exceeding 7 million barrels per day, Beijing has effectively placed a ceiling on Brent crude benchmarks during the acute phase of the Iran supply shock, preventing the kind of immediate price spike that would otherwise have accompanied a disruption of this magnitude.

However, that ceiling is finite and time-limited. Three structural realities define the path ahead:

- The drawdown clock is advancing. Every day that Chinese refineries process 13.5 mb/d while importing 6.36 mb/d, the buffer shrinks. Depletion toward operational minimums in Q3 2026 is the base case for most analysts.

- The replenishment imperative is non-negotiable. Beijing's investment in storage infrastructure and its demonstrated commitment to strategic reserve depth make a sustained depleted inventory position politically and strategically untenable.

- The global supply environment into which China re-enters matters enormously. The IEA has warned that global stocks are approaching historical lows ahead of summer peak demand. If China's buying surge coincides with continued Hormuz disruption and delayed OPEC+ volume recovery, the price implications could be severe.

Forward-Looking Summary: The real oil price shock from the Iran war may still be ahead of markets, not behind them. China draws down billion-barrel stockpile reserves to absorb the blow in the near term. When the time comes to replenish those reserves, the question of where Brent crude trades will no longer be moderated by phantom supply. It will be determined by the raw arithmetic of a supply-constrained market suddenly facing one of its largest buyers returning at full force.

This article contains forward-looking analysis and scenario projections based on publicly available data and analyst commentary. All price forecasts and depletion timelines represent analyst estimates, not guaranteed outcomes. Readers should conduct their own independent research before making any investment or commercial decisions based on the information presented here.

Want to Stay Ahead of the Next Major Market-Moving Discovery?

While geopolitical shocks reshape global energy and commodity markets, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex data across 30+ commodities into clear, actionable insights for investors at every level. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major market opportunity.