July 15, 2026

When Physical Scarcity Meets Financial Innovation: The New Architecture of Platinum Pricing

Commodity markets have long operated on the assumption that price discovery belongs to whoever controls the benchmark. For platinum, that power has historically resided in Western financial centres, with the London Platinum and Palladium Market (LPPM) setting the reference price that producers, refiners, and industrial buyers around the world relied upon. That architecture is now being fundamentally challenged — not through geopolitical pressure or regulatory intervention, but through the mechanics of physical scarcity meeting a new financial instrument with genuine delivery teeth.

Understanding why China platinum futures demand has become one of the most consequential developments in global commodity markets requires starting not with the futures contract itself, but with what makes platinum structurally different from most other metals. It cannot be easily substituted, cannot be quickly expanded in supply, and once absorbed into the Chinese domestic market, cannot re-enter international supply chains through conventional trade channels.

When big ASX news breaks, our subscribers know first

The GFEX Contract: A Structurally Different Instrument

Most observers focused on the launch date of 27 November 2025, when the Guangzhou Futures Exchange introduced China's first domestically settled platinum futures contract. However, the more instructive detail lies in the contract's physical specifications, which distinguish it from virtually every comparable instrument in global commodity markets.

The GFEX platinum contract accepts industrial-grade sponge platinum alongside refined bars for physical delivery. This dual-grade acceptance is a world-first in precious metals futures design. Sponge platinum — a porous, lower-processed form of the metal that sits closer to the refinery output stage than polished bars — is the form in which most industrial-scale platinum moves through supply chains.

By accepting sponge platinum, the GFEX dramatically lowered the barrier to entry for physical delivery, enabling industrial producers and mid-tier refiners to participate in the delivery mechanism without incurring the additional cost of upgrading material to bar specification. Furthermore, the contract is open to international participants, a feature that creates a direct arbitrage bridge between Chinese domestic pricing and Western benchmarks — a bridge that has been consistently profitable since the contract's inception.

What Are the Key Structural Features?

Key structural features that differentiate the GFEX platinum contract include:

- Settlement format: Physically delivered, not cash-settled, creating direct linkage between derivatives positions and real metal

- Grade eligibility: Sponge platinum and refined bars both qualify, broadening the supply base eligible for delivery

- Participant access: Open to international entities, unlike many domestically restricted Chinese commodity instruments

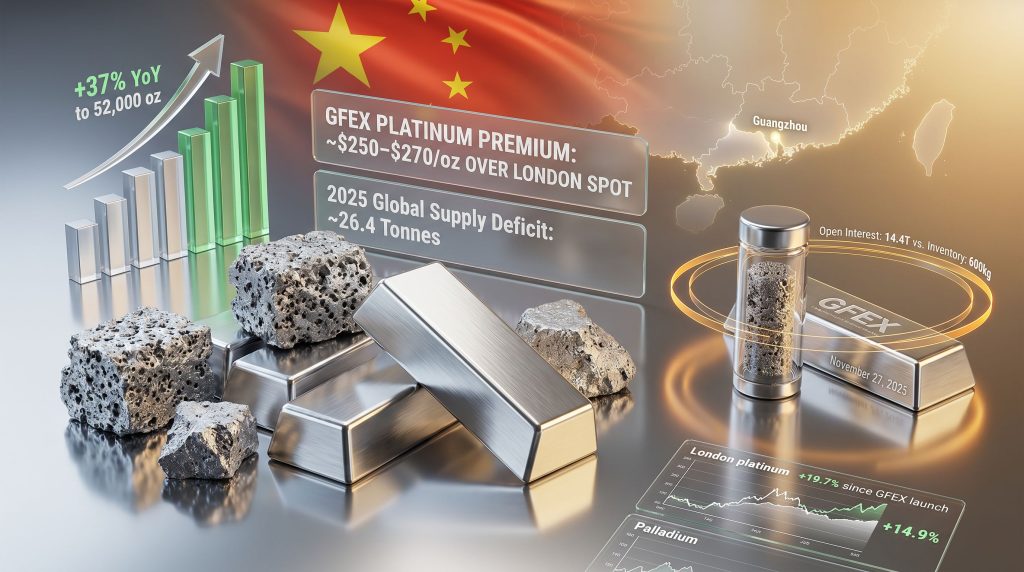

- Price premium: GFEX pricing has traded at approximately $250–$270/oz above Western spot benchmarks on a sustained basis

- Mandate origin: Launched under the Guangzhou Futures Exchange, which also hosts China's lithium carbonate and industrial silicon contracts, establishing a pattern of new economy commodity focus

When a futures contract sustains a premium of more than 20% over the internationally recognised benchmark, the market is communicating something specific: physical metal available domestically is insufficient to meet demand at global prices. This is not speculative froth. It is a real-time scarcity signal embedded in contract mechanics.

Understanding the broader precious metals market structure helps contextualise how unusual this sustained premium truly is.

Mapping the Supply Deficit: Numbers That Demand Attention

The structural backdrop against which the GFEX contract launched is one of sustained and deepening undersupply. The projected 2025 global platinum supply deficit stands at approximately 26.4 tonnes — a figure that places the market in territory where incremental demand shifts produce outsized price responses.

China's role in this equation is not peripheral. The country accounts for approximately 60% of global platinum demand, concentrated heavily in industrial applications across automotive, chemical, electronics, and increasingly, clean energy sectors. When a single country represents the majority of demand for a commodity facing a multi-decade supply deficit, the price discovery implications are significant.

The GFEX data as of late May 2026 illustrates the severity of the imbalance in precise terms:

| Metric | Data Point |

|---|---|

| June 2026 Contract Open Interest | ~14.4 tonnes |

| GFEX Warehouse Inventory on Warrant | ~600 kilograms |

| Open Interest-to-Inventory Ratio | ~24:1 |

| Projected 2025 Global Supply Deficit | ~26.4 tonnes |

| Chinese Investment Demand Growth (2024 YoY) | +37% to 52,000 oz |

| Forecasted Chinese Investment Demand (2025) | ~60,000 oz |

Why Does the 24:1 Ratio Matter?

The open interest-to-inventory ratio of approximately 24:1 is the most operationally significant figure in this dataset. In commodity markets, ratios above 10:1 are generally considered precursors to delivery stress, where short-position holders face expiry without sufficient physical metal available for settlement. At 24:1, the June 2026 GFEX platinum contract is operating at more than double that stress threshold.

Compounding this pressure is the concentration of available warehouse inventory. China Platinum Co., a state-owned trading entity, holds the majority of the limited 600-kilogram stockpile currently warehoused on the exchange. This concentration means that access to deliverable metal is effectively controlled by a single participant, introducing a structural asymmetry in any delivery negotiation.

The Arbitrage Corridor Pulling Metal Into China

The mechanics driving physical delivery demand on the GFEX contract are rooted in a straightforward economic calculation. A persistent and substantial price spread between London spot prices and GFEX domestic prices creates a profitable arbitrage pathway for market participants who can source platinum internationally and deliver it into Chinese warehouses.

Wang Yanhui, General Manager at Shenzhen Yuexin Precious Metals Co. Ltd — one of China's largest precious metals refiners — confirmed to Bloomberg News in May 2026 that large numbers of speculators and industrial clients holding short platinum positions were actively selecting physical delivery over position closure because the economics favoured it. The spread between London spot pricing and the domestic GFEX benchmark was the key driver of that calculation.

This behaviour is self-reinforcing in a way that distinguishes it from typical speculative commodity cycles:

- Short-position holders elect physical delivery rather than closing positions, driven by the price spread

- Physical delivery elections draw down available warehouse inventory

- Lower inventory tightens the supply available for future deliveries

- The GFEX premium widens further as scarcity intensifies

- The wider premium makes the arbitrage corridor even more attractive, pulling additional metal into China

- International supply tightens, reinforcing upward pressure on global benchmarks

Shenzhen Yuexin's operational scale provides important context. The company produced approximately 20 tonnes of platinum and approximately 200 tonnes of gold in 2025, positioning it as a critical intermediary between international mine supply and domestic delivery obligations. Wang confirmed that industrial clients were approaching the refiner seeking long-term supply contracts specifically to secure forward platinum availability — behaviour consistent with a market transitioning from spot procurement to strategic supply security.

The shift from spot purchasing to long-term contract procurement is one of the most reliable behavioural signals in commodity markets. When industrial buyers begin locking in forward supply at current prices, they are signalling a belief that future availability will be more constrained and more expensive than it is today.

Sponge Platinum: The Grade Specification That Changes Everything

One of the least discussed but most consequential features of the GFEX contract is its acceptance of sponge platinum as a deliverable grade. Platinum extracted from ore undergoes a series of processing stages. After initial concentration and smelting, the metal passes through a refining process that produces platinum sponge — a porous, high-surface-area form of the metal with purity typically exceeding 99.95% but in a physical form distinct from the polished bars and ingots traded on traditional precious metals exchanges.

Sponge platinum is the preferred commercial form for industrial catalytic applications precisely because its high surface area makes it more effective as a catalyst in chemical reactions and fuel cell systems. By accepting sponge platinum for delivery, the GFEX created a direct pipeline from industrial production to exchange warehouses, bypassing the additional melting, casting, and assaying steps required to produce bar-form platinum.

This reduces delivery costs, shortens supply chain timelines, and expands the pool of market participants capable of physically settling contracts. It also means that Chinese industrial buyers who take delivery receive platinum in precisely the form they need for manufacturing, eliminating intermediate processing steps. Consequently, this specification reflects sophisticated market design thinking — the contract was built not just for financial traders but for the industrial ecosystem that drives China's genuine physical demand.

China's Green Economy and the Structural Demand Floor

The investment demand figures, while growing rapidly, represent only one layer of China's platinum consumption story. The more durable demand driver is industrial, rooted in the country's clean energy transition across multiple technology verticals. Indeed, energy transition demand across China's industrial base is increasingly anchoring the structural floor for platinum consumption.

Platinum's role in proton exchange membrane fuel cell systems is particularly significant. In PEM fuel cells, platinum serves as the primary electrocatalyst at both the anode and cathode, enabling the electrochemical conversion of hydrogen into electricity. There is currently no commercially viable substitute for platinum in high-performance PEM systems at scale. The PEM technology expansion across China's hydrogen vehicle and stationary power sectors effectively sets an industrial demand floor that operates independently of short-term price sensitivity.

What Other Industrial Demand Sources Exist?

Additional structural demand sources include:

- Automotive catalytic converters: Ongoing internal combustion and hybrid vehicle production maintains substantial baseline demand, particularly as emission standards tighten

- Chemical industry catalysts: Platinum group metals catalyse nitric acid production and a range of petroleum refining and petrochemical processes

- Electronics manufacturing: Hard disk drives, specialty glass production, and semiconductor manufacturing consume platinum in technically irreplaceable quantities

- Emissions control systems: Industrial and power generation facilities operating under tightening environmental frameworks require platinum-based catalytic reduction systems

Layered over these industrial demand sources is Beijing's long-standing policy of restricting platinum exports. Metal that enters China through import channels does not return to international supply through conventional trade, effectively removing it from the globally available pool on a semi-permanent basis. As GFEX delivery volumes compound this one-way flow dynamic, the pressure on international supply intensifies with each contract cycle.

The next major ASX story will hit our subscribers first

From Price-Taker to Price-Setter: The Geopolitical Dimension

The repricing of platinum following the GFEX launch has not been confined to the Chinese domestic market. London benchmark prices rose approximately 19.7% in USD terms following the contract's introduction, while palladium markets recorded a correlated gain of approximately 14.9%, reflecting broader recalibration of platinum group metals sentiment across global markets. The platinum and palladium dynamics at play here represent a genuine structural shift rather than a cyclical bounce.

Initial GFEX trading sessions saw domestic prices reach approximately ¥430.30/g (roughly $1,890/oz) against a global spot price of approximately $1,554/oz, representing a launch premium of roughly 21.6%. That premium has since stabilised at approximately $250–$270/oz but has not converged toward parity, indicating that the structural scarcity driving China platinum futures demand has not been resolved by international supply flows.

The geographic concentration of platinum mine supply amplifies the significance of this repricing. South Africa accounts for approximately 70–75% of global platinum mine output, meaning that a sustained elevation of the global price floor driven by Chinese futures demand translates directly into material revenue uplift for South African platinum group metals producers.

Scenario Framework: Where Platinum Prices Go From Here

No supply-demand analysis carries certainty, and the platinum market contains multiple variables that could shift price trajectories materially in either direction. The following scenario framework captures the range of plausible outcomes, and applying sound commodity hedging strategies remains essential for participants navigating this environment.

| Scenario | Trigger Conditions | Price Implication |

|---|---|---|

| Accelerated Tightening | GFEX delivery volumes exceed warehouse replenishment capacity | Significant upside; further premium expansion likely |

| Base Case Deficit | Supply deficit persists near 26 tonnes; modest demand growth | Sustained elevated prices; gradual benchmark repricing |

| Demand Softening | Chinese industrial slowdown or policy reversal | Near-term correction; structural floor remains |

| Supply Response | South African output expansion or recycling surge | Partial relief; deficit closure unlikely within 24 months |

What Does This Mean for Industrial Buyers and Investors?

The June 2026 GFEX contract expiry represents the first genuine stress test of the physical delivery infrastructure. For industrial buyers in automotive, hydrogen, and electronics sectors, the strategic implication is clear: the era of relying on spot market availability to meet manufacturing requirements is closing.

The combination of structural supply deficits, GFEX-driven demand absorption, and one-way export restrictions creates a procurement environment where forward contracting is no longer optional risk management but essential supply security strategy. For investors, meanwhile, platinum's dual identity as both an industrial input and a monetary metal offers portfolio characteristics distinct from gold or silver. It is leveraged to the green economy transition, sensitive to Chinese industrial policy, and priced through a market structure that is actively repricing global benchmarks from an entirely new geographic centre of gravity. You can track live platinum price data to monitor how these structural forces continue to influence the market.

China platinum futures demand, in this context, is not simply a trading story. It is a structural repricing event with multi-year implications for producers, industrial buyers, and investors operating across the full platinum value chain.

Disclaimer: This article contains forward-looking statements, forecasts, and scenario projections that involve inherent uncertainty. Nothing in this article constitutes financial advice. Readers should conduct their own due diligence and consult qualified financial professionals before making investment decisions. Commodity prices are subject to significant volatility and past performance is not indicative of future results.

Want to Position Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex commodity data into actionable insights for both short-term traders and long-term investors. Explore historic examples of major discoveries and their market returns, then start your 14-day free trial at Discovery Alert to secure your edge before the broader market moves.