May 11, 2026

Frontier Basin Economics and the Art of Timing an Entry

In deepwater exploration, timing rarely follows a straight line. Capital cycles in offshore oil markets tend to compress years of geological promise into narrow windows of commercial opportunity, then snap shut when commodity prices retreat, balance sheets tighten, or competing basins offer faster returns. Understanding when a frontier market transitions from geological curiosity to genuine investment target requires watching a specific constellation of signals: improved subsurface data quality, the arrival of a credible anchor operator, a commercially attractive fiscal structure, and renewed IOC appetite for long-cycle exploration risk.

All four of those signals are converging simultaneously in the waters off São Tomé and Príncipe in 2026, and the country's São Tomé offshore licensing round for Blocks 7, 8, and 9 is the mechanism through which that convergence is being tested against real capital allocation decisions.

When big ASX news breaks, our subscribers know first

Why the Gulf of Guinea's Smallest Nation Is Attracting Offshore Capital in 2026

The Micro-State With a Macro-Scale Geological Position

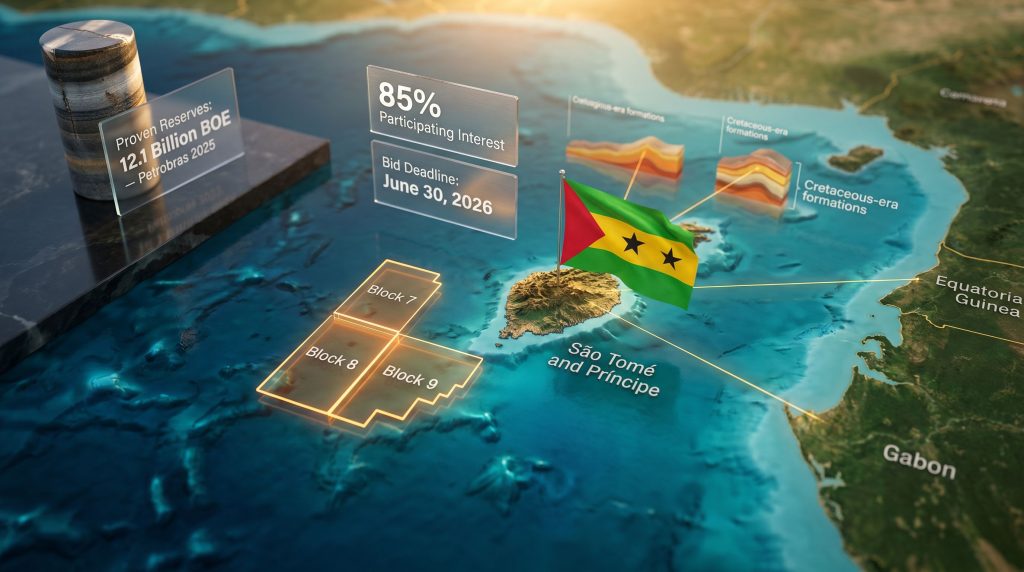

São Tomé and Príncipe (STP) occupies a deceptively important geographic position in the Gulf of Guinea. Despite a land area of approximately 1,001 km² and a population of roughly 230,000 people, the country controls a substantial Exclusive Economic Zone (EEZ) whose subsurface geology sits within the same Cretaceous-era rift corridor that has generated long-established hydrocarbon production in neighbouring Gabon and Equatorial Guinea.

This is the fundamental paradox at the heart of STP's upstream ambitions: the country's onshore footprint is negligible, yet its offshore acreage occupies a petroleum system of genuine regional significance. For IOCs managing frontier exploration portfolios across West Africa's Atlantic margin, that asymmetry creates an interesting entry calculus, particularly when the fiscal terms are structured to offset exploration risk.

The Regional Exploration Renaissance Providing Tailwinds

STP's 2026 licensing round is not unfolding in isolation. A broader re-engagement with underexplored African Atlantic margin acreage has been building momentum across multiple jurisdictions simultaneously. The broader commodity outlook for energy resources further supports this trend, as investor appetite for frontier exploration continues to grow:

- Namibia's Orange Basin has attracted major discovery announcements from TotalEnergies and Shell, fundamentally repositioning sub-Saharan Atlantic Africa as a credible deepwater exploration destination

- Angola's ultra-deepwater acreage continues to attract capital from large-scale operators extending their existing footprint

- Côte d'Ivoire's offshore shelf and deepwater areas are hosting multiple active IOC campaigns

- South Africa's frontier offshore plays are drawing renewed technical evaluation

This regional momentum matters for STP specifically because IOC exploration teams rarely evaluate frontier acreage in isolation. When a basin corridor generates fresh discovery news in adjacent jurisdictions, the technical confidence to evaluate analogous plays in under-drilled areas increases measurably. STP's geological alignment with this corridor makes it a natural candidate for the next wave of attention.

Industry observers noted in May 2026 that new seismic surveys and drilling programs could commence in STP's waters as early as late 2026, contingent on bid round outcomes. (Ecofin Agency, May 11, 2026)

The Geological Case for Blocks 7, 8, and 9

Cretaceous Targets and Basin Analogue Confirmation

The three blocks on offer, all situated in the western portion of STP's EEZ, share structural and stratigraphic characteristics with producing formations in Gabon and Equatorial Guinea, according to the African Energy Chamber, which has publicly noted this geological alignment as a substantive credibility signal for technically-driven exploration teams. (Ecofin Agency, May 11, 2026)

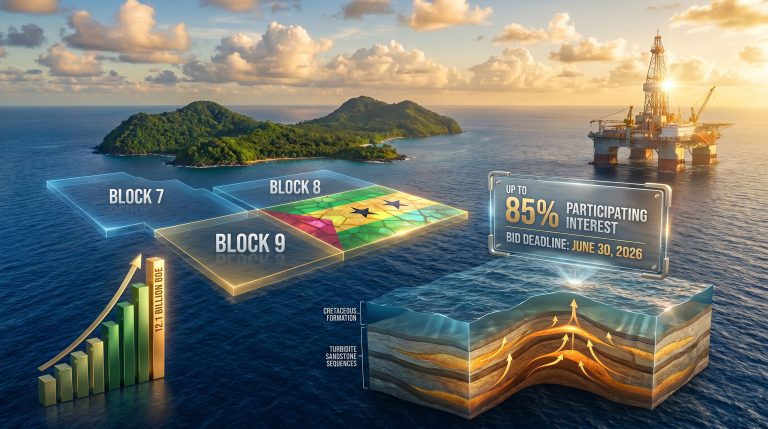

The primary exploration targets within Blocks 7, 8, and 9 are tied to Cretaceous-era formations. This is not incidental. Cretaceous sequences in the Gulf of Guinea have been the source of some of the most commercially significant hydrocarbon accumulations along Africa's Atlantic margin, and targeting the same geological interval in a structurally analogous setting represents a geologically coherent, if unproven, exploration thesis.

What Historical Drilling Actually Established

Two earlier exploration wells, designated Jaca-1 and Falcão-1, provided the foundational geological dataset that informs the current licensing round. A critical distinction is worth understanding here: these wells did not result in commercial discoveries, but they succeeded in confirming the existence of active petroleum systems within the basin. (Ecofin Agency, May 11, 2026)

In frontier petroleum economics, this distinction carries significant weight. The difference between a basin with no evidence of petroleum generation and one where active systems have been confirmed is the difference between a speculative geological hypothesis and a risk-adjusted exploration opportunity. The wells moved STP from the former category to the latter.

Recent seismic reprocessing work completed ahead of the 2026 round has further validated the petroleum system interpretation, providing prospective investors with a materially higher-confidence geological dataset than was available during earlier bid cycles. This reduction in subsurface uncertainty is one of the key factors that differentiates the 2026 round from its predecessors.

The Infrastructure Sharing Dimension

STP authorities are actively encouraging incoming operators to share infrastructure and technical data as a mechanism for reducing per-well exploration costs in deepwater environments, where capital requirements can be prohibitive for standalone programs. (Ecofin Agency, May 11, 2026)

This cooperative framework addresses a structural economic challenge specific to micro-state frontier exploration: the absence of existing offshore infrastructure means that every exploration program must effectively bear full standalone development costs. By enabling data and infrastructure pooling across operators, the government is attempting to lower the economic threshold for participation, particularly for mid-tier IOCs that might be deterred by the capital intensity of a fully independent deepwater program.

| Block | EEZ Location | Primary Geological Target | Maximum Offered Interest | Bid Deadline |

|---|---|---|---|---|

| Block 7 | Western EEZ | Cretaceous-era formations | 85% | June 30, 2026 |

| Block 8 | Western EEZ | Cretaceous-era formations | 85% | June 30, 2026 |

| Block 9 | Western EEZ | Cretaceous-era formations | 85% | June 30, 2026 |

The Fiscal and Regulatory Framework Governing the 2026 Round

Regulatory Architecture and Bidding Structure

The National Petroleum Agency, known as ANP-STP, administers the 2026 licensing round. The bid process requires separate technical and financial proposals for each individual block, a structure designed to maximise competitive tension while permitting targeted participation by companies with varying appetite across the three blocks.

Companies considering participation should note that the regulatory framework governing offshore exploration in STP provides a degree of legislative continuity that has persisted across multiple bid cycles. This policy stability is frequently cited as a positive attribute in frontier market risk assessments, where regulatory unpredictability can function as a more significant deterrent to investment than geological risk alone.

The 85% Participating Interest: What It Signals

The decision to offer participating interests of up to 85% in each block is commercially notable. By regional frontier market standards, this is a highly generous equity stake offering, and it signals a government that is prioritising capital attraction over short-term state revenue maximisation. For IOCs performing risk-adjusted return modelling, an 85% working interest in a proven petroleum system, even at an early exploration stage, offers meaningful upside leverage relative to more restrictive equity structures common in mature producing jurisdictions.

Qualifying companies may also access benefits under STP's framework for offshore fiscal incentives, which is designed to attract international capital into high-risk, long-cycle exploration projects of the type represented by Blocks 7, 8, and 9.

The Petrobras-Oranto Block 3 Approval: A Regulatory Litmus Test

The regulatory approval process for Petrobras' acquisition of a 75% operating stake in Block 3, previously held by Oranto Petroleum at a 90% interest, is currently ongoing as of May 2026. The resulting post-transaction consortium structure for Block 3 is expected to comprise Petrobras at 75%, Oranto Petroleum at 15%, and ANP-STP at 10%. (Ecofin Agency, May 11, 2026)

The pace and transparency of this approval process will function as a de facto benchmark for how STP's administrative systems handle complex IOC transactions. Companies evaluating bids for Blocks 7, 8, and 9 will be watching this process carefully. A smooth and timely outcome would materially strengthen investor confidence ahead of the June 30, 2026 bid deadline.

A slow or opaque approval process for Block 3 would raise legitimate questions about institutional capacity and could dampen competitive interest in the new blocks, regardless of how compelling the geological or fiscal case appears on paper.

Petrobras as an Anchor Investor: What It Means for the Broader Investment Thesis

Scale, Reserves, and Strategic Intent

Petrobras' decision to acquire operatorship of Block 3 is the single most consequential development in STP's recent upstream history. The company reported 12.1 billion barrels of oil equivalent in proven reserves at the close of 2025, with daily production of approximately 3 million barrels of oil equivalent, positioning it among the most significant state-backed upstream operators globally. (Ecofin Agency, May 11, 2026)

This is not a company making opportunistic bets in frontier markets. The Block 3 acquisition reflects the deliberate execution of Petrobras' 2026-2030 strategic plan, which prioritises reserve growth and international portfolio expansion. (Ecofin Agency, May 11, 2026) The commercial logic is coherent: as legacy producing fields mature and reserve replacement ratios tighten, technically sophisticated operators must increasingly look to frontier acreage to sustain long-term production profiles.

The Gondwana Geological Thesis: Why Atlantic Africa Is a Natural Extension

Petrobras has built arguably the world's most advanced technical capability in deepwater pre-salt petroleum systems through decades of work in Brazil's offshore basins. What makes STP's acreage strategically interesting for the company is the geological kinship between those Brazilian pre-salt systems and the conjugate margin along Africa's Atlantic coast.

The tectonic breakup of the Gondwana supercontinent created mirror-image geological architectures on opposing sides of the Atlantic. The subsurface formations that Petrobras has spent decades learning to evaluate and develop in Brazil have direct structural and stratigraphic analogues on the African side of the ocean. For Petrobras, entering STP's waters is not a leap into the unknown. It is an extension along a geological corridor the company understands more intimately than perhaps any other operator in the world.

The Anchor Effect in Frontier Basin Economics

In frontier exploration economics, the entry of a technically credible, well-capitalised operator functions as a powerful signal that reshapes the risk perception of the entire basin for subsequent investors. This is the anchor effect, and it operates through a well-documented psychological and analytical mechanism:

- A major operator's entry signals that rigorous technical due diligence has been completed and a positive assessment reached

- The operator's presence creates future data-sharing opportunities that reduce subsurface uncertainty for other blocks

- The operational infrastructure established by an anchor operator lowers the standalone cost of adjacent exploration programs

- The reputational credibility of a large operator reduces the perceived institutional and geopolitical risk of the jurisdiction

STP's government has explicitly framed Petrobras' growing role as a catalyst for broader market participation, recognising that the anchor dynamic is a standard and well-understood mechanism in frontier energy market development. (Ecofin Agency, May 11, 2026)

Competitive Positioning: How STP Compares Across the West African Frontier

Understanding STP's relative attractiveness requires placing it within the competitive landscape of West African frontier and emerging producer markets. Furthermore, the evolving geopolitical risk landscape across the region adds another dimension to how IOCs weigh their exposure across competing jurisdictions. Each jurisdiction presents a distinct combination of geological risk, fiscal terms, institutional capacity, and commercial maturity.

| Country | Exploration Stage | Key Recent Activity | Primary Geological Analogue | Commercial Discovery Status |

|---|---|---|---|---|

| São Tomé & Príncipe | Early frontier | 2026 licensing round; Petrobras Block 3 entry | Gabon, Equatorial Guinea basins | No confirmed commercial discovery |

| Namibia | Emerging producer | Major Orange Basin discoveries (TotalEnergies, Shell) | South Atlantic conjugate margin | Significant discoveries confirmed |

| Côte d'Ivoire | Active exploration | Multiple IOC campaigns underway | Gulf of Guinea shelf | Incremental discoveries |

| Gabon | Mature producer | Production optimisation; new exploration incentives | Established producing basin | Long-established production |

| Equatorial Guinea | Mature producer | Declining output; renewed exploration push | Established producing basin | Long-established production |

STP's primary competitive advantage is geological positioning within a proven petroleum corridor. Its primary competitive challenge is the absence of a confirmed commercial discovery, which elevates the risk premium that IOCs must apply to their economic models relative to basins where commercial-scale accumulations have already been documented.

The 85% participating interest offering is notably more generous than fiscal terms typically available in more established African producing jurisdictions, reflecting the government's conscious decision to price exploration risk appropriately given the current stage of basin maturity.

The next major ASX story will hit our subscribers first

Key Risk Factors That Must Be Weighed Carefully

Geological Risk: The Commercial Discovery Gap

Despite confirmation of active petroleum systems through Jaca-1, Falcão-1, and subsequent seismic reprocessing, no commercial discovery has been officially announced in STP's exclusive EEZ. This absence is the dominant risk factor in the investment equation, and it cannot be wished away by favourable fiscal terms or geological analogues alone.

The Falcão-1 well results represent a closely watched data point whose interpretation will either accelerate or temper near-term investor enthusiasm. Results from continued drilling activity within STP's EEZ carry disproportionate signalling power relative to their geological scope, because the market is effectively waiting for a single confirmation event to shift its risk assessment of the entire basin.

Commercial Risk: Deepwater Economics at Micro-State Scale

Deepwater exploration requires substantial capital commitments over long time horizons, typically a decade or more from initial exploration to first production. Shifts in global oil benchmarks can further compound these challenges, as price volatility directly influences how IOCs allocate capital across long-cycle frontier programmes. For a micro-state with limited domestic market depth, no existing offshore production infrastructure, and constrained institutional bandwidth, the economics of deepwater development present structural challenges that fiscal incentives can partially but not fully address.

The government's infrastructure-sharing initiative directly targets this challenge, however its effectiveness depends on the willingness of multiple competing operators to coordinate in an environment where data and technical intelligence are core commercial assets.

Institutional Risk: Administrative Capacity Constraints

STP's small governmental and regulatory infrastructure means that approval processes, contract negotiations, and compliance monitoring may operate more slowly than in larger, more institutionally developed petroleum jurisdictions. The pending Block 3 regulatory approval serves as a live test of the country's administrative capacity, and its outcome will be closely scrutinised by prospective bidders evaluating Blocks 7, 8, and 9.

Investors approaching the 2026 bid round should apply a frontier basin risk premium to their economic models, while recognising that the combination of Petrobras' entry, improved seismic data, and a generous equity offering materially reduces the risk-adjusted cost of entry relative to earlier licensing cycles.

Scenario Pathways: STP's Upstream Trajectory Through 2030

Scenario 1: Accelerated Development (Bull Case)

Multiple credible IOC bids are received for Blocks 7, 8, and 9 before the June 30 deadline. Petrobras' Block 3 regulatory approval is completed within 2026, with drilling operations initiated by 2027. Subsequent well results confirm commercial-scale accumulations, triggering a significant re-rating of STP's offshore acreage across all blocks. By 2030, STP has established itself as a recognised emerging producer within the Gulf of Guinea, attracting development capital and infrastructure investment from a broadening set of operators.

Scenario 2: Measured Progression (Base Case)

The 2026 bid round attracts limited but technically qualified interest, with one or two blocks awarded by year-end. Petrobras advances Block 3 operations on a cautious timeline, completing new seismic acquisition by 2027 but deferring drilling decisions pending further data analysis. No commercial discovery is confirmed within the forecast period, but sustained exploration activity maintains investor engagement and gradually de-risks the basin. STP remains a credible frontier market with growing IOC presence but no transformative production breakthrough before 2030.

Scenario 3: Stalled Momentum (Bear Case)

The bid round attracts insufficient qualified interest, leaving blocks unawarded or allocated to undercapitalised operators lacking the technical and financial resources to execute meaningful work programmes. Regulatory delays impede Petrobras' Block 3 advancement, generating negative confidence signals for the broader investor community. A deterioration in crude oil price trends simultaneously reduces IOC appetite for high-risk frontier exploration. Under this scenario, STP's upstream ambitions are effectively deferred beyond 2030, with the country remaining in an extended pre-commercial exploration phase.

Frequently Asked Questions: São Tomé and Príncipe 2026 Offshore Licensing Round

What blocks are being offered in the 2026 round?

The licensing round covers offshore Blocks 7, 8, and 9, all located in the western section of STP's Exclusive Economic Zone. Separate technical and financial proposals may be submitted for each block, with a submission deadline of June 30, 2026.

What equity stake can participating companies acquire?

ANP-STP is offering eligible international oil companies a participating interest of up to 85% in each block, representing one of the most generous equity structures currently available in West African offshore exploration.

What is the geological basis for exploration interest in these blocks?

The blocks contain Cretaceous-era exploration targets within a petroleum system sharing structural characteristics with producing basins in Gabon and Equatorial Guinea. Historical wells including Jaca-1 and Falcão-1 confirmed active petroleum systems, and recent seismic reprocessing has further validated the prospectivity of the acreage. (Ecofin Agency, May 11, 2026)

What role does Petrobras play in STP's offshore sector?

Petrobras has agreed to acquire a 75% stake and operatorship in Block 3, taking over from Oranto Petroleum, which previously held a 90% interest. The transaction is pending regulatory approval. Petrobras, which reported 12.1 billion barrels of oil equivalent in proven reserves and production of approximately 3 million barrels of oil equivalent per day at end-2025, views STP's geology as analogous to Brazil's pre-salt offshore basins. (Ecofin Agency, May 11, 2026)

Has any commercial oil discovery been made in STP?

No commercial discovery has been officially confirmed in STP's exclusive EEZ to date. Historical drilling has confirmed active petroleum systems, and ongoing exploration activity continues to refine the basin's commercial potential.

What legal framework governs offshore exploration in STP?

Offshore exploration in STP is administered by the National Petroleum Agency (ANP-STP), with fiscal incentives available to qualifying companies through the country's offshore activities framework.

The Strategic Verdict: A Genuine Inflection Point or Familiar Frontier Frustration?

Where the Balance of Evidence Currently Sits

Three factors have converged to make the 2026 São Tomé offshore licensing round the most compelling market access opportunity the country has presented to international capital in over a decade. Improved seismic intelligence has materially reduced geological uncertainty. Petrobras' anchor investment in Block 3 has provided the basin with its most credible institutional endorsement to date. An 85% participating interest offering creates a risk-reward profile that compares favourably with competing frontier opportunities across the same regional basin system.

What the round cannot offer is what would transform it from interesting to compelling: a confirmed commercial discovery. That gap remains the defining constraint on capital mobilisation, and no combination of fiscal generosity, geological analogy, or anchor operator credibility fully substitutes for proven barrels. Consequently, understanding these commodity price impacts on overall investment decisions remains essential for companies evaluating their position in this round.

What Strong or Weak Participation Will Tell the Market

The outcome of the June 30, 2026 bid deadline will itself become a piece of market intelligence. Strong bidder participation signals that the combination of Petrobras' presence and improved geological data has successfully de-risked STP's offshore environment sufficiently to justify capital allocation from technically sophisticated operators. Limited participation signals that the absence of a commercial discovery continues to function as the dominant barrier, regardless of the fiscal and geological case constructed around it.

Either outcome provides the market with a clearer read on where STP sits in the frontier exploration risk spectrum, and how much de-risking work remains before the basin can compete on equal terms with more established Atlantic margin exploration destinations.

The São Tomé offshore licensing round is best understood not as a single news event, but as a strategic inflection test in a decades-long effort to convert geological promise into economic reality. The June 30, 2026 deadline is the near-term catalyst. The quality of participation it attracts is the signal investors should be watching.

Disclaimer: This article is intended for informational purposes only and does not constitute financial, investment, or professional advice. All forecasts, scenario projections, and analytical assessments involve inherent uncertainty and should not be relied upon as predictions of future outcomes. Investors should conduct independent due diligence and seek qualified professional advice before making any investment decisions. Historical geological data and exploration results cited are sourced from publicly available reporting and do not guarantee future exploration success or commercial discovery.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

While frontier energy plays like São Tomé's offshore blocks demand patience across long capital cycles, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX — turning complex data across 30-plus commodities into clear, actionable insights for both traders and long-term investors. Explore how historic ASX discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.