June 8, 2026

The Geology That Connects Two Continents Is Driving Frontier Oil Investment Into Unexpected Territory

When the South Atlantic began opening roughly 130 million years ago, it separated what is now Brazil's prolific offshore basins from the hydrocarbon-rich margins of West Africa. That ancient geological kinship has never stopped mattering to petroleum geologists, and today it sits at the centre of a renewed push into one of the world's least-drilled offshore jurisdictions. São Tomé and Príncipe, a small island nation positioned at a striking geological crossroads in the Gulf of Guinea, is betting that this connection, combined with improving data quality and growing supermajor interest nearby, can finally convert decades of exploration intent into confirmed reserves through the São Tomé offshore oil licensing round.

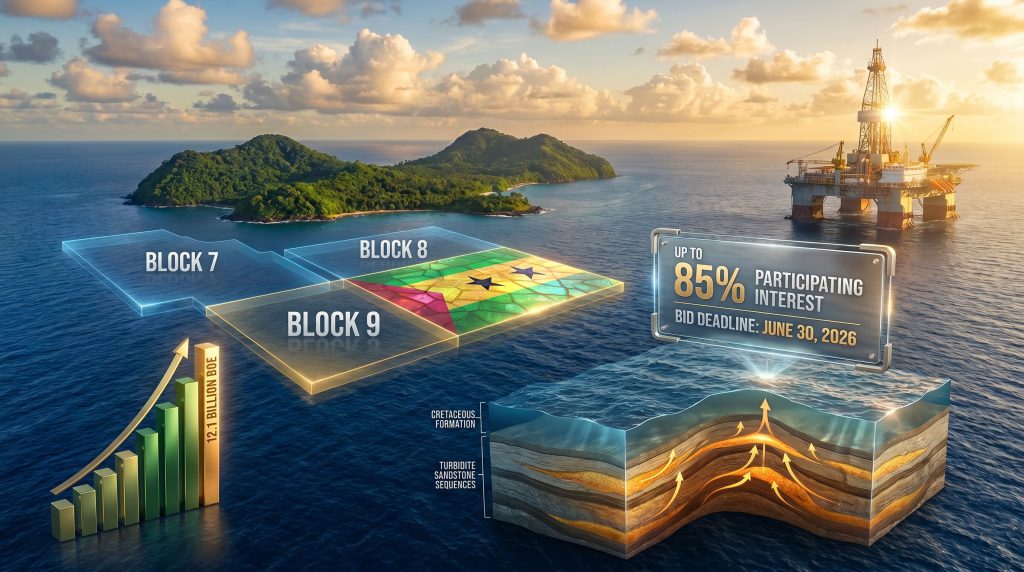

The country's 2026 São Tomé offshore oil licensing round, covering Blocks 7, 8, and 9 in the western portion of its exclusive economic zone, represents the most substantive attempt yet to build momentum in a basin where active petroleum systems have been confirmed but commercial discoveries have remained elusive. With bids due by 30 June 2026 and participating interest stakes of up to 85% on offer, the round is structured explicitly to absorb frontier risk rather than maximise near-term government take.

When big ASX news breaks, our subscribers know first

Why the Gulf of Guinea Has Re-Entered the Exploration Conversation

The global oil industry is navigating a structural tension between near-term energy transition narratives and the physical reality that conventional reserve replacement has become genuinely difficult. Maturing fields across established producing regions are yielding less, while the economics of large-scale deepwater frontier exploration have been progressively improved by advances in seismic imaging, reprocessing technology, and subsurface interpretation software.

West Africa's Atlantic margin has re-emerged in this context as a priority destination for exploration capital. Furthermore, the trade war impact on oil markets and shifting macroeconomic conditions have reinforced the urgency for operators to identify and secure long-horizon frontier acreage before competitive capital rushes in. The African Energy Chamber has noted that renewed activity across the Gulf of Guinea reflects both the geological richness of the region and the improved data frameworks operators now have access to.

Exploration momentum across Namibia, Angola, South Africa, and Côte d'Ivoire has materially changed the risk calculus for frontier acreage that was previously considered marginal by IOC portfolio committees (Ecofin Agency, May 2026).

São Tomé and Príncipe occupies a particularly compelling position within this broader regional story. Its exclusive economic zone spans approximately 160,000 km², sitting at the geological intersection of two of Africa's most consistently productive offshore systems: the Gabon Basin to the north and the Equatorial Guinea margin to the northeast. The African Energy Chamber has confirmed that STP's offshore blocks share geological characteristics with producing formations in both of these established basins. That alignment is not coincidental; it reflects the underlying Cretaceous-era stratigraphy that ties the region together as a coherent hydrocarbon province.

What Frontier Deepwater Really Means for Investors

The term frontier deepwater carries a specific meaning in petroleum exploration that laypeople often misinterpret. It does not mean the geology is speculative or poorly understood. Rather, it means that the combination of remoteness, absence of existing infrastructure, limited well control, and perceived political or regulatory complexity has historically kept the basin outside the core capital allocation frameworks of the largest operators.

Frontier risk premiums are not permanent. They compress when:

- Adjacent basins deliver commercial discoveries that validate the regional play system

- Seismic reprocessing improves subsurface confidence without new acquisition costs

- An anchor investor of sufficient credibility commits capital to nearby acreage

- Infrastructure sharing arrangements reduce per-well breakeven thresholds

All four of these conditions are beginning to converge in São Tomé and Príncipe's western EEZ.

What the 2026 São Tomé Offshore Oil Licensing Round Actually Offers

The São Tomé offshore oil licensing round is administered by the country's National Petroleum Agency and covers three deepwater blocks in the western EEZ. Bids submitted by 30 June 2026 must be prepared as separate technical and financial proposals for each individual block, meaning a company can target one, two, or all three blocks through distinct submissions.

The headline commercial term is the up to 85% participating interest available to successful applicants. By West African licensing standards, this is an unusually high ceiling. Most licensing rounds in mature basins such as Angola or Nigeria offer foreign investors much lower direct equity stakes, with national oil companies retaining substantial carried interests. STP's willingness to offer the majority of project economics to incoming operators reflects a deliberate strategy: attract the technical expertise and risk capital that deepwater exploration demands, and prioritise the long-term revenue potential of a producing basin over short-term signature bonus income.

| Parameter | Detail |

|---|---|

| Blocks Available | 7, 8, and 9 |

| EEZ Location | Western portion of STP exclusive economic zone |

| Maximum Participating Interest | Up to 85% |

| Bid Submission Deadline | 30 June 2026 |

| Administering Authority | National Petroleum Agency (ANP-STP) |

| Primary Geological Target | Cretaceous-era formations |

| Analogous Basins | Gabon offshore, Equatorial Guinea offshore |

The Geological Case for Blocks 7, 8, and 9

The petroleum system confidence underpinning the 2026 round has been built incrementally through historical well data and recent seismic reprocessing campaigns. Two exploration wells drilled in earlier phases, known as Jaca-1 and Falcão-1, penetrated the basin's subsurface and returned data that confirmed the presence of source rocks capable of generating hydrocarbons, reservoir intervals with trapping potential, and structural geometries consistent with commercial accumulations (Ecofin Agency, May 2026).

These wells did not deliver commercial discoveries, but in frontier basin terms, their value is significant. The confirmation of an active petroleum system, meaning one where source rocks have generated hydrocarbons and migration into reservoir structures has occurred, is the foundational prerequisite for any commercial exploration programme. Many frontier basins fail at this basic test; STP's western EEZ has passed it.

Recent seismic reprocessing work has further de-risked the blocks available in the current round. According to the African Energy Chamber's assessment, the reprocessed data confirmed viable petroleum systems across the western EEZ, with primary exploration targets tied to Cretaceous-era turbidite sandstone sequences analogous to those that host producing reservoirs in Gabon's offshore fields. The four key geological building blocks for a commercial discovery in these blocks are assessed as follows:

- Source rock: Organic-rich Cretaceous shales confirmed by historical well penetrations

- Reservoir: Turbidite sandstone sequences analogous to Gabon's producing offshore formations

- Trap: Four-way dip closures and fault-bounded structures identified through seismic interpretation

- Migration: Structural analysis indicates viable hydrocarbon migration routes from kitchen areas toward identified trap geometries

Infrastructure Strategy in an Undeveloped Basin

One of the more practically important aspects of the 2026 round is the authorities' emphasis on infrastructure and data sharing. The National Petroleum Agency is actively encouraging prospective operators to co-utilise infrastructure and pool technical information to reduce the per-well exploration cost burden in an area where no production infrastructure currently exists. In deepwater frontier contexts, this kind of cooperative framework can make the difference between a project that reaches final investment decision and one that stalls indefinitely in appraisal limbo.

Petrobras and the Anchor Investor Thesis

No single development has done more to shift STP's exploration outlook than Petrobras' agreement to acquire a 75% participating interest in Block 3 from Nigeria's Oranto Petroleum. The transaction was still pending regulatory clearance as of May 2026, but its strategic significance is already measurable.

Petrobras closed 2025 with 12.1 billion barrels of oil equivalent in proven reserves and daily production of approximately 3 million barrels of oil equivalent, making it one of the largest deepwater operators in the world. Its 2026-2030 strategic plan explicitly prioritises international reserve growth and operational expansion, and the company has been systematically targeting regions where the geological setting mirrors Brazil's world-class pre-salt offshore province.

That comparison is not marketing language. Brazil's pre-salt basins and West Africa's Atlantic margin were once physically connected before the South Atlantic opened, meaning the hydrocarbon-generating geological systems share a common origin. For Petrobras, applying its deepwater operational expertise, developed across Brazil's Santos, Campos, and Espírito Santo basins, to STP's deepwater environment represents an extension of core competency rather than a move into unfamiliar territory.

The Anchor Effect on Smaller Operators

From an investment psychology standpoint, Petrobras' presence creates a powerful signal for mid-tier and smaller IOCs evaluating Blocks 7, 8, and 9. The anchor investor effect in frontier basin exploration works as follows:

- A credible, technically sophisticated operator commits capital to acreage within the basin

- That commitment implicitly validates the basin's geological thesis and operational feasibility

- Smaller operators who could not independently justify the due diligence cost of evaluating a truly frontier basin can leverage the anchor operator's public commitment as a first-order data point

- The resulting increase in bidder interest raises competitive tension in the licensing round, improving the quality of work programme commitments from successful applicants

São Tomé's government has explicitly acknowledged that it hopes Petrobras' growing role will encourage additional investors to enter the market. That expectation is grounded in observable frontier basin dynamics, not optimism alone.

A History of Ambition and Incomplete Follow-Through

Understanding why the 2026 São Tomé offshore oil licensing round matters requires contextualising it against a long history of rounds that generated interest without transforming that interest into production. The country has been attempting to build a functioning oil industry for decades, and no commercial discovery has been officially announced as of mid-2026.

Earlier exploration phases, including joint development zone arrangements with Nigeria and standalone EEZ licensing rounds, produced geological data of real value but fell short of the sustained operator commitment needed to progress through appraisal to development. Governance transparency concerns during earlier rounds have been noted by international observers as a factor that dampened investor confidence, and the current administration faces the ongoing task of demonstrating through process integrity that the 2026 round operates under a materially different standard.

The legal architecture has been strengthened through Petroleum Operations Law No. 16/2009, which provides the contractual and fiscal framework governing all exploration agreements in the EEZ. The round's administration by ANP-STP under this established legal framework represents a more structured institutional environment than some previous rounds operated within.

What Has Changed to Make 2026 Different?

Several factors genuinely differentiate the current round from its predecessors. In addition to improved geological data, broader macroeconomic conditions, including the current crude oil prices environment and evolving supply dynamics, have made frontier deepwater acreage increasingly attractive to capital allocators seeking long-horizon growth options.

- Seismic data quality has improved substantially through reprocessing of legacy datasets, reducing subsurface uncertainty without requiring new acquisition investment from potential bidders

- Petrobras' Block 3 commitment provides an anchor that no previous STP round has had access to

- Regional exploration momentum across West Africa's Atlantic margin has reduced the psychological frontier discount that previously kept institutional capital away from the basin

- TotalEnergies' operatorship of Block STP02, covering approximately 4,969 km² off Príncipe island following acquisition of a 60% stake, confirms that supermajors view the basin as strategically viable

- Shell's Falcao-1 well in Block 10 represents the most recent drilling activity in the basin, with results contributing to basin-wide geological understanding and reducing the data gap for operators evaluating adjacent western EEZ acreage

Three Scenarios for How the Round Could Play Out

Frontier licensing rounds rarely proceed according to a single script. The following scenario framework provides a structured way to assess the range of outcomes, with each scenario driven by identifiable probability factors rather than speculation.

Scenario 1: High Participation

Multiple operators submit competitive bids for one or more of Blocks 7, 8, and 9 by the June 30 deadline. At least one block is awarded in Q3 2026, with new seismic acquisition commencing before year-end. An initial exploration well could be drilled by 2028, with commercial discovery potential assessed by 2029-2030. The primary driver of this outcome is Petrobras' Block 3 anchor investment combined with the regional exploration momentum across Africa's Atlantic margin.

Scenario 2: Limited Participation

One or two blocks attract qualifying bids whilst at least one receives insufficient interest. The award process extends into late 2026 or early 2027, delaying the seismic acquisition phase and pushing first-well timing to 2029 or beyond. The primary driver of this outcome would be oil price volatility trends combined with competing frontier acreage in Namibia and Angola drawing capital allocation away from STP.

Scenario 3: Transformational Catalyst

A positive result from Shell's Falcao-1 well in Block 10 confirms a material discovery in the adjacent basin, triggering a surge of investor interest in the western EEZ blocks. All three blocks receive competitive bids, seismic and drilling timelines accelerate, and STP enters a genuinely transformational exploration phase. Under this scenario, first commercial production could realistically occur post-2032.

The next major ASX story will hit our subscribers first

Risk Framework: What Investors and Analysts Must Weigh

| Risk Category | Description | Mitigation Framework |

|---|---|---|

| Geological Risk | No commercial discovery confirmed in STP to date | Seismic reprocessing data; analogous basin production in Gabon and Equatorial Guinea |

| Infrastructure Risk | No production infrastructure in deepwater EEZ | Data-sharing frameworks; potential Petrobras Block 3 anchor development |

| Regulatory and Governance Risk | Historical transparency concerns from earlier rounds | Established legal framework; ANP-STP institutional processes |

| Market Risk | Oil price volatility affecting deepwater project economics | Long-term demand forecasts support frontier investment horizon beyond 2030 |

| Operational Risk | Deepwater logistics in remote island nation context | Proximity to established West African offshore service hubs |

| Competitive Capital Risk | Competing frontier acreage drawing IOC attention | Petrobras anchor investment and supermajor activity in adjacent blocks |

However, it is worth noting that OPEC's market influence over global supply decisions remains a significant variable in the broader economics of any new deepwater development. Furthermore, an oil price rally driven by geopolitical or tariff-related factors could meaningfully accelerate operator appetite for securing frontier acreage before competitive bidding intensifies.

Disclaimer: This article contains forward-looking statements and scenario projections based on publicly available information as of May 2026. Frontier exploration outcomes are inherently uncertain. Nothing in this article constitutes financial advice, and readers should conduct their own due diligence before making any investment decisions related to companies or projects operating in São Tomé and Príncipe's offshore sector.

Frequently Asked Questions: São Tomé and Príncipe 2026 Offshore Licensing

Which blocks are available in the 2026 round?

Blocks 7, 8, and 9 in the western portion of São Tomé and Príncipe's exclusive economic zone are on offer. Bidders may apply for one, two, or all three blocks, but must submit separate technical and financial proposals for each.

What participating interest can incoming operators acquire?

Successful applicants can acquire up to an 85% participating interest in each block, which represents one of the highest equity ceilings in any current African offshore licensing round.

When must bids be submitted?

All proposals must reach the National Petroleum Agency by 30 June 2026.

Has oil ever been commercially produced in São Tomé and Príncipe?

No commercial hydrocarbon discovery has been formally declared in STP's waters as of mid-2026. However, historical exploration wells including Jaca-1 and Falcão-1 confirmed the presence of active petroleum systems with source rocks, reservoir intervals, and structural traps. Consequently, the basin retains genuine long-term commercial potential that the 2026 round is designed to unlock.

Why is Petrobras pursuing acreage in STP?

Petrobras views the West African Atlantic margin as a geological extension of Brazil's pre-salt offshore province, reflecting the shared continental origin of the two regions before the South Atlantic opened. The company's 2026-2030 strategic plan prioritises international reserve growth, and STP's deepwater acreage aligns directly with its pre-salt technical expertise, as explored in detail by Upstream Online.

When could first production realistically begin?

Industry forecasts suggest new seismic surveys and initial drilling campaigns could commence by late 2026. Given standard deepwater appraisal and development timelines, first commercial production, if a discovery is confirmed, would realistically occur post-2030.

Want to Stay Ahead of the Next Major Resource Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, translating complex resource data into clear, actionable insights for both short-term traders and long-term investors — explore historic discoveries and their returns to see what early positioning can mean, then begin your 14-day free trial to ensure you're never the last to know.