August 2, 2026

Global supply chain security has become the defining strategic battleground of the 21st century, where control over critical materials determines technological sovereignty and economic independence. Among all commodities, rare earth elements represent perhaps the most concentrated source of geopolitical leverage, with processing capabilities concentrated in the hands of a single nation that has systematically built an integrated ecosystem spanning from mining to manufacturing. Understanding how China's rare earth strategy operates, and more importantly, how it might evolve, requires examining the intricate mechanisms of control that extend far beyond simple market share statistics.

How Does China Maintain Its Rare Earth Supremacy Through Strategic Export Controls?

The architecture of Beijing's rare earth dominance operates through a sophisticated multi-layered control system that combines direct regulatory oversight with administrative complexity designed to create uncertainty for international buyers. This framework has evolved from simple export quotas to a comprehensive licensing regime that can selectively restrict access based on end-use applications, destination countries, and broader geopolitical considerations. Furthermore, this approach aligns with broader patterns seen in China's export control strategy across multiple critical materials.

The Architecture of Beijing's Licensing Framework

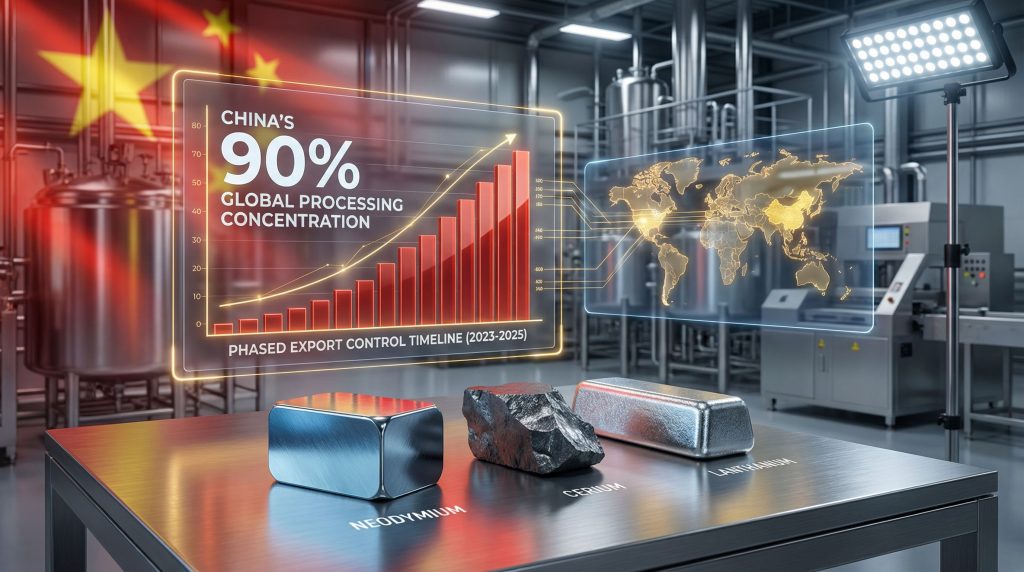

China's approach to rare earth export control has matured into a phased implementation strategy that allows for precise calibration of market pressure. The system operates on multiple timelines, creating different levels of restriction based on strategic priorities and international responses. Moreover, these controls often escalate during periods of heightened tension, as evident in recent US-China trade war impacts.

Table: China's Phased Export Control Evolution

| Phase | Timeline | Target Elements | Primary Focus |

|---|---|---|---|

| Technology Export Restrictions | Late 2023 | Processing equipment | Preventing capacity transfer |

| Initial Element Controls | April 2025 | 7 critical elements | High-tech applications |

| Expanded Restrictions | November 2025 | 12 element categories | Broader industrial coverage |

| Defense Sector Targeting | December 2025 | Military applications | Strategic security concerns |

The licensing system creates multiple decision points where Chinese authorities can evaluate applications based on evolving strategic considerations. Each application undergoes technical review, end-use verification, and political assessment that can extend processing times indefinitely when geopolitical tensions escalate. Additionally, China's New Rare Earth and Magnet Restrictions Threaten US Defense Supply Chains, highlighting the strategic implications of these controls.

Administrative Weaponization: The 45-Day Uncertainty Window

Perhaps more significant than outright denials, China's licensing process incorporates deliberate administrative delays that create supply chain uncertainty for international manufacturers. The standard 45-day review period frequently extends to months, forcing buyers to maintain larger inventories and accept higher carrying costs.

Key pressure points within the administrative system include:

• End-use documentation requirements that demand detailed technical specifications and manufacturing plans

• Supply chain transparency mandates requiring disclosure of downstream customers and applications

• Re-export restriction compliance monitoring that extends Chinese jurisdiction to third-party transactions

• Periodic renewal processes that reset the approval timeline for established supply relationships

This administrative complexity serves dual purposes: maintaining plausible deniability regarding trade restrictions while creating practical barriers that discourage reliance on Chinese suppliers for critical applications.

Extraterritorial Jurisdiction: Extending Control Beyond Borders

China's rare earth strategy extends beyond direct export controls to encompass extraterritorial oversight of Chinese-origin materials throughout global supply chains. This approach leverages the integrated nature of rare earth processing to maintain influence over downstream applications regardless of where final manufacturing occurs.

The extraterritorial framework operates through several mechanisms:

• Technology licensing requirements for overseas processing facilities using Chinese equipment or expertise

• Material tracking obligations that follow Chinese-origin rare earths through multiple manufacturing stages

• Compliance certification processes for foreign manufacturers seeking access to Chinese materials

• Joint venture approval protocols that give Chinese entities veto power over overseas capacity expansion

This system effectively extends Chinese regulatory reach into allied nations' defense industrial bases, creating dependencies that persist even when alternative supply sources become available.

When big ASX news breaks, our subscribers know first

What Makes China's Processing Monopoly So Difficult to Challenge?

The foundation of China's rare earth strategy rests not primarily on mining capacity but on an unparalleled concentration of processing capabilities that took decades to develop and integrate. With approximately 90% of global processing capacity, China has created technical and economic barriers that newcomers struggle to overcome even with substantial government backing.

The Midstream Chokepoint Analysis

Rare earth processing represents one of the most complex metallurgical challenges in modern industry, requiring sophisticated separation technologies that can isolate individual elements from complex ore matrices. The technical knowledge accumulated over decades of industrial practice creates institutional advantages that cannot be replicated quickly through capital investment alone.

Critical processing complexities include:

• Separation chemistry expertise developed through proprietary solvent extraction processes

• Quality control systems that ensure consistent purity levels across 17 different elements

• Waste management protocols for handling radioactive and toxic byproducts

• Integration capabilities linking upstream mining with downstream manufacturing

China's processing facilities achieve economies of scale that make smaller operations economically unviable. The infrastructure investment requirements for competitive processing plants typically exceed $500 million, with additional costs for environmental compliance and technical expertise acquisition.

Vertical Integration Advantages

Chinese rare earth companies operate integrated supply chains that span from mine development through final product manufacturing, creating cost advantages and quality control that independent operators cannot match. This vertical integration enables optimisation across production stages while maintaining flexibility to adjust output based on market conditions.

The integrated model provides several competitive advantages:

• Cost optimisation through elimination of intermediate profit margins and logistics costs

• Quality standardisation across all production stages using consistent technical specifications

• Supply security that reduces dependence on external suppliers and market fluctuations

• Technology development that can be deployed across multiple production facilities simultaneously

This integration creates natural barriers for new entrants who must either accept dependence on Chinese intermediates or invest in complete supply chain development from mining through manufacturing.

Technical Moat Protection Strategies

Beyond market position, China actively protects its technological advantages through intellectual property controls and knowledge transfer restrictions that prevent rapid capacity replication in competing jurisdictions. These protections extend to both hardware and human capital mobility.

Key protection mechanisms include:

• Equipment export restrictions that limit access to specialised processing machinery

• Technical personnel controls that restrict emigration of experienced engineers and managers

• Patent portfolio management that creates licensing requirements for alternative processing methods

• Research collaboration limitations that prevent technology transfer through academic partnerships

These measures ensure that even when alternative processing capacity comes online, it operates at technological disadvantages that translate into higher costs and lower product quality.

How Are Western Nations Responding to China's Strategic Positioning?

The recognition that rare earth dependence represents a critical vulnerability has triggered comprehensive policy responses across Western allies, moving beyond diplomatic protests to substantive investment in alternative supply chains. However, these efforts face significant technical and economic challenges that require sustained government support and private sector coordination. Notably, recent Trump's critical minerals order demonstrates the growing urgency of supply chain security concerns.

United States Counter-Strategy Development

The U.S. response to Chinese rare earth dominance combines direct government investment with private sector partnerships designed to create economically viable alternative processing capacity. The Department of Defense has emerged as a key catalyst, providing both funding and guaranteed demand for domestic production.

Current strategic initiatives include:

• Defense Production Act authorisations enabling rapid capacity expansion for critical applications

• Development Finance Corporation commitments exceeding $400 million for international projects

• Public-private partnerships linking government funding with commercial expertise

• Technology development programmes focused on breakthrough processing methods

The MP Materials-Saudi Arabia joint venture represents a significant structural shift, combining American technical expertise with Saudi financial resources under Department of Defense backing. This model provides guaranteed offtake agreements that reduce private sector risk while accelerating capacity development timelines.

The United States-Uzbekistan partnership framework establishes preferential access rights to Central Asian rare earth deposits while providing technical assistance for local processing development. This approach creates alternative supply chains outside Chinese influence while building strategic relationships in resource-rich regions.

Multi-Country Alliance Building

Western allies have coordinated rare earth strategies through formal frameworks that pool resources and share technical capabilities. These alliances recognise that no single country can replicate China's integrated supply chain independently, requiring collaborative approaches that leverage comparative advantages. In addition, European critical materials supply initiatives demonstrate coordinated responses to supply chain vulnerabilities.

Table: Western Rare Earth Processing Capacity Development

| Country | Lead Companies | Investment Focus | Timeline |

|---|---|---|---|

| Australia | Lynas Rare Earths | Heavy rare earth separation | 2025-2027 |

| Canada | Saskatchewan Research Council | Light rare earth processing | 2026-2028 |

| Japan | Sumitomo Corporation | Technology development | 2025-2029 |

| Brazil | Vale S.A. | Integrated mining-processing | 2027-2030 |

These coordinated investments aim to create processing capacity distributed across multiple jurisdictions, reducing vulnerability to single points of failure while maintaining economic viability through shared demand and technical cooperation.

Financial Tools vs. Traditional Diplomacy

The Western response has evolved from traditional diplomatic engagement to deployment of sophisticated financial instruments that can compete with Chinese development finance. This shift recognises that resource-rich nations respond more to concrete economic incentives than political alignment.

Key financial innovations include:

• Price floor guarantees that protect new producers from market volatility during capacity ramp-up periods

• Blended finance structures combining government grants with private investment to improve project economics

• Technology transfer agreements that provide access to Western processing expertise in exchange for supply commitments

• Infrastructure bundling that links rare earth development with broader economic assistance programmes

The Development Finance Corporation's catalytic funding approach provides initial project financing that attracts additional private investment, multiplying the impact of government resources while creating sustainable commercial operations.

Why Do Global South Nations Favor China's Approach?

The preference for Chinese partnership among resource-rich developing nations reflects practical considerations rather than ideological alignment, driven by Beijing's ability to provide immediate financing with fewer conditions and faster implementation timelines compared to Western alternatives.

The "Bulldozers vs. Conditions" Dynamic

China's engagement model emphasises rapid project implementation with integrated financing that addresses immediate infrastructure needs beyond just resource extraction. This comprehensive approach contrasts sharply with Western practices that separate resource development from broader economic assistance.

Chinese advantages in developing nation engagement include:

• Streamlined approval processes that reduce project development timelines by months or years

• Infrastructure integration linking rare earth development with transportation, power, and communication improvements

• Local employment generation through technology transfer and skills development programmes

• Guaranteed purchase commitments that provide revenue certainty for long-term planning

Western engagement often requires extensive environmental and governance reviews that, while well-intentioned, create delays that developing nations view as obstacles to economic development.

Historical Relationship Advantages

China's two-decade engagement timeline with African, Asian, and Latin American nations has created institutional relationships and cultural familiarity that new Western initiatives cannot quickly replicate. These relationships extend beyond government-to-government contacts to include business networks and technical expertise exchanges.

The Belt and Road Initiative integration provides a framework for embedding rare earth projects within broader economic development strategies, creating synergies that make Chinese participation particularly attractive to resource-rich nations seeking comprehensive modernisation.

Key relationship advantages include:

• Institutional knowledge of local regulatory and business environments

• Established supply chains for equipment and materials needed for project development

• Cultural competency that facilitates smoother negotiations and implementation

• Flexible financing terms adapted to local economic conditions and capabilities

Speed-to-Market Competitive Edge

Perhaps most significantly, China's state-directed approach enables decision-making timelines that democratic nations cannot match, particularly for large-scale infrastructure projects requiring environmental and regulatory approval across multiple jurisdictions.

Chinese speed advantages manifest through:

• Centralised decision-making that eliminates bureaucratic delays common in Western systems

• Integrated project delivery using Chinese contractors and equipment suppliers

• Risk assumption by state-backed entities that private companies cannot accept

• Technical standardisation that reduces design and engineering timelines

This speed differential becomes particularly important for developing nations facing immediate fiscal pressures or political cycles that demand visible progress within short timeframes.

What Are the Vulnerabilities in China's Rare Earth Fortress?

Despite its commanding position, China's rare earth strategy faces emerging challenges from technological innovation, geopolitical diversification, and market dynamics that could gradually erode Beijing's strategic advantages. Understanding these vulnerabilities provides insight into potential evolution scenarios over the coming decade.

Emerging Supply Chain Diversification

The most significant threat to Chinese dominance comes from coordinated efforts to develop alternative processing capacity in multiple countries, reducing the concentration risk that currently characterises global rare earth supply chains. These efforts benefit from advancing technology that makes smaller-scale processing operations economically viable. Furthermore, critical minerals energy security concerns are driving unprecedented investment in alternative supply chains.

Key diversification trends include:

• Distributed processing networks that reduce dependence on single-country capacity

• Technology advancement enabling smaller plants to achieve competitive economics

• Alternative material development reducing demand for traditional rare earth applications

• Recycling infrastructure expansion creating secondary supply sources independent of Chinese control

Heavy rare earth alternative sources are beginning to emerge in Australia, Canada, and Brazil, though these remain years away from commercial production at scales that could meaningfully impact Chinese market share.

Geopolitical Risk Calculations

China's willingness to use rare earth access as a geopolitical tool creates incentives for major economies to accept higher costs in exchange for supply security. This political weaponisation of commodity access undermines long-term commercial relationships even when short-term leverage proves effective.

Escalation risks include:

• Trade war expansion that could trigger comprehensive rare earth embargos

• Alliance formation creating coordinated Western responses to Chinese restrictions

• Technology competition spurring breakthrough developments in processing efficiency

• Alternative material adoption accelerating substitution away from rare earth applications

Each use of rare earth leverage for political purposes strengthens the business case for developing alternatives, creating self-defeating dynamics that could accelerate diversification efforts.

Market Dynamics Shifting

Growing global demand for rare earth elements, driven primarily by renewable energy and electric vehicle adoption, is creating market opportunities that exceed China's capacity expansion plans. This demand growth provides economic justification for alternative processing investments that might otherwise struggle for viability.

Market pressure factors include:

• Demand growth rates exceeding 15% annually in key applications

• Price volatility from export restrictions creating cost uncertainty for manufacturers

• Quality concerns regarding Chinese processing consistency under political pressure

• Investment capital availability from governments prioritising supply chain resilience

These market dynamics suggest that even without explicit government intervention, commercial forces are beginning to favour supply chain diversification that reduces Chinese concentration. However, as noted in analysis of China's Rare Earth Monopoly and the Geopolitics of Minerals, the transition away from Chinese dominance remains challenging.

How Will the Rare Earth Competition Evolve Through 2030?

The trajectory of global rare earth markets over the next decade will depend on the intersection of technological development, geopolitical competition, and economic factors that could produce significantly different outcomes depending on policy choices and investment priorities across major economies.

Scenario 1: Continued Chinese Dominance

In this scenario, China successfully maintains processing capacity retention at 80%+ through aggressive capacity expansion, competitive pricing, and continued Global South partnership maintenance. Alternative processing developments face cost and technical challenges that prevent meaningful market share capture.

Key characteristics of this outcome include:

• Processing moat preservation through continued technology restrictions and cost advantages

• Global South loyalty maintenance via comprehensive development assistance programmes

• Western alternative struggles due to higher costs and smaller scale operations

• Limited market diversification despite substantial government investment in alternatives

This scenario assumes Chinese technology advantages prove more durable than currently anticipated while alternative capacity development encounters greater obstacles than projected.

Scenario 2: Bipolar Supply Chain Development

Under this evolution, coordinated Western investment successfully creates alternative processing capacity reaching 30-40% market share by 2030, establishing a bipolar market structure with Chinese and Western supply chains serving different customer bases based on geopolitical alignment and security considerations.

Characteristics of bipolar development include:

• Regional processing hubs serving allied nation demand independently of Chinese capacity

• Technology competition intensification as both blocs invest heavily in processing advancement

• Premium pricing for non-Chinese supply chain participation

• Market segmentation based on security requirements rather than pure economic optimisation

This scenario requires sustained government support for alternative capacity through the inevitable period of higher costs and operational challenges during capacity ramp-up.

Scenario 3: Multipolar Fragmentation

The most complex potential outcome involves development of multiple regional supply chains with Chinese market share reduced to 50-60% through successful capacity development in Australia, Canada, Brazil, and other resource-rich nations that achieve independent processing capabilities.

Multipolar characteristics include:

• Increased price volatility from multiple supplier interactions and reduced coordination

• Technology diversification as different regions develop distinct processing approaches

• Supply chain complexity requiring sophisticated risk management across multiple sources

• Reduced Chinese leverage but potentially higher overall system costs and coordination challenges

This scenario offers the greatest supply security but potentially the highest economic costs due to reduced economies of scale and increased coordination requirements.

Disclaimer: The scenarios presented represent potential future developments based on current trends and policy directions. Actual outcomes will depend on numerous factors including technological breakthroughs, policy changes, and geopolitical developments that cannot be predicted with certainty. Investment decisions should not be based solely on these projections.

The next major ASX story will hit our subscribers first

What Investment Implications Emerge from China's Strategy?

The evolving rare earth landscape creates distinct investment opportunities and risks that require sophisticated analysis of geopolitical trends, technological development, and market dynamics. Understanding these implications helps investors navigate a sector where strategic considerations increasingly override traditional economic factors.

Risk Assessment Framework

Investment in rare earth-related opportunities demands comprehensive risk evaluation that extends beyond traditional financial metrics to encompass regulatory, geopolitical, and supply chain factors that can dramatically impact returns regardless of operational performance.

Critical risk categories include:

• Regulatory uncertainty from evolving export controls and trade restrictions

• Technology obsolescence risks from breakthrough developments in processing or alternative materials

• Geopolitical disruption potential affecting supply chain access and market relationships

• Environmental compliance costs that may not be fully reflected in current project economics

Supply chain disruption probability assessments must consider not just direct restrictions but also secondary effects from financial system limitations, insurance constraints, and shipping complications that can emerge during geopolitical tensions.

Opportunity Identification

The transition toward supply chain diversification creates investment opportunities across multiple stages of rare earth development, from mining through processing to downstream manufacturing applications. However, these opportunities require patient capital and risk tolerance for extended development timelines.

Primary opportunity categories include:

• Western rare earth processing companies positioned to capture market share from Chinese competitors

• Technology development investments in breakthrough processing methods or alternative materials

• Downstream manufacturing security for companies reducing Chinese supply chain dependence

• Infrastructure development supporting alternative rare earth supply chains

Valuations for Western rare earth companies often reflect substantial premiums for supply chain security benefits rather than traditional financial metrics, requiring investment approaches that account for strategic value creation.

Portfolio Hedging Strategies

Given the volatile intersection of geopolitics and commodity markets, effective rare earth investment strategies require hedging approaches that protect against multiple potential disruption scenarios while maintaining exposure to positive supply chain evolution trends.

Effective hedging strategies include:

• Geographic diversification across multiple supply chain jurisdictions

• Technology exposure balancing between current and alternative processing methods

• Demand sector spreading across different end-use applications with varying security requirements

• Timeline diversification balancing near-term operational investments with longer-term capacity development

The correlation between rare earth investments and broader geopolitical tensions requires portfolio construction that can withstand extended periods of heightened uncertainty while capturing benefits from eventual supply chain stabilisation.

How Should Investors Navigate This Geopolitical Landscape?

Successfully investing in the rare earth sector during this period of strategic competition requires sophisticated understanding of both commercial and political dynamics that influence market evolution. Traditional investment approaches must adapt to incorporate geopolitical analysis and policy risk assessment alongside financial metrics.

Due Diligence Enhancement

Investment analysis in rare earth opportunities demands expanded due diligence processes that evaluate political risks, regulatory compliance, and strategic positioning alongside traditional financial and operational assessments. This enhanced analysis becomes particularly critical given the sector's intersection with national security considerations.

Enhanced due diligence requirements include:

• Supply chain traceability analysis documenting complete material flows and dependencies

• Regulatory compliance monitoring across multiple jurisdictions with evolving trade restrictions

• Government relationship assessment evaluating official support and policy alignment

• Strategic positioning evaluation determining competitive advantages in diversifying markets

Alternative source verification requires technical assessment of processing capabilities, quality standards, and cost competitiveness compared to established Chinese suppliers, often requiring specialised expertise not typically needed for traditional commodity investments.

Strategic Positioning Recommendations

Effective rare earth investment strategies must align with the broader geopolitical trends driving supply chain evolution while maintaining flexibility to adapt as political and economic conditions change. This requires balancing exposure to different development scenarios and timeline assumptions.

Strategic positioning principles include:

• Processing capacity investment priorities focusing on technologies and locations most likely to achieve commercial viability

• Technology development partnerships that provide access to breakthrough capabilities while sharing development risks

• Government relations importance recognising the critical role of policy support in sector economics

• Market timing considerations accounting for the extended development cycles typical in rare earth projects

The most successful rare earth investments typically involve companies with strong government backing, proven technical capabilities, and patient capital structures capable of weathering extended development periods and market volatility.

Risk Mitigation Approaches

Given the inherent volatility and political sensitivity of rare earth markets, effective risk mitigation requires multi-layered strategies that protect against supply disruptions, regulatory changes, and market volatility while maintaining upside exposure to sector growth and diversification trends.

Comprehensive risk mitigation includes:

• Diversified supplier networks reducing dependence on single sources or regions

• Inventory buffer strategies providing protection against short-term supply disruptions

• Contractual protection mechanisms including force majeure provisions and alternative sourcing rights

• Insurance and hedging instruments where available to protect against specific risk categories

The evolving nature of rare earth markets requires regular strategy reassessment as geopolitical conditions change and alternative supply capacity comes online, demanding active management rather than passive investment approaches.

Investment Disclaimer: The analysis presented here is for informational purposes only and should not be considered as investment advice. Rare earth investments involve significant risks including regulatory changes, geopolitical tensions, technology obsolescence, and market volatility. Past performance does not guarantee future results, and investors should conduct their own due diligence and consult with qualified financial advisors before making investment decisions. The evolving nature of geopolitical competition in this sector creates uncertainties that may not be fully captured in traditional financial analysis.

Looking for opportunities in small-cap ASX rare earth companies?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant rare earth and critical minerals discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market as supply chain diversification accelerates. Understanding why historic discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page showcases exceptional outcomes in the critical minerals sector, then begin your 30-day free trial today to position yourself ahead of the market.