June 6, 2026

China's rare earth export controls represent a sophisticated evolution in economic statecraft, demonstrating how resource concentration creates strategic leverage beyond traditional trade mechanisms. The implementation of china rare earth export controls through targeted restrictions on critical elements exemplifies a new paradigm where geological advantages translate directly into geopolitical influence. Understanding these dynamics requires examining how supply chain dependencies function across multiple processing stages, from extraction through final manufacturing integration.

Critical materials differ fundamentally from traditional commodities because substitution barriers, processing complexity, and end-use applications create inelastic demand patterns. When governments control both upstream resources and downstream processing capacity, they possess multiple intervention points within global supply chains. This multi-stage control architecture enables graduated escalation strategies where restrictions can be tightened or relaxed based on diplomatic objectives rather than market fundamentals.

Understanding the Strategic Framework Behind China's Critical Materials Policy

China's approach to china rare earth export controls reflects sophisticated integration of resource management with broader economic statecraft objectives. The framework encompasses licensing requirements, end-user verification protocols, and extraterritorial compliance mechanisms targeting specific elements essential to modern technology manufacturing. This system operates through the Ministry of Commerce (MOFCOM), which administers export permits based on strategic assessments rather than purely commercial considerations.

The policy architecture distinguishes between market-based trade tools and access-based strategic controls. While traditional tariffs function as price deterrents, china rare earth export controls operate through scarcity creation, generating what analysts characterise as strategic monopoly leverage. This approach enables Beijing to influence downstream manufacturing sectors without directly restricting final products, creating compliance burdens and supply uncertainty that extend far beyond immediate rare earth users.

China's dominance across the rare earth value chain provides the foundation for this strategic framework:

-

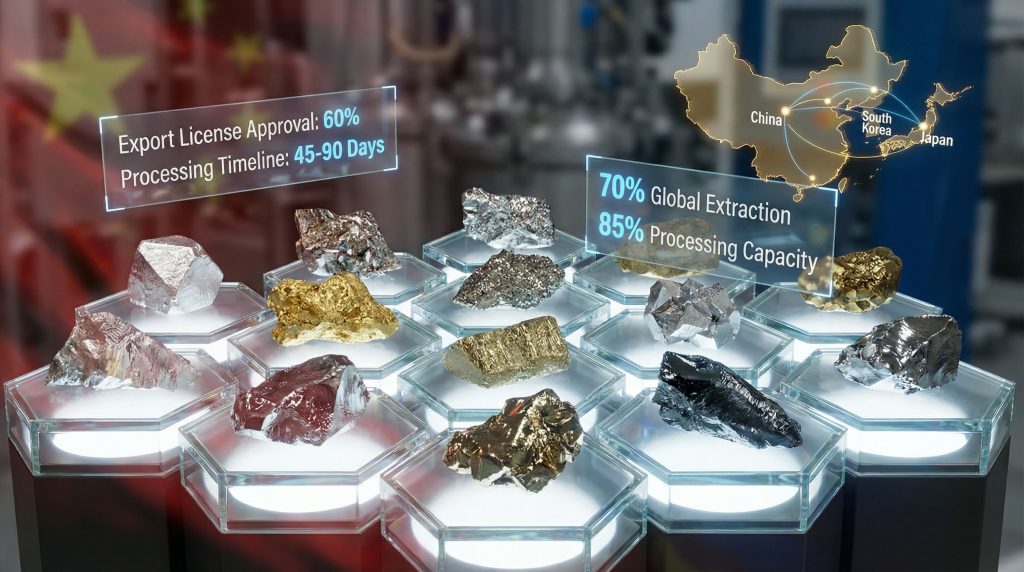

Mining operations: China accounts for approximately 60% of global rare earth element production, concentrated primarily in Inner Mongolia's Baiyun Obo deposit and lighter rare earth mines across Southern China's Guangdong, Sichuan, and Yunnan provinces

-

Processing capacity: Chinese separation facilities handle over 85% of global rare earth oxide and metal production, creating bottlenecks that cannot be bypassed through raw material diversification alone

-

Manufacturing integration: Downstream magnet and component production remains heavily concentrated in Chinese facilities, completing the vertical control structure

The regulatory framework governing these controls has undergone successive tightening cycles since 2010. Initial licensing requirements established following WTO dispute panel decisions evolved through integration into China's "Made in China 2025" industrial policy framework. Recent reformulations emphasise national strategic interests language, with 2025 amendments introducing extraterritorial provisions that extend control reach to products containing even trace amounts of Chinese-sourced materials.

This institutional architecture involves multiple state agencies operating under State Council guidance. MOFCOM administers export licensing whilst the National Development and Reform Commission manages production quotas, and provincial authorities enforce environmental compliance tied to extraction permits. This multi-agency framework creates opportunities for policy escalation where licensing denials can be justified through environmental or quota rationales rather than explicit geopolitical grounds, providing strategic plausible deniability.

When big ASX news breaks, our subscribers know first

How China's Two-Wave Control System Actually Works

The current Chinese rare earth export control system operates through two distinct implementation waves, each targeting different strategic objectives. This phased approach reflects calculated understanding of substitution barriers and regulatory compliance costs as separate mechanisms of economic leverage.

The April 2025 Heavy Rare Earth Restrictions

The initial wave focuses on seven critical heavy rare earth elements: dysprosium, terbium, gadolinium, samarium, lutetium, scandium, and yttrium. These elements function as bottleneck materials in high-performance applications where substitution remains technically or economically unviable. The targeting strategy reflects deep understanding of downstream manufacturing dependencies and processing limitations.

Licensing Mechanism Details:

-

Pre-shipment documentation: Exporters must submit end-user certificates identifying importing companies, registered business locations, and stated end-use applications

-

Application processing: MOFCOM review examines end-user legitimacy through cross-reference with import-export registries and sector-specific regulatory compliance databases

-

Processing timeline: Standard 45-day review period with documented extension authority to 90 days for geopolitically-sensitive applications

-

Shipment tracking: Licensed exports require real-time monitoring through Chinese customs (General Administration of Customs)

The control mechanism succeeds because Chinese separation facilities control the oxide and metal production stage where these elements become industrially usable. Companies cannot source unprocessed rare earth ore from alternative locations like Mongolia, Vietnam, or Tanzania and bypass Chinese processing without developing alternative separation facilities – a capital-intensive process requiring 3-7 years to reach commercial scale.

The October 2025 Expanded Framework

The second wave expanded controls to five additional elements: holmium, erbium, thulium, europium, and ytterbium, whilst introducing extraterritorial provisions that fundamentally alter the regulatory landscape. The 0.1% threshold mechanism transforms these controls from simple supply restrictions into comprehensive compliance frameworks.

This expansion creates two distinct compliance pathways:

-

Direct application: Companies exporting rare earth oxides or metals remain subject to MOFCOM licensing requirements as established in the April wave

-

Indirect application: Companies manufacturing products incorporating even trace amounts of Chinese rare earth materials or technology must theoretically obtain export permits for finished products

The extraterritorial reach extends to manufacturing equipment, technical expertise, and production know-how, creating compliance uncertainty for multinational corporations operating complex supply chains. A Japanese automotive manufacturer using magnets containing Chinese-sourced dysprosium as a minor alloy component would theoretically require MOFCOM export permission for completed vehicles – generating compliance burdens of uncertain enforceability but clear strategic impact.

Current Implementation Status

The October 2025 controls currently remain under temporary suspension until November 2026, representing formal regulatory pause rather than policy abandonment. During this suspension period, pre-existing export licences maintain validity whilst no new licences are issued for the five October-wave elements. This structure preserves Beijing's ability to resume enforcement without requiring new regulatory authorisation, functioning as a negotiation mechanism rather than policy reversal.

Recent market indicators demonstrate the system's effectiveness even during partial implementation. Following the April 2025 control announcement, dysprosium oxide spot prices increased from approximately $1,200-1,400 per kilogram to $1,800-2,100 per kilogram, reflecting supply uncertainty premiums rather than actual scarcity. Terbium oxide prices escalated from $3,000-3,500 per kilogram to $4,200-4,800 per kilogram within 60 days, indicating market expectations of sustained supply constraints.

What Makes These Controls Different from Traditional Trade Barriers?

China's rare earth export controls operate through fundamentally different mechanisms than conventional trade policy instruments. Understanding these distinctions clarifies why traditional economic responses prove insufficient when addressing strategic resource restrictions.

| Control Mechanism | Traditional Tariffs | China's REE Controls |

|---|---|---|

| Primary Function | Price-based market deterrent | Supply access restriction |

| Market Selectivity | Broad product categories | Element-specific precision targeting |

| Enforcement Method | Customs-based collection | End-user verification and tracking |

| Strategic Objective | Revenue generation or protection | Industrial leverage and dependency creation |

| Policy Reversibility | Domestic policy-dependent | Geopolitically-driven and conditional |

| Substitution Response | Price elasticity drives alternatives | Technical barriers limit substitution |

Traditional trade barriers function through price mechanisms, making imports more expensive but not impossible. Companies can absorb higher costs, seek alternative suppliers, or pass expenses to consumers. China's rare earth controls eliminate these options by restricting access regardless of price willingness, creating binary outcomes where materials are either available or unavailable based on regulatory approval.

The selectivity difference proves equally important. Tariffs typically apply to broad product classifications (steel, automobiles, electronics) whilst rare earth controls target specific elements within complex supply chains. This precision enables surgical economic pressure without triggering comprehensive trade war dynamics, allowing continued cooperation in non-targeted sectors whilst maintaining leverage over critical applications.

Enforcement mechanisms reflect these strategic differences. Tariff collection occurs at border crossings through established customs procedures, whilst rare earth export licensing requires ongoing compliance monitoring and end-use verification. This creates sustained regulatory interaction between Chinese authorities and foreign companies, generating information advantages about downstream applications and supply chain structures.

The strategic objectives distinguish these controls most clearly from conventional trade policy. Tariffs aim to protect domestic industries or generate revenue, creating temporary market adjustments that companies can adapt to through efficiency improvements or alternative sourcing. Rare earth controls seek to create permanent dependency relationships where foreign manufacturers require Chinese approval for continued operations, establishing ongoing leverage rather than one-time economic adjustment.

Why Japan Remains Structurally Vulnerable Despite Diversification Efforts

Japan's continued exposure to china rare earth export controls reflects structural dependencies that cannot be resolved through conventional diversification strategies. Despite significant investment in alternative supply chain development since 2010, Japanese manufacturers remain vulnerable across three critical stages of rare earth processing.

Upstream Mining Dependencies

Whilst Japan has successfully diversified raw rare earth ore sourcing through investments in Australian, Malaysian, and Vietnamese mining operations, this diversification provides limited protection against downstream processing controls. Rare earth ores require extensive separation and purification before becoming industrially useful, with each element requiring specialised chemical processing techniques.

Chinese separation facilities maintain technical advantages developed over decades of production experience:

-

Process optimisation: Chinese facilities achieve higher recovery rates and lower processing costs through accumulated expertise and scale economies

-

Environmental externalisation: Rare earth separation generates significant radioactive and chemical waste, with Chinese facilities operating under less stringent environmental standards than potential Western competitors

-

Integrated supply chains: Chinese separation facilities benefit from proximity to both upstream mining operations and downstream manufacturing, reducing transportation and coordination costs

Midstream Processing Bottlenecks

The separation of rare earth elements into individual oxides and metals represents the most critical bottleneck in global supply chains. This process requires specialised facilities, technical expertise, and regulatory approval for handling radioactive materials. China controls approximately 85% of global separation capacity, with no alternative facilities capable of processing heavy rare earth elements at commercial scale outside Chinese territory.

Attempts to develop alternative processing capacity face multiple constraints:

-

Capital requirements: Building commercial-scale separation facilities requires $500 million to $2 billion in initial investment, with uncertain return timelines

-

Technical complexity: Separation processes involve proprietary knowledge developed through decades of industrial experience, creating intellectual property barriers

-

Regulatory approval: Environmental and safety approvals for rare earth processing facilities face substantial political and community opposition in developed countries

-

Economic viability: Chinese facilities benefit from scale economies and government subsidies that make competition economically challenging even with operational facilities

Downstream Manufacturing Integration

Japan's most critical vulnerability exists in permanent magnet manufacturing, where Chinese suppliers dominate global production of neodymium-iron-boron (NdFeB) magnets essential to electric vehicle motors, wind turbines, and advanced electronics. Approximately 95% of global NdFeB magnet production occurs in China, predominantly in Shandong and Zhejiang provinces.

The magnet manufacturing process involves multiple stages where Chinese control creates compounding vulnerabilities:

- Alloy processing and homogenisation (China controls ~85% of capacity)

- Casting and crystallisation (China controls ~70% of capacity)

- Machining and magnetisation (China controls ~60% of capacity)

Even if Japanese manufacturers source rare earth oxides from alternative suppliers, they typically cannot obtain finished NdFeB magnets without Chinese processing involvement. This creates the paradox where Japan leads in high-precision manufacturing whilst remaining dependent on Chinese-controlled inputs for critical components.

Inventory Limitations and Strategic Stockpiling

Japan maintains strategic rare earth stockpiles through government and private sector initiatives, but these provide only temporary protection against sustained supply disruptions. Rare earth elements and processed materials face degradation challenges that limit long-term storage effectiveness:

-

Oxidation sensitivity: Many rare earth metals require controlled atmosphere storage to prevent degradation

-

Inventory carrying costs: Strategic stockpiles tie up significant capital in slowly-moving materials

-

Technology evolution: Rapid changes in end-use applications can render stored materials less valuable or technically obsolete

Current Japanese stockpiles provide approximately 6-12 months of operational continuity under normal demand conditions, insufficient to bridge the 3-7 year timeline required for alternative supply chain development.

How Export Control Timing Reveals Strategic Calculation

The implementation timing of China's rare earth export controls demonstrates sophisticated understanding of global supply chain development cycles and strategic vulnerability windows. Beijing's restriction announcements consistently precede meaningful alternative capacity development by several years, maximising leverage whilst minimising effective countermeasures.

The Pre-Capacity Gap Strategy

China's control timing exploits the gap between Western policy announcements and operational capacity development. Government initiatives in the United States, Europe, Japan, and Australia have announced billions in funding for rare earth supply chain independence, yet commercial-scale alternative facilities remain in development phases with completion timelines extending into the late 2020s.

This creates a strategic window where:

-

Policy commitments exist but lack operational backing through functioning alternative supply chains

-

Investment capital has been allocated but not yet converted into production capacity

-

Technical partnerships are forming but have not achieved commercial-scale operations

-

Regulatory frameworks are being established but do not yet govern operational facilities

The April and October 2025 control implementations occur during this vulnerability period, when target countries have committed to supply chain independence but lack the industrial infrastructure to achieve it. This timing maximises economic disruption whilst minimising the effectiveness of policy responses.

Market Conditioning and Escalation Testing

The two-wave implementation structure functions as market conditioning for potential permanent restrictions. By introducing controls in phases with temporary suspensions, Beijing can:

-

Test market responses to different restriction levels without committing to permanent escalation

-

Gauge political reactions from target countries and adjust implementation based on diplomatic feedback

-

Condition expectations among downstream manufacturers to accept Chinese regulatory oversight as normal business practice

-

Preserve escalation options whilst maintaining diplomatic flexibility through suspension and resumption mechanisms

Correlation with Diplomatic Cycles

Export control timing demonstrates coordination with broader geopolitical developments rather than market-driven decision making. Recent restrictions correlate with:

-

Japanese foreign policy positions on Taiwan and regional security arrangements

-

US-China trade negotiation cycles and technology competition dynamics

-

Broader alliance coordination on critical minerals strategy resilience

This pattern indicates that rare earth controls function as diplomatic signalling mechanisms rather than purely economic policy tools. The ability to quickly impose or suspend restrictions provides Beijing with responsive leverage that can be calibrated to specific international developments.

What the Extraterritorial Provisions Actually Mean for Global Supply Chains

The October 2025 extraterritorial provisions represent a qualitative escalation from supply restriction to comprehensive compliance framework. The 0.1% threshold mechanism transforms rare earth controls from bilateral trade measures into multilateral regulatory systems affecting companies with minimal direct Chinese rare earth exposure.

Secondary Boycott Architecture

The extraterritorial provisions create potential secondary boycott scenarios where companies face Chinese regulatory oversight regardless of their direct rare earth sourcing strategies. This mechanism operates through:

-

Supply chain traceability requirements: Companies must verify and document the origin of rare earth materials throughout complex multi-tier supplier networks

-

Technology transfer implications: Manufacturing processes, equipment designs, and production techniques developed using Chinese rare earth inputs become subject to Chinese regulatory oversight

-

Joint venture complications: Technical partnerships or licensing agreements with Chinese entities extend regulatory reach to non-Chinese operations

Third-Country Manufacturing Impact

European and North American manufacturers face indirect exposure through supplier relationships and component integration. A German automotive company manufacturing electric vehicles in Mexico using magnets processed in Malaysia with Chinese rare earth inputs would theoretically require Chinese approval for vehicle exports under the extraterritorial framework.

This creates compliance complexity that extends far beyond traditional trade relationships:

-

Supplier certification requirements: Manufacturers must verify rare earth origin across multiple processing stages and intermediate suppliers

-

Technology documentation: Companies must maintain detailed records of Chinese rare earth integration into manufacturing processes and equipment

-

Regulatory uncertainty: The enforcement scope and compliance requirements remain intentionally ambiguous, creating business planning challenges

Compliance Architecture and Enforcement Challenges

The practical implementation of extraterritorial provisions faces significant technical and legal challenges that may limit their effectiveness whilst still creating strategic uncertainty:

Technical Verification Challenges:

-

Material traceability: Tracking 0.1% rare earth content through complex metallurgical processing and component integration presents substantial technical challenges

-

Testing limitations: Existing analytical methods may not reliably detect trace rare earth content in finished products, creating enforcement gaps

-

Documentation requirements: Comprehensive supply chain documentation for trace material content imposes significant administrative burdens

Legal Enforcement Limitations:

-

Jurisdictional conflicts: Extraterritorial enforcement may conflict with domestic regulatory frameworks in target countries

-

WTO compliance: The extraterritorial provisions may violate World Trade Organisation rules regarding trade restrictions and regulatory overreach

-

Enforcement mechanisms: China lacks direct enforcement authority over foreign companies operating outside Chinese territory, limiting practical compliance requirements

The next major ASX story will hit our subscribers first

How Different Industries Face Varying Vulnerability Levels

Rare earth supply chain dependencies create differentiated risk profiles across industrial sectors, with vulnerability levels determined by application criticality, substitution barriers, and supply chain concentration. Understanding these sector-specific exposures clarifies why blanket diversification strategies prove insufficient for comprehensive risk mitigation.

Automotive Sector Critical Dependencies

The automotive industry faces the highest acute vulnerability to rare earth supply disruptions due to electric vehicle adoption and advanced driver assistance system integration. Critical applications include:

High-Risk Applications:

-

Electric vehicle motors: Permanent magnet synchronous motors require dysprosium and terbium for high-temperature performance, with no commercially viable substitutes maintaining equivalent efficiency and power density

-

Hybrid powertrain systems: Neodymium-iron-boron magnets in hybrid electric vehicle motors and generators represent non-negotiable technical requirements for regulatory compliance and performance standards

-

Advanced driver assistance sensors: Radar and lidar systems incorporate rare earth-doped semiconductors and optical components with limited substitution options

Mitigation Constraints:

Current automotive sector mitigation strategies face fundamental limitations:

-

Recycling limitations: Magnet recycling provides less than 10% of automotive industry demand requirements, with technical barriers limiting recovery rates from complex automotive assemblies

-

Alternative chemistry performance: Ferrite and other non-rare-earth magnet technologies sacrifice 30-50% of power density, requiring larger, heavier motor designs that compromise vehicle efficiency and range

-

Supply diversification timeline: Developing non-Chinese magnet supply chains requires 5-7 year development periods, exceeding automotive product development cycles

Electronics Manufacturing Vulnerabilities

Electronics manufacturing faces broad but technically sophisticated rare earth dependencies across multiple component categories, creating complex mitigation challenges:

Critical Applications:

-

Smartphone manufacturing: Camera lens polishing requires cerium oxide with specific particle size distributions achievable only through controlled processing techniques

-

LED production: Phosphor materials incorporating europium and terbium create specific colour characteristics required for white LED lighting and display applications

-

Hard disk drive manufacturing: Neodymium magnets in voice coil motors require precise magnetic properties achievable only through controlled rare earth metallurgy

Supply Chain Complexity:

Electronics supply chains involve multiple processing stages where rare earth materials become integrated into components manufactured across different countries:

-

Semiconductor fabrication: Rare earth materials function as dopants and process chemicals in semiconductor manufacturing, with traceability challenges across complex multi-national supply chains

-

Component integration: Finished electronics incorporate rare earth materials through multiple component suppliers, creating verification and compliance challenges for extraterritorial provisions

-

Technology licensing: Electronics manufacturers rely on Chinese-developed processes and equipment for certain rare earth applications, extending regulatory reach through intellectual property relationships

Renewable Energy Infrastructure Dependencies

Wind power and solar energy systems incorporate rare earth materials in critical components where performance requirements limit substitution options:

Wind Power Systems:

-

Generator magnets: Direct-drive wind turbine generators use large permanent magnets containing dysprosium for high-temperature stability, with magnet requirements scaling with turbine capacity

-

Power electronics: Inverter and transformer systems incorporate rare earth materials in magnetic cores and specialised alloys

Solar Energy Systems:

-

Inverter manufacturing: Grid-tie inverters use rare earth permanent magnets in high-frequency transformers and power conversion systems

-

Tracking systems: Solar panel tracking mechanisms incorporate rare earth magnets for precise positioning and weather resistance

Defence and Aerospace Applications

Military and aerospace applications represent the highest strategic criticality despite lower volume consumption, with performance requirements that eliminate substitution options:

-

Guidance systems: Precision-guided munitions and navigation systems require rare earth permanent magnets for actuators and sensors

-

Radar systems: Military radar applications incorporate rare earth materials in high-power amplifiers and signal processing components

-

Jet engine components: Advanced alloys incorporating rare earth elements provide high-temperature performance in military aircraft engines

These applications face absolute substitution barriers where performance degradation creates operational mission failures rather than economic inefficiencies.

Why Traditional Commodity Market Analysis Fails Here

Conventional commodity market frameworks prove inadequate for analysing rare earth supply chains because these materials function as strategic assets rather than market-traded commodities. Standard economic models based on supply-demand equilibrium, price elasticity, and substitution effects cannot predict or explain rare earth market behaviour during restriction periods.

Strategic Assets vs. Commodity Pricing

Rare earth elements operate through what analysts describe as "strategic valve" mechanisms rather than traditional commodity price discovery:

Supply Concentration Effects:

- Market concentration enables coordinated supply restriction policies that override price signals

- Producers can maintain artificial scarcity regardless of demand levels or price premiums

- Alternative suppliers lack capacity to respond to price incentives through increased production

Substitution Barriers:

- Technical performance requirements eliminate price-sensitive substitution responses

- Demand remains inelastic even at significant price premiums because alternative materials cannot meet performance specifications

- End-use applications require specific rare earth elements with no economically viable alternatives

Processing Complexity:

- Multi-stage control opportunities enable intervention at different points in supply chains

- Processing bottlenecks create leverage independent of raw material availability

- Technical expertise requirements limit the number of potential alternative suppliers

Policy-Driven Price Discovery

Rare earth markets experience price volatility driven by geopolitical risk assessments rather than supply-demand fundamentals. This creates pricing patterns that confuse traditional commodity analysis:

Speculation-Driven Volatility:

During control announcements, rare earth prices demonstrate extreme volatility reflecting uncertainty premiums rather than actual supply constraints. Dysprosium oxide prices increasing 50-70% within 60 days of the April 2025 control announcement despite unchanged physical supply availability illustrates this disconnect between price signals and market fundamentals.

Inventory Hoarding Effects:

Downstream manufacturers respond to control announcements through strategic inventory accumulation, creating temporary demand spikes that further distort price signals. These inventory building cycles generate short-term price increases followed by demand normalisation as strategic stockpiles reach target levels.

Government Stockpiling Programmes:

Strategic stockpiling by government entities creates additional demand layers independent of commercial consumption patterns. These programmes operate through different decision-making criteria than commercial purchasers, generating price support that may not reflect underlying industrial demand.

Market Structure Inefficiencies

Traditional commodity markets rely on transparent pricing, multiple suppliers, and standardised products. Rare earth markets lack these characteristics:

Price Transparency Limitations:

- Most rare earth transactions occur through private contracts with non-disclosed pricing terms

- Spot market trading represents minimal volume compared to long-term supply agreements

- Published price indices may not reflect actual transaction prices or market conditions

Quality and Specification Variations:

- Rare earth materials vary significantly in purity, particle size, and chemical composition based on processing techniques

- End-users require specific material specifications that limit supplier interchangeability

- Quality differences create supplier lock-in effects independent of price considerations

Information Asymmetries:

- Chinese suppliers maintain superior information about global demand patterns and supply constraints

- Western buyers lack visibility into Chinese production capacity, inventory levels, and government policy intentions

- Market participants operate with incomplete information about actual supply availability and competitive alternatives

What This Means for Investment and Policy Strategy

The structural nature of rare earth supply chain dependencies requires fundamental reorientation of both investment strategies and policy frameworks. Traditional approaches based on market diversification and price hedging prove insufficient when addressing strategic resource controls that operate outside conventional economic mechanisms.

Corporate Risk Management Framework

Companies exposed to rare earth supply chain risks must develop comprehensive strategies addressing multiple vulnerability dimensions simultaneously:

Immediate Risk Assessment:

-

Supply chain mapping: Comprehensive identification of rare earth exposure across all product lines, including indirect exposure through component suppliers and sub-contractors

-

Criticality analysis: Ranking of rare earth applications by operational importance, substitution difficulty, and supply concentration to prioritise risk mitigation investments

-

Scenario planning: Development of response strategies for different restriction levels and enforcement patterns, including graduated supply reductions and complete access denial

Strategic Supply Chain Restructuring:

-

Supplier diversification: Qualification and relationship development with non-Chinese suppliers, despite current capacity limitations and higher costs

-

Vertical integration: Investment in rare earth processing capabilities or equity stakes in alternative supply chain development projects

-

Technology adaptation: Research and development programmes for substitute materials, alternative manufacturing processes, and design modifications that reduce rare earth content

Financial Risk Management:

-

Strategic inventory optimisation: Balancing inventory carrying costs against supply security, with inventory levels calibrated to realistic alternative supply development timelines

-

Insurance and hedging: Development of supply chain insurance products and financial hedging mechanisms for rare earth price and availability risks

-

Capital allocation: Prioritising investments in supply chain resilience over short-term cost optimisation when strategic materials are involved

Government Policy Response Architecture

National governments face complex tradeoffs between defensive measures that reduce vulnerability and offensive capabilities that create reciprocal leverage opportunities. This becomes particularly relevant as countries develop their own critical minerals energy transition strategies:

Defensive Policy Measures:

-

Strategic stockpile expansion: Government-managed reserves calibrated to provide bridge capacity during supply disruptions whilst alternative sources develop

-

Allied coordination frameworks: Multilateral cooperation on supply chain resilience, information sharing, and coordinated response to supply restrictions

-

Regulatory framework development: Trade policy reciprocity mechanisms and legal frameworks for addressing extraterritorial compliance requirements

Offensive Capability Development:

-

Critical materials leverage: Development of export controls on materials where Western countries maintain supply advantages (lithium, cobalt, specialised semiconductors)

-

Technology transfer restrictions: Limiting Chinese access to processing technologies, equipment, and technical expertise required for rare earth supply chain advancement

-

Financial system leverage: Using banking and financial market access as reciprocal pressure mechanisms during supply restriction periods

Investment and Industrial Policy:

-

Domestic capacity incentives: Financial incentives for rare earth processing facility development, including risk-sharing mechanisms and guaranteed purchase agreements

-

Research and development funding: Government support for substitute material research, recycling technology development, and alternative supply chain innovations

-

International partnership development: Coordinated investment in alternative supply countries and processing facility development in allied nations

Furthermore, countries are implementing comprehensive critical minerals reserve strategy frameworks to ensure supply security. The US critical minerals order demonstrates how policy responses are evolving to address these strategic vulnerabilities.

Investment Strategy Implications

Traditional commodity investment approaches require modification when applied to rare earth markets where strategic considerations override commercial dynamics:

Direct Investment Considerations:

-

Geographic risk assessment: Evaluating rare earth investments based on geopolitical stability and strategic alignment rather than purely geological or economic factors

-

Technology and processing focus: Prioritising investments in separation, processing, and downstream manufacturing capabilities over raw mining operations

-

Timeline expectations: Accepting longer investment payback periods due to the strategic nature of these materials and government policy support

Portfolio Risk Management:

-

Diversification strategies: Balancing rare earth exposure across different elements, processing stages, and geographic locations to reduce concentration risk

-

Hedging mechanisms: Developing financial instruments for rare earth supply chain risks, potentially including political risk insurance and supply guarantee products

-

Strategic partnerships: Forming alliances with end-users, government entities, and other investors to share risks and coordinate supply chain development

How the Suspension-Extension Cycle Creates Strategic Uncertainty

China's implementation of temporary suspensions and potential resumptions in its rare earth export controls creates calculated uncertainty that may prove more strategically valuable than permanent restrictions. This approach generates continuous compliance costs and strategic planning challenges for target countries whilst preserving Beijing's escalation options and diplomatic flexibility.

The Negotiation Leverage Architecture

The November 2026 suspension timeline for October 2025 controls creates a structured negotiation period where multiple stakeholders face different incentive structures:

For Chinese policymakers:

- Maintains threat credibility whilst allowing space for diplomatic progress on broader trade and technology issues

- Preserves the ability to resume restrictions without requiring new regulatory authorisation or domestic political justification

- Creates recurring negotiation cycles that generate sustained pressure rather than one-time policy adjustment

For target countries:

- Forces continued investment in alternative supply chain development without certainty about future restrictions

- Creates recurring decision points about policy concessions versus supply chain independence investment

- Generates sustained political attention to rare earth vulnerabilities that may not be sustainable over multiple cycles

For private sector:

- Requires sustained investment in supply chain risk mitigation without clarity about future threat levels

- Creates permanent compliance and monitoring costs even during suspension periods

- Forces strategic planning based on worst-case scenarios rather than current operational requirements

Market Conditioning and Expectations Management

The suspension-extension cycle functions as market conditioning for potential permanent implementation by establishing regulatory frameworks and compliance expectations during temporary periods:

Regulatory Infrastructure Development:

During suspension periods, Chinese regulatory agencies maintain and refine licensing systems, end-user verification databases, and enforcement mechanisms. This creates operational readiness for rapid resumption whilst generating detailed intelligence about foreign supply chain structures and dependencies.

Compliance System Integration:

Foreign companies must develop and maintain compliance systems during suspension periods to prepare for potential resumption. These systems create ongoing costs and operational complexity that persist regardless of current enforcement status.

Supply Chain Behaviour Modification:

The possibility of future restrictions influences supply chain decisions during suspension periods, as companies adjust sourcing, inventory, and investment strategies based on potential rather than actual restrictions.

Reading the Diplomatic Signal Framework

Control timing and suspension decisions correlate with broader diplomatic developments, suggesting coordination with other economic statecraft tools:

Taiwan Policy Correlation:

Restriction announcements and suspension decisions demonstrate correlation with Japanese government positions on Taiwan policy and regional security arrangements. This suggests rare earth controls function as response mechanisms for broader strategic disagreements rather than standalone trade policy.

Technology Competition Integration:

Export control timing aligns with developments in semiconductor restrictions, artificial intelligence cooperation limitations, and other technology-related trade measures, indicating coordination across different strategic resource categories.

Allied Coordination Response:

Chinese policy adjustments appear to respond to multilateral coordination efforts among G7 countries, NATO allies, and Indo-Pacific security partners, suggesting sensitivity to collective response strategies rather than bilateral negotiations alone.

What Comes Next: Scenario Planning Framework

Future developments in China's rare earth export control system will likely follow one of several strategic pathways, each reflecting different assessments of Western vulnerability, alternative supply development progress, and broader geopolitical competition dynamics.

Scenario Analysis: Graduated Tightening

Implementation Pattern:

Progressive extension of controls to additional rare earth elements currently outside licensing requirements, combined with reduced approval rates for existing controlled elements and enhanced enforcement of extraterritorial provisions.

Indicators to Monitor:

- Expansion of controls to light rare earth elements (lanthanum, cerium, praseodymium)

- Integration of rare earth processing equipment and technology transfer restrictions

- Mandatory technology licensing for companies using Chinese rare earth inputs

Strategic Logic:

This pathway assumes continued Western vulnerability and slow alternative supply development progress. Beijing would escalate pressure gradually to maximise economic disruption whilst minimising comprehensive retaliation risks.

Timeline Implications:

Implementation would likely occur through 2026-2028, targeting the period before significant non-Chinese processing capacity becomes operational. This timing would exploit the maximum vulnerability window whilst alternative supply chains remain in development phases.

Scenario Analysis: Selective Targeting

Implementation Pattern:

Country-specific restrictions based on foreign policy alignment, industry-specific exemptions for non-strategic applications, and conditional licensing tied to technology transfer agreements or diplomatic concessions.

Indicators to Monitor:

- Differential approval rates for different countries or end-use applications

- Explicit linkage between licensing decisions and broader diplomatic issues

- Preferential treatment for countries demonstrating strategic cooperation

Strategic Logic:

This approach would attempt to fragment Western coordinated responses by creating differentiated treatment that rewards cooperation and punishes confrontation. It reflects confidence in the ability to manage bilateral relationships separately rather than facing unified opposition.

Economic Impact:

Selective targeting could prove more economically efficient by maintaining revenue from cooperative partners whilst concentrating pressure on strategic competitors. However, it risks creating arbitrage opportunities and undermining the credibility of universal restrictions.

Diplomatic Implications:

This scenario would test alliance solidarity by creating economic incentives for individual countries to break from coordinated responses. Success would depend on Beijing's ability to offer sufficient economic benefits to overcome strategic alignment concerns.

Scenario Analysis: Comprehensive Implementation

Implementation Pattern:

Full enforcement of October 2025 extraterritorial provisions combined with expansion to additional rare earth elements and processing technologies, creating comprehensive Chinese oversight of global rare earth supply chains.

Indicators to Monitor:

- Active enforcement of the 0.1% threshold mechanism

- Expansion of licensing requirements to rare earth processing equipment and technology

- Integration with other strategic material export controls (gallium, germanium, bismuth)

Strategic Logic:

This scenario reflects maximum confidence in Chinese leverage and minimal concern about retaliation. It would represent a decisive shift from economic statecraft to comprehensive supply chain control.

Furthermore, this approach could also be observed in China's export control mechanics being applied to other strategic materials, creating a coordinated framework of resource-based leverage. Such developments would indicate Beijing's commitment to using strategic materials as instruments of geopolitical influence.

The success of comprehensive implementation would depend on China's assessment that alternative supply chains cannot develop quickly enough to provide meaningful alternatives, and that target countries lack sufficient retaliatory capabilities to impose unacceptable costs on Chinese interests.

Companies and governments monitoring these scenarios must prepare for each pathway whilst recognising that actual implementation may combine elements from multiple scenarios based on evolving strategic assessments and international responses. The complexity of rare earth supply chains ensures that china rare earth export controls will remain a critical factor in global economic and security planning for the foreseeable future.

According to the International Energy Agency's analysis, these export controls represent a new reality in critical minerals supply concentration risks. Additionally, analysis from White & Case highlights how China's extraterritorial jurisdiction provisions create unprecedented compliance challenges for global supply chains.

Need Strategic Minerals Intelligence for Your Portfolio?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including critical materials companies positioned to benefit from rare earth supply disruptions. With geopolitical tensions reshaping strategic minerals supply chains, Discovery Alert's dedicated discoveries page showcases historic examples of exceptional returns from major mineral discoveries. Begin your 30-day free trial today to identify actionable opportunities ahead of the market in this rapidly evolving sector.