June 19, 2026

The Processing Bottleneck That Defines Modern Geopolitical Risk

For decades, economists and strategists framed resource security around the question of who holds the ore. Reserves maps, drilling programmes, and mining licences dominated the conversation. However, the rare earth supply crisis unfolding across 2025 and 2026 has exposed a more uncomfortable truth: ownership of geology means very little when a single nation controls the industrial infrastructure needed to transform raw material into usable product.

This is the structural reality that sits beneath the current wave of China rare earth export controls. It is not simply a trade dispute or a diplomatic pressure tactic. It represents the culmination of decades of deliberate industrial policy that turned a geological advantage into a processing monopoly, and then converted that monopoly into geopolitical leverage of a kind that reserve data alone cannot capture.

Understanding what is actually happening in rare earth markets in 2025 and 2026 requires moving beyond headlines about bans and restrictions. It requires examining the architecture of the supply chain itself, the specific points of concentration that make substitution so difficult, and the realistic timelines facing nations that are now, belatedly, trying to build alternative capacity.

When big ASX news breaks, our subscribers know first

Why Geology Alone Cannot Explain China's Market Power

Reserves Are Distributed. Processing Is Not.

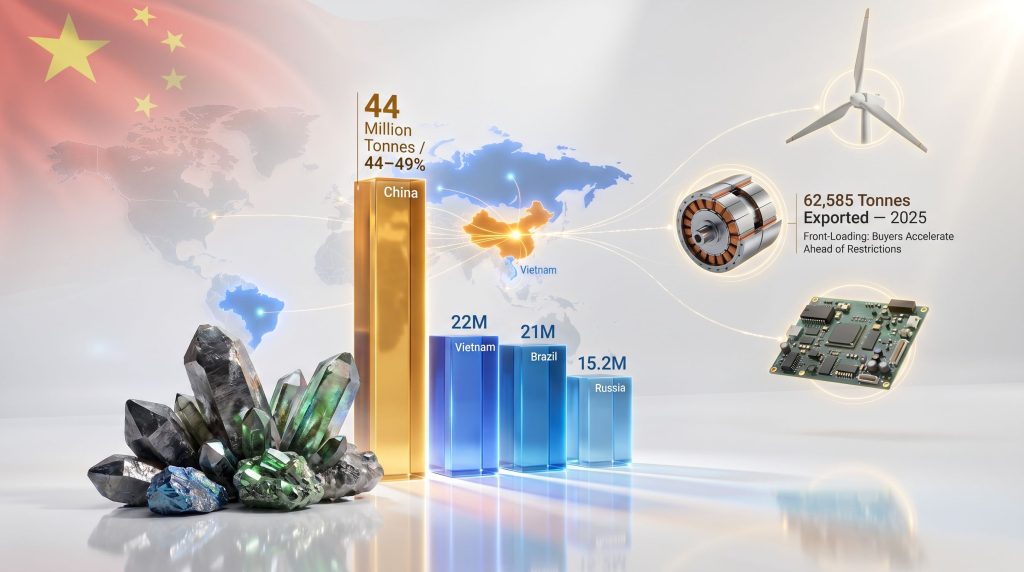

A common misconception holds that China dominates rare earths simply because it has the most of them. The reserve data does not fully support this narrative. China holds an estimated 44 million tonnes of identified rare earth reserves, representing roughly 44 to 49 percent of the global total. That is a significant concentration, but it is not monopolistic.

Consider the broader distribution of known reserves across other major economies:

| Country | Estimated Reserves (Million Tonnes) | Approximate Share of Global Total |

|---|---|---|

| China | 44 | 44–49% |

| Vietnam | 22 | ~11% |

| Brazil | 21 | ~10% |

| Russia | 15.2 | ~8% |

| India | 6.9 | ~3.5% |

| Australia | 5.7 | ~3% |

| United States | 2.3 | ~1% |

Vietnam and Brazil together account for roughly 32 to 38 percent of global identified reserves. Russia and India hold meaningful quantities. Australia and the United States are far from barren. On paper, the world has more than enough rare earth material to supply itself without relying on China at all.

The problem is not in the ground. The problem is in what happens after extraction.

The Separation and Refining Bottleneck

Rare earth elements are notoriously difficult to isolate from one another. They share nearly identical chemical properties, which means that conventional separation techniques are insufficient. Industrial-scale separation requires sophisticated solvent extraction processes, significant capital investment, and years of operational experience to optimise. China spent decades building this expertise, often at subsidised cost, while Western producers exited the market during periods of low prices in the 1990s and 2000s.

The result is a processing landscape where China controls an estimated 60 to 85 percent of global rare earth separation and refining capacity, despite holding less than half of global reserves. This means that ore extracted in Australia, Canada, or the United States frequently has no domestic processing pathway and must be shipped to China for separation. For a deeper examination of these structural constraints, the rare earth processing challenges facing the sector are considerable and well-documented.

Nations that secure mining rights without simultaneously developing domestic refining infrastructure will remain functionally dependent on Chinese processing capacity, regardless of where the ore is extracted. The refining bottleneck, not the mining bottleneck, is the defining constraint in rare earth supply chain security.

Embedded Exposure: The Hidden Layer of Dependence

Beyond direct rare earth exports lies a more opaque form of dependence. Rare earth elements embedded within finished components — such as permanent magnets in electric vehicle motors, turbine generators, missile guidance systems, and consumer electronics — are essentially invisible to standard trade monitoring. A tonne of exported rare earth compound appears clearly in customs data. The rare earths inside an assembled EV drivetrain or a wind turbine nacelle do not.

This embedded exposure is where China's leverage becomes most difficult to quantify and most dangerous to ignore. Even nations that believe they have reduced direct rare earth imports may carry significant indirect dependence through their manufactured goods supply chains.

How China's Export Controls Have Evolved: A Regulatory Timeline

From Technology Restrictions to Extraterritorial Reach

China's approach to rare earth export controls did not emerge suddenly. It has developed through a sequenced escalation strategy that progressively closes off the pathways nations might use to bypass restrictions. Furthermore, understanding China's rare earth strategy reveals just how deliberately this architecture has been constructed over time:

-

December 2023: Beijing prohibited the export of rare earth extraction, separation, and smelting technologies. This targeted process knowledge rather than physical commodities, making it illegal to transfer the industrial know-how that could allow other nations to build independent processing capability.

-

April 2025 (Wave 1): Licensing requirements were imposed on seven heavy rare earth elements, including associated compounds, metals, and magnets. Exporters were required to submit end-user declarations, creating a screening mechanism that allows Beijing to selectively approve or delay shipments based on the buyer's identity and intended use.

-

October 2025 (Wave 2): Controls expanded to five additional rare earth elements and extended restrictions to cover equipment, technical expertise, personnel, and critically, foreign-manufactured products incorporating Chinese-sourced rare earth inputs or processing technologies.

-

Post-October 2025: The second wave was suspended until November 2026, temporarily pausing the most expansive restrictions while structural uncertainty in global supply chains persists.

The Foreign Direct Product Rule Analogy

The October 2025 measures introduced a mechanism with significant extraterritorial implications. Under this framework, foreign manufacturers that incorporate Chinese rare earth inputs or use Chinese-developed processing technologies in their own products may require Chinese government approval before exporting those products to third countries.

This is structurally analogous to the United States foreign direct product rule applied to semiconductor technology, a tool Washington has used to restrict Huawei's access to chips manufactured anywhere in the world using American equipment or software. China has now applied a comparable logic to rare earth supply chains, representing a genuinely unprecedented move in commodity trade policy. White & Case has provided a detailed legal analysis of the extraterritorial jurisdiction implications of these measures.

The Distinction Between a Ban and a Control

A critical point is frequently misunderstood in public coverage of this issue. China has not banned rare earth exports. It has imposed a licensing and approval regime that creates uncertainty, extends lead times, enables selective denial, and allows Beijing to screen buyers for end-use purposes.

The practical effect of this approach is often more disruptive than an outright ban. A ban is predictable; buyers can plan around it. A licensing regime with opaque approval criteria and variable processing times forces manufacturers to hold larger inventories, pay risk premiums, and accept ongoing uncertainty about whether their next shipment will be approved. China's export restrictions, as the IEA has noted, mean that supply concentration risks are rapidly becoming reality rather than theoretical scenarios.

Trade Flow Data: What the Numbers Actually Reveal

The 2024 to 2025 Export Surge and What It Means

Trade data from the General Administration of Customs and the World Integrated Trade Solution reveals a striking pattern in Chinese rare earth export flows:

| Metric | 2024 | 2025 |

|---|---|---|

| Total Rare Earth Compound Exports (Tonnes) | 35,304 | 62,585 |

| Total Export Value (USD) | USD 377 million | Data pending |

| Top Importer (2024) | United States: 12,517 t / USD 104M | |

| Second Importer (2024) | Japan: 7,933 t / USD 134M |

At first glance, the surge from 35,304 tonnes in 2024 to 62,585 tonnes in 2025 appears to contradict the narrative of tightening restrictions. In reality, it confirms it. This volume increase reflects a front-loading dynamic, where global buyers accelerated purchases ahead of anticipated further restrictions following the April 2025 Wave 1 measures. This behaviour pattern mirrors historical commodity supply disruptions, where buyers deplete spot availability to build strategic buffers, temporarily inflating export volumes before supply tightens sharply.

Why Japan Pays More Per Tonne Than the United States

Japan's import profile offers a revealing insight into rare earth grade dynamics. Despite importing 7,933 tonnes compared to the United States' 12,517 tonnes in 2024, Japan's total import value of USD 134 million exceeded the American total of USD 104 million. This implies a significantly higher price per tonne for Japanese-bound material, reflecting Japan's preference for higher-purity, separation-ready, and magnet-grade rare earth compounds suited to its precision manufacturing and consumer electronics industries. Grade and specification premiums are a critical and often overlooked dimension of rare earth trade economics.

Downstream Processing Hubs Carrying Hidden Risk

Vietnam, South Korea, and the Netherlands appear as significant importers of Chinese rare earth compounds, but their role is frequently mischaracterised as end consumption. In practice, these nations function as midstream processing hubs, refining Chinese rare earth inputs for onward export in higher-value forms. Consequently, restrictions on Chinese exports create cascading disruption not just for final consumers, but for the entire downstream processing network that sits between Chinese mines and global manufacturers.

Which Industries Face the Greatest Supply Chain Exposure

Defence and Aerospace

Permanent magnets containing neodymium, dysprosium, and terbium are embedded in precision guidance systems, radar equipment, drone motors, and advanced munitions. The defence sector faces the dual problem of high rare earth dependence and the highest sensitivity around end-use declarations, making Chinese licensing approvals potentially subject to geopolitical considerations.

Electric Vehicles and Clean Energy

The clean energy transition has created what analysts describe as a clean energy paradox: the technologies intended to reduce dependence on fossil fuels have created deep new dependence on Chinese rare earth processing. Each EV motor typically contains approximately 1 to 2 kilograms of rare earth permanent magnets. Offshore wind turbines using direct-drive generators can require several hundred kilograms per unit. Scaling these technologies to net-zero targets without addressing the rare earth processing bottleneck is structurally inconsistent.

Consumer Electronics and Semiconductors

Smartphones, hard drives, speakers, and display systems all contain rare earth compounds at various stages of their production. At consumer volumes, the aggregate rare earth content embedded within global electronics manufacturing represents a supply chain exposure that no single alternative source can currently offset.

Building a Resilient Supply Chain: Strategic Frameworks

Three Levers Available to Rare Earth-Importing Nations

Nations confronting single-source dependence on Chinese rare earth processing have three primary strategic options, each with distinct timelines and capital requirements:

-

Upstream investment — Directing capital into mining and resource development in non-Chinese jurisdictions, including Australia, Canada, Brazil, and Greenland, to establish alternative ore supply.

-

Midstream technology transfer — Investing in domestic or allied-nation separation and refining infrastructure, the most capital-intensive and time-consuming element of supply chain independence.

-

Demand-side substitution — Funding research into magnet architectures that reduce or eliminate heavy rare earth content, including ferrite-based alternatives and rare earth-lean motor designs.

The Decade-Long Reality of Diversification

No single lever is sufficient in isolation, and none delivers results quickly. Building a rare earth separation facility from greenfield status typically requires seven to fifteen years when accounting for environmental approvals, community consultation, technical commissioning, and operational optimisation. This timeline creates an unavoidable window of structural vulnerability for G7 nations that are only now seriously engaging with supply chain diversification.

Bilateral resource agreements and critical minerals partnerships between allied nations can accelerate some stages of this process, particularly by enabling technology sharing and coordinated capital deployment. In addition, America's rare earth supply chain strategy illustrates both the ambition and the constraints facing Western nations in this space. However, even the most optimistic scenarios suggest meaningful processing diversification remains a mid-2030s outcome at the earliest.

The uncomfortable reality for policymakers is that recycling, urban mining, and demand substitution — while genuinely valuable over the long term — cannot close the near-term supply gap created by concentrated Chinese processing control. Structural vulnerability is not a risk scenario. For most G7 nations, it is the current state.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: China Rare Earth Export Controls

What rare earth elements are covered by China's 2025 export controls?

The April 2025 Wave 1 measures covered seven heavy rare earth elements including samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium, along with associated compounds and permanent magnets. The October 2025 Wave 2 expansion added five additional elements and extended restrictions to processing equipment and embedded products.

How do China's export controls differ from an outright ban?

Rather than prohibiting exports entirely, China's export controls licensing regime requires exporters to obtain government approval, submit end-user declarations, and satisfy screening criteria that are not fully transparent. This creates uncertainty and delays rather than a hard cutoff, which in many respects is more disruptive to global supply chains than a predictable ban.

Which countries are most exposed to China's rare earth restrictions?

Direct importers including the United States, Japan, South Korea, the Netherlands, and Vietnam carry the highest immediate exposure. Furthermore, China's export restrictions affect any nation whose manufacturers depend on downstream products from these processing hubs, creating secondary supply chain risk.

Can Western nations realistically replace Chinese rare earth processing capacity?

In the near term, no. The capital requirements, technical expertise gaps, permitting timelines, and operational learning curves associated with building separation infrastructure make meaningful diversification a decade-long project at minimum. Near-term resilience depends more on inventory strategy, allied-nation cooperation, and demand-side efficiency than on independent processing buildout.

How long will China's export restrictions remain in place?

The October 2025 Wave 2 measures were suspended until November 2026, creating a temporary reprieve. However, the underlying policy architecture — including the April 2025 licensing requirements and the December 2023 technology transfer bans — remains fully in effect. The suspension of Wave 2 should not be interpreted as a signal of policy reversal.

Disclaimer: This article contains forward-looking assessments and industry analysis based on publicly available trade data and regulatory announcements. It does not constitute financial or investment advice. Supply chain projections and timeline estimates involve significant uncertainty and should not be relied upon as definitive forecasts.

Want to Capitalise on the ASX Opportunities Emerging From Critical Minerals Supply Chain Disruption?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly cutting through complex geological and commodity data to surface actionable investment opportunities the moment they are announced. Explore historic discoveries and their market returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.