June 25, 2026

The Processing Chokepoint: Why China's Rare Earth Dominance Is About Chemistry, Not Geography

Most discussions about rare earth minerals begin in the wrong place. They focus on where these elements exist in the ground, which misses the point entirely. The real story of why China rare earth export controls on U.S. companies carry such strategic weight has almost nothing to do with geology and everything to do with industrial chemistry developed over decades of deliberate policy investment.

Rare earth elements are, by geological standards, not particularly scarce. Cerium, for instance, is more abundant in the Earth's crust than copper. The challenge lies not in finding these materials but in separating them from one another and processing them into forms that advanced manufacturing can actually use. This is where the global supply chain bottleneck exists, and it is precisely where China has constructed its most durable source of geopolitical leverage.

Understanding this distinction is essential to interpreting why Beijing continues to deploy China rare earth export controls on U.S. companies as a preferred instrument of trade retaliation, and why Washington's response, however well-funded, cannot resolve the underlying dependency within any politically relevant timeframe. Furthermore, the rare earth supply chain implications extend far beyond bilateral trade tensions into the architecture of global industrial competition.

When big ASX news breaks, our subscribers know first

How the Export Control Architecture Works in Practice

From Licensing to Blacklisting: A Regulatory Escalation

China's export control regime has undergone a meaningful structural evolution. Earlier iterations of the system operated on a permission-based model, where exporters sought individual licenses and trade could proceed under review. The current framework has moved toward categorical designation, where entities placed on China's export control list face what amounts to an effective ban on receiving dual-use material transfers, not a licensing hurdle that can be navigated through paperwork.

On 22 June 2026, Beijing added MP Materials and USA Rare Earth to this export control list, alongside eight additional U.S. entities with documented military-sector ties. According to reporting from Reuters, the action was framed as a proportional response to Washington's decision to add Chinese companies to the Pentagon's blacklist. In regulatory terms, the difference between a license requirement and a blacklist designation is the difference between a speed bump and a closed road.

Why These Two Companies Were Targeted

The selection of MP Materials and USA Rare Earth was not arbitrary. These firms represent the two structural pillars of America's domestic rare earth independence strategy:

-

MP Materials operates the Mountain Pass mine in California, the only rare earth mine of meaningful scale currently active in the United States. The company receives financial backing from the U.S. Department of Defense to build out domestic processing capacity and permanent magnet production, explicitly aimed at reducing reliance on Chinese-controlled supply chains.

-

USA Rare Earth is pursuing a vertically integrated model that spans mining, separation, and magnet manufacturing, targeting both industrial and defence-sector demand within the United States.

By targeting the firms most architecturally central to Washington's supply chain sovereignty agenda, Beijing's regulatory action functions as a direct challenge to U.S. industrial policy rather than simply a commercial trade measure. China's export restrictions have consequently evolved into a formalised doctrine of calibrated retaliation.

China's Structural Dominance: Where the Real Leverage Lives

The Three-Stage Supply Chain and China's Control Points

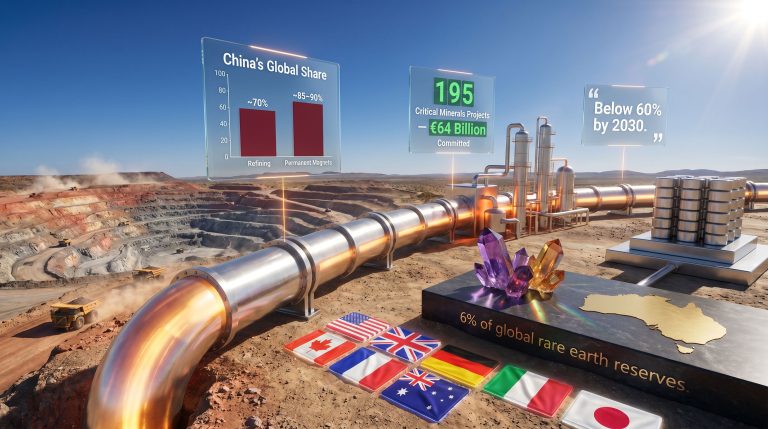

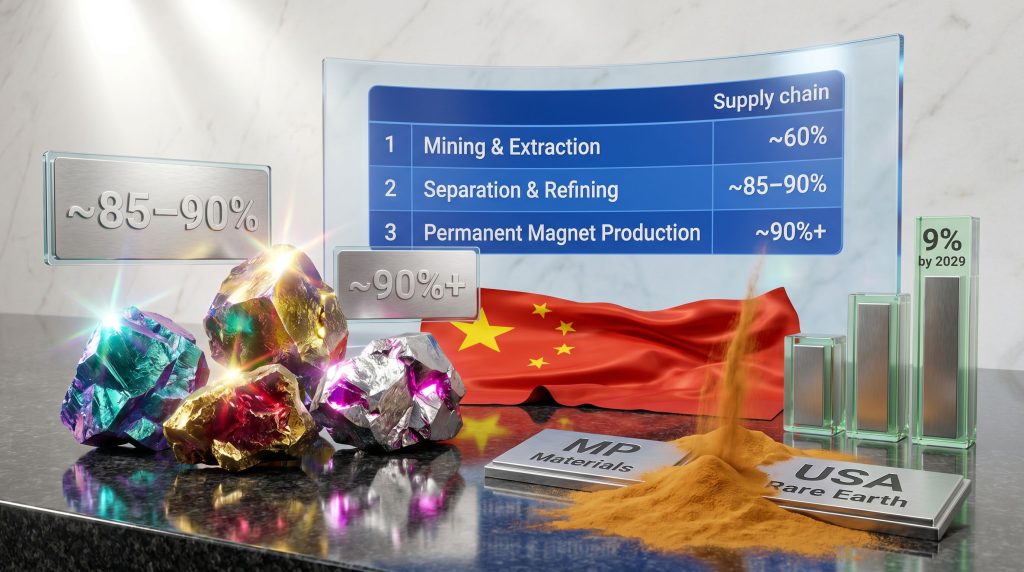

| Stage of Rare Earth Supply Chain | China's Global Share | Strategic Significance |

|---|---|---|

| Mining and Extraction | ~60% | High, but increasingly contested |

| Separation and Refining | ~85-90% | Critical chokepoint |

| Permanent Magnet Production | ~90%+ | Defence and EV dependency |

According to the International Energy Agency, China controls the overwhelming majority of the world's rare earth separation and refining capacity, as well as the dominant share of permanent magnet production. These magnets are irreplaceable components in a remarkably broad range of systems: electric vehicle drivetrains, wind turbine generators, drone propulsion, missile guidance systems, radar arrays, and fighter aircraft.

The separation and refining stage is where China's advantage is most entrenched and most difficult to replicate. The rare earth processing challenges involved in solvent extraction require highly specialised chemical engineering, significant capital investment, and generate substantial toxic waste streams. China spent decades building this industrial base under a deliberate national strategy. Replicating it elsewhere is measured in decades, not years.

Why Rare Earths Are Beijing's Preferred Trade Weapon

A useful analytical exercise is to compare rare earth export controls against the other coercive trade instruments available to Beijing:

| Commodity | China's Leverage Type | Countermeasure Availability | Diplomatic Cost to China |

|---|---|---|---|

| Soybeans | Buyer-side (import reduction) | High – Brazil and Argentina alternatives | Moderate – China also needs supply |

| Active Pharmaceutical Ingredients | Upstream chemical inputs | Moderate | High – patient welfare implications |

| Rare Earth Elements | Processor-side (export restriction) | Low – few viable alternatives | Low – limited self-harm |

The soybean comparison is instructive. When Beijing imposed additional tariffs on U.S. soybeans in 2025, it was exercising buyer-side leverage. China needs soybeans to sustain its livestock sector, which means it absorbs economic pain alongside the pressure it applies. It can redirect purchases to Brazil or Argentina, but it remains exposed to price fluctuations and logistical risks. The leverage is real but structurally limited.

Pharmaceutical inputs present a closer structural parallel to rare earths, given that Western dependence is concentrated at the upstream processing level. However, restricting chemical inputs that affect medicine manufacturing carries significant diplomatic costs. The optics of impacting patient health systems globally would make this a far more politically expensive tool for Beijing to deploy in a trade dispute.

Rare earth export restrictions, by contrast, impose asymmetric costs. The economic self-harm to China is minimal. The processing monopoly means restrictions fall almost entirely on the importing side. This asymmetry makes rare earths structurally superior as a coercive instrument, which explains why Beijing has deployed China rare earth export controls on U.S. companies in April 2025, October 2025, and again in June 2026, establishing a clear doctrine of calibrated, repeatable application.

Defence and Industrial Systems Exposed by the Controls

The Military Dependency Problem

The U.S. defence sector's exposure to rare earth supply chain disruption is not theoretical. Neodymium-iron-boron (NdFeB) permanent magnets, the most powerful permanent magnets commercially available, are embedded in critical military systems including F-35 fighter aircraft, nuclear submarine propulsion systems, radar array components, and precision missile guidance mechanisms.

This dual-use reality, where the same materials serve both civilian clean energy applications and defence procurement, creates a supply chain vulnerability that cannot be easily compartmentalised. An EV motor and a missile guidance actuator may rely on chemically identical magnet material sourced through the same upstream processing chain.

China's Tiered Review System: A Weaponised Regulatory Gradient

Beyond entity-specific blacklisting, China has implemented a tiered review framework for rare earth export applications that functions as a precision instrument rather than a blunt tool:

Regulatory Architecture: Standard civilian applications receive automatic approval. Advanced semiconductor manufacturing applications, specifically those involving sub-14nm chip production processes, face case-by-case individual review. Military artificial intelligence end-uses receive automatic rejection.

This gradient allows Beijing to calibrate pressure with surgical precision, maintaining trade flow for non-sensitive applications while creating maximum friction exactly where the United States is most technologically vulnerable. In addition, the case-by-case review mechanism for advanced chipmaking serves a secondary function: each individual approval or denial becomes a discrete diplomatic signal in ongoing trade negotiations. The broader implications for critical minerals for semiconductors underscore how intertwined these regulatory levers have become.

Assessing the Immediate Impact: Symbolic or Structural?

Why the Short-Term Operational Disruption May Be Limited

Both MP Materials and USA Rare Earth have proactively reduced their procurement dependence on Chinese-sourced equipment and raw material inputs ahead of their designation. This means the immediate operational impact of the June 2026 action is assessed as limited in the short term. The firms anticipated this regulatory risk and built some degree of supply chain resilience into their operations.

However, framing the impact as merely symbolic would be analytically incomplete for several reasons:

-

Precedent establishment – Blacklist designation signals Beijing's willingness to escalate from entity-specific controls toward potential sector-wide restrictions.

-

Financing and partnership risk – Designation affects future business development negotiations, equipment sourcing relationships, and the risk appetite of potential financing partners who must now factor Chinese regulatory exposure into their analysis.

-

Strategic ambiguity – The parallel pledge by China to review rare earth export applications on a case-by-case basis introduces ongoing uncertainty that complicates long-term supply chain investment planning for U.S. companies.

The escalation pattern across April 2025, October 2025, and June 2026 confirms a deliberate policy doctrine rather than reactive improvisation. Each application of the tool refines Beijing's understanding of the threshold at which these controls generate sufficient strategic pressure.

Washington's Response: Federal Investment and Its Limits

Domestic Capacity Building: The Mountain Pass Gap

MP Materials' Mountain Pass facility represents the ceiling of current U.S. domestic rare earth mining capacity. The critical policy insight is that raw ore extraction, even at scale, does not resolve strategic dependence. The processing and separation infrastructure required to convert rare earth ore into magnet-grade material remains the persistent gap in America's rare earth supply chain sovereignty.

Department of Defence financial backing for downstream processing and magnet manufacturing at Mountain Pass represents a recognition of this distinction, moving federal investment beyond the mining stage toward the actual chokepoint.

U.S. Investment in African Rare Earth Projects

| Financing Body | Project | Country | Commitment |

|---|---|---|---|

| U.S. DFC (via TechMet) | Phalaborwa Rare Earth Project | South Africa | $50 million |

| U.S. DFC | Songwe Hill Project | Malawi | $4.6 million |

| EXIM Bank | Longonjo Mine (Pensana) | Angola | Up to $160 million |

The U.S. International Development Finance Corporation and the Export-Import Bank of the United States have both deployed capital toward African rare earth projects as a medium-term supply chain hedge. Angola's Longonjo mine, backed by up to $160 million from EXIM, represents the nearest-term production milestone, with initial output projected from 2027.

The Timeline Problem That Policy Cannot Solve

Even under optimistic assumptions, the scale of African rare earth production remains a partial solution at best. Benchmark Mineral Intelligence projects Africa could account for as much as 9% of global rare earth supply by 2029, while Fitch Solutions estimates approximately 7% of global production by 2034. Neither projection approaches the 85-90% processing share that China currently holds.

This creates a decade-long vulnerability window that no current investment programme closes. African mining projects face compounding challenges beyond capital:

- Infrastructure gaps in power, water, and transport logistics specific to remote deposit locations

- Regulatory and permitting complexity across multiple sovereign jurisdictions

- The processing infrastructure problem extends to African projects too, as mined ore still requires separation and refining that currently has no large-scale alternative to Chinese facilities

- China's existing investment presence across African mining sectors introduces geopolitical competition for the same assets Washington is attempting to secure

Emerging alternative processing hubs in Australia, Canada, and Estonia offer partial solutions, and allied industrial policy coordination among the United States, European Union, Japan, and Australia is gradually building toward a distributed processing ecosystem. However, the realistic timeline for this ecosystem to meaningfully offset Chinese processing dominance remains measured in decades.

The next major ASX story will hit our subscribers first

The Strategic Logic Behind Beijing's Repeated Use of This Tool

The most analytically important observation about China rare earth export controls on U.S. companies is not the individual regulatory actions themselves but the consistency of their application. Three deployments within fourteen months, each triggered by U.S. additions to the Pentagon blacklist, establish rare earth export controls as a formalised instrument in Beijing's retaliatory trade doctrine.

As Al Jazeera has reported, the tool possesses characteristics that make it strategically superior to alternatives:

- Low self-harm cost – China's processing monopoly means restrictions impose costs almost entirely on the recipient side

- Calibrated escalation path – Movement from entity-specific controls to sector-wide restrictions provides a credible escalation ladder

- Diplomatic optionality – Case-by-case review preserves the ability to signal cooperation without altering the underlying regulatory architecture

- High target sensitivity – U.S. defence and clean energy industries cannot rapidly substitute Chinese-processed rare earths

Disclaimer: This article contains forward-looking projections from third-party research organisations including Benchmark Mineral Intelligence and Fitch Solutions. These projections represent analytical estimates subject to change based on market conditions, investment flows, and geopolitical developments. Nothing in this article constitutes financial or investment advice.

For ongoing coverage of African critical minerals investment and global rare earth supply chain developments, Ecofin Agency provides sector-focused analysis at ecofinagency.com.

Want to Stay Ahead of Critical Mineral Discoveries Before the Broader Market Reacts?

As rare earth supply chain tensions reshape global industrial strategy, Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, translating complex geological and commodity data into clear, actionable investment insights. Explore why transformative mineral discoveries have historically generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.