June 24, 2026

The Invisible Chokepoint: Why Rare Earth Processing Dominance Matters More Than Mining

Most industrial commodity discussions centre on who holds the largest reserves in the ground. With rare earth elements, this framing fundamentally misses the point. The critical leverage in the rare earth supply chain does not sit at the mine face — it sits inside the separation plant, the refinery, and the magnet alloy facility. Understanding this distinction is essential to grasping why G7 rare earth targets and non-Chinese supply chains have become one of the defining geopolitical and industrial policy conversations of the mid-2020s.

Rare earth elements are a group of 17 metallic elements, including neodymium, praseodymium, dysprosium, and terbium, that are indispensable to permanent magnet production. These magnets sit at the heart of electric vehicle drive motors, offshore wind turbine generators, precision-guided defence systems, and the miniaturised components inside consumer electronics. The functional properties of neodymium-iron-boron (NdFeB) magnets — high magnetic strength at relatively low weight — are currently irreplaceable at commercial scale.

The problem is not that rare earths are geologically scarce. They are more abundant in the Earth's crust than gold or platinum. The problem is that converting raw ore into separated oxides, and then into finished magnets, requires highly specialised hydrometallurgical processing infrastructure that has been concentrated in a single country for decades. The rare earth supply chains underpinning these industries are consequently among the most geopolitically exposed in the global economy.

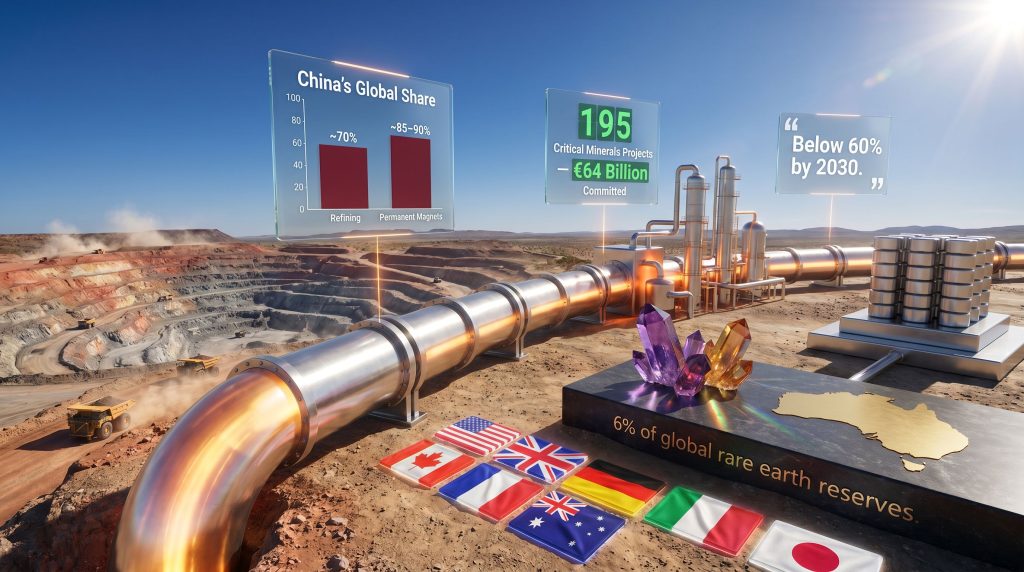

| Supply Chain Stage | China's Estimated Global Share (2025) |

|---|---|

| Rare earth mining | ~60–65% |

| Rare earth refining and processing | ~70% |

| Permanent magnet production | ~85–90% |

| Heavy REE processing (dysprosium, terbium) | Near monopoly |

Key Insight: A non-Chinese mine that ships ore or mixed concentrate to a Chinese separation facility has not achieved supply chain independence. It has simply moved the dependency one step upstream. The G7's formal acknowledgement of this structural reality is itself a significant policy development.

When big ASX news breaks, our subscribers know first

What the Evian Declaration Actually Commits To

The G7 summit held in Evian, France produced a declaration with measurable, time-bound targets that distinguishes it from earlier rounds of critical minerals rhetoric. Member nations committed to reducing dependence on any single supplier of rare earths and permanent magnets to below 60% of total import volume by 2030, with a stated ambition to push that figure below 50% as soon as practically achievable beyond that date.

These targets apply to both volumetric share and processing dependency — meaning that sourcing ore from a non-Chinese mine while continuing to rely on Chinese refining infrastructure would not satisfy the framework's intent. Furthermore, China's export restrictions on key materials have added considerable urgency to this policy shift, accelerating timelines that G7 governments had previously treated as longer-term ambitions.

The €64 Billion Commitment: What It Includes and What It Doesn't

Since the start of 2026, 195 critical minerals projects across G7 and partner nations have attracted €64 billion in committed capital. This figure spans equity investments, offtake agreements with manufacturers and defence contractors, and financing instruments from development institutions. According to G7 critical minerals alliance reporting, this represents the most coordinated Western response to supply chain vulnerability in modern industrial history.

An important distinction for investors and analysts: committed capital is not the same as deployed capital. Many of these commitments represent conditional financing tied to project milestones, environmental approvals, or offtake execution. The gap between announced commitments and actual construction activity is where the practical test of this framework will play out.

From Aspiration to Architecture: The Critical Minerals Resilience and Production Alliance

Previous G7 statements on critical minerals diversification were largely aspirational. The Evian declaration introduces something structurally different: a Critical Minerals Resilience and Production Alliance designed to coordinate policy, financing, stockpiling, and market transparency across member and partner nations.

This shift from bilateral deal-making toward institutional coordination echoes historical precedents in industrial security policy, including post-World War II strategic materials stockpiling programmes and the coordinated semiconductor export control architectures developed over the past decade. The analogy is instructive: those frameworks also began with political declarations before translating into enforceable industrial structures over years.

The Mine-to-Magnet Timeline: Why 2030 Is a Tight Window

One of the most underdiscussed dimensions of the G7's diversification agenda is the physical timeline for building supply chain infrastructure. Rare earth project development follows a long sequence of capital-intensive, permitting-dependent stages:

- Geological exploration and resource definition — typically 3 to 7 years

- Feasibility studies and environmental permitting — 2 to 5 years

- Mine construction and commissioning — 2 to 4 years

- Separation and processing facility development — 3 to 6 years

- Magnet alloy production and downstream integration — 1 to 3 years

From greenfield discovery to operational magnet production, the full timeline in most Western jurisdictions runs to 10 to 20 years or more. This means that projects already in advanced development stages — with completed feasibility studies, environmental approvals in progress, or secured offtake — are the only realistic candidates for contributing to 2030 outcomes.

Projects still in exploration or pre-feasibility phases should not be evaluated as 2030 contributors regardless of the quality of their resource endowment. The rare earth processing challenges involved in these later development stages are frequently underestimated by those focused primarily on mining activity.

The Cost Structure Problem: Understanding the Ex-China Premium

Building rare earth processing capacity outside China is not simply a matter of replicating existing technology in a new location. Non-Chinese operations face a series of structural cost disadvantages that create what market participants are beginning to call the ex-China premium — the price differential required to make Western production commercially viable.

These cost pressures include:

- Stricter environmental compliance standards and associated capital costs

- Longer and more expensive permitting cycles, particularly for processing facilities involving radioactive thorium and uranium byproducts

- Higher labour and energy costs relative to Chinese production baselines

- Greater capital intensity per tonne of separated oxide output

- Limited availability of domestic technical expertise in hydrometallurgical separation

The radioactive byproduct issue deserves particular attention. Rare earth ores commonly contain thorium and, to a lesser extent, uranium as co-occurring elements. Managing these materials under Western regulatory frameworks adds significant cost and complexity to processing operations — a factor that Chinese facilities operating under different regulatory conditions do not face to the same degree. This is one of the least-discussed technical barriers to building ex-China processing capacity at scale.

Heavy Rare Earths: The Hardest Problem Nobody Is Solving Fast Enough

Within the broader rare earth landscape, a critical distinction separates light rare earths (primarily neodymium and praseodymium, used in bulk magnet production) from heavy rare earths (principally dysprosium and terbium, used as performance-enhancing additives that allow magnets to operate at elevated temperatures without demagnetising).

Lynas Rare Earths, the world's largest rare earth producer outside China, has established meaningful production capacity for neodymium and praseodymium. However, there is currently no large-scale heavy rare earth separation and processing facility operating outside China. Dysprosium and terbium are sourced almost exclusively from ionic clay deposits concentrated in southern China, with very limited equivalent geology identified and developed elsewhere.

The significance of this gap is difficult to overstate. An EV motor manufacturer or defence contractor seeking full supply chain independence cannot achieve it through light rare earth diversification alone. Until non-Chinese heavy rare earth separation capacity exists, the G7's diversification agenda will remain structurally incomplete regardless of progress on neodymium and praseodymium.

Who Is Actually Positioned to Deliver?

Australia's Strategic Role

Australia holds approximately 6% of global rare earth reserves and accounts for roughly 4% of current global mining production — a gap that reflects underinvestment in processing infrastructure relative to the country's resource endowment. Lynas Rare Earths operates as the most advanced non-Chinese producer globally, with separation infrastructure in Malaysia producing neodymium-praseodymium oxide for global magnet manufacturers.

Australia formally endorsed the G7 Evian declaration as a partner country. The view from Australian industry participants reflects a clear-eyed assessment of what is required: the chairman of Australian Rare Earths, Angus Barker, has indicated publicly that G7 manufacturers will need a substantial number of non-Chinese projects to achieve production before 2030 to fulfil the declared targets, and that demand for pre-2030 supply agreements from both manufacturers and defence customers is intensifying.

The United States: Vertical Integration as National Strategy

The United States has chosen a more assertive domestic approach. MP Materials operates the Mountain Pass facility in California — the only commercial-scale rare earth mine currently active in the U.S. — and is developing downstream processing capability in Texas, supported by $150 million in separation infrastructure investment.

USA Rare Earth is pursuing a fully vertically integrated model from mine to finished magnet, backed by $277 million in federal incentive support. America's rare earth supply chain reflects a clear preference for domestic self-sufficiency over allied-nation processing — a strategic posture with different financing and timeline implications compared to the distributed model favoured by the broader G7 alliance.

Broader Supply Landscape

| Country/Region | Current Role | Key Development Focus |

|---|---|---|

| Canada | Partner country in G7 alliance | Exploration and early-stage processing |

| Greenland and Scandinavia | Exploration-stage assets | Permitting and project financing |

| Africa (select jurisdictions) | Resource-rich, infrastructure-limited | Development finance and offtake-backed models |

| India | Domestic reserves, limited processing | Processing capacity investment |

The Financial Architecture: How the G7 Plans to Fund the Gap

The economics of rare earth project development outside China require more than political will. They require financial engineering that can bridge the gap between current project economics and the cost structure needed to attract private capital. In addition, the broader critical minerals demand surge across clean energy and defence sectors is compressing the window for orderly project development.

The G7 framework calls for coordinated deployment of capital across multiple tiers:

- Multilateral development bank lending and project guarantees

- Development finance institution equity participation in strategic projects

- Export credit agency support for project financing and offtake arrangements

- Private capital mobilised through structured de-risking instruments

The underlying logic is that public finance absorbs early-stage geological, permitting, and construction risk, making the residual investment profile attractive to institutional private capital. This crowding-in model has been used successfully in renewable energy infrastructure and is now being applied to critical minerals.

Revenue Stabilisation: What Tools Are Being Examined?

Rare earth price volatility has historically undermined project financing. Chinese producers have demonstrated the ability to suppress prices through coordinated oversupply, making it difficult for higher-cost non-Chinese projects to maintain bankable economics. Consequently, the G7 is examining several demand-side mechanisms to address this structural vulnerability, as detailed analysis of G7 supply chain diversification highlights the central unresolved question of who ultimately bears the cost.

| Mechanism | Purpose | Status |

|---|---|---|

| Price-gap subsidies | Bridge the cost differential between Chinese and non-Chinese production | Under examination |

| Price floors | Provide revenue floor certainty for project developers | Under examination |

| Joint procurement instruments | Aggregate demand to support offtake economics | Under examination |

| Import quotas | Limit single-source supplier dependency | Under examination |

| Strategic stockpiling | Buffer supply disruptions during transition | Pilot phase (lithium, nickel) |

The IEA's mandate is also proposed to expand into systematic critical mineral market monitoring, beginning with nickel and lithium before extending to rare earths. This would create an early warning function for supply distortions — an institutional layer that does not currently exist for rare earth markets.

How China Is Likely to Respond

China's Foreign Ministry formally characterised the G7's coordinated diversification effort as the conduct of exclusionary blocs rather than legitimate security policy, framing its own market dominance as a natural outcome of comparative advantage and industrial development rather than deliberate strategic concentration.

The more analytically useful question is not what China says, but what tools it has available to respond. Three scenarios are worth considering:

- Scenario A — Price suppression: Coordinated oversupply to undercut the economics of non-Chinese projects, exploiting the cost differential before Western revenue stabilisation mechanisms become operational

- Scenario B — Export restriction escalation: Tightening controls on heavy rare earth exports to maximise geopolitical leverage before alternative separation capacity comes online outside China

- Scenario C — Alliance fragmentation: Bilateral engagement with individual G7 members to weaken coordinated procurement commitments through preferential supply arrangements

The asymmetry in each scenario is notable: China can execute these responses faster than Western supply chain infrastructure can be built. The 2030 window is tight precisely because of this temporal mismatch.

The next major ASX story will hit our subscribers first

What This Means for Project Developers and Investors

Offtake Agreements as the New Project Finance Currency

In the current environment, secured offtake agreements from G7-aligned manufacturers and defence contractors have become the primary de-risking instrument for rare earth project financing. A project with committed offtake from a credible buyer occupies a fundamentally different financing position than an equivalent project without one — regardless of resource quality.

This dynamic is reshaping how developers approach project advancement. Demonstrating demand security has become as important as demonstrating geological quality.

Key Investment Themes Emerging From the G7 Framework

- Processing assets over mining assets: Investment appetite is shifting downstream toward separation and processing facilities, where the value chain bottleneck actually sits

- Heavy REE exposure commands a premium: Projects with meaningful dysprosium and terbium content are attracting disproportionate strategic interest given the near-total absence of non-Chinese processing capacity

- Jurisdiction matters as much as geology: Assets in politically stable, G7-aligned jurisdictions command financing advantages over equivalent deposits in higher-risk geographies, regardless of ore grade

- Vertical integration preferred by institutional financiers: The mine-to-magnet model is increasingly favoured by development finance institutions seeking to avoid partial supply chain dependency

Risks That Could Derail the 2030 Timeline

- Permitting backlogs in the U.S., Canada, and Australia, particularly for facilities handling radioactive processing byproducts

- The gap between publicly announced financing commitments and actual capital deployment

- Technical scaling challenges for heavy rare earth separation outside established Chinese processing clusters

- Price volatility undermining project economics before revenue stabilisation mechanisms are implemented

- Geopolitical divergence within the G7 alliance weakening procurement coordination

This article contains forward-looking analysis based on publicly available policy documents, industry commentary, and market data. It does not constitute financial advice. Investors should conduct their own due diligence before making investment decisions related to rare earth or critical minerals projects.

Frequently Asked Questions: G7 Rare Earth Targets and Non-Chinese Supply Chains

What are the specific G7 rare earth concentration targets?

The G7 has committed to reducing dependence on any single supplier of rare earths and permanent magnets to below 60% of total import volume by 2030, with a further ambition to reduce this to below 50% on an accelerated timeline beyond 2030.

Why does China's processing dominance matter more than its mining share?

Even nations that mine rare earths outside China often ship ore or partially processed material to Chinese separation facilities, meaning the end product still passes through Chinese-controlled infrastructure. True supply chain independence requires sovereign processing and separation capacity, not just mining activity.

What is the difference between light and heavy rare earths?

Light rare earths, principally neodymium and praseodymium, are used in bulk magnet production and have more diverse global supply sources. Heavy rare earths, primarily dysprosium and terbium, are critical performance additives for high-temperature magnet applications and are currently processed almost exclusively in China, representing the most difficult element of the diversification challenge.

Which country is best positioned to contribute to G7 rare earth supply targets?

Australia is widely regarded as one of the most credible near-term contributors, hosting Lynas Rare Earths — the world's largest non-Chinese producer — alongside a pipeline of emerging developers. The United States is pursuing a more self-contained vertical integration strategy through MP Materials and USA Rare Earth.

What financial tools is the G7 deploying to support non-Chinese rare earth projects?

The framework includes coordinated deployment of development finance institutions, multilateral development banks, and export credit agencies, alongside demand-side tools including price floors, price-gap subsidies, joint procurement instruments, and strategic stockpiling programmes.

What is the biggest single barrier to meeting the 2030 targets?

The absence of large-scale heavy rare earth separation and processing capacity outside China represents the most technically challenging and commercially complex barrier. Without this infrastructure, the G7's diversification targets cannot be fully achieved regardless of progress on light rare earth production.

A Structural Shift Measured in Years, Not Declarations

The G7's Evian declaration represents a genuine escalation in the seriousness with which the world's largest economies are approaching rare earth supply chain risk. The shift from aspirational language to numerical targets, institutional coordination mechanisms, and explicit financial architectures marks a meaningful change in policy posture.

However, declarations do not separate oxides, construct processing plants, or commission magnet alloy facilities. The physical infrastructure of alternative supply chains is built over years of capital deployment, permitting cycles, and technical development. The projects, financing instruments, and institutional frameworks being assembled over the next 24 to 36 months will determine whether the 60% concentration target becomes a verifiable industrial milestone or an enduring aspiration.

For investors, developers, and downstream manufacturers tracking G7 rare earth targets and non-Chinese supply chains, the critical variable is not political commitment — that now appears durable. The critical variable is execution velocity against a timeline that was already tight before the first shovel broke ground.

Want to Identify the Next Major ASX Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including critical and rare earth minerals attracting intense G7 strategic interest — instantly translating complex geological and commodity data into actionable investment insights. Explore historic discoveries and their returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.