June 30, 2026

The Hidden Architecture of a Supply Chain Crisis

Few vulnerabilities in modern industrial economies are as deeply embedded, yet as poorly understood, as the structural dependency on rare earth processing. Unlike oil, where supply disruption is immediately visible at the pump, rare earth shortages operate silently inside the supply chains of jet engines, missile guidance systems, electric vehicle motors, and wind turbines. By the time the shortage reaches public consciousness, the damage is already compounding through manufacturing pipelines that can take years to reconfigure.

China rare earth export controls and US concerns are not a sudden trade spat. They are the visible symptom of a dependency that was decades in the making, and one that diplomacy alone is proving insufficient to resolve. Understanding why requires looking beyond the headlines and into the industrial architecture that makes these minerals so consequential.

When big ASX news breaks, our subscribers know first

Why Rare Earths Are Not Rare, But Their Processing Is

The name is misleading. Rare earth elements are geologically abundant across many regions of the world, including the United States, Australia, Canada, Brazil, and parts of Africa. The scarcity that matters is not geological but industrial.

What China built over roughly three decades was not simply mining dominance. It constructed an end-to-end processing ecosystem that no other nation has replicated at scale. Today, China accounts for approximately 60% of global rare earth mining output and, more critically, controls an estimated 90% of global refining and separation capacity. That second figure is the strategic chokepoint that makes alternative sourcing so difficult in practice.

The rare earth processing challenges involved are not limited to a single step. Processing involves a multi-stage industrial chain:

- Mining and crushing of ore

- Physical and chemical separation of individual elements

- Refining into oxide or metal form

- Alloying into specialist materials

- Manufacturing into permanent magnets or other end-use components

Each stage requires specialised chemical knowledge, significant capital investment, and years of operational expertise. Most Western nations currently lack capacity at stages two through five, meaning that even if ore is mined domestically, it typically must still be shipped to China for processing.

Light vs Heavy Rare Earths: Why Does the Distinction Matter?

Not all rare earth elements carry equal strategic weight. Light rare earths, such as cerium and lanthanum, are more abundant and more widely produced. Heavy rare earths, including yttrium, dysprosium, terbium, and scandium, are produced in far smaller volumes and are overwhelmingly concentrated in Chinese supply chains.

Heavy rare earths are disproportionately critical for high-performance applications. Dysprosium and terbium are essential for maintaining magnet performance at high temperatures, a requirement in electric vehicle motors and aerospace systems. Yttrium is irreplaceable as a thermal barrier coating material for turbine blades. These are not elements where substitution is straightforward. In most defence and industrial applications, technical alternatives either do not exist or impose severe performance penalties.

China's Export Control Architecture: A Three-Phase Framework

China's rare earth export restrictions were introduced in phases beginning in April 2025, widely interpreted as a response to escalating US tariff pressure during the broader trade confrontation.

| Control Phase | Date | Scope | Status (as of May 2026) |

|---|---|---|---|

| Phase One | April 2025 | 7 heavy rare earths, compounds, metals, magnets | Active |

| Phase Two | October 2025 | 5 additional REEs, equipment, technology transfers | Suspended until Nov 2026 |

| Phase Two Suspension | November 2025 | Temporary pause on Phase Two expansion | In effect |

Phase One introduced export licensing requirements for seven heavy rare earth elements, including yttrium and scandium. This was not a blanket prohibition. Licensed civilian applications could still be approved. However, the licensing process introduced uncertainty, delays, and selective allocation that effectively constrained supply to US manufacturers.

Phase Two, introduced in October 2025, extended controls to five additional rare earth elements and expanded scope to include related processing equipment, technical knowledge transfers, and potentially foreign-manufactured products incorporating Chinese-sourced rare earth inputs. This final dimension is particularly significant because it raised the prospect of third-country manufacturers being subject to Chinese regulatory approval, extending Beijing's reach well beyond bilateral US-China trade.

The temporary suspension of Phase Two in November 2025 attracted considerable analytical attention. Rather than representing a diplomatic concession, most observers interpreted it as a strategic reserve — a tool Beijing chose to hold in abeyance rather than permanently relinquish. As analysts at CSIS have noted, these restrictions pose a direct threat to US defence supply chains.

"The selective suspension of Phase Two controls functions less as a rollback and more as a calibrated signal of Beijing's willingness to escalate further if negotiations deteriorate. The controls remain available as leverage, not abandoned as a concession."

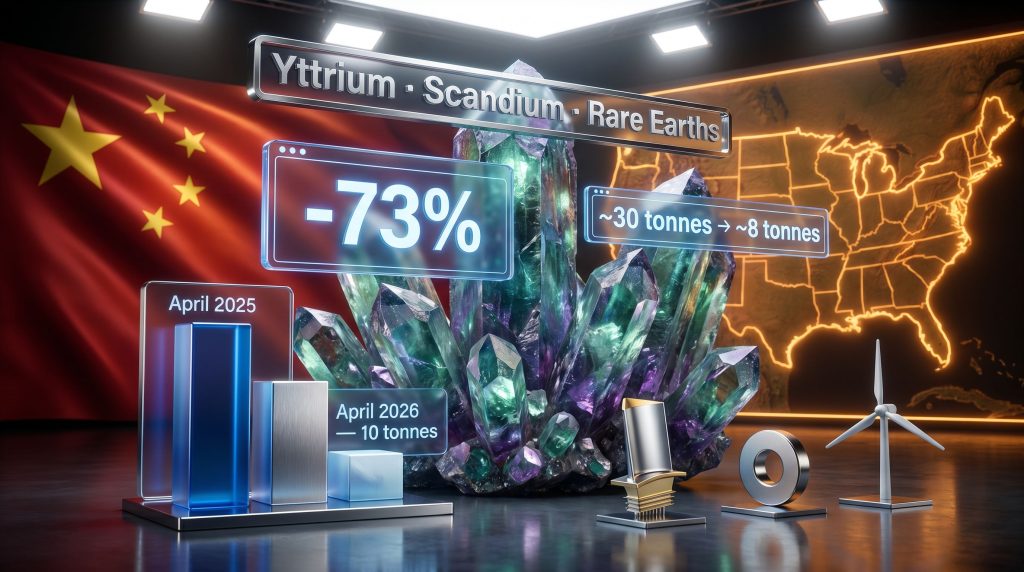

The Yttrium Shortage: Quantifying the Supply Collapse

Of all the elements affected, yttrium has emerged as the most acute case study in supply disruption. Its industrial role is specific and difficult to replicate: yttrium oxide coatings protect turbine blades in aircraft engines and power generation facilities from extreme thermal stress, enabling components to operate at temperatures that would otherwise cause rapid material failure.

The supply data tells a stark story:

| Metric | Pre-Controls (13-Month Average) | Post-Controls Average | Change |

|---|---|---|---|

| Monthly yttrium oxide exports to US | ~30 tonnes | ~8 tonnes | -73% |

| April 2026 shipment volume | N/A | 10 tonnes | vs. 60 tonnes in March 2026 |

The month-on-month collapse between March and April 2026 — from 60 tonnes to just 10 tonnes — represents an 83% reduction in a single month. This is not a gradual adjustment. It reflects the granular power that China's licensing framework gives Beijing over which buyers receive supply and when.

For US aerospace and defence contractors, these are not abstract trade statistics. Turbine blade coatings are maintenance-critical components. Furthermore, shortfalls in yttrium supply translate directly into delayed maintenance schedules, extended aircraft downtime, and constrained production capacity for new engine programmes.

Decoding the Diplomatic Standoff

The bilateral leaders' summit held in Beijing in May 2026 produced two statements that, read together, illuminate the current state of the relationship with considerable precision.

The White House indicated that China had agreed to address concerns around shortages of critical minerals including yttrium and scandium. China's Ministry of Commerce characterised the outcome differently, stating that both sides had discussed the matter and would "study and resolve" what it termed each other's "reasonable and lawful concerns." The divergence in framing is not incidental.

Washington's language emphasised Chinese commitments. Beijing's language emphasised process, reciprocity, and the legitimacy of its own regulatory framework. Notably, China's statement explicitly described its export control regime as lawful and characterised applications for compliant civilian licences as the appropriate mechanism for obtaining supply.

This represents a material shift from the diplomatic posture that followed the earlier Busan summit, after which the White House suggested China's restrictions would be dismantled. The current framing carries no such expectation. Consequently, the United States appears to have moved toward a posture of tacit acceptance that these controls are a structural feature of the trade relationship rather than a temporary negotiating instrument.

"The evolution from expecting controls to be dismantled (post-Busan) to expecting reasonable concerns to be studied (post-Beijing) signals a significant recalibration of US leverage assumptions and implicitly validates China's export control architecture as a legitimate regulatory framework."

What Does China's Licensing Framework Actually Do?

A critical but under-appreciated feature of China's approach is that the licensing system provides Beijing with extraordinarily fine-grained control over rare earth allocation. Rather than imposing a uniform embargo, the framework allows China to:

- Approve or deny applications on a case-by-case basis

- Distinguish between end-users and end-use applications

- Prioritise allied or neutral trading partners over adversaries

- Use approval rates as a real-time diplomatic signal

- Maintain plausible regulatory legitimacy under international trade law

This architecture is more sophisticated than a blanket ban and, arguably, more effective as a long-term strategic instrument. It creates persistent uncertainty rather than a clear embargo that might galvanise a faster Western industrial response.

The Refinery Gap: Why Mining More Ore Does Not Solve the Problem

A common misconception in policy discussions is that expanding rare earth mining outside China can resolve the supply dependency. This fundamentally misunderstands where the bottleneck lies. The broader rare earth supply chain encompasses far more than simply extracting ore from the ground.

Australia's Lynas Rare Earths represents the most notable exception to Chinese processing dominance among Western-aligned producers. However, even Lynas concentrates its downstream processing in Malaysia, and its output, while significant, represents a fraction of what US industrial demand requires.

Building credible ex-China processing capacity involves:

- Acquiring appropriate ore deposits with sufficient grade and volume

- Constructing separation and refining facilities with significant capital investment

- Developing chemistry expertise and operational knowledge that takes years to accumulate

- Building downstream alloying and magnet manufacturing capacity

- Establishing reliable supply relationships with industrial end-users

Independent analysts and policy experts broadly agree that developing meaningful alternative processing capacity will require five to ten years under optimistic scenarios and substantially longer if permitting, financing, or technical challenges cause delays.

The magnet manufacturing bottleneck deserves particular emphasis. Rare earth permanent magnets — primarily neodymium-iron-boron and samarium-cobalt types — are the critical end-product that most defence and clean energy applications require. Even if the US were to secure ore and build refining capacity, converting refined materials into finished high-performance magnets requires an industrial base that currently does not exist at meaningful scale outside Asia.

The next major ASX story will hit our subscribers first

Strategic Scenarios: Three Pathways Forward

Scenario A: Managed Coexistence (Base Case)

Controls remain in place but licensing approvals provide reduced, relatively stable supply volumes. US manufacturers adapt through inventory management, partial substitution, and continued diplomatic engagement. Disruption is chronic and costly but not catastrophic for most sectors.

Scenario B: Escalation (Downside Risk)

Phase Two controls are reinstated after the November 2026 suspension expires, potentially combined with additional restrictions. Critical defence and energy supply chains face acute shortages requiring emergency government intervention.

Scenario C: Structural Diversification (Upside Scenario)

Accelerated capital deployment into ex-China processing capacity, coordinated through frameworks like the Minerals Security Partnership, delivers credible supply alternatives by 2028 to 2030. China's leverage diminishes over a ten-year horizon as Western industrial capacity grows.

| Sector | Exposure Level | Primary Risk | Mitigation Pathway |

|---|---|---|---|

| Aerospace and Defence | Critical | Turbine coatings, guidance systems | Domestic processing, allied sourcing |

| Electric Vehicles | High | Permanent magnet motors | Magnet-free motor R&D, supply diversification |

| Wind Energy | High | Generator magnets | Alternative technologies, allied supply |

| Semiconductors | Moderate-High | REE-dependent processes | Inventory buffers, supply mapping |

| Power Generation | Moderate | Turbine maintenance components | Strategic stockpiling |

In addition, the role of critical minerals for semiconductors has intensified scrutiny across allied governments seeking to reduce exposure to Chinese supply chain leverage.

Frequently Asked Questions

What Rare Earths Are Currently Under Chinese Export Controls?

Seven heavy rare earth elements, including yttrium and scandium, along with associated compounds, metals, and permanent magnets, have been subject to export licensing requirements since April 2025. A second wave targeting five additional elements and related technologies, introduced in October 2025, remains temporarily suspended until November 2026.

Are the Controls a Complete Ban on Exports?

No. China has consistently characterised the measures as a licensing regime rather than a prohibition. Civilian applications meeting regulatory standards can be approved. However, the licensing process introduces delays, uncertainty, and selective allocation that functionally restricts supply, as the yttrium volume data clearly demonstrates.

Why Can't the US Simply Buy Rare Earths From Other Countries?

The core challenge is not ore availability but processing capacity. Approximately 90% of global rare earth refining and separation infrastructure is located in China. Even ore mined elsewhere must typically be processed through Chinese facilities to produce usable industrial materials. Efforts to rebuild America's rare earth supply chain are ongoing but face significant structural and timeline constraints.

What Should Investors and Industry Strategists Watch Over the Next 12 to 18 Months?

Key indicators include whether Phase Two controls are reinstated after November 2026, the pace of US domestic processing facility development, licensing approval rates as a signal of Beijing's diplomatic intent, rare earth price movements as a leading indicator of supply tightness, and the evolution of allied coordination through the Minerals Security Partnership and similar frameworks. Chatham House's recent analysis outlines how these restrictions send a stark warning to the West regarding long-term strategic dependencies.

The Structural Conclusion

China rare earth export controls and US concerns they generate are not a temporary disruption. The yttrium supply data, the shift in diplomatic language between the Busan and Beijing summits, and the multi-year timeline required to build alternative processing capacity all point toward the same conclusion: this is a structural feature of the global industrial landscape for at least the remainder of this decade.

For policymakers, the implication is that industrial policy investment in domestic and allied processing capacity must accelerate dramatically and consistently, regardless of short-term diplomatic fluctuations. For manufacturers, the priority is supply chain mapping, strategic stockpiling, and investment in alternative technologies where technically feasible. For investors, the rare earth processing sector outside China represents a multi-year thematic opportunity, though one requiring patient capital and tolerance for the execution risks inherent in building complex industrial infrastructure from limited existing foundations.

Diplomacy can manage the symptoms. Only structural industrial investment can address the underlying vulnerability.

Want to Identify ASX Opportunities in the Critical Minerals Sector Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including rare earths and other strategic commodities — instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore why major mineral discoveries have historically generated substantial returns and begin your 14-day free trial today to position yourself ahead of the market.