July 16, 2026

The $6.5 Trillion Hostage Situation Hidden Inside the Global Supply Chain

Consider a scenario where a single country controls the refining of a material so essential that its absence halts production across defence contractors, electric vehicle manufacturers, wind turbine builders, and semiconductor fabs simultaneously. This is not a thought experiment. It is the operational reality that the International Energy Agency has now quantified with striking precision: China rare earth export curbs, if fully implemented, place an estimated $6.5 trillion in annual downstream industrial output outside China at measurable risk.

That figure demands scrutiny. It is not a projection of what rare earths themselves are worth. The global rare earth market is, by comparison, tiny. What the IEA is calculating is the value of everything that cannot be made without them. Rare earth elements function less like commodities and more like biological catalysts: present in trace quantities, irreplaceable in function, and capable of shutting down entire production lines when they disappear.

When big ASX news breaks, our subscribers know first

Understanding the Architecture of China's Export Control System

China's approach to rare earth export controls is not a single policy. It is a layered, adaptive architecture designed to provide both broad leverage and granular targeting capability. Understanding the distinct mechanisms within this system is essential for manufacturers, investors, and policymakers trying to assess their actual exposure. The China rare earth export restrictions have evolved considerably since their initial introduction, adding complexity at each stage.

The April 2025 Licensing Regime: Still Fully Active

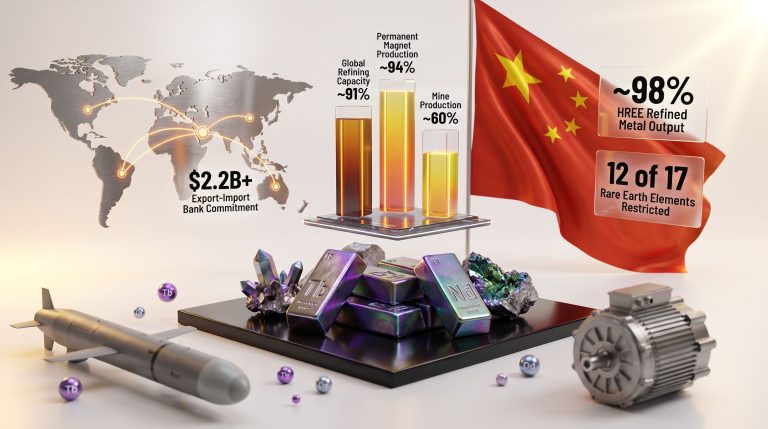

The foundation of China's current export control posture was established in April 2025, when Beijing placed seven heavy rare earth elements under mandatory export licensing. The affected materials include dysprosium, terbium, and lutetium, along with permanent magnet materials that incorporate them. These are not obscure byproducts. Dysprosium and terbium are the elements that allow neodymium-iron-boron magnets to retain their magnetic properties at elevated operating temperatures, which is precisely why they are indispensable in EV motors, wind turbine generators, and military guidance systems.

The licensing requirement operates on a case-by-case approval basis. Western defence manufacturers have found themselves effectively excluded from the approval pathway, creating what amounts to a functional embargo on heavy rare earth supply to that sector even without a formal prohibition.

The October 2025 Expansion: Suspended, Not Withdrawn

A second wave of controls proposed in October 2025 would have extended restrictions to foreign exporters dealing in products containing 0.1% or more of Chinese-origin rare earths. The compliance implications of this threshold are enormous: at that concentration level, the controls would sweep up electronics, precision instruments, and industrial equipment produced across dozens of countries using components that had passed through Chinese refining at any point in their supply chain.

China's Ministry of Commerce announced on November 7, 2025 that implementation of these rules would be paused. The suspension window runs until November 10, 2026. This pause was widely interpreted as a tactical concession within the context of US-China trade negotiations, not a strategic reversal. The core licensing system from April 2025 was explicitly excluded from the suspension and remains fully operational.

June 2026 Entity-Level Restrictions: Targeting by Name

A third layer of enforcement emerged in June 2026, when China added specific US rare earth firms to its export control entity list. This mechanism is qualitatively different from licensing-based controls. Entity list designations create comprehensive dual-use export bans against named organisations, bypassing the case-by-case licensing process entirely. The practical effect is a severance of supply relationships with identified companies, sending a pointed signal about the granularity of enforcement capability Beijing retains.

| Control Layer | Current Status | Primary Targets | Effective Date |

|---|---|---|---|

| April 2025 Heavy REE Licensing | Active | Dysprosium, Terbium, Lutetium, Permanent Magnets | April 4, 2025 |

| October 2025 Expansion (0.1% threshold) | Suspended to Nov 10, 2026 | Foreign exporters of REE-containing goods | Paused Nov 7, 2025 |

| June 2026 Entity List Additions | Active | Named US rare earth firms | June 22, 2026 |

Why Concentration Risk Has Worsened, Not Improved

The IEA's findings on supply chain concentration challenge a narrative that has been gaining traction in policy circles: that diversification efforts are succeeding. The more nuanced picture is that progress at the mining stage has not translated into meaningful change at the refining stage, which is where the real chokepoint lies.

China's share of global rare earth refining has declined modestly, from approximately 90% to 85%, due in part to investments by the United States and Malaysia in domestic and regional processing capacity. The IEA projects this could fall further to 70% by 2035, but critically, only if planned projects come online on schedule. Permitting timelines, capital availability, and the difficulty of transferring specialised processing technology are all variables that have historically caused significant delays in this sector.

The Refining-Mining Gap: A Distinction Most Analysis Misses

One of the most important and underappreciated dynamics in rare earth supply chains is the structural difference between mining diversification and refining diversification. Mining a rare earth ore body is technically complex, but the knowledge and capital requirements are broadly distributed globally. Refining and separating individual rare earth elements to the purity grades required by high-technology manufacturers is a different challenge entirely.

The separation process involves solvent extraction techniques refined over decades, proprietary chemical processing sequences, and significant environmental management requirements. China's dominance in refining is not primarily a consequence of geology. It reflects decades of accumulated technical expertise, infrastructure investment, and regulatory frameworks calibrated to enable high-volume processing. Competing nations are working to close this gap, but they are starting from a position of significant disadvantage. Furthermore, the rare earth processing challenges facing Western nations remain formidable barriers to rapid diversification.

Indonesia and the Nickel Parallel

The IEA's report draws an instructive parallel between rare earth concentration and nickel refining. Indonesia has become the dominant force in refined nickel supply, and together with China, these two countries account for more than three-quarters of total growth in refined critical mineral supply globally. Export restrictions from the Democratic Republic of Congo on cobalt, and from Zimbabwe on lithium-related minerals, reinforce the pattern. The risk of supply chain concentration is no longer a theoretical concern flagged in risk assessments. It has become an operational reality confirmed by active policy decisions across multiple jurisdictions.

The Sectors With the Most to Lose

Defence and Aerospace

The defence sector occupies a unique position in this analysis. Western military manufacturers rely on heavy rare earths for guided munitions, radar arrays, satellite communications systems, and next-generation fighter aircraft propulsion. The April 2025 licensing system has effectively severed their access to Chinese-sourced dysprosium and terbium through legitimate commercial channels.

What makes this particularly acute is the competitive asymmetry at play. China's domestic defence and technology manufacturers retain uninterrupted access to the same materials being withheld from Western competitors. This is not a broad restriction applied uniformly. It is a targeted policy that simultaneously preserves Chinese industrial capacity while constraining that of strategic rivals.

Clean Energy Technologies

Neodymium-iron-boron permanent magnets, which depend on dysprosium for high-temperature performance, are central to both offshore wind turbine generators and electric vehicle drive motors. The critical minerals demand driven by the energy transition has, consequently, amplified the strategic leverage these export controls provide.

The practical tension is significant. National clean energy targets and EV manufacturing timelines are premised on access to materials whose supply is now actively restricted. Automakers and wind turbine manufacturers cannot simply reformulate their products to eliminate rare earth dependencies on short notice. Magnet design, motor architecture, and generator specifications are engineered around specific material properties that currently have no commercially viable substitutes at scale.

Semiconductors and Electronics

Rare earth elements appear throughout semiconductor manufacturing, precision optics, and display technologies. The history of the sector provides a useful reference point: during the 2010-2011 rare earth price spike, triggered by Chinese export quota reductions, prices for some heavy rare earths increased by more than 900% within a single year. Manufacturing disruptions cascaded across electronics supply chains well before any physical shortage materialised. Price volatility alone, without a complete supply cutoff, was sufficient to destabilise procurement planning globally.

The IEA's Proposed Response: Insurance at Scale

The IEA's recommended response centres on a multilateral stockpiling programme covering 11 high-risk critical materials. The initial acquisition cost is estimated at $9.2 billion, with a net annual maintenance cost of approximately $900 million. In the context of national defence and energy budgets, these are not large figures. Benchmarked against the $6.5 trillion in exposed downstream output, the ratio is stark.

According to Reuters reporting on the IEA's findings, IEA Director Fatih Birol has framed the cost of diversified supply chains not as economic inefficiency, but as a mineral security premium. In his articulation, paying above market rates for supply sourced outside highly concentrated single-country channels represents a rational form of economic insurance against disruptions that could dwarf those costs by orders of magnitude.

The IEA is explicit that unilateral stockpiling is insufficient. Coordinated international action is identified as a structural requirement, not an optional enhancement. The logic is straightforward: individual national reserves can be depleted quickly in a genuine supply crisis, while multilateral reserves create a larger, more credible buffer that also dilutes the strategic leverage any single restricting country can exercise.

| Metric | Stockpile Programme | Inaction Scenario |

|---|---|---|

| Initial capital required | $9.2 billion (one-time) | None |

| Annual net maintenance | ~$900 million | None |

| Downstream output at risk | Substantially hedged | $6.5 trillion per year |

| China's current refining share | 85% (slowly declining) | Projected 70% by 2035 (conditional) |

| Active export restriction regimes | China, DRC, Zimbabwe | Expanding trend |

The November 2026 Cliff: What Happens When the Suspension Expires?

The window created by China's November 2025 decision to pause the October 2025 expansion rules closes on November 10, 2026. If those controls are reinstated without modification, every foreign exporter of products containing 0.1% or more of Chinese-origin rare earths would require a licence to continue operating. The compliance burden would be immediate, the sourcing alternatives limited, and the disruption across electronics, clean energy, and precision manufacturing potentially severe.

The 12-month suspension window is not simply a grace period. It represents the most consequential window available for governments and manufacturers to advance alternative sourcing arrangements, accelerate refining investment outside China, and build the multilateral coordination frameworks the IEA has identified as essential. America's rare earth supply chain development, for instance, will be a key determinant of how much resilience Western industries can build before this deadline arrives.

Whether that window is used productively or allowed to expire without structural change will determine how much of the $6.5 trillion exposure remains operational risk versus theoretical ceiling. The European Parliament's analysis of these controls similarly underscores the urgency for coordinated policy responses before the suspension lapses.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: China Rare Earth Export Controls

What rare earth elements are currently under active Chinese export controls?

Seven heavy rare earth elements, including dysprosium, terbium, and lutetium, along with permanent magnet materials incorporating them, remain under mandatory licensing requirements established in April 2025. These controls were explicitly excluded from the November 2025 suspension.

Has China ended its rare earth export restrictions?

No. China paused one specific expansion of its controls until November 10, 2026. The core April 2025 licensing system remains active. Entity-level restrictions added in June 2026 also remain in force.

Why does a 0.1% concentration threshold matter so much?

At that level, the requirement would capture a vast range of manufactured goods that incorporate components processed through Chinese refining at any stage. The compliance implications extend far beyond direct rare earth buyers to affect the broader electronics and industrial manufacturing ecosystem.

What is the IEA's stockpile recommendation based on?

The IEA proposes multilateral acquisition of 11 high-risk critical materials at an initial cost of $9.2 billion, with annual net maintenance of approximately $900 million. The recommendation is framed as proportionate hedging against the $6.5 trillion in downstream industrial output that active China rare earth export curbs place at risk.

How much of global rare earth refining does China control?

China currently controls approximately 85% of global rare earth refining capacity. Combined with Indonesia's position in nickel refining, these two countries account for more than 75% of total growth in refined critical mineral supply globally.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Figures, projections, and policy timelines are drawn from publicly available IEA reporting and other cited sources. Forward-looking statements and scenario analyses involve uncertainty and should not be relied upon as predictions of future outcomes. Readers should conduct independent research before making any investment or procurement decisions.

Want to Identify ASX Opportunities in the Critical Minerals Sector Before the Market Does?

As rare earth supply chain pressures reshape global industries, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly alerting subscribers to significant critical mineral discoveries and actionable investment opportunities — explore historic discoveries and their remarkable returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.