July 15, 2026

The Geopolitics of Scarcity: Understanding China's Grip on the Minerals That Power Modern Civilisation

Few industrial dependencies in history have been constructed as deliberately, or as patiently, as China's dominance over rare earth element supply chains. While headlines focus on trade negotiations and export licences, the deeper story is one of decades-long strategic accumulation, deliberate market manipulation, and the systematic elimination of international competition. Today, the consequences of that strategy are being felt across defence programs, automotive production lines, semiconductor fabrication, and clean energy infrastructure simultaneously. Understanding how this situation developed, and what it genuinely means for the global economy, requires moving well beyond the political news cycle. China rare earth export restrictions now sit at the centre of one of the most consequential geopolitical contests of our era.

When big ASX news breaks, our subscribers know first

Critical Minerals vs. Rare Earth Elements: Why the Distinction Matters Strategically

One of the most persistent sources of confusion in policy discussions is the conflation of critical minerals with rare earth elements. These are related but distinct categories, and the distinction carries real strategic weight.

The United States Department of the Interior maintains the definitive domestic classification framework. Every three years, the Department reviews and updates its critical minerals list based on two specific criteria: how economically central a material is to U.S. industry, and how vulnerable its supply chain is to disruption. The 2025 update identified 60 critical minerals in total. Furthermore, rare earth elements form a specific subset of that list, comprising exactly 17 distinct elements, including neodymium, praseodymium, terbium, and dysprosium.

Importantly, materials like cobalt, lithium, and nickel are critical minerals under this framework but are not rare earth elements. This distinction matters because China rare earth export restrictions target a defined chemical group, not the broader critical minerals category, and the supply concentration dynamics are fundamentally different across these groups.

Light vs. Heavy Rare Earth Elements: Where the Real Vulnerability Lies

Within the rare earth category itself, a further division shapes the entire strategic landscape. Heavy rare earth elements (HREEs) carry a higher atomic number and correspondingly greater atomic weight. More critically from a supply perspective, they occur in significantly lower natural concentrations, making economically viable extraction far more technically demanding than for light rare earth elements (LREEs).

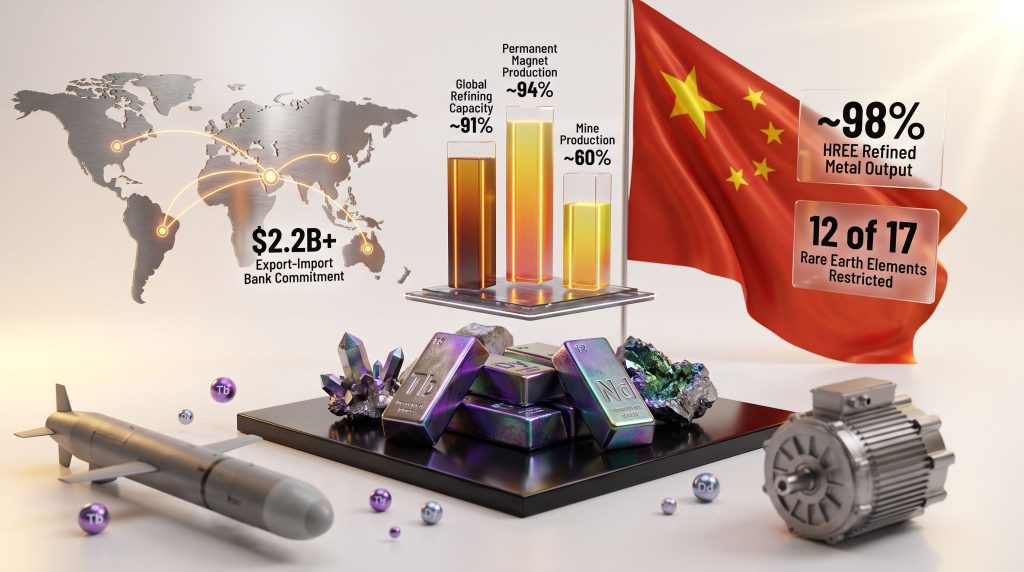

This geological reality translates directly into market concentration. According to analysis from the Center for Strategic and International Studies (CSIS) Critical Mineral Security Program, China controls approximately 98% of global HREE refined metal production, compared to roughly 70 to 80% for light rare earths. That 20-percentage-point gap explains precisely why China's export restriction architecture has been constructed almost entirely around heavy rare earths rather than lighter elements.

Why Permanent Magnets Sit at the Centre of Everything

The strategic importance of rare earths, particularly HREEs, is almost entirely driven by one application: permanent magnets. Unlike electromagnets, which require a continuous external electrical current to maintain their field, permanent magnets generate their magnetic field from the intrinsic properties of their constituent materials. This characteristic makes them uniquely suited to applications where size, weight, and power efficiency are simultaneously constrained.

The dual-use nature of rare earth permanent magnets is what elevates them from an industrial commodity to a national security priority:

- Defence applications: Tomahawk cruise missiles, advanced radar systems, fifth-generation fighter aircraft propulsion and guidance systems

- Clean energy infrastructure: Electric vehicle drivetrains, offshore and onshore wind turbine generators

- Medical and industrial technology: MRI scanners, industrial robotics, advanced manufacturing equipment

- Consumer electronics: Smartphones, hard disk drives, high-fidelity audio equipment

Any disruption to rare earth magnet supply simultaneously affects military readiness, energy transition timelines, and consumer technology production. No other single material category spans these domains so completely.

How the United States Lost the Industry It Invented

There is a striking historical irony embedded in the current crisis. The United States did not simply fail to develop rare earth processing capability — it pioneered it. Rare earth separation techniques were first developed at the Ames Laboratory as part of the Manhattan Project, where scientists needed methods to purify uranium by isolating rare earth element impurities. The foundational processing knowledge that now underpins China's industrial dominance was originally American intellectual property.

Through the 1950s, 1960s, 1970s, and into the early 1990s, the United States remained the world's leading rare earth producer, with applications expanding progressively from coloured television manufacturing into defence electronics and emerging clean technology platforms.

China's displacement of U.S. dominance followed a recognisable four-stage strategic playbook:

- Flood global markets with subsidised production, leveraging state-backed financing and tax rebate structures established after China emerged from the Cultural Revolution in the 1970s and 1980s

- Crash market prices to levels that made Western producers commercially unviable, combined with lower labour costs and less stringent domestic environmental regulation

- Dominate global supply chains once international competitors had exited the market

- Restrict supply strategically to extract geopolitical leverage when required

This strategy was not accidental. China designated rare earths as a central pillar of its long-term industrial policy, investing systematically in joint venture arrangements, technology transfer agreements, specialist research infrastructure, and the development of deep technical human capital across multiple decades.

The broader forces of economic globalisation accelerated this process. As manufacturing shifted internationally during the 1990s and 2000s, rare earth processing migrated with it — a trend that seemed economically rational at the time but created structural dependencies that are now extraordinarily difficult to unwind.

China's Current Market Control: Key Statistics

| Metric | China's Share |

|---|---|

| Global rare earth mine production | ~60% |

| Global rare earth refining capacity | ~91% |

| Permanent magnet production | ~94% |

| Heavy rare earth refined metal output | ~98% |

| Light rare earth refined metal output | ~70-80% |

China's 2025 Export Restriction Architecture: A Two-Wave Strategy

The China rare earth export restrictions that began materialising in 2025 represent the most aggressive deployment of this strategic leverage in the history of the sector. The restrictions were constructed in two distinct waves, each carefully calibrated to maximise economic pressure while preserving negotiating optionality. According to the IEA's analysis of these controls, supply concentration risks have now become a tangible reality rather than a theoretical concern.

Wave One: April 2025

Introduced as a direct response to escalating U.S. tariff measures, the first wave imposed mandatory export licensing requirements across seven heavy rare earth elements: samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium. The scope covered raw minerals, chemical compounds, refined metals, and finished magnet products.

For overseas entities with any connection to defence sector supply chains, licences are generally not issued under Wave One. This restriction remains fully active as of mid-2026.

Wave Two: October 2025

The second wave extended coverage to an additional five heavy rare earth elements: holmium, erbium, thulium, europium, and ytterbium. More significantly, it introduced a sweeping foreign direct product rule requiring Chinese government approval for any product manufactured anywhere in the world that contains 0.1% or more Chinese-origin rare earths or was produced using Chinese processing technology. This extraterritorial reach extended the restriction framework to cover technologies, processing equipment, and even specialist personnel expertise.

The November 2025 Moratorium: A Reprieve, Not a Resolution

Following direct engagement between President Trump and President Xi, a one-year moratorium on Wave Two restrictions was announced in November 2025. The suspension applies specifically to the October 2025 directives and expires in November 2026.

Wave One licensing requirements for the initial seven elements remain fully in force. China retains complete discretionary authority over who receives export licences and in what volumes. The moratorium does not restore supply certainty — it defers a portion of the restriction framework temporarily.

What makes the practical reality even more concerning is the gap between the formal policy position and actual trade flows. Reporting from The New York Times indicates the United States has not successfully imported dysprosium or terbium from China since restrictions were first imposed, regardless of the moratorium. Yttrium export volumes have remained anomalously low even during the suspension period. U.S. aerospace and semiconductor manufacturers have been unable to secure the shipment volumes their production requirements demand.

In June 2026, China escalated further by adding MP Materials and USA Rare Earth specifically to its export control entity list, halting dual-use exports to both firms irrespective of the broader moratorium terms.

Full Restriction Coverage Summary

| Element Group | Wave | Current Status |

|---|---|---|

| Samarium, Gadolinium, Terbium, Dysprosium, Lutetium, Scandium, Yttrium | Wave 1 (Apr 2025) | Active: licensing required |

| Holmium, Erbium, Thulium, Europium, Ytterbium | Wave 2 (Oct 2025) | Suspended until Nov 2026 |

| Foreign direct product rule (≥0.1% Chinese REE content) | Wave 2 (Oct 2025) | Suspended until Nov 2026 |

| Defence sector export ban | Both waves | Active and unchanged |

| MP Materials & USA Rare Earth dual-use ban | June 2026 entity list | Active |

In aggregate, China's restriction framework now covers 12 of the 17 recognised rare earth elements, creating simultaneous supply risk across smartphones, military platforms, electric vehicles, and advanced semiconductor fabrication equipment.

The Real Economic Cost: What Restriction Looks Like at the Production Line

The strategic and geopolitical dimensions of China rare earth export restrictions can obscure their immediate industrial consequences. In 2025, major automotive manufacturers were forced to pause production lines when they could not secure sufficient HREE-dependent permanent magnets. This was not an abstract supply chain modelling exercise — it translated directly into factory shutdowns and revenue loss at some of the world's largest industrial companies.

That operational disruption proved more diplomatically persuasive than years of policy advocacy, bringing rare earth access directly onto the agenda of U.S.-China trade negotiations alongside tariffs and semiconductor export controls. The automotive sector experience demonstrated that HREE dependency creates genuine, near-term production risk, not merely long-term strategic vulnerability.

Price dynamics have reinforced this message. Following the April 2025 restriction announcements, rare earth element prices experienced significant upward pressure across global commodity markets. Terbium and dysprosium, the two elements most critical to high-performance permanent magnets used in EV drivetrains and defence systems, recorded the sharpest price movements. These represent the strategic importance of rare earths at their most acute, with scandium, yttrium, and europium all experiencing compounding supply risk as restrictions layered across multiple high-value industrial sectors simultaneously.

The United States Response: An All-of-Government Mobilisation

The U.S. response to China rare earth export restrictions has involved coordinated action across multiple federal departments and international financing institutions, representing the most comprehensive government-level engagement with critical mineral supply security in decades.

On the domestic front, the U.S. Department of the Interior has focused on accelerating permitting processes for domestic rare earth mining and refining projects, while the Department of Energy has directed funding toward rare earth recycling innovation and next-generation processing technologies. The U.S. defence industry has been given a target of 2027 to transition rare earth sourcing away from Chinese supply chains — a timeline that the CSIS Critical Mineral Security Program characterises as ambitious given current production realities.

International financing has been deployed with notable scale and geographic breadth:

- The Development Finance Corporation (DFC) has financed rare earth production projects in Brazil

- The Export-Import Bank has committed over $2.2 billion to Australian critical mineral projects, with a significant allocation directed toward rare earth development specifically

- The Department of Defence Office of Strategic Capital has invested in a rare earth refining facility in Saudi Arabia

These financing commitments represent a meaningful shift in how the U.S. government uses its international financial institutions, deploying them as instruments of supply chain security rather than purely commercial development vehicles.

The next major ASX story will hit our subscribers first

What G7 Allies Are Doing: The Paris Declaration and Japan's 15-Year Lesson

At the most recent G7 summit held in Paris, member nations issued a formal collective commitment: no single country should supply more than 60% of any G7 member's rare earth imports by 2030. This represents the first multilateral, quantified rare earth diversification benchmark agreed among major allied economies, aligning with but extending beyond the U.S. defence sector's 2027 target.

The realism of this commitment deserves sober assessment. Outside China, primary HREE production remains extremely limited. The most significant non-Chinese producer is Lynas Rare Earths, an Australian company operating processing facilities in both Australia and Malaysia, which supplies rare earths to both Japan and the United States. However, beyond Lynas, announced projects across the U.S., Australia, and Brazil remain largely in development stages, with translation from announcement to commercial production requiring years of capital deployment, permitting work, and technical commissioning.

Japan's experience provides the most instructive real-world benchmark for what supply diversification actually requires at scale. Japan was the first major economy to experience China weaponising rare earth export access, during a 2010 maritime dispute that resulted in Chinese rare earth shipments to Japan being severed. Given that Japan's permanent magnet industry accounts for approximately 15% of global production, the impact was severe and immediate.

Japan's response over the following 15 years incorporated:

- Domestic innovation programs targeting rare earth recycling technologies

- Investment in deep-sea mining research and development

- Early strategic investment in Lynas Rare Earths, enabling the development of an alternative supply source that now also serves the United States

- International partnership frameworks to diversify import sources across multiple jurisdictions

The result after 15 years of sustained effort and investment? Japan still sources approximately 60% of its rare earths from China. This is not a failure of strategy or commitment — it is an accurate reflection of how structurally entrenched China's processing dominance has become. The CSIS Critical Mineral Security Program points to Japan's experience as the most important lesson for the United States and its allies: rare earth supply diversification is a decade-scale undertaking, not a problem solvable within a single policy cycle or electoral term.

Can China's Dominance Actually Be Broken? A Structural Assessment

Answering this question honestly requires confronting several structural barriers that political announcements and financing commitments do not automatically resolve.

The Processing Infrastructure Gap

Mining rare earth ore is only the first step in a complex, capital-intensive value chain. The refining, separation, and metallisation infrastructure that transforms raw ore into usable metals, alloys, and magnet precursors is almost entirely concentrated in China. Building equivalent processing capacity elsewhere requires not just capital but decades of accumulated technical knowledge that China has systematically developed and retained within its domestic industry.

Where Non-Chinese Supply Is Emerging

| Country/Region | Development Stage | Key Focus |

|---|---|---|

| Australia (Lynas) | Operational | Light and heavy REE separation, Malaysia processing |

| United States | Permitting and early production | Domestic mining and refining scale-up |

| Brazil | Development (DFC-backed) | REE production diversification |

| Malaysia | Operational (Lynas facility) | HREE processing capacity |

| Saudi Arabia | Refining investment | DoD-backed processing infrastructure |

The Recycling and Innovation Pathway

A frequently underappreciated medium-term supply lever is rare earth recycling from end-of-life products. Electric vehicle motors, wind turbine generators, and consumer electronics all contain recoverable rare earth content. Magnet-to-magnet recycling loops, if scaled effectively, could meaningfully reduce primary mining dependency over a 10 to 15 year horizon.

U.S. Department of Energy funding is specifically targeting new separation and processing technologies designed to reduce both the cost and environmental footprint of rare earth recovery from secondary sources. Furthermore, this pathway — combined with the energy transition's demand for new primary production from allied nation projects — represents a meaningful structural contribution to long-run supply diversification.

Frequently Asked Questions: China Rare Earth Export Restrictions

What triggered China's 2025 rare earth export restrictions?

China introduced mandatory export licensing in April 2025 as a direct countermeasure to escalating U.S. tariff policies, framing the controls under a national security rationale.

Which rare earth elements remain restricted today?

The April 2025 Wave One restrictions covering samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium remain active. The October 2025 Wave Two restrictions have been suspended until November 2026, but Wave One and the defence sector ban remain unchanged.

Has the U.S.-China trade agreement resolved the rare earth problem?

The November 2025 moratorium provides only a temporary, partial reprieve. Wave One licensing is still active, specific U.S. firms remain on China's entity list, the defence sector ban is unchanged, and the moratorium itself expires in November 2026 subject to renegotiation.

What is the G7's commitment on rare earth diversification?

G7 nations pledged at their Paris summit that no single country should supply more than 60% of any member nation's rare earth imports by 2030.

How long has Japan been working to reduce its rare earth dependency on China?

Japan has been executing a diversification strategy since 2010, following China's weaponisation of rare earth exports during a maritime dispute. After 15 years of sustained investment and effort, Japan still imports approximately 60% of its rare earths from China.

What is the practical difference between light and heavy rare earth elements for investors and industry?

Heavy rare earth elements occur in lower natural concentrations, making economically viable extraction far more technically demanding. China controls approximately 98% of global HREE refined metal production, compared to 70 to 80% for light rare earths. This concentration differential explains why China's export restriction architecture has been constructed almost entirely around heavy rare earths, and why supply disruption risk is most acute in this category.

Key Takeaways: The Strategic Landscape at a Glance

| Strategic Dimension | Current Reality |

|---|---|

| China's HREE refining control | ~98% |

| Elements under active Wave 1 restrictions | 7 (from April 2025) |

| Elements under suspended Wave 2 restrictions | 5 (from October 2025) |

| Moratorium expiry date | November 2026 |

| G7 diversification target | No single nation above 60% by 2030 |

| U.S. defence sector deadline | 2027 |

| Japan's progress after 15 years | Still approximately 60% China-dependent |

| Export-Import Bank Australia commitment | $2.2 billion and above |

| Total rare earth elements now within China's restriction framework | 12 of 17 |

A Temporary Truce in a Long-Term Structural Contest

The November 2025 moratorium should not be mistaken for a resolution of the underlying challenge. It addresses Wave Two measures only, while the foundational licensing architecture of Wave One remains fully operational. China retains complete discretionary authority over export licence issuance, volume allocation, and entity-level targeting.

The June 2026 decision to add specific U.S. firms to the export control entity list — within an active moratorium period — demonstrates that selective restriction continues as an active tool regardless of broader diplomatic agreements. As detailed analysis from the European Parliament's think tank highlights, China's trade strategy in this sector is far more architecturally sophisticated than a simple on-off policy lever.

For the United States and its G7 allies, the window between now and November 2026 represents a critical period for accelerating non-Chinese supply development. The investments being made through the DFC, the Export-Import Bank, and allied nation partnerships are meaningful steps. However, as Japan's 15-year experience demonstrates, the structural challenge of rare earth supply diversification operates on timescales that outlast individual administrations, trade negotiations, and market cycles. Understanding China's rare earth trade strategy in its full complexity is consequently essential for any government or industry stakeholder seeking to navigate what lies ahead.

The nation that controls rare earth processing controls the enabling inputs for both the clean energy transition and next-generation military capability. For allied nations, China rare earth export restrictions have made unmistakably clear that this is not a commodity market problem to be managed through procurement strategy. It is a foundational question of industrial sovereignty that will define strategic competitiveness for decades.

This article contains forward-looking assessments and policy analysis based on publicly available information as of mid-2026. Supply chain conditions, restriction frameworks, and geopolitical dynamics in this sector can change rapidly. Nothing in this article constitutes financial or investment advice. Readers should conduct independent due diligence before making any investment decisions related to rare earth elements or critical mineral sectors.

Want to Invest in the Next Major Rare Earth or Critical Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, instantly translating complex geological and commodity data into actionable investment insights — including across the rare earth and critical minerals sectors reshaping global supply chains. Explore historic discoveries and the returns they generated, then begin your 14-day free trial to position yourself ahead of the broader market.