June 23, 2026

China rare earth export restrictions have emerged as a defining force in global supply chain transformation, fundamentally altering the landscape of manufacturing dependencies that emerged from decades of globalisation. The industrial architecture that previously prioritised efficiency over resilience now confronts systematic vulnerabilities extending far beyond immediate commodity markets. These developments highlight the critical importance of critical minerals energy security as nations reassess their resource dependencies.

The transformation currently unfolding demonstrates how resource nationalism can rapidly alter established trade relationships and force manufacturers to confront supply chain dependencies they previously considered manageable risks. Economic warfare through commodity controls represents a departure from traditional trade disputes, utilising critical materials as leverage points that cascade through entire industrial sectors.

Understanding China Rare Earth Export Restrictions and Their Strategic Significance

The Foundation of Modern Supply Chain Dependencies

Rare earth elements comprise seventeen chemically similar metals that serve as essential components in modern technology manufacturing. These materials enable the magnetic properties in electric vehicle motors, the conductivity in smartphone circuitry, and the precision guidance systems in defence equipment. Despite their name, these elements exist in relatively abundant quantities globally, but their extraction and processing require specialised knowledge and significant environmental management capabilities.

China's dominance in rare earth production stems not from geological advantages but from decades of investment in processing infrastructure and willingness to accept environmental costs that other nations avoided. This strategic positioning has created dependencies that extend beyond simple supply relationships into technological and industrial vulnerabilities.

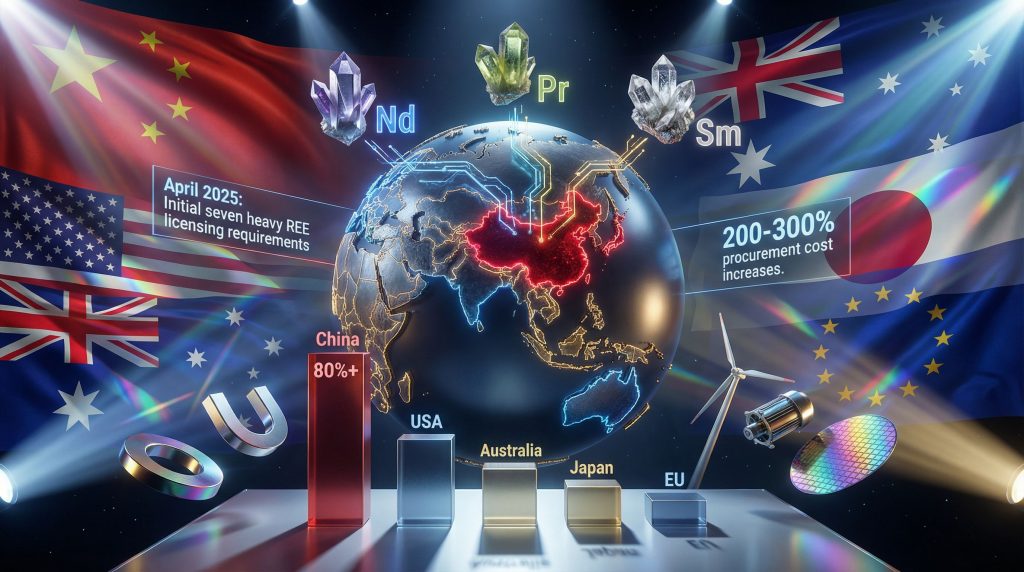

The April 2025 implementation of export licensing requirements marked a departure from market-based allocation toward administrative control mechanisms. These restrictions initially targeted seven heavy rare earth elements before expanding to encompass alloys and finished magnets. The escalation pattern reveals deliberate economic pressure application rather than reactive trade policy.

Policy Evolution and Escalation Mechanisms

China's export control implementation followed a calculated progression designed to maximise economic disruption while maintaining plausible policy justification. The initial April 2025 measures emerged as Beijing responded to intensified U.S. trade pressures, establishing precedent for using rare earth exports as geopolitical leverage.

The July 2025 expansion to alloys and magnets represented significant escalation, as these downstream products require substantial processing infrastructure that few nations possess outside China. This progression forced manufacturers to confront not merely raw material constraints but complete supply chain disruption.

October 2025 brought extraterritorial enforcement provisions requiring end-use verification for products containing even minimal Chinese rare earth content. These measures created compliance challenges extending far beyond direct trade relationships, forcing global manufacturers to audit their entire supply chains for Chinese material content.

The November 2025 tactical suspension and subsequent reimplementation demonstrated how export restrictions function as dynamic policy tools rather than static trade measures. This volatility created persistent uncertainty that proved as disruptive as the restrictions themselves.

When big ASX news breaks, our subscribers know first

Economic Leverage Mechanisms and Bureaucratic Bottlenecks

Administrative Control Through Licensing Systems

Export licensing creates multiple pressure points beyond simple approval delays. The application process requires detailed end-use documentation, corporate ownership verification, and technological transfer commitments that extend Chinese oversight into foreign manufacturing operations. These requirements transform routine procurement into strategic negotiations.

The licensing system's opacity generates additional uncertainty as approval criteria remain unpublished and appear to shift based on geopolitical considerations. Japanese manufacturers report particular difficulty securing approvals following Prime Minister Sanae Takaichi's Taiwan-related statements, indicating that licensing decisions incorporate foreign policy considerations beyond commercial factors.

Processing timelines create operational challenges that extend beyond administrative delays. Manufacturers accustomed to just-in-time inventory management find themselves forced to maintain strategic stockpiles or accept production interruptions. This shift from lean manufacturing toward inventory buffering increases working capital requirements and reduces operational efficiency.

Extraterritorial Enforcement and Global Compliance Challenges

The implementation of content thresholds for re-export restrictions creates compliance challenges affecting manufacturers with no direct Chinese trade relationships. Components containing Chinese rare earth materials trigger licensing requirements when incorporated into products destined for certain markets, forcing global supply chain auditing.

Technology transfer restrictions accompanying export licences extend Chinese policy influence into foreign industrial development. Manufacturers seeking stable rare earth supplies must accept limitations on their technological partnerships and development priorities, representing sovereignty implications beyond commercial concerns.

Third-country manufacturing operations face particular challenges as Chinese enforcement mechanisms create uncertainty about existing supply agreements and processing capabilities. Facilities that previously enjoyed operational independence find themselves subject to Chinese policy decisions affecting their input costs and production schedules.

Industrial Sector Vulnerabilities and Supply Chain Disruption

High-Technology Manufacturing Dependencies

Electric vehicle manufacturers face severe supply constraints as motor magnets require specific rare earth combinations that offer limited substitution possibilities. Neodymium and praseodymium provide magnetic strength-to-weight ratios essential for vehicle performance and efficiency targets. Alternative magnet technologies exist but require significant engineering modifications and performance compromises.

Defence equipment manufacturing confronts critical supply vulnerabilities as guidance systems, communications equipment, and propulsion technologies depend on rare earth elements with no viable substitutes. Samarium-cobalt magnets maintain performance under extreme temperature conditions that aluminium-nickel-cobalt alternatives cannot match. These technical requirements create national security implications beyond commercial concerns.

Semiconductor fabrication requires rare earth compounds for specialised processing steps and substrate preparation. Lanthanum glass provides optical clarity for precision lithography equipment, while cerium compounds enable chemical-mechanical polishing processes. These applications demand material purity levels that limit alternative sourcing options.

Cost Multiplication and Profit Margin Compression

Japanese manufacturers report procurement costs that have doubled or tripled according to Katahiro Yasukochi, chair of the Japanese Association of Metal, Machinery and Manufacturing Workers. These increases reflect not only material costs but also procurement complexity, inventory requirements, and supply security measures.

The inability of companies to pass increased costs to customers creates structural profitability pressure across affected industries. This margin compression forces manufacturers to absorb input cost volatility while maintaining competitive pricing, reducing their financial flexibility for research and development investments.

Wage negotiation impacts demonstrate how supply chain disruptions transmit into labour markets. Japanese union negotiations show wage increases of 5.70% compared to 5.77% the previous year, reflecting constrained corporate profitability despite inflationary pressures elsewhere in the economy.

| Manufacturing Sector | Primary REE Dependencies | Cost Impact Range | Substitution Feasibility |

|---|---|---|---|

| Electric Vehicles | Neodymium, Praseodymium | 200-300% increase | Limited alternatives |

| Defence Systems | Samarium, Gadolinium | Variable supply | Minimal substitutes |

| Consumer Electronics | Lanthanum, Cerium | Significant margins | Some alternatives available |

| Renewable Energy | Multiple magnet materials | Supply constraints | Long-term development needed |

Furthermore, the implications of these disruptions extend to national policy frameworks, with governments developing strategic minerals reserve programs to enhance supply security against future restrictions.

Economic Theory Applications in Resource Nationalism

Strategic Trade Policy and Mercantile Economics

China's export restriction strategy reflects mercantile trade theory principles that prioritise domestic industrial development over pure export revenue optimisation. By constraining raw material exports while encouraging downstream processing investment, Beijing attempts to capture higher value-added manufacturing within Chinese borders.

This approach follows historical precedents where resource-controlling nations leveraged commodity exports for industrial development objectives. The oil embargoes of the 1970s demonstrated how strategic commodities could achieve foreign policy goals while forcing structural adjustments in importing economies.

Vertical integration incentives created by export restrictions encourage foreign manufacturers to relocate processing operations to China to secure stable material supplies. This "resource magnetism" effect supports Chinese industrial policy goals while increasing foreign technological dependency.

Game Theory Dynamics in Trade Confrontation

The prisoner's dilemma framework applies to rare earth trade disputes as both exporters and importers face choices between cooperation and defection strategies. China benefits from export restrictions when importers cannot coordinate alternative supply development, but faces retaliation risks if targeted nations successfully diversify their sources.

First-mover advantages in supply chain control provide temporary leverage but create long-term vulnerabilities as restricted markets develop alternative sources. China's current dominance reflects decades of investment in processing infrastructure, but export restrictions accelerate competing nations' development timelines.

Nash equilibrium outcomes suggest that sustainable trade relationships require mutual benefit recognition rather than zero-sum competition. Current tensions indicate departure from equilibrium conditions, creating instability that affects all participants regardless of their individual strategies.

Global Market Response Patterns and Investment Flows

Price Discovery in Constrained Markets

Spot market pricing for non-Chinese rare earth sources reflects supply security premiums that extend far beyond traditional commodity price differentials. Australian and African producers command significant premiums despite higher processing costs, as manufacturers prioritise supply reliability over cost minimisation.

Long-term contract renegotiations incorporate force majeure provisions and alternative sourcing requirements that fundamentally alter traditional buyer-seller relationships. These contractual innovations distribute supply risk more explicitly while creating flexibility mechanisms for both parties during disruption periods.

Inventory accumulation strategies among manufacturers create artificial demand spikes that exaggerate short-term price volatility while building strategic buffers against future supply interruptions. This hoarding behaviour reflects rational responses to supply uncertainty but amplifies market instability.

Alternative Supply Development and Strategic Partnerships

Lynas Corporation's expanded partnerships with Japanese manufacturers represent emerging insurance strategies against Chinese supply disruptions. These bilateral arrangements prioritise supply security over cost optimisation, creating parallel supply chains that reduce dependency risks.

Investment acceleration in non-Chinese processing facilities reflects long-term strategic positioning rather than short-term profit optimisation. Australian, Canadian, and African projects receive funding despite higher operational costs because they offer supply diversification benefits that justify premium pricing.

Strategic Development Insight: Government subsidies for domestic processing capacity development signal policy recognition that market mechanisms alone cannot address supply security concerns in strategic materials sectors.

However, these developments must contend with broader geopolitical considerations, as China rare earth tariffs continue to reshape global pricing dynamics and investment flows.

Macroeconomic Transmission Mechanisms and Policy Implications

Balance of Payments Adjustments and Currency Effects

Trade deficit implications for major importing economies extend beyond immediate commodity costs to encompass broader current account adjustments. Nations previously enjoying competitive advantages in rare earth-intensive manufacturing face structural trade balance deterioration as their input costs increase relative to competitors.

Currency market effects reflect not only trade flow changes but also investment capital redirection toward alternative supply development. Resource-rich nations with rare earth potential experience investment inflows that strengthen their currencies while creating domestic inflation pressures.

Central bank policy responses must balance supply-driven inflation pressures against broader economic stability objectives. Traditional monetary policy tools prove less effective against supply constraint inflation, forcing consideration of strategic reserve policies and industrial support measures.

Labour Market Impacts and Wage Transmission

Employment effects vary significantly across industrial sectors depending on their rare earth intensity and substitution possibilities. High-tech manufacturing faces potential job losses if production relocates to secure supply access, while mining and processing sectors in alternative source countries experience employment growth.

Wage negotiation dynamics demonstrate direct transmission from commodity supply disruptions to labour market outcomes. Japanese manufacturers' constrained wage growth reflects profit margin compression from input cost increases, creating broader economic effects beyond the immediately affected industries.

Skill development requirements shift as nations invest in domestic processing capabilities, creating demand for specialised technical expertise in rare earth processing and alternative technology development. These human capital investments represent long-term structural adjustments to supply chain disruption.

The next major ASX story will hit our subscribers first

Geopolitical Alliance Formation and Strategic Partnerships

Coalition Building for Supply Security

The U.S.-Australia Critical Minerals Partnership demonstrates how traditional alliance structures extend into resource security cooperation. These agreements combine military alliance frameworks with commercial supply arrangements, creating hybrid institutions that address both security and economic objectives.

Additionally, the development of European raw materials supply initiatives reflects broader concerns about supply chain dependencies that extend beyond Chinese relationships. These programmes aim to develop comprehensive domestic capabilities rather than simply diversifying import sources.

Japan-India cooperation arrangements leverage India's rare earth deposits and Japan's processing technology to create alternative supply chains that bypass Chinese control points. These partnerships require substantial investment coordination but offer long-term supply security benefits.

Technology Sharing and Knowledge Transfer

Research collaboration frameworks accelerate technological development through shared investment in recycling technology and substitution research. These cooperative programmes would be economically inefficient for individual nations but provide collective benefits that justify coordinated funding.

Patent sharing agreements facilitate technology transfer between allied nations while maintaining competitive advantages over non-participating countries. These arrangements create exclusive technology clubs that support strategic supply chain development.

Export credit agency financing enables alternative supply project development through government-backed lending that commercial markets would not support. These programmes socialise investment risks while privatising eventual returns, creating mixed economic incentives that prioritise strategic objectives over market efficiency.

Long-Term Structural Transformation and Innovation Acceleration

Supply Chain Regionalisation Trends

Friend-shoring strategies replace globalised sourcing with politically aligned supply networks that prioritise relationship stability over cost minimisation. These arrangements create regional trading blocs that may prove less economically efficient but offer greater supply security.

Transportation cost implications for decentralised supply chains include not only shipping expenses but also inventory requirements and quality control complexity. Regional supply networks require duplicate infrastructure investments that increase overall system costs while improving resilience.

Processing hub development in multiple regions creates redundant capacity that provides supply security at the expense of economies of scale. These investments represent strategic insurance policies that may prove economically justified if supply disruptions continue.

Materials Science Innovation and Substitution Development

Research and development acceleration in alternative magnet technologies receives both government funding and private investment as manufacturers seek independence from rare earth dependencies. These programmes focus on both performance improvements and cost reduction to achieve commercial viability.

Recycling technology advancement offers potential supply augmentation that reduces dependency on primary mining operations. Urban mining of electronic waste provides rare earth recovery opportunities that become economically attractive as primary material costs increase.

Venture capital investment in critical minerals startups reflects market recognition that supply chain disruptions create business opportunities for innovative companies developing alternative solutions. These investments support technological diversification while potentially generating substantial returns.

Investment Strategy Considerations and Portfolio Positioning

Sector Allocation and Risk Management

Investment strategies must account for supply chain vulnerabilities that traditional financial analysis may underestimate. Companies with high rare earth intensity face operational risks that extend beyond normal business cycle considerations, requiring specialised risk assessment methodologies.

Portfolio diversification strategies should consider geographic and technological exposure to supply chain disruptions. Traditional sector allocation may prove inadequate if supply constraints affect multiple industries simultaneously through shared input dependencies.

Currency hedging approaches must account for commodity supply disruption effects that may persist longer than typical trade cycle adjustments. Resource-producing nations may experience sustained currency appreciation that affects international investment returns.

Alternative Investment Opportunities

Mining and processing company investments in non-Chinese jurisdictions offer potential benefits from supply diversification trends while carrying geological and political risks specific to their operating environments. These investments require specialised due diligence capabilities and long-term holding periods.

Technology company investments in substitution and recycling solutions provide exposure to innovation opportunities created by supply constraints. These investments offer potential for substantial returns but carry technological development risks and uncertain commercialisation timelines.

Real asset allocation adjustments may provide inflation protection against supply-driven cost increases while offering physical commodity exposure that traditional financial instruments cannot replicate. Strategic mineral investments require specialised storage and handling capabilities.

Policy Response Frameworks and International Coordination

Government Intervention Mechanisms

Strategic reserve policies modelled on petroleum reserve systems provide supply security buffers during disruption periods. These programmes require substantial upfront investment and ongoing management costs but offer supply stability that markets alone cannot provide.

Antitrust exemptions for supply chain cooperation enable industry collaboration in alternative source development that would otherwise violate competition regulations. These policy adjustments recognise that supply security may require coordination mechanisms that pure market competition cannot achieve.

Trade finance guarantees support alternative sourcing investments through government-backed lending that reduces private sector risks. These programmes socialise certain investment costs while maintaining private sector operational efficiency and innovation incentives.

Multilateral Cooperation Frameworks

World Trade Organisation dispute resolution mechanisms face limitations when addressing strategic commodity export restrictions that countries justify on national security grounds. These limitations highlight needs for new international frameworks that can address resource security concerns while maintaining trade cooperation benefits.

Bilateral investment treaty renegotiations must address supply chain security considerations that traditional trade agreements did not anticipate. These revisions require balancing investment protection with supply security objectives that may conflict during crisis periods.

In this context, the evolution of critical minerals policy frameworks represents emerging international cooperation mechanisms specifically designed to address supply chain vulnerabilities in strategic materials.

Why Are China's Export Controls Particularly Concerning?

The concern surrounding China rare earth export restrictions stems from the country's overwhelming market dominance combined with the essential nature of these materials for modern technology. China controls approximately 80% of global rare earth processing capacity, creating a near-monopoly that affects everything from electric vehicle manufacturing to defence systems.

Moreover, the extraterritorial nature of these controls means that companies worldwide must comply with Chinese regulations even when they don't directly trade with Chinese suppliers, fundamentally altering global supply chain governance.

What Alternative Sources Are Available?

While rare earth deposits exist globally, processing capability remains concentrated in China. Australia's Lynas Corporation operates the only significant non-Chinese processing facility, but its capacity remains limited compared to global demand. New projects in Canada, the United States, and Africa are under development but require substantial investment and time to reach commercial production.

These alternative sources face significant challenges including higher processing costs, environmental regulations, and the need to develop downstream manufacturing capabilities. Furthermore, many projects rely on Chinese investment or technology partnerships, creating potential vulnerability to political pressure.

Navigating Resource Geopolitics and Supply Chain Resilience

Strategic Planning Considerations

Supply chain diversification represents a national security imperative that extends beyond commercial optimisation to encompass strategic independence objectives. These considerations require government-business cooperation frameworks that traditional market mechanisms cannot adequately address.

Market-based solutions offer efficiency advantages but may prove inadequate for addressing supply security concerns that involve long-term strategic considerations. Government intervention mechanisms must balance market efficiency with supply security objectives through carefully designed policy instruments.

Long-term competitiveness implications for manufacturing nations include both immediate supply cost effects and broader technological development consequences. Nations that successfully develop alternative supply chains may gain sustainable competitive advantages while those that remain dependent face persistent vulnerabilities.

Monitoring and Assessment Framework

Leading indicators for policy escalation include diplomatic tensions, trade negotiation outcomes, and investment flow patterns that may signal future supply disruption risks. These indicators require systematic monitoring capabilities that combine political analysis with economic assessment.

Supply-demand balance projections for alternative sources must account for development timelines, capacity constraints, and quality specifications that may limit substitution possibilities. These assessments require technical expertise in mining, processing, and manufacturing applications.

Technology breakthrough potential in substitution and recycling offers long-term supply security improvements that may fundamentally alter strategic material dependencies. Innovation monitoring requires understanding both current research directions and potential breakthrough applications.

The transformation of global supply chains through China rare earth export restrictions demonstrates how resource nationalism can rapidly restructure international trade relationships. These changes require adaptive strategies that balance economic efficiency with supply security considerations while anticipating further evolution in the global resource landscape.

This analysis is provided for informational purposes and should not be considered as investment advice. Readers should conduct their own research and consult with qualified professionals before making investment decisions. The rare earth market involves significant risks including geological, political, and technological uncertainties that may affect investment outcomes.

Looking to Capitalise on Critical Minerals Supply Chain Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, helping subscribers identify actionable opportunities as global supply chains realign toward alternative sources. Begin your 14-day free trial today and position yourself ahead of the market during this period of unprecedented resource sector transformation.