August 4, 2026

The Hidden Chokepoint Driving Billions Into Australian Rare Earth Processing

For decades, the rare earth supply chain has operated as one of the most quietly consequential chokepoints in global industrial production. Unlike oil or copper, these materials rarely make front-page news during periods of stability. Yet the seventeen elements grouped under the rare earth classification underpin virtually every advanced technology transition currently underway, from electric vehicle drivetrains to precision-guided defence systems.

The mechanics of this vulnerability are specific. Rare earth elements are not merely mined in concentrated geographic areas; they require highly specialised, chemistry-intensive separation processes that are extraordinarily difficult and expensive to replicate outside established industrial clusters. China spent decades building this processing expertise, absorbing costs and environmental burdens that Western nations were unwilling to accept. The result is a structural dependency that cannot be unwound quickly, regardless of how urgently downstream manufacturers demand alternatives.

It is within this context that the Iluka rare earths refinery loan from Australia represents something far larger than a single infrastructure financing deal.

When big ASX news breaks, our subscribers know first

Understanding the Rare Earth Processing Bottleneck

Most discussions of rare earth supply risk focus on mining concentration. The more operationally significant constraint, however, sits downstream in the separation and refining stage. Even ore extracted from deposits outside China has, until recently, been shipped to Chinese facilities for processing because no viable alternatives existed at commercial scale.

China currently controls an estimated 85 to 90% of global rare earth refining capacity, a figure that reflects not just geographic advantage but decades of accumulated process chemistry knowledge, infrastructure investment, and deliberate industrial policy. Furthermore, this dominance means that a nation or company can own a world-class rare earth deposit and still remain functionally dependent on Beijing to convert that asset into usable material.

The consequences of this dependency became concrete in 2025 and 2026 as China's rare earth export restrictions imposed export licensing controls on terbium, dysprosium, and other heavy rare earth materials. The effect was immediate and measurable: no shipments of terbium or dysprosium oxide reached Japan from China after November 2025, according to reporting by Mining.com. For Japanese automotive and electronics manufacturers, who rely on these elements for high-performance permanent magnets, this was not a theoretical risk scenario. It was an operational crisis.

The export restriction episode exposed a fundamental reality: ownership of a rare earth mine is not equivalent to security of supply. What matters is control over the refining and separation infrastructure that transforms ore into market-ready oxide products.

Why Heavy Rare Earths Carry Disproportionate Strategic Weight

Within the rare earth family, a critical distinction separates light rare earths (such as neodymium and praseodymium) from heavy rare earths (primarily dysprosium and terbium). This distinction is commercially and strategically significant for several reasons:

- Heavy rare earths are sourced from a narrower geographic base, with China accounting for an even higher share of heavy REE production than it does for light REEs

- Dysprosium and terbium are functionally irreplaceable in high-temperature permanent magnets, where they preserve magnetic performance above 150 degrees Celsius, a critical requirement for EV motors and wind turbine generators

- Per-unit prices for heavy rare earths are substantially higher than for light fractions, meaning supply disruptions carry amplified economic consequences for downstream manufacturers

- Most Western rare earth processing projects focus on light REE fractions, because the chemistry is more established and the economics are more accessible, leaving heavy REE separation as an acute unmet need

This is precisely why the Eneabba facility's design scope, which targets separated output of both light and heavy rare earth oxides including neodymium, praseodymium, dysprosium, and terbium, positions it differently from most competing Western initiatives.

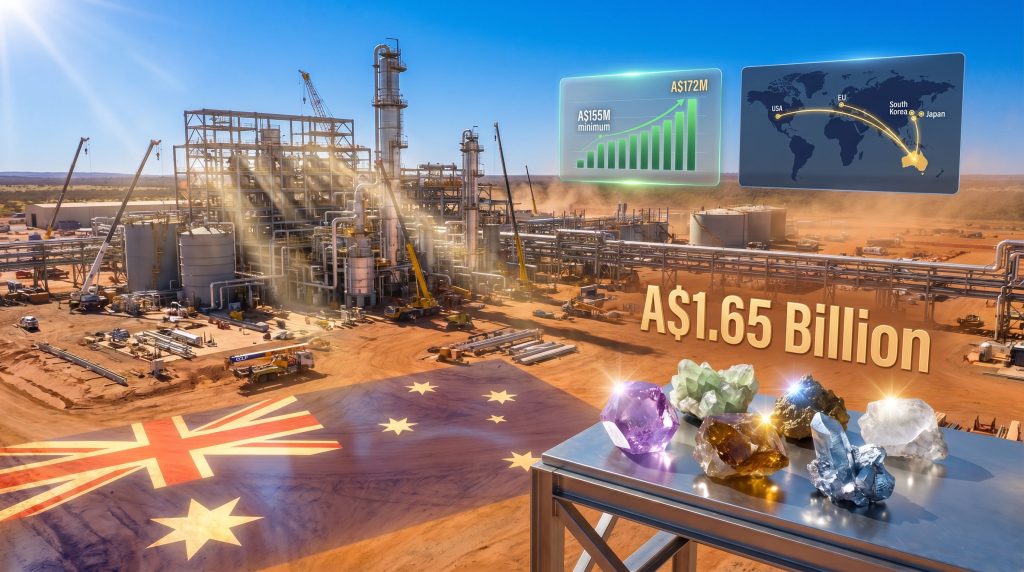

The A$1.65 Billion Financing Structure: Architecture and Rationale

The loan facility supporting the Eneabba refinery was not assembled as a single transaction. It evolved across multiple rounds of government decision-making, reflecting both the escalating strategic urgency of the project and the realities of cost revision that characterise first-of-kind processing infrastructure.

| Funding Component | Amount (AUD) | Key Condition |

|---|---|---|

| Original Critical Minerals Facility loan | A$1.25 billion | Approved 2022 |

| Supplementary tranche | A$400 million | Conditional on offtake agreements and community benefit compliance |

| Total government debt support | A$1.65 billion | First tranche fully drawn by end of 2026 |

| Iluka equity contribution | A$214 million | Committed alongside government loan |

| Cost overrun facility | A$150 million (50/50 split) | Available for potential cost escalation |

The loan is administered through Export Finance Australia (EFA), the federal government's export credit agency, and is structured on a non-recourse basis. This is a technically important distinction. Under a non-recourse structure, repayment obligations are tied specifically to project cash flows rather than to Iluka's broader corporate balance sheet. If the refinery underperforms commercially, lenders cannot pursue the parent company's general assets to recover shortfalls.

This structure serves a deliberate policy function. By ring-fencing the debt against project revenues, the government enables a commercially marginal but strategically essential project to proceed at a scale and on a timeline that purely commercial financing would not support. It is, in effect, a mechanism for transferring a portion of sovereign industrial policy risk onto the public balance sheet.

Non-recourse project finance is a well-established instrument in infrastructure development globally, but its application to a rare earth refinery of this scale in Australia represents a novel deployment of the model in the critical minerals context.

The supplementary A$400 million tranche carries specific access conditions. Iluka must demonstrate satisfactory offtake agreements before this portion becomes available, and must show compliance with community benefits principles embedded in the Future Made in Australia policy framework. Critically, this tranche can only be accessed after the original A$1.25 billion component has been fully utilised, creating a sequenced drawdown architecture that aligns capital deployment with construction progress.

Construction Progress and the First Confirmed Customer

As of June 2026, the Eneabba refinery has surpassed the 50% construction completion threshold, with the first tranche of funding expected to be fully drawn by year-end when the facility is projected to reach approximately 75% completion. The awarding of the Civmec structural, mechanical, piping, electrical and instrumentation contract in June 2026 marked a significant execution milestone, bringing a major works package under a confirmed contractor arrangement.

The commissioning target remains 2027, and the progression of construction milestones suggests this timeline is being actively tracked:

| Milestone | Status |

|---|---|

| Construction commencement | Underway |

| Current completion level | Over 50% (June 2026) |

| Projected completion at first tranche drawdown | ~75% (end 2026) |

| Civmec SMPEI contract awarded | Confirmed June 2026 |

| Target commissioning | 2027 |

Alongside the construction update, Iluka confirmed a binding four-year supply agreement with an unnamed global automotive manufacturer for magnet rare earth oxides. The contract covers approximately 10% of Iluka's planned production over the agreement period, with minimum contracted revenue of A$155 million and an upside scenario of approximately A$172 million under industry price forecasts.

While the automotive customer's identity remains confidential, the structure of the deal reflects several important market dynamics. Automotive manufacturers committing to long-term offtake agreements with non-Chinese rare earth suppliers are effectively paying a strategic premium for supply chain security. They accept price terms that may not undercut Chinese material on a spot basis but provide certainty of access that Chinese supply cannot currently guarantee.

The Offtake Gap: What Securing 10% of Production Means

The confirmed offtake agreement covering 10% of planned output is commercially meaningful but also highlights the scale of the commercial challenge ahead. For the Eneabba refinery to operate as a financially self-sustaining asset, Iluka will need to secure offtake arrangements or spot market access for the remaining 90% of planned production. This is not an unusual position for a project at this stage of construction, however it represents a material execution risk that investors should account for.

The magnet rare earth oxide market operates quite differently from bulk commodity markets. Buyers are often vertically integrated manufacturers with specific quality, specification, and provenance requirements. Building a commercial book of customers in this segment requires sustained engagement at the technical level, typically involving qualification processes that can take 12 to 24 months before a supply relationship converts to a binding contract.

Cost Escalation: A Structural Feature, Not a Project-Specific Failure

The revision of Eneabba's capital cost estimate from approximately A$1.2 billion to a range of A$1.7 billion to A$1.8 billion represents a 42 to 50% increase from the original figure. For observers unfamiliar with first-of-kind processing infrastructure, this may appear alarming. In practice, it reflects patterns documented across the rare earth processing challenges faced by the critical minerals sector globally.

Several structural factors drive cost escalation in greenfield refinery construction:

- Process chemistry novelty: Rare earth separation involves complex hydrometallurgical processes, often using solvent extraction circuits with dozens of sequential stages. Contractors with limited prior exposure to these specific chemistries routinely under-estimate labour and materials requirements at early design stages

- Remote location logistics: The Eneabba site in Western Australia is not proximate to major labour pools or industrial supply chains, creating cost structures that differ materially from projects in established industrial corridors

- Scope refinement during detailed design: The progression from conceptual or feasibility-level design to detailed engineering consistently reveals scope additions and specification changes that inflate capital requirements

- Broader construction cost inflation: The 2022 to 2025 period saw sustained inflation in construction materials, skilled trades labour, and equipment procurement across the global mining and processing sector

Large-scale first-of-kind processing facilities across lithium, nickel, and rare earth sectors have experienced average cost overruns of 30 to 60% between feasibility and construction completion. The establishment of a dedicated A$150 million cost overrun facility, shared equally between Iluka and the government, signals institutional recognition that further variance beyond the current revised range remains possible.

For investors assessing project economics, the relevant question is not whether cost escalation occurred, but whether the revenue model scales proportionally with the revised capital base. A facility that costs 50% more to build but operates in a market where prices for separated heavy rare earth oxides have risen substantially over the same period may still generate acceptable returns on the capital deployed.

Benchmarking Eneabba Against Global Competing Initiatives

The Eneabba project does not exist in isolation. Multiple government-backed rare earth processing initiatives are advancing globally, each with distinct scope, funding models, and strategic positioning:

| Project | Country | REE Focus | Government Support Model |

|---|---|---|---|

| Eneabba Refinery (Iluka) | Australia | Separated light and heavy REO | Non-recourse sovereign loan (A$1.65B) |

| MP Materials (Mountain Pass) | USA | Light rare earth concentrate | DoD offtake and equity investment |

| Lynas Rare Earths (Kalgoorlie) | Australia | Light rare earth separation | DoD-backed US processing facility |

| Pensana (Saltend) | UK | Separated NdPr oxide | UK government grant support |

| Solvay / Less Common Metals | Europe | Magnet alloy recycling | EU Critical Raw Materials Act funding |

Eneabba's competitive distinction lies in its integrated scope covering both light and heavy rare earth separation within a single facility. Most Western projects have concentrated on lighter, more commercially accessible fractions where the chemistry is better understood and feedstock is more abundant. The heavy REE separation component at Eneabba directly addresses the most acute supply gap in the current allied-nation rare earth landscape.

China's decision in mid-2026 to blacklist US-based rare earth producers including MP Materials from accessing Chinese rare earth inputs and supply chains further accelerated the urgency of developing ex-China processing alternatives. As reported by Reuters, Beijing's trade restrictions are deepening a wider struggle over supply chains vital to defence and advanced manufacturing, a dynamic that materially strengthens the strategic case for Eneabba's completion.

The next major ASX story will hit our subscribers first

Australia's Industrial Policy Framework and the Future Made in Australia Agenda

The Eneabba loan sits within a broader federal policy architecture designed to transition Australia from raw material exporter to value-chain participant in critical minerals. The Future Made in Australia agenda identifies critical minerals processing as a priority sector, with community benefit principles embedded as a condition of accessing government financing instruments.

Australia's critical minerals strategy is increasingly coordinated with allied nations through mechanisms including the Minerals Security Partnership (MSP) and bilateral trade and investment frameworks with the United States, Japan, South Korea, and the European Union. These arrangements create demand-side pull for Australian processed material among allied manufacturers seeking to reduce exposure to Chinese supply chains.

It is important to note, however, that participation in these multilateral frameworks does not constitute project-specific government endorsement or guaranteed offtake from allied governments. The commercial success of Eneabba will ultimately depend on Iluka's ability to convert the strategic demand narrative into binding, economically viable supply contracts with manufacturers who require separated rare earth oxides at the specification and volume the refinery is designed to produce.

Key Risks Investors and Industry Observers Should Monitor

Several risk vectors remain relevant to assessing Eneabba's probability of delivering against its strategic and commercial objectives:

- Further cost escalation beyond the A$1.8 billion upper boundary, particularly if construction timelines extend materially into 2027 or commissioning encounters technical challenges specific to the separation chemistry

- Rare earth price trajectory: the A$172 million upside revenue scenario under the confirmed offtake agreement is explicitly conditional on industry price forecasts holding. If dysprosium, terbium, or NdPr oxide prices decline substantially from current levels, revenue assumptions compress

- Offtake book concentration: with one confirmed customer representing 10% of planned production, Iluka remains heavily exposed to spot market conditions for the majority of its output until additional long-term agreements are secured

- Geopolitical normalisation risk: any diplomatic or commercial resolution that restores Chinese rare earth export flows to allied nations at competitive pricing could temporarily reduce the urgency premium that currently incentivises Western manufacturers to commit to higher-cost allied supply

- Technical commissioning risk: first-of-kind solvent extraction refineries have historically encountered unexpected process chemistry challenges during initial commissioning phases, which can extend ramp-up timelines and defer revenue recognition

This article contains forward-looking assessments based on publicly available information and general industry analysis. It does not constitute financial advice. Readers should conduct independent due diligence before making any investment decisions related to Iluka Resources or the rare earth sector.

What Success at Eneabba Would Structurally Change

If the Eneabba refinery commissions on schedule and ramps to designed production capacity, the implications extend well beyond Iluka's balance sheet. A successfully operating integrated rare earth refinery in Australia would validate the non-recourse sovereign loan model as a replicable template for financing other first-of-kind critical minerals processing facilities. Furthermore, it could serve as a model both domestically and in allied jurisdictions observing the Australian experiment.

It would also establish Australia as a genuine full value-chain participant in rare earths, capable of supplying separated oxide products directly to magnet manufacturers rather than exporting concentrate for offshore processing. This shift is directly tied to the growing critical minerals demand driving allied nations to seek alternatives to Chinese-controlled supply chains. Consequently, this is the primary strategic objective underpinning the A$1.65 billion Iluka rare earths refinery loan from Australia, and it is what makes the project's completion or failure consequential far beyond the individual company level.

The rare earth sector is entering a period where the infrastructure decisions made between 2024 and 2028 will define the supply landscape for the following decade. Eneabba is one of a small number of projects globally with the technical scope, sovereign financial backing, and geographic positioning to materially reshape that landscape. Whether it delivers on that potential will become clear as construction progresses toward the 2027 commissioning target.

Want To Stay Ahead of the Next Major ASX Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex mineral data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the broader market.