May 17, 2026

Strategic Materials Innovation Reshaping Global Competition

Within the rapidly evolving landscape of advanced materials manufacturing, China rare earth innovation polymer materials represents a fundamental shift in global supply chain dynamics. While traditional focus has centred on raw mineral extraction and primary processing capabilities, emerging technologies now demonstrate how integrated access to critical minerals and energy security can enable breakthrough innovations in high-performance polymer systems.

This transformation extends beyond conventional manufacturing paradigms, positioning China to capture significantly higher value margins through proprietary materials platforms rather than commodity-level production. Furthermore, the implications ripple across multiple industrial sectors, from automotive components to medical device manufacturing, where material performance specifications increasingly determine competitive positioning and market access opportunities. In addition, these developments highlight the importance of understanding critical minerals in semiconductors and their broader strategic implications.

When big ASX news breaks, our subscribers know first

Understanding China's Strategic Materials Innovation Framework

The integration of rare earth elements into polymer matrices represents a convergence of metallurgical expertise and advanced chemical engineering that addresses persistent challenges in materials performance. Unlike conventional polymer additives that rely on organic compounds or common metal-based stabilisers, rare earth-enhanced formulations leverage the unique electronic configurations and coordination chemistry of lanthanide elements to achieve superior thermal stability and flame resistance characteristics. This innovative approach connects directly with broader mining innovation trends shaping the industry.

What Makes Rare Earth-Enhanced Polymers a Game-Changing Technology?

Rare earth functional additives operate through fundamentally different mechanisms compared to traditional polymer enhancement approaches. The seventeen chemical elements comprising rare earth elements – fifteen lanthanides plus scandium and yttrium – possess distinctive electronic structures that enable multiple coordination bonds with polymer chains during thermal processing and service conditions.

Key Performance Advantages:

- Heat stabilisation systems extending polymer service life by 15-25% through coordinated metal-polymer interactions

- Composite flame retardants achieving UL 94 V-0 ratings without halogenated compounds, addressing environmental compliance requirements

- Enhanced thermal processing stability during manufacturing, reducing scrap rates and enabling higher processing temperatures

- Superior environmental stress-crack resistance for outdoor applications and harsh chemical environments

The technical breakthrough centres on three primary application categories that directly compete with imported specialty additives. However, rare earth heat stabilisers function by coordination chemistry mechanisms, stabilising polymer chains during thermal degradation and processing through free-radical scavenging and metal-ion stabilisation of polymer backbones.

Composite flame retardants leverage rare earth oxides' thermal absorption and char-formation properties, creating insulating barriers during combustion without releasing toxic halogenated byproducts that face increasing regulatory restrictions in European Union and other global markets. Consequently, environmental compliance advantages emerge from eliminating legacy additives that pose occupational health and environmental disposal challenges, particularly important for biomedical applications requiring ISO 10993 biocompatibility testing and FDA approval pathways.

Application Sectors Driving Market Demand

The most strategically significant applications target sectors where material performance directly impacts safety, regulatory compliance, and competitive positioning:

Biomedical Materials:

- Regulatory-sensitive applications requiring material purity and biocompatibility certification

- Sterilisation resistance for medical device manufacturing

- Long-term implant stability and tissue compatibility requirements

Electric Vehicle Cable Applications:

- Continuous operating temperatures ranging 80-130°C for automotive wire harnesses

- Flame resistance meeting UL 94 standards for passenger compartment safety

- Environmental stress-crack resistance for under-hood applications

High-Performance Composite Matrices:

- Aerospace component requirements for thermal cycling and mechanical durability

- Industrial equipment applications demanding chemical resistance and dimensional stability

China's Innovation Competition Ecosystem: National Technology Acceleration

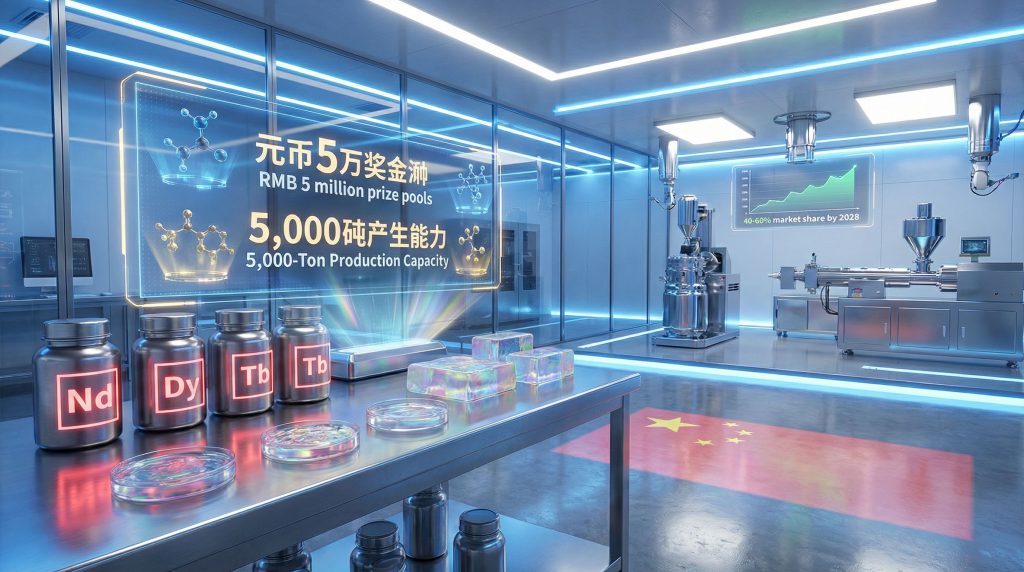

The China Innovation & Entrepreneurship Competition represents a sophisticated state-aligned innovation pipeline designed to identify scalable technologies and accelerate their commercialisation through integrated policy, financial, and market access support systems. This national-level competition uniquely integrates participants from mainland China, Hong Kong, Macao, and Taiwan regions, concentrating innovation resources across the Greater Bay Area development framework.

How China's Innovation Competitions Drive Commercial Breakthroughs

The 14th competition cycle attracted 891 national entries competing across five strategic industry tracks: artificial intelligence and embodied intelligence, life and health technologies, new materials and energy systems, cultural creativity and sports technology, and financial technology applications.

Competition Structure and Support Mechanisms:

| Support Category | Implementation | Strategic Benefit |

|---|---|---|

| Prize Pool | RMB 5 million ($690,000-$705,000) | Direct funding for scaling |

| High-Tech Enterprise Status | 15% corporate tax reduction | Operating cost advantages |

| "Little Giant" Designation | Government procurement access | Market demand creation |

| National Industrial Funds | State-backed venture capital | Growth capital availability |

| Policy Bank Credit | Development Bank financing | Low-cost expansion funding |

The post-award ecosystem provides multiple pathways for technology scaling that extend far beyond initial prize funding. For instance, high-tech enterprise designation reduces corporate tax rates from standard levels to 15% over three-year periods while providing VAT incentives and R&D expense deductions.

Specialised and sophisticated enterprise classifications, known as "little giant" designations, create preferential access to government procurement contracts and priority financing from policy banks including the Development Bank of China and Agriculture Development Bank. These developments significantly impact critical raw materials supply chains globally.

Integration Across Greater Bay Area Development

The competition's regional integration strategy aligns with broader Chinese policy objectives for cross-strait economic coordination and Greater Bay Area development initiatives. This framework enables technology transfer and manufacturing scale-up across complementary regional capabilities, from Hong Kong's financial services infrastructure to mainland China's manufacturing capacity.

Regional Coordination Benefits:

- Access to Hong Kong capital markets for international expansion funding

- Integration with Macao's specialised service sectors for regulatory navigation

- Taiwan technology collaboration within controlled policy frameworks

- Mainland manufacturing infrastructure for large-scale production deployment

Technical Innovation Analysis: Ruihong's Polymer Materials Platform

Ruihong Company's recognition as a top prize winner in the disruptive technology track demonstrates the commercial viability of rare earth polymer integration at industrial scale. The company operates a 5,000-ton-per-year pilot production line for rare earth functional additives, providing a clear bridge from laboratory innovation to manufacturing scale-up.

What Specific Breakthroughs Enable Commercial Scaling?

The technical achievements that distinguish Ruihong's approach from conventional polymer additive technologies centre on three core innovation areas that directly address import substitution priorities and environmental compliance requirements. Moreover, these advances reflect broader China rare earth innovation polymer materials developments.

Rare Earth Heat Stabiliser Systems:

These formulations replace imported thermal stabilisers through coordination chemistry mechanisms that outperform traditional organotin and metal soap stabilisers. The rare earth coordination complexes provide enhanced thermal protection during polymer processing and end-use service conditions, extending product life cycles and reducing replacement frequency.

Composite Flame Retardant Platforms:

The breakthrough involves rare earth oxide integration that achieves superior flame resistance without halogenated compounds increasingly restricted under environmental regulations. This technology enables manufacturers to meet stringent safety standards while eliminating toxic combustion byproducts that complicate disposal and recycling operations.

Environmental Compliance Integration:

By eliminating dependence on legacy additives that pose occupational health risks and environmental disposal challenges, these formulations support China's dual-carbon strategy objectives and plastic pollution mitigation goals while creating competitive advantages in environmentally sensitive markets.

How 5,000-Ton Production Capacity Signals Market Readiness

The operational pilot-scale production line demonstrates manufacturing process validation and quality control capabilities necessary for commercial market entry. This capacity level indicates transition from laboratory development to industrial production, addressing customer requirements for supply reliability and technical support.

Production Scale Implications:

- Pilot-scale validation: Demonstrates manufacturing process control and quality assurance systems

- Customer qualification: Enables material testing and certification by downstream manufacturers

- Regulatory pathway: Supports documentation for safety and environmental compliance approvals

- Market positioning: Creates competitive supply alternative to imported specialty additives

The expansion plans targeting biomedical materials and electric vehicle cable applications represent strategically selected market segments where performance specifications create high barriers to entry and command premium pricing structures.

Global Competitive Implications: Western Response Scenarios

The emergence of Chinese rare earth polymer capabilities creates multiple strategic challenges for Western specialty chemical suppliers, automotive manufacturers, and advanced materials companies that have historically dominated high-performance additive markets through proprietary formulations and regulatory certifications. Furthermore, these developments occur against the backdrop of ongoing US–China trade impacts affecting global supply chains.

What Strategic Vulnerabilities Does This Create for Western Manufacturers?

Supply Chain Dependency Risks:

Western polymer manufacturers currently rely on established suppliers including Clariant, BASF, and Dow Chemical for specialty additives that command premium pricing due to technical performance and regulatory certification rather than material availability constraints.

Chinese rare earth polymer integration threatens this market structure by combining raw material access advantages with formulation capabilities, potentially creating cost and performance advantages that existing suppliers cannot match without securing alternative rare earth sources.

Technology Transfer Limitations:

Traditional approaches to managing strategic technology competition through export controls and investment restrictions become less effective when competing nations develop alternative technical pathways using different raw material inputs and processing approaches.

The rare earth polymer breakthrough demonstrates how material abundance can enable entirely different technological solutions that bypass Western intellectual property positions and regulatory frameworks designed around conventional additive chemistries. This development has been highlighted in research on China's advancing downstream rare earth innovation.

Market Bifurcation Scenarios

Scenario 1: Accelerated Chinese Market Capture

- Domestic Chinese polymer producers gain cost and performance advantages through integrated rare earth access

- Western specialty chemical suppliers face margin compression and market share erosion

- Technology transfer restrictions prove ineffective against indigenous innovation pathways

- Chinese manufacturers expand export capabilities in finished polymer products

Scenario 2: Supply Chain Bifurcation

- Parallel materials ecosystems develop with Chinese and Western technical standards

- Higher costs for non-Chinese manufacturers unable to access rare earth polymer technologies

- Innovation gaps widen favouring integrated rare earth access and processing capabilities

- Global markets fragment along technology availability and regulatory framework boundaries

Strategic Response Framework for Western Industries

The development of Chinese rare earth polymer capabilities requires coordinated responses across multiple dimensions of technology development, supply chain diversification, and policy frameworks to maintain competitive positioning in advanced materials markets. Consequently, understanding China rare earth innovation polymer materials becomes critical for strategic planning.

How Should Western Polymer and Automotive Industries Respond?

Technology Development Priorities:

Western manufacturers must accelerate research and development programmes focused on alternative material approaches that achieve comparable performance without rare earth element dependencies. This includes investigation of organic polymer stabilisation systems, bio-based additives, and novel synthetic approaches to flame resistance and thermal stability.

Supply Diversification Strategies:

| Response Type | Implementation Timeline | Risk Mitigation Focus |

|---|---|---|

| Alternative material R&D | 3-5 years | Technology substitution |

| Supply diversification | 1-2 years | Vendor risk reduction |

| Joint venture partnerships | 2-3 years | Market access preservation |

| Strategic stockpiling | 6-12 months | Supply continuity assurance |

Strategic Partnership Considerations:

Joint ventures with non-Chinese rare earth processors and specialty chemical companies may provide pathways to competitive materials platforms while maintaining technology control and intellectual property protection. These partnerships could focus on alternative rare earth sources from Australia, Canada, and other Western-aligned suppliers combined with specialised processing capabilities developed through collaborative research and development programmes.

Investment Strategy Implications

The shift toward downstream rare earth processing fundamentally alters investment thesis frameworks for critical materials sectors, moving emphasis from mining-focused strategies toward integrated processing and technology development capabilities. Research indicates that global rare earth supply chains are at an inflection point, highlighting the importance of strategic positioning.

Investment Priority Reallocation:

- Traditional mining investments: Face limitations due to downstream processing bottlenecks and technology integration requirements

- Specialty chemical capabilities: Become increasingly critical for maintaining competitive positioning in advanced materials markets

- Technology development partnerships: Enable access to alternative technical pathways and diversified supply relationships

- Regulatory compliance systems: Support market access and competitive positioning in environmentally sensitive applications

The next major ASX story will hit our subscribers first

Policy Framework and Regulatory Response Considerations

The emergence of Chinese rare earth polymer capabilities presents challenges for Western industrial policy frameworks designed around traditional concepts of strategic materials control and technology competition management.

How Will This Influence Western Industrial Policy?

Critical Materials Stockpiling Frameworks:

Traditional approaches to strategic materials management focus on raw material stockpiling rather than processed materials and finished products that incorporate critical materials into high-value applications. The rare earth polymer breakthrough suggests policy frameworks must expand to address downstream processing capabilities and finished product dependencies, requiring more sophisticated analysis of supply chain vulnerabilities and strategic response options.

Research Funding Prioritisation:

Government research and development funding programmes must adapt to address alternative technical pathways that reduce dependence on Chinese rare earth processing capabilities while maintaining performance specifications required for advanced applications.

Trade Policy Adaptations:

Existing trade policy frameworks designed around raw material exports and finished product imports may require adjustment to address integrated materials platforms that combine critical material access with proprietary processing technologies.

Regulatory Compliance and Market Access

The development of Chinese rare earth polymer capabilities creates opportunities for regulatory framework development that supports Western technology alternatives while maintaining performance and safety standards.

Environmental Compliance Advantages:

Chinese rare earth polymer formulations that eliminate halogenated flame retardants and toxic stabilisers may create competitive advantages in markets with stringent environmental regulations, requiring Western alternatives to match both performance and environmental compliance characteristics.

Safety Certification Pathways:

Established safety certification systems for biomedical applications, automotive components, and aerospace materials provide opportunities to maintain competitive positioning through regulatory requirements and testing protocols that favour established Western suppliers.

Future Market Scenarios: 2026-2030 Projections

The trajectory of Chinese rare earth polymer development will significantly influence global materials markets across multiple industrial sectors, with outcomes dependent on Western response effectiveness and Chinese commercialisation success rates. In addition, developments in China rare earth innovation polymer materials will continue shaping competitive dynamics.

Market Share Evolution Projections

Baseline Scenario: Measured Chinese Expansion

Chinese rare earth polymer technologies achieve 25-35% market penetration in specialised additive segments by 2028, primarily through domestic market capture and selective export market development. Western manufacturers maintain majority market positions through alternative technology development and established customer relationships, though operating margins face pressure from Chinese cost competition.

Accelerated Scenario: Rapid Chinese Dominance

Chinese manufacturers capture 40-60% market share in specialised polymer additives by 2028 through successful commercial scaling and aggressive export expansion. Western specialty chemical suppliers face significant margin compression and market share erosion, with limited ability to compete on cost while maintaining performance specifications.

Competitive Response Scenario: Technology Bifurcation

Western alternative technologies achieve commercial viability, creating parallel supply chains with different technical approaches and performance characteristics. Market bifurcation develops along technological and geographic lines, with higher costs but maintained technological independence for Western manufacturers.

Investment Flow Implications

Capital Allocation Shifts:

Investment flows within critical materials sectors will increasingly favour integrated processing capabilities over pure-play mining operations, reflecting the higher value creation potential of downstream applications.

Geographic Concentration Effects:

Chinese government support for rare earth polymer development may accelerate capital formation in Greater Bay Area manufacturing clusters, creating concentrated expertise and supply chain integration that becomes difficult for competitors to replicate.

Technology Development Competition:

Research and development spending competition between Chinese state-supported programmes and Western private sector initiatives will intensify, with outcomes dependent on sustained funding commitment and technical execution capabilities.

Strategic Recommendations for Industry Stakeholders

The emergence of Chinese rare earth polymer capabilities requires coordinated responses across technology development, supply chain management, and policy engagement to maintain competitive positioning and market access in advanced materials sectors.

For Western Polymer Manufacturers

Immediate Actions (6-12 months):

- Conduct comprehensive supply chain vulnerability assessment focused on specialty additive dependencies

- Establish alternative supplier relationships for critical polymer additives outside Chinese supply chains

- Initiate strategic materials stockpiling for essential specialty chemicals with long lead times

Medium-term Development (1-3 years):

- Accelerate research and development programmes for non-rare earth polymer enhancement technologies

- Establish joint ventures with Western rare earth processors and specialty chemical manufacturers

- Develop regulatory compliance pathways for alternative additive technologies in key markets

Long-term Positioning (3-5 years):

- Create integrated alternative technology platforms competitive with Chinese rare earth polymer systems

- Establish geographic supply chain diversification across multiple Western-aligned countries

- Build customer relationship depth through technical support and application development services

For Investors and Fund Managers

Investment Thesis Rebalancing:

Traditional rare earth investment approaches focused on mining operations face limitations as value creation shifts toward downstream processing and application integration capabilities. Investment strategies should emphasise integrated processing capabilities, proprietary technology development, and supply chain control rather than pure commodity exposure to rare earth pricing volatility.

Due Diligence Framework Enhancement:

- Technology differentiation assessment: Evaluate proprietary capabilities versus commodity material dependencies

- Supply chain resilience analysis: Map vulnerability to Chinese processing capabilities and alternative pathway availability

- Regulatory positioning evaluation: Assess competitive advantages through environmental compliance and safety certification capabilities

- Market access sustainability: Determine long-term defensibility of market position against integrated Chinese competitors

For Policymakers

Strategic Research Investment:

Government research funding programmes should prioritise alternative material technologies that reduce Western industrial dependence on Chinese rare earth processing capabilities while maintaining performance requirements for critical applications.

Regulatory Framework Development:

Environmental and safety regulations should support Western alternative technologies through performance-based standards rather than prescriptive requirements that may favour specific material approaches or supply relationships.

International Coordination:

Multilateral cooperation frameworks among Western-aligned countries should address critical materials supply chain resilience through coordinated research and development programmes, strategic stockpiling initiatives, and alternative supplier development.

Key Performance Indicators for Market Evolution

Monitoring the progression of Chinese rare earth polymer capabilities and Western competitive responses requires tracking specific metrics across technology development, market penetration, and policy implementation dimensions.

Technology Development Metrics

Patent Filing Analysis:

- Geographic distribution of rare earth polymer patent applications (Chinese versus Western entities)

- Technical sophistication progression in patent disclosures over time

- Alternative technology patent development by Western manufacturers and research institutions

Commercial Production Capacity:

- Chinese rare earth polymer production capacity expansion announcements and timeline execution

- Western alternative technology pilot plant developments and scaling commitments

- Manufacturing process improvement indicators through cost reduction and quality enhancement metrics

Market Penetration Indicators

Supply Chain Integration Tracking:

- Chinese domestic market share capture in specialty polymer additive segments

- Export growth rates for Chinese rare earth-enhanced polymer products

- Western manufacturer sourcing pattern changes and supplier relationship modifications

Pricing and Margin Analysis:

- Specialty polymer additive pricing trends comparing Chinese versus Western suppliers

- Operating margin pressure indicators for established Western specialty chemical companies

- Cost competitiveness evolution between rare earth-based and alternative additive technologies

Policy Response Measures

Government Support Quantification:

- Research and development funding allocations for alternative materials technologies by Western governments

- Strategic stockpiling programme implementations and inventory level commitments

- Trade policy adjustment announcements and technology transfer restriction modifications

International Cooperation Development:

- Strategic partnership announcements between Western companies and non-Chinese rare earth processors

- Multilateral government cooperation agreements on critical materials supply chain resilience

- Joint research and development programme establishments and funding commitment levels

This analysis is based on publicly available information and industry developments. Market projections and strategic scenarios involve uncertainties and should be independently verified for business planning purposes. Investment decisions should consider multiple risk factors and professional advisory guidance.

Looking to Gain an Edge in Next-Generation Materials Investments?

Discovery Alert's proprietary Discovery IQ model instantly identifies breakthrough materials discoveries across the ASX, turning complex mineral developments into actionable investment insights before they hit mainstream markets. With major materials innovations reshaping global supply chains, understanding which ASX mineral discoveries have historically delivered exceptional returns could position you ahead of this evolving sector. Begin your 30-day free trial today to access real-time alerts on the next wave of strategic materials opportunities.