May 12, 2026

Understanding China's Strategic Framework for Critical Materials Control

The global technology landscape increasingly depends on a handful of critical materials that power everything from smartphone screens to wind turbines. Among these materials, rare earth elements occupy a uniquely strategic position, with applications spanning clean energy infrastructure, defense systems, and consumer electronics. China's dominance in rare earth processing and refining has created structural dependencies that extend far beyond simple commodity trading relationships.

Recent developments in China's export licensing framework represent a fundamental shift in how Beijing manages its most strategically valuable resources. Rather than relying on transparent quota systems or market-based allocation mechanisms, Chinese authorities have implemented a sophisticated regulatory apparatus that provides maximum policy flexibility while maintaining information asymmetries with international buyers.

The Ministry of Commerce's (MOFCOM) approval of general export licenses for select rare earth exporters marks not market liberalization, but rather the institutionalization of selective access controls. This regulatory evolution transforms China rare earth export licenses from a commercial activity into a carefully managed strategic asset, with profound implications for global supply chain resilience.

When big ASX news breaks, our subscribers know first

China's Regulatory Architecture for Export Control

Historical Evolution from Market Access to Strategic Governance

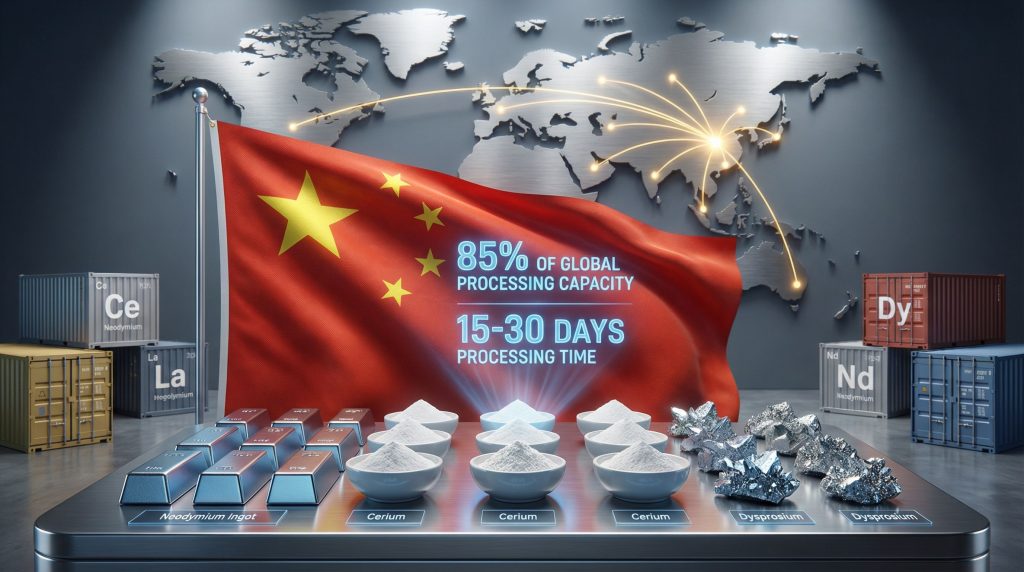

China's approach to rare earth export management has undergone significant transformation over the past fifteen years. Initially operating under relatively open market conditions, Beijing gradually recognised the strategic leverage inherent in controlling approximately 85% of global rare earth separation and processing capacity. This dominance extends beyond raw material extraction to encompass the sophisticated technical processes required to transform rare earth ores into the high-purity compounds essential for advanced manufacturing.

The regulatory framework governing China rare earth export licenses represents the culmination of this strategic evolution. Following World Trade Organization rulings against explicit export quotas in 2015, Chinese authorities developed increasingly sophisticated administrative mechanisms to maintain supply chain control while avoiding direct violations of international trade law. The current licensing system exemplifies this approach, providing regulatory flexibility without the transparency requirements associated with traditional quota systems.

MOFCOM's expanded authority encompasses not only raw material exports but also technology transfer controls, equipment restrictions, and downstream manufacturing oversight. This comprehensive approach ensures that Chinese regulatory influence extends throughout the entire rare earth value chain, from mining operations to final product assembly.

Key Regulatory Bodies and Administrative Mechanisms

The institutional architecture supporting China's export licensing framework involves multiple government agencies operating under coordinated policy directives. MOFCOM serves as the primary licensing authority, but its decisions reflect input from the Ministry of Industry and Information Technology, the National Development and Reform Commission, and relevant military-industrial oversight bodies.

Export license applications undergo multi-tier review processes that evaluate not only commercial considerations but also strategic implications for China's national interests. This evaluation framework considers factors including:

- Corporate ownership structure and foreign investment exposure

- End-use applications and potential dual-use implications

- Destination countries and their strategic relationships with China

- Re-export risks and downstream supply chain vulnerabilities

- Technology transfer implications associated with processing techniques

The regulatory framework deliberately maintains information asymmetries that complicate strategic planning for international manufacturers. Unlike traditional trade mechanisms that provide transparent pricing and allocation signals, China rare earth export licenses operate through discretionary administrative processes with limited external visibility.

Operational Structure of the Two-Tier Access System

Preferential Pathways for State-Aligned Enterprises

The emerging two-tier structure for China rare earth export licenses creates distinct advantages for enterprises demonstrating alignment with Chinese strategic priorities. Large-scale processors with established compliance records and state ownership connections receive general export licenses that provide relative predictability in export operations. These licenses typically process within 15-30 days and offer renewable terms that enable longer-term supply planning.

State-owned enterprises such as China Northern Rare Earth Group and China Rare Earth Holdings Group benefit from institutional relationships that facilitate regulatory approval processes. Their integrated operations, spanning from mining through final product manufacturing, align with Beijing's preference for consolidated industry structure under national oversight.

The criteria for obtaining preferential license treatment include:

- Demonstrated compliance history spanning multiple years of operations

- Consistent adherence to environmental and safety regulations

- Absence of sanctions violations or unauthorised technology transfers

- Integration with state industrial development priorities

- Capacity for supply chain monitoring and end-use verification

| License Category | Processing Timeline | Renewal Frequency | Compliance Requirements |

|---|---|---|---|

| General Export | 15-30 days | Annual | Standard documentation |

| Enhanced Review | 45-90 days | Case-by-case | Additional verification |

| Restricted Access | Indefinite | N/A | National security clearance |

Conditional Access for Non-Preferred Entities

Smaller processors, foreign-owned enterprises, and companies lacking established relationships with Chinese authorities face significantly different treatment under the licensing framework. These entities must navigate case-by-case approval processes that introduce substantial uncertainty into supply planning and contract negotiations.

The conditional access tier reflects deliberate policy design intended to maintain Chinese leverage over international supply chains. By creating information asymmetries and processing delays for non-preferred entities, the licensing system functions as a subtle but effective means of directing market behaviour without explicit coercion.

Foreign manufacturers dependent on Chinese rare earth supplies frequently encounter:

- Extended approval timelines ranging from 45-90 days or longer

- Enhanced documentation requirements including end-use certifications

- Volume limitations that may not align with production planning needs

- Revocation risks based on changing political or strategic considerations

- Limited transparency regarding approval criteria and decision processes

These structural uncertainties force international manufacturers to maintain higher inventory levels, develop alternative sourcing strategies, and accept elevated supply chain costs. The cumulative effect creates competitive advantages for Chinese manufacturers while imposing additional burdens on international competitors.

Scope and Coverage of Export Controls

Material Categories Under Regulatory Oversight

The comprehensive scope of China rare earth export licenses extends across multiple categories of materials and processing stages. Light Rare Earth Elements (LREEs) including cerium, lanthanum, and neodymium face licensing requirements alongside Heavy Rare Earth Elements (HREEs) such as dysprosium, terbium, and yttrium. This coverage encompasses both raw concentrates and highly processed compounds essential for advanced manufacturing applications.

Light Rare Earth Elements dominate global production volumes but typically command lower market prices due to relatively abundant supply. However, their essential role in catalytic converters, battery systems, and optical applications creates significant strategic dependencies for manufacturing sectors worldwide. Cerium alone represents approximately 30% of total rare earth demand, primarily through automotive and industrial catalyst applications.

Heavy Rare Earth Elements constitute a smaller portion of total production volumes but carry disproportionate strategic importance due to their critical applications in defense systems, precision manufacturing, and advanced energy technologies. Dysprosium's role in high-temperature permanent magnets makes it essential for military applications, while terbium's unique properties enable advanced fluorescent lighting and medical imaging systems.

The licensing framework specifically addresses:

- Raw rare earth concentrates (2-10% rare earth element content)

- Separated oxides with 99%+ purity levels

- Magnetic alloys and sintered permanent magnet materials

- Specialised compounds for optical and electronic applications

- Manufacturing equipment and processing technology

Volume Controls and Geographic Targeting

Unlike the transparent quota systems previously employed by China, current volume limitations under China rare earth export licenses remain deliberately opaque. MOFCOM does not publish quarterly or annual allocation targets, creating persistent uncertainty for supply chain planning across dependent industries.

Industry analysis suggests current effective export volumes approximate 120,000-150,000 metric tons annually across all rare earth categories, but these figures reflect market estimates rather than official policy statements. The absence of transparent allocation mechanisms enables Chinese authorities to adjust export levels rapidly in response to changing strategic priorities or international political developments.

Geographic targeting appears to influence license approval processes, though specific destination preferences remain undisclosed. Analysis of trade flows suggests preferential treatment for:

- ASEAN member states participating in Belt and Road Initiative programs

- Countries maintaining neutral positions on China-U.S. strategic competition

- Trading partners with limited involvement in technology restrictions targeting China

Conversely, entities with connections to sanctioned countries, defense contractors in adversarial nations, or companies participating in semiconductor restrictions may face extended approval delays or license denials. These targeting mechanisms operate through administrative discretion rather than published policy guidelines.

Export Controls as Economic Statecraft Tools

Administrative Flexibility Beyond Traditional Trade Measures

China rare earth export licenses represent a sophisticated evolution in economic statecraft that provides policy flexibility unavailable through conventional trade mechanisms. Unlike tariffs, quotas, or sanctions that operate through transparent legal frameworks, licensing systems enable rapid policy adjustments while maintaining plausible commercial justification for regulatory decisions.

This administrative approach offers several strategic advantages:

- Selective targeting of specific companies, industries, or countries without broad policy announcements

- Rapid adjustment capability enabling responses to changing geopolitical circumstances

- Information asymmetry maintenance that complicates strategic planning for potential adversaries

- Escalation control through graduated access restrictions rather than binary on/off mechanisms

Furthermore, this European CRM facility approach has prompted international responses to address supply vulnerabilities. The licensing framework functions as what policy analysts term a "gray zone" economic tool, operating below the threshold of explicit economic warfare while providing substantial leverage over international supply chains.

Market Psychology and Signaling Effects

Beyond direct supply impacts, China rare earth export licenses generate significant market psychology effects that amplify Chinese strategic influence. The opacity of approval processes creates persistent uncertainty that influences investment decisions, contract negotiations, and strategic planning across dependent industries.

International manufacturers frequently adjust business strategies based on perceived rather than actual supply restrictions. This anticipatory behaviour multiplies the effectiveness of Chinese export controls, as companies self-impose restrictions or strategic adjustments to avoid potential future supply disruptions.

The psychological impact of supply uncertainty often exceeds the direct material effects, as companies modify long-term strategies to address perceived rather than realised risks in critical material access.

Market signalling through licensing policy announcements enables Chinese authorities to communicate strategic intentions without explicit diplomatic statements. Selective approval or denial patterns send clear messages regarding acceptable international behaviour while maintaining commercial justifications for regulatory decisions.

Supply Chain Implications for International Manufacturing

Risk Assessment Across Dependent Industries

The structural implications of China rare earth export licenses extend across multiple manufacturing sectors with varying degrees of strategic importance and supply chain vulnerability. Automotive manufacturers face particular exposure through electric vehicle battery systems and permanent magnet motor applications that require consistent access to neodymium, dysprosium, and other critical elements.

Renewable energy infrastructure development depends heavily on rare earth-based permanent magnets for wind turbine generators. A single 3-megawatt wind turbine requires approximately 600 kilograms of neodymium-based magnetic materials, creating substantial aggregate demand across expanding renewable energy installations worldwide. This demand directly impacts energy transition security across developed nations.

Defense contractors encounter the highest strategic sensitivity regarding rare earth access, as military systems frequently incorporate precision components requiring high-performance magnetic materials. Advanced radar systems, precision-guided munitions, and electronic warfare equipment depend on rare earth elements with no readily available substitutes.

Key vulnerability factors include:

- Concentration risk from single-country sourcing dependencies

- Processing bottlenecks requiring Chinese technical expertise

- Quality specifications that limit alternative supplier options

- Long-term contracts exposed to regulatory approval uncertainties

- Inventory costs associated with supply chain buffer requirements

Supply Chain Adaptation Strategies

International manufacturers have implemented various adaptation strategies to address uncertainties associated with China rare earth export licenses. Inventory optimisation approaches involve maintaining 90-180 day supply buffers to accommodate potential licensing delays, though this strategy imposes significant working capital requirements and storage costs.

Supplier diversification efforts have accelerated development of alternative rare earth processing capabilities in Australia, Canada, and several African nations. However, establishing competitive separation and refining capabilities requires substantial technical expertise and capital investment over multi-year development timelines. Additionally, developments in Australia's minerals reserve provide potential alternatives for international buyers.

Strategic partnerships with Chinese state-owned enterprises offer some manufacturers preferential access to licensed exports through joint venture arrangements or long-term supply agreements. These partnerships provide supply security but may impose technology transfer requirements or other strategic concessions.

Alternative material research has gained increased investment focus, though breakthrough developments require extended development timelines and substantial uncertainty regarding performance characteristics. Recycling and urban mining initiatives offer partial supply diversification but cannot address primary demand growth in expanding technology applications.

| Adaptation Strategy | Implementation Timeline | Cost Impact | Risk Reduction |

|---|---|---|---|

| Strategic inventory | 6-12 months | Medium | Low-Medium |

| Supplier diversification | 2-5 years | High | Medium-High |

| Alternative materials | 5-10 years | Very High | High |

| Recycling programs | 1-3 years | Medium | Low-Medium |

The next major ASX story will hit our subscribers first

Historical Context and Precedent Analysis

Lessons from Previous Resource Control Episodes

China's current approach to rare earth export controls draws inspiration from historical precedents in strategic resource management while incorporating lessons learned from previous international responses. The 1973 oil embargo implemented by OPEC demonstrated the economic leverage available through coordinated supply restrictions, though it also accelerated development of alternative energy sources and strategic petroleum reserves.

Japan's semiconductor material restrictions in the 1980s provided a more relevant model for China's current approach, as Japanese authorities used administrative mechanisms to control access to critical manufacturing inputs without explicit trade policy announcements. These controls contributed to Japanese competitive advantages in electronics manufacturing while spurring alternative technology development in targeted countries.

Consequently, these historical examples demonstrate how resource controls can drive mining industry evolution and technological innovation. The Soviet Union's strategic material policies during the Cold War demonstrated both the potential and limitations of resource-based economic statecraft. While successful in creating short-term leverage, these policies ultimately accelerated Western efforts to develop alternative supply sources and reduce strategic dependencies.

China's Unique Strategic Position

China's position in rare earth markets differs significantly from these historical precedents due to several unique factors:

- Vertical integration spanning from mining through final product manufacturing

- Technical expertise in separation and purification processes requiring decades to replicate

- Scale advantages creating substantial cost barriers for alternative suppliers

- Market timing coinciding with rapid expansion in clean energy and technology applications

Unlike previous resource control episodes that focused primarily on raw material access, China's approach encompasses the entire rare earth value chain including processing technology, manufacturing equipment, and technical expertise. This comprehensive approach creates more durable competitive advantages while complicating international efforts to develop alternative supply sources.

The integration of China rare earth export licenses with broader technology transfer policies and industrial development strategies represents a more sophisticated approach to economic statecraft than previous resource control episodes. Rather than using material restrictions purely as economic weapons, Chinese authorities employ export controls as tools for advancing long-term strategic objectives including technology acquisition, industrial development, and geopolitical influence.

What Are the Geopolitical Implications?

Strategic Competition and Alliance Formation

The implementation of China rare earth export licenses has accelerated strategic competition dynamics between major powers, particularly affecting US-China trade impact relationships. The United States, European Union, and allied nations have responded by developing coordinated policies aimed at reducing critical mineral dependencies and building alternative supply chains.

In response to China's licensing controls, the Biden administration has accelerated efforts to rebuild domestic rare earth processing capabilities through the Defense Production Act and strategic partnerships with allied nations. Similarly, the European Union's Critical Raw Materials Act establishes targets for domestic processing capabilities and strategic partnerships with resource-rich countries outside China's sphere of influence.

The licensing system has also influenced alliance structures, as countries recognise the strategic vulnerability inherent in critical material dependencies. Recent agreements between Australia, Canada, and the United States demonstrate growing cooperation on critical minerals development, while Japan and South Korea have expanded their rare earth recycling programs and alternative sourcing initiatives.

Regional Supply Chain Reconfiguration

However, the geopolitical implications extend beyond bilateral relationships to encompass regional supply chain restructuring. Southeast Asian nations find themselves positioned between competing strategic pressures, as Chinese investment in regional rare earth processing capabilities offers economic opportunities while potentially creating new dependencies.

The establishment of rare earth processing facilities in Malaysia, Vietnam, and other ASEAN nations reflects Chinese efforts to maintain supply chain control while diversifying processing locations. These investments provide technology transfer and economic development benefits but may also extend Chinese regulatory influence through joint venture requirements and technology licensing agreements.

For instance, Reuters reports that China has confirmed granting some rare earth export licences, indicating ongoing policy adjustments within the framework. Nonetheless, the strategic implications of these regional investments remain complex, as host countries must balance economic benefits against strategic autonomy considerations.

Future Policy Evolution and Investment Implications

How Will Regulatory Frameworks Develop?

The trajectory of China rare earth export licenses will likely reflect broader geopolitical dynamics and technological development trends over the coming decade. Tightening scenarios could involve expanded controls covering downstream applications, technology transfer restrictions, and enhanced end-use monitoring requirements that extend Chinese regulatory influence further into international supply chains.

Selective liberalisation represents an alternative pathway where Chinese authorities might provide enhanced access to strategic partners while maintaining restrictions on adversarial nations. This approach would deepen economic relationships with preferred countries while using export controls as diplomatic leverage in multilateral negotiations.

Technology-focused evolution could shift emphasis from raw material controls toward restrictions on advanced manufacturing capabilities, processing equipment, and technical expertise. This approach would maintain Chinese competitive advantages in high-value applications while potentially relaxing controls on basic rare earth compounds.

Factors influencing future policy direction include:

- International development of alternative rare earth processing capabilities

- Evolution of U.S.-China strategic competition and alliance structures

- Technological breakthroughs in alternative materials or recycling processes

- Global demand patterns for clean energy and defense applications

- Chinese domestic industrial development priorities and capacity utilisation

Strategic Investment Considerations

The structural uncertainties associated with China rare earth export licenses create both risks and opportunities across various investment categories. Upstream mining projects outside China command strategic premiums due to supply diversification value, though these projects face substantial technical and capital requirements for competitive development.

Midstream processing capacity development in allied nations represents potentially high-return investments given current supply chain vulnerabilities, but requires significant technology transfer agreements and multi-year construction timelines. Government support programs in the United States, Europe, and allied nations provide risk mitigation for these capital-intensive projects.

Alternative material research and recycling technology development offer long-term growth potential as industries seek to reduce rare earth dependencies. However, these investments carry substantial technical risk and uncertain commercialisation timelines that may not address near-term supply security concerns.

Strategic Partnership Opportunities:

- Joint ventures with approved Chinese exporters

- Technology licensing agreements for processing capabilities

- Long-term supply contracts with volume guarantees

- Rare earth recycling and urban mining development

- Alternative material research and development programs

Risk Management and Supply Chain Resilience

Operational Risk Assessment Framework

Organisations dependent on rare earth supplies must implement comprehensive risk assessment frameworks that account for the multiple uncertainty factors introduced by China rare earth export licenses. Regulatory risk represents the primary concern, as licensing decisions remain subject to administrative discretion rather than transparent policy guidelines.

Supply continuity risks extend beyond simple availability concerns to encompass quality consistency, delivery scheduling, and contract terms that may change based on evolving licensing requirements. Companies must evaluate their exposure across multiple dimensions including volume requirements, material specifications, and alternative sourcing capabilities.

Financial risk management becomes critical given the potential for rapid price movements associated with supply uncertainty or policy announcements. Hedging strategies may include physical inventory buffers, financial derivatives where available, and diversified supplier relationships that provide pricing flexibility.

Essential risk evaluation criteria include:

- Criticality assessment of rare earth inputs to core business operations

- Substitution analysis evaluating alternative materials and suppliers

- Inventory optimisation balancing carrying costs against supply security

- Contract structure incorporating force majeure and price adjustment mechanisms

- Geographic diversification reducing single-country dependency risks

Building Long-Term Supply Chain Resilience

Developing resilient rare earth supply chains requires multi-year strategic planning that addresses both immediate operational needs and long-term industry evolution. Supplier relationship diversification represents the most critical element, requiring active development of relationships with alternative processors and technology providers outside China.

Technology investment in recycling capabilities and alternative materials research provides potential long-term solutions to supply dependencies, though these approaches require sustained commitment and uncertain development timelines. Urban mining programs for rare earth recovery from electronic waste offer promising near-term opportunities for supply augmentation.

Furthermore, strategic partnerships with allied nations and companies can provide enhanced supply security through coordinated development programs and mutual support arrangements. Government-industry collaboration programs in the United States, Europe, and allied nations offer risk-sharing mechanisms for strategic supply chain investments.

Moreover, specialised analysis from ECAG's Navigator Journal examines how China's critical minerals and rare earth export controls represent a new non-tariff battlefield in international trade.

Implementation Timeline for Resilience Building:

Phase 1 (0-12 months): Emergency preparedness through inventory optimisation and contract restructuring

Phase 2 (1-3 years): Supplier diversification and alternative sourcing development

Phase 3 (3-7 years): Technology development and alternative material implementation

Phase 4 (7+ years): Strategic supply chain transformation and reduced dependency

The evolution of China rare earth export licenses represents more than regulatory adjustment; it reflects fundamental changes in how critical materials function within international economic relationships. Understanding these dynamics becomes essential for navigating an increasingly complex landscape where commercial transactions intersect with strategic competition and technological advancement. Organisations that proactively address these challenges through comprehensive risk management and strategic adaptation will be best positioned to thrive in this transformed operating environment.

Looking to Invest in the Next Major Mineral Discovery?

Discovery Alert instantly alerts investors to significant ASX mineral discoveries using its proprietary Discovery IQ model, turning complex mineral data into actionable insights. Understand why historic discoveries can generate substantial returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, and begin your 30-day free trial today to position yourself ahead of the market.