August 1, 2026

China's rare earth processing dominance represents one of the most significant supply chain consolidations in modern industrial history. The global materials ecosystem faces unprecedented transformation as technological complexity intersects with geopolitical tensions. Modern industrial processes require sophisticated chemical separations, metallurgical precision, and integrated supply chains spanning multiple continents. Within this landscape, certain nations have developed comprehensive advantages that extend far beyond raw material extraction, fundamentally reshaping how critical technologies reach global markets.

What Makes Rare Earth Processing So Strategically Important?

The Hidden Complexity Behind Critical Materials

While many understand that rare earth elements power everything from electric vehicle motors to defense systems, the true strategic value lies not in mining these materials but in transforming them into commercially viable products. Furthermore, the critical minerals energy transition highlights the increasing importance of these processing capabilities for global energy security.

The separation chemistry required for rare earth processing involves mastery of hydrometallurgical techniques, including complex acid leaching systems, multi-stage solvent extraction, and precision precipitation chemistry. These processes demand expertise across metallurgical engineering, applied chemistry, and advanced analytical techniques including chromatography and spectrometry protocols.

According to research published in Processes journal, materials science has emerged as the central hub of rare earth research with a Cross-Disciplinary Publication Index (CDPI) of 0.81, indicating exceptionally tight integration across geology, chemistry, and metallurgy. This integration creates technical barriers that extend far beyond simple extraction capacity.

Processing margins fundamentally determine supply chain control because refined rare earth products command substantially higher prices than raw concentrates. The economic moat emerges from the combination of:

• Technical know-how in proprietary separation processes

• Scale economies in specialised equipment manufacturing

• Control of supply chains for intermediate chemical inputs

• Regulatory and environmental compliance systems optimised for specific geographic and cost structures

Beyond Mining: Where Real Market Power Lies

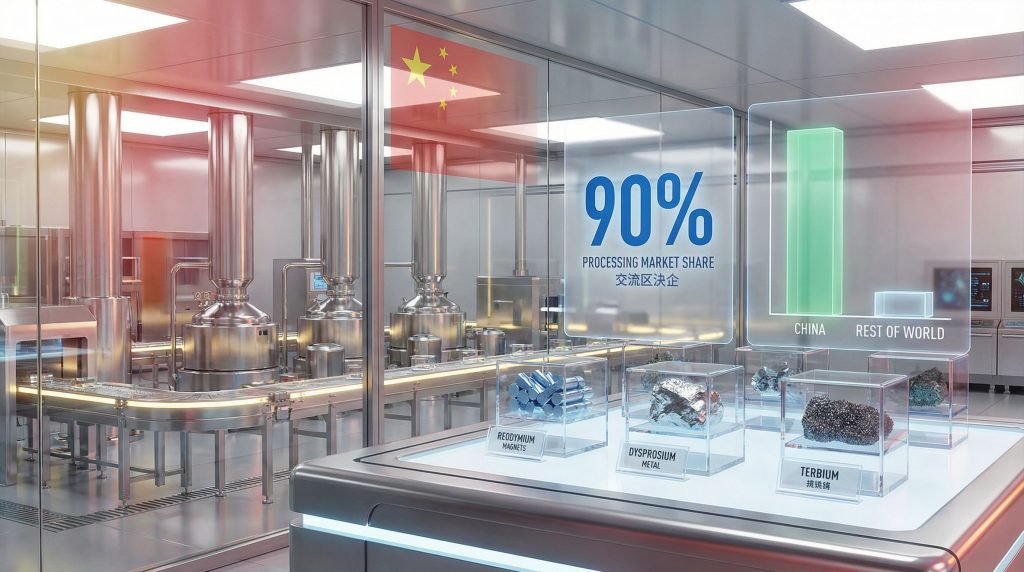

The value differential between extraction and processing becomes clear when examining global market shares. China controls approximately 69-70% of global rare earth mining but commands 90% of processing capacity and 99% of heavy rare earth element processing. This 3x multiplier effect on market control suggests processing operations capture 70-90% of supply chain margins.

Infrastructure requirements for downstream operations include high-temperature metallurgical facilities, sophisticated waste management systems, and specialised analytical laboratories for quality assurance. The capital expenditure requirements for new processing facilities typically exceed mining investments by orders of magnitude due to the complex chemical processing equipment and environmental control systems required.

However, the distribution of global rare earth reserves suggests that alternative processing capacity could theoretically be developed in multiple countries. Quality standards for defence and technology applications demand precision that few global facilities can achieve. Magnet-grade materials require specific purity levels and coercivity specifications that depend on advanced separation techniques and metallurgical processes developed over decades of industrial experience.

When big ASX news breaks, our subscribers know first

How Did China Achieve 90% Global Processing Dominance?

The Academic-Industrial Integration Strategy (1975-2024)

China's path to rare earth processing supremacy represents a deliberate, multi-decade strategy that integrated academic research with industrial capacity building. Analysis of over 76,000 scientific papers published between 1975 and 2024 reveals how systematic coordination between universities, state laboratories, and industrial facilities created unmatched capabilities in critical processing technologies.

| Metric | China | Rest of World |

|---|---|---|

| Global REE Publications | 24.1% | 75.9% |

| Processing Market Share | 90% | 10% |

| Heavy REE Processing | 99% | 1% |

| Mining Share | 69-70% | 30-31% |

The research reveals that China's advantage stems from massive, coordinated public research funding rather than individual technological breakthroughs. This systematic approach differs fundamentally from Western fragmented research models where multiple institutions pursue parallel efforts without integrated strategic direction.

Three-Phase Market Capture Evolution

Phase 1 (1975-1990): Foundation Building

This period was characterised by low-volume, geology-driven research focused on traditional deposits. Chinese institutions established foundational capabilities in rare earth chemistry and separation sciences while building the academic infrastructure necessary for later industrial scaling.

Phase 2 (1991-2007): Scale Development During Electronics Boom

Steady growth in research publication volume corresponded with China's rise as a global producer and expanding electronics demand. The strategic alignment between research direction and market opportunities enabled rapid translation of academic discoveries into industrial capacity.

Phase 3 (Post-2008): Monopolisation Through Export Restrictions

The post-2008 period brought explosive growth in rare earth research, triggered by China's export restrictions and the accelerating clean energy transition. This phase consolidated China's rare earth processing dominance as global supply chain crises accelerated research investment worldwide, though China's research growth exceeded other nations.

Cross-Disciplinary Research Concentration

The Technology-Economic Linkage Model reveals how China built tight coupling between academia, state laboratories, and industry, creating a pipeline where academic discoveries translate rapidly into industrial capacity. This integration spans:

• Materials science as the coordinating discipline (CDPI = 0.81)

• Metallurgical engineering for processing optimisation

• Applied chemistry for separation technique refinement

• Environmental science for waste management and sustainability

China achieved research leadership not through volume alone but by concentrating expertise at the intersection of multiple disciplines required for complete value chain mastery. While the United States and Europe remain strong in advanced materials research, their efforts remain fragmented, slower to commercialise, and less integrated across the full processing chain.

Why Traditional Mining-Focused Strategies Have Failed to Break China's Grip

The Processing Bottleneck Reality

Despite successful mining operations worldwide, China's rare earth processing dominance persists because diversifying supply chains requires more than adding raw material capacity. The fundamental challenge lies in the technical ecosystem needed to transform rare earth concentrates into high-purity oxides, metals, and finished products at commercial scale.

Mountain Pass in the United States exemplifies this limitation. While the facility produces approximately 12.3% of global rare earth output, it lacks integrated downstream processing capabilities. Rare earth concentrates from the mine typically require processing in Chinese facilities, maintaining dependency on Chinese separation services and technical expertise.

Lynas Rare Earths has attempted to address this gap through its operations spanning Mount Weld mine in Western Australia and processing facilities in Malaysia. However, the company faces ongoing challenges including:

• Regulatory approval delays and community opposition in Malaysia

• Processing capacity constraints limiting ore throughput

• Competition from established Chinese pricing and supply relationships

• Technical expertise gaps in advanced separation methodologies

Cost Structure Advantages That Persist

China's cost advantages extend beyond simple labour differentials to encompass systemic factors that create sustained competitive moats. In addition, recent developments in battery recycling breakthrough technology demonstrate how China continues to innovate across the entire value chain.

Labour and Energy Cost Differentials

Processing operations require skilled technical personnel and energy-intensive chemical processes. China benefits from lower wage costs for specialised metallurgical and chemical engineering expertise, combined with subsidised energy prices for industrial users.

Environmental Compliance Arbitrage

Rare earth processing generates significant chemical waste requiring sophisticated treatment systems. Variations in environmental compliance costs between jurisdictions create substantial cost differentials that affect processing economics and facility location decisions.

Scale Economies in Specialised Equipment

Processing equipment vendors concentrate in regions with established rare earth industries, creating advantages for Chinese operations through proximity to suppliers, reduced transportation costs, and integrated technical support. Minimum economic scale requirements for processing facilities favour locations with existing industrial ecosystems.

What Are the Emerging Technological Pathways for Diversification?

Unconventional Source Development

Research patterns show a decisive pivot away from traditional high-grade deposits toward unconventional and secondary sources. This shift reflects both environmental pressures and declining ore quality worldwide, creating opportunities for technological innovation in alternative processing approaches.

Alternative REE Sources Analysis:

| Source | Global Potential | Processing Characteristics |

|---|---|---|

| Coal Ash Deposits | ~50 million tonnes | Lower concentration, distributed availability |

| Ion-Adsorption Clays | Multiple countries | Lower-grade but simplified processing |

| Electronic Waste | Urban mining potential | Secondary source, circular economy |

| Bauxite Residue | Large industrial waste streams | Industrial waste utilisation opportunity |

Coal ash deposits represent particularly significant potential, with approximately 50 million tonnes of material containing recoverable rare earth content distributed across multiple countries. These deposits offer geographic diversification opportunities while utilising existing industrial waste streams.

Ion-adsorption clays provide processing advantages despite lower grades because they require less aggressive chemical treatment compared to traditional hard rock deposits. These deposits exist in multiple countries beyond China, offering potential supply chain diversification.

Advanced Processing Innovations

Research increasingly emphasises bioleaching, membrane separation, ionic liquids, and recycling technologies as alternatives to traditional acid leaching methodologies. These approaches address environmental concerns while potentially reducing capital requirements for new processing facilities.

Bioleaching and Membrane Separation Technologies

Biological extraction methods use microorganisms to solubilise rare earth elements from ores, potentially reducing chemical reagent requirements and environmental impacts. Membrane separation technologies offer precision separation capabilities with reduced waste generation.

Ionic Liquid Extraction Methods

Ionic liquids provide environmentally friendlier alternatives to traditional organic solvents used in rare earth separation. These techniques show promise for selective extraction while reducing chemical waste generation.

Recycling and Circular Economy Approaches

Electronic waste and urban mining represent substantial secondary rare earth sources. Recycling technologies offer the potential to recover high-purity materials from end-of-life products, reducing dependency on primary extraction while addressing waste management challenges.

Which Countries Are Positioned to Challenge China's Processing Monopoly?

United States Reshoring Initiatives

The United States has implemented comprehensive strategies to rebuild domestic rare earth processing capacity through the Defence Production Act and targeted industrial policy. These initiatives focus on public-private partnerships designed to overcome the technical and financial barriers that have historically prevented processing facility development.

Defence Production Act funding allocations specifically target critical mineral processing capabilities, recognising that national security requires domestic control over key material transformation processes. However, these programmes face challenges including technology transfer limitations and intellectual property protection requirements that complicate international cooperation.

European Union Critical Materials Strategy

The European Union's strategic autonomy objectives for 2030 include specific targets for domestic and allied processing capability development. The strategy emphasises partnerships with resource-rich countries in Africa and Greenland to create alternative supply chains independent of Chinese processing capacity.

European initiatives particularly focus on green processing technologies that align with environmental regulations and sustainability goals. This approach seeks to create competitive advantages through technological differentiation rather than direct cost competition with established Chinese operations.

Emerging Producer Positioning

Several countries possess both rare earth resources and growing research capabilities that could support processing capacity development:

Myanmar's Strategic Position

Myanmar currently accounts for 10.9% of global rare earth mining and possesses significant heavy rare earth deposits. However, political instability and regulatory uncertainty limit investment in processing infrastructure development.

Madagascar and Uganda Development Trajectories

Both countries possess substantial rare earth deposits and growing mining operations. Madagascar particularly holds heavy rare earth resources that could support specialised processing operations focused on high-value applications.

Kazakhstan's Research Leadership Potential

Kazakhstan has developed significant expertise in metallurgical research and processing technologies. The country's academic institutions contribute substantially to global rare earth research, providing potential foundations for industrial capacity development.

What Economic and Geopolitical Risks Does Processing Concentration Create?

Supply Chain Vulnerability Assessment

The concentration of rare earth processing in China creates systemic risks across multiple critical industries. Defence contractors, clean energy manufacturers, and technology companies face potential supply disruptions that could affect production timelines and national security capabilities. Moreover, the broader US-China trade war impact demonstrates how geopolitical tensions can exacerbate these vulnerabilities.

Defence Industry Exposure Analysis

Military applications require specific rare earth products including permanent magnets for guidance systems, specialised alloys for advanced materials, and electronic components for communications equipment. Processing concentration means defence supply chains depend on foreign capacity for mission-critical materials.

Clean Energy Transition Dependencies

Wind turbines, electric vehicle motors, and energy storage systems require processed rare earth materials in specific grades and configurations. The global clean energy transition relies on Chinese processing capacity for key enabling technologies, creating potential bottlenecks for climate goals.

Technology Sector Bottleneck Risks

Consumer electronics, telecommunications infrastructure, and computing systems incorporate rare earth elements in sophisticated applications. Processing monopolisation creates single points of failure for multiple technology sectors simultaneously.

Historical Precedents and Market Responses

The 2010-2014 export restriction period provides insight into how processing concentration affects global markets. During this time, export limitations created dramatic price volatility and forced industrial users to develop substitution strategies and alternative sourcing arrangements.

Market responses included accelerated recycling programme development, material efficiency improvements, and increased research into alternative technologies. However, these adaptations required years to implement and often involved performance compromises compared to optimal rare earth-based solutions.

The next major ASX story will hit our subscribers first

How Are Investment Patterns Shifting in Response to Processing Concentration?

Capital Allocation Trends in Non-Chinese Processing

Investment flows increasingly target downstream integration as mining companies recognise that processing capabilities determine long-term value capture. This shift reflects investor understanding that raw material assets provide limited strategic value without corresponding processing capacity.

Investment Flow Analysis:

• Downstream Integration: Mining companies expanding into processing operations

• Technology Development: Increased R&D spending on alternative separation methods

• Strategic Partnerships: Government-industry collaboration models emerging globally

• Acquisition Activity: Premium valuations for existing processing assets and technology companies

Traditional mining-focused investment strategies are evolving toward integrated value chain approaches that encompass both extraction and processing capabilities. This requires substantially higher capital commitments but offers greater strategic positioning and margin potential.

Venture Capital and Strategic Investment Focus

Technology-focused investment activity concentrates on innovations that could disrupt established processing approaches. Furthermore, the broader mining industry evolution demonstrates how technological disruption is reshaping traditional approaches across the sector.

Recycling Technology Startups

Companies developing advanced recycling processes for rare earth recovery from electronic waste attract significant venture capital interest. These technologies offer potential for distributed processing models that reduce dependency on centralised facilities.

Alternative Extraction Methods

Investment in bioleaching, membrane separation, and ionic liquid technologies reflects recognition that environmental constraints and resource availability drive innovation toward gentler processing approaches.

Automation and Process Optimisation

Digital technologies and process automation offer potential to reduce labour costs and technical expertise requirements for rare earth processing, potentially enabling processing capacity development in higher-cost jurisdictions.

What Does the Future Hold for Global Rare Earth Processing Competition?

Scenario Modelling for Market Structure Evolution

Multiple scenarios exist for how China's rare earth processing dominance might evolve over the next decade, each dependent on technological developments, geopolitical decisions, and investment flows. Analysts note that despite Western efforts, China is poised to dominate rare earths for years to come.

Baseline: Continued Chinese Dominance Through 2030

Under current trajectories, China likely maintains 80-90% processing market share through 2030. This scenario assumes continued integration advantages, cost competitiveness, and limited success in alternative processing capacity development globally.

Diversification: 20-30% Non-Chinese Processing by 2035

Successful development of alternative processing facilities in the United States, Australia, and other allied countries could reduce Chinese market share to 70-80%. This scenario requires sustained government support, technological breakthroughs, and successful scaling of pilot operations.

Fragmentation: Regional Processing Hubs Emergence

Development of specialised regional processing centres focused on specific rare earth products or applications could create a more distributed global industry structure. Heavy rare earth processing might remain concentrated while light rare earth processing becomes more geographically diverse.

Technology Disruption Potential

Several technological developments could fundamentally alter rare earth processing economics and geographic distribution:

Breakthrough Separation Technologies

Advanced membrane technologies, biological extraction methods, or novel chemical processes could reduce capital requirements and technical barriers for new processing facilities, enabling more distributed capacity development.

Synthetic Alternatives Development

Research into synthetic materials that provide equivalent performance to rare earth-based products could reduce overall demand and eliminate supply chain dependencies for specific applications.

Circular Economy Scaling Impacts

Successful scaling of rare earth recycling from electronic waste and industrial applications could provide alternative supply sources that bypass traditional mining and processing bottlenecks.

Key Takeaways for Investors and Policymakers

Strategic Implications for Portfolio Construction

Investment strategies must differentiate between companies focused on extraction versus processing capabilities. Processing-integrated companies command premium valuations due to their control over higher-margin value chain segments and strategic importance for supply chain security.

Geographic diversification considerations extend beyond traditional country risk assessment to encompass processing capacity location and technology access. Companies with processing capabilities outside China offer strategic value that justifies premium investment multiples.

Technology and innovation exposure strategies should focus on companies developing alternative processing methods, recycling technologies, and synthetic substitutes. These investments provide potential upside from technological disruption while offering hedge positions against continued China's rare earth processing dominance.

Policy Recommendations for Supply Chain Resilience

Research and development funding priorities should emphasise interdisciplinary approaches that integrate materials science, metallurgy, and environmental technologies. Successful processing capacity development requires the same academic-industrial integration that enabled China's dominance.

International cooperation frameworks must balance technology sharing with intellectual property protection to enable allied processing capacity development while maintaining competitive advantages in critical technologies.

Strategic stockpiling considerations should focus on processed materials rather than raw concentrates, recognising that processing bottlenecks represent the primary supply chain vulnerability for critical applications.

Disclaimer: This analysis is based on published research and publicly available information. Market conditions, technological developments, and geopolitical situations change rapidly in the rare earth sector. Investors should conduct independent due diligence and consider consulting with qualified professionals before making investment decisions. Past performance and current market positions do not guarantee future results.

Ready to Capitalise on Critical Minerals Investment Opportunities?

Discovery Alert provides instant notifications on significant ASX mineral discoveries, powered by its proprietary Discovery IQ model, helping investors identify actionable opportunities in critical minerals and rare earth sectors ahead of the broader market. Explore why major mineral discoveries can generate substantial returns and begin your 30-day free trial today to position yourself strategically in Australia's evolving critical minerals landscape.