June 9, 2026

China's Strategic Consolidation Through CMRG Formation

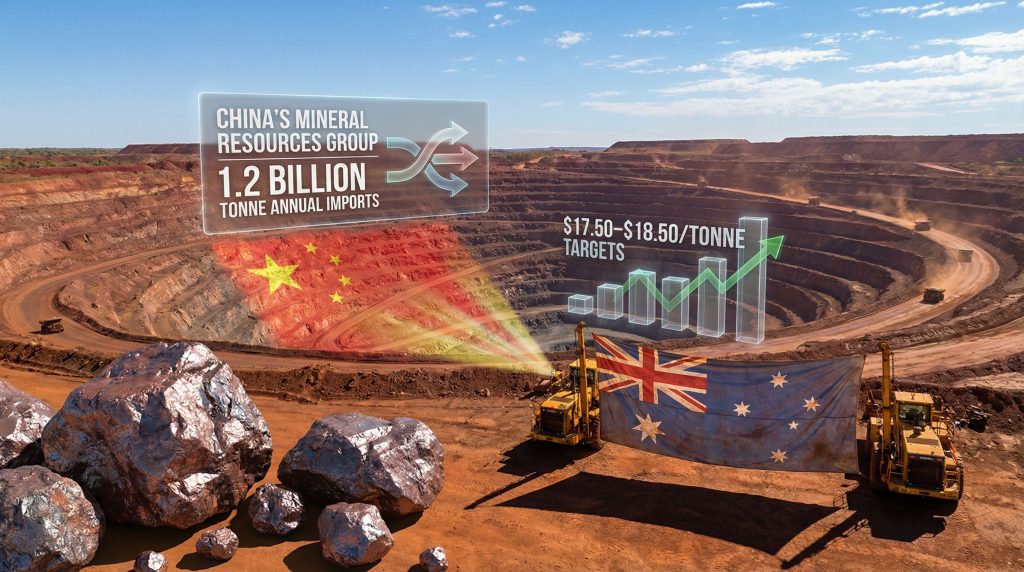

The establishment of China Mineral Resources Group Co represents a fundamental shift in how the world's largest steel-producing nation approaches commodity procurement. Fortescue chair urges China to end iron-ore buying strategy that has consolidated significant negotiating power by aggregating demand from multiple Chinese steel mills, creating a coordinated approach that diverges sharply from traditional market mechanisms. Furthermore, this centralized entity has introduced new dynamics that affect global iron ore price trends and supply relationships.

Centralised Negotiation Power and Market Impact

CMRG's formation has introduced a new dynamic where individual steel mills no longer negotiate independently with major mining companies. Instead, this state-backed entity acts as an intermediary, leveraging collective buying power to influence pricing structures across the entire supply chain.

The organisation's approach extends beyond simple price negotiations, encompassing broader strategic objectives including currency diversification initiatives and supply chain control mechanisms. By centralising procurement decisions, CMRG can implement coordinated responses to market conditions, potentially creating artificial scarcity or abundance depending on economic policy objectives.

Strategic Leverage Tactics and Implementation

The buying group has demonstrated willingness to employ selective restriction strategies against specific suppliers when negotiations do not align with their objectives. These tactics include temporary product bans, quality specification changes, and payment term modifications that significantly impact mining company cash flows.

Currency settlement requirements have emerged as another key negotiation point. CMRG pushes for increased use of yuan-denominated transactions rather than traditional US dollar arrangements, serving dual purposes of reducing foreign exchange risk while supporting broader Chinese monetary policy objectives.

Long-term contract structures versus spot market participation has become a central tension point. The organisation prefers arrangements that provide greater price predictability and supply security over market-driven pricing mechanisms.

When big ASX news breaks, our subscribers know first

Australian Mining Industry Response Strategies

The major Australian iron ore producers have adopted distinctly different approaches to managing relationships with CMRG. These strategies reflect varying risk tolerances and strategic philosophies regarding Chinese market engagement, particularly considering Australian industry advantages in the global market.

Fortescue's Collaborative Integration Model

Fortescue Metals Group has positioned itself as a collaborative partner rather than adversarial negotiator in dealings with Chinese interests. The company has secured a substantial $14.2 billion yuan ($2 billion USD) financing arrangement from major Chinese lenders, demonstrating successful integration with Chinese financial systems.

Key elements of Fortescue's strategy include:

- Procurement of electric mining equipment from Chinese manufacturers

- Integration with Chinese supply chains for operational equipment

- Financial partnerships that create mutual dependency relationships

- Focus on long-term supply agreements rather than spot market exposure

The company's approach reflects a belief that collaborative engagement produces more sustainable outcomes than confrontational negotiation tactics. By aligning operational requirements with Chinese industrial capacity, Fortescue has created multiple touchpoints that extend beyond simple commodity transactions.

Andrew Forrest, Fortescue's executive chairman, has characterised CMRG's approach as an attempt to create artificial market manipulation through coordinated buyer behaviour. However, rather than responding with confrontational tactics, he advocates for expanded trade relationships and technological cooperation as more effective long-term strategies.

BHP's Market Resistance and Consequences

BHP Group has experienced more significant friction in its relationship with CMRG, resulting in restrictions on certain iron ore products and complicated contract negotiations. The company's approach appears to prioritise market-driven pricing mechanisms over accommodative relationship management.

The restrictions imposed on BHP products demonstrate CMRG's willingness to use market access as a negotiation tool. These actions create revenue uncertainty and operational complexity for the mining giant, serving as a clear signal to other producers regarding potential consequences of non-compliance.

Rio Tinto's Balanced Approach

Rio Tinto has adopted a more measured response that seeks to maintain market access while preserving pricing flexibility. The company's strategy emphasises relationship preservation through limited operational integration whilst avoiding the comprehensive partnership model employed by Fortescue.

This balanced approach reflects recognition that Chinese market access remains critical for operational viability. However, it maintains sufficient independence to respond to changing market conditions and alternative customer requirements.

Economic and Geopolitical Implications for Australia

Iron ore exports represent a cornerstone of Australia's economic stability, generating substantial export revenue and supporting employment across multiple sectors. The concentration of demand in Chinese markets creates significant vulnerability to coordinated buyer behaviour and policy changes.

Economic Dependency Analysis

Australia's iron ore industry generates hundreds of billions in annual export revenue, with Chinese purchases representing the dominant share of total production. This concentration creates systemic risk where policy changes or trade relationship deterioration could significantly impact national economic performance.

The mining sector's contribution extends beyond direct employment and tax revenue. It supports extensive supply chain networks including transportation, port operations, equipment manufacturing, and professional services. Consequently, disruption to iron ore exports would create cascading effects throughout these interconnected sectors.

Currency implications are particularly significant, as iron ore exports represent a major source of foreign exchange earnings. These earnings support Australia's current account balance and currency stability in global markets.

Strategic Response Options and Policy Considerations

Australian policymakers face complex decisions regarding appropriate responses to centralised buyer behaviour. Direct government intervention could escalate trade tensions while potentially violating international trade agreements and established market principles.

Alternative market development strategies require substantial investment and time to implement effectively. Diversifying customer bases beyond Chinese markets would necessitate infrastructure development, relationship building, and potentially accepting lower prices from alternative buyers.

Infrastructure resilience planning has become increasingly important as CMRG's tactics demonstrate how concentrated buyer power can create operational uncertainty. This uncertainty affects both mining companies and broader economic implications for resource-dependent regions.

Future Supply Dynamics and Market Evolution

The global iron ore supply landscape faces potential transformation from several major developments that could alter current power dynamics between buyers and sellers. Moreover, understanding these developments is crucial for assessing iron ore demand insights and future market trends.

Alternative Supply Development Projects

Guinea's Simandou iron ore project represents one of the world's largest undeveloped iron ore deposits, with potential production capacity that could significantly impact global supply balances. Chinese investment positioning in this project suggests strategic thinking beyond simple commodity procurement toward supply chain control.

The development timeline for major new supply sources typically spans decades, creating extended periods where current market dynamics remain relevant. However, successful development of alternative supply sources could provide Chinese buyers with additional leverage in negotiations with Australian producers.

West African iron ore development presents both opportunities and challenges, including infrastructure requirements, political stability considerations, and quality specifications. These factors may differ significantly from established Australian supply sources.

Technology Integration and Green Steel Transitions

Clean energy integration in iron ore processing and steel production creates new quality specifications and pricing premiums. These changes could alter traditional supply relationships and provide mining companies with differentiation opportunities.

Innovation partnerships between mining companies and steel producers could create collaborative relationships that transcend simple buyer-seller dynamics. Technical cooperation in areas such as carbon reduction, automation, and process optimisation may provide alternative frameworks for managing commercial relationships.

Quality premium trends for low-carbon steel production reflect growing environmental requirements that create differentiation opportunities. Mining companies willing to invest in advanced processing technologies and environmental management systems may command premium pricing.

Strategic Scenario Analysis and Market Projections

Three primary scenarios emerge from current market dynamics, each presenting distinct implications for mining companies, buyers, and broader economic systems. Furthermore, these scenarios reflect the ongoing China surplus impact on global commodity markets.

Scenario One: Enhanced Chinese Consolidation

Further expansion of CMRG's influence could result in even greater centralised control over iron ore purchasing decisions. This scenario would likely increase price volatility for mining companies whilst providing Chinese steel mills with enhanced supply security and cost predictability.

Mining company responses would necessarily become more sophisticated, potentially including:

- Increased focus on operational efficiency and cost reduction

- Enhanced customer diversification efforts

- Technology partnerships that create mutual dependency relationships

- Financial hedging strategies to manage price volatility

Global iron ore market restructuring under this scenario would likely favour buyers over sellers. This restructuring could potentially reduce mining company profitability whilst increasing supply chain integration between Chinese industrial systems and global resource extraction operations.

Scenario Two: Market Fragmentation and Diversification

Alternative buyer development could emerge through coordinated responses from non-Chinese steel producers, government intervention, or technological changes. These developments might reduce dependency on traditional supply relationships and create more balanced market dynamics.

New pricing mechanisms might evolve that provide mining companies with greater flexibility whilst maintaining transparent market-driven valuations. Regional trade arrangements could create alternative frameworks for commodity transactions that reduce exposure to centralised buyer behaviour.

Market fragmentation responses would require substantial coordination among producing countries and alternative buyers. This coordination presents implementation challenges but potentially creates more balanced negotiation dynamics for all parties involved.

Scenario Three: Collaborative Integration Framework

Joint venture partnerships and shared value creation could emerge as preferred alternatives to adversarial negotiation approaches. This scenario would emphasise long-term supply security and technological cooperation over short-term price optimisation.

Technology transfer agreements and mutual dependency relationships could create win-win frameworks where mining companies provide supply security. In return, Chinese partners contribute financing, equipment, and market access for expanded operations.

Long-term supply contracts with built-in flexibility mechanisms could provide both sides with adequate protection against market volatility. These contracts would maintain incentives for operational efficiency and innovation investment.

Investment and Industry Implications

The evolving dynamics between centralised buyers and mining companies create significant implications for investment decisions, company valuations, and industry structure. Additionally, companies like those following the Zijin expansion strategy are adapting to these changing market conditions.

Mining Company Valuation Considerations

Cash flow volatility assessments must incorporate increased political and commercial risk factors resulting from concentrated buyer behaviour. Traditional valuation models may inadequately capture the complexity of managing relationships with centralised purchasing entities.

Capital allocation priorities for major producers are shifting toward operational efficiency improvements, customer diversification initiatives, and technology investments. These investments create differentiation advantages beyond simple cost competition.

| Valuation Factor | Traditional Model | Current Environment |

|---|---|---|

| Price Predictability | Market-driven cycles | Negotiation-dependent |

| Customer Concentration Risk | Moderate concern | High impact factor |

| Technology Investment | Cost optimisation | Strategic differentiation |

| Political Risk Assessment | Country-specific | Relationship-dependent |

Merger and acquisition activity potential may increase as companies seek scale advantages, operational synergies, and enhanced negotiation power through consolidated operations.

Infrastructure and Logistics Optimisation

Port capacity optimisation strategies have become increasingly important as mining companies seek flexibility to respond to changing customer requirements. These strategies also address potential supply chain disruptions that could affect operational continuity.

Shipping route diversification requirements reflect recognition that concentrated buyer relationships create vulnerability to logistics disruption and transportation cost manipulation. Companies must develop alternative pathways to maintain operational flexibility.

Storage and blending facility investments allow mining companies to optimise product specifications for different customers whilst maintaining operational efficiency. These investments support varying demand patterns across multiple customer segments.

Key infrastructure considerations include:

- Multi-customer port access capabilities

- Flexible blending and product specification systems

- Alternative transportation route development

- Strategic stockpile management systems

The next major ASX story will hit our subscribers first

Risk Management and Strategic Recommendations

Successfully navigating the current market environment requires sophisticated risk management frameworks and strategic planning. These approaches must extend beyond traditional commodity market considerations to address relationship-dependent market dynamics.

Comprehensive Risk Assessment Frameworks

Mining companies must develop integrated risk management systems that address political, commercial, operational, and financial uncertainties simultaneously. Traditional commodity price hedging strategies provide insufficient protection against negotiation-based pricing mechanisms and relationship-dependent market access.

Scenario planning exercises should incorporate multiple potential outcomes including further buyer consolidation, market fragmentation, and collaborative integration alternatives. Each scenario requires distinct operational and financial preparation to maintain business viability.

Relationship management protocols must balance accommodation with independence, seeking mutually beneficial outcomes whilst preserving strategic flexibility. This balance becomes crucial for adapting to changing market conditions.

Strategic Planning Recommendations

For Mining Companies:

- Operational Excellence: Invest in cost reduction and efficiency improvements that provide competitive advantages regardless of market structure changes

- Customer Diversification: Develop alternative market relationships that reduce dependency on any single buyer or buyer group

- Technology Leadership: Pursue innovation investments that create quality premiums and differentiation opportunities

- Financial Resilience: Maintain balance sheet strength and hedging strategies appropriate for increased volatility

For Investors:

- Due Diligence Enhancement: Incorporate relationship quality and political risk assessments into investment evaluations

- Portfolio Diversification: Balance exposure across different mining companies, commodities, and geographic regions

- Long-term Perspective: Focus on companies with sustainable competitive advantages rather than short-term market position

For Policymakers:

- Market Monitoring: Develop systems for tracking concentrated buyer behaviour and potential anti-competitive practices

- Diplomatic Engagement: Maintain dialogue channels that address trade relationship tensions before they escalate

- Strategic Planning: Consider infrastructure investments and policy frameworks that support market diversification

Industry Outlook and Future Considerations

The iron ore market's evolution toward centralised buyer power represents a fundamental shift in global commodity trading dynamics. As mining companies navigate this new landscape, they must address challenges whilst identifying opportunities for sustainable growth and operational excellence.

Recent developments in the industry highlight the importance of adaptive strategies. According to Mining Weekly, industry leaders are calling for more balanced approaches to commodity procurement that support market stability.

Furthermore, Bloomberg's analysis suggests that the current tensions between centralised buying strategies and traditional market mechanisms require careful diplomatic and commercial navigation.

Consequently, whilst this creates challenges for traditional mining operations, it also presents opportunities for companies willing to adapt their strategic approaches and operational frameworks. Success in this environment will require balancing collaborative engagement with strategic independence, operational excellence with relationship management, and short-term adaptability with long-term sustainability planning.

Mining companies, investors, and policymakers must recognise that traditional market mechanisms are being replaced by more complex systems requiring sophisticated risk management and strategic planning capabilities. The companies and nations that successfully navigate this transition will likely emerge stronger and more resilient, whilst those that fail to adapt may face significant competitive disadvantages in an increasingly interconnected and politically sensitive global commodity market.

Ready to Capitalise on Iron Ore Market Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 14-day free trial today and secure your market-leading advantage in the evolving commodities landscape.