July 20, 2026

Understanding China's Strategic Energy Independence Initiative

Global energy markets face unprecedented transformation as major consuming nations prioritise domestic resource development over international commodity dependencies. This shift challenges fundamental assumptions about energy trade patterns and reveals how technological advancement can rapidly alter geopolitical energy relationships. For China specifically, the world's second-largest economy has embarked on an aggressive domestic natural gas expansion strategy that fundamentally reshapes global liquefied natural gas market dynamics, with China's LNG demand decline becoming a critical factor.

The implications extend far beyond simple supply-demand calculations. China's evolving energy procurement approach demonstrates how strategic planning, technological innovation, and bilateral partnerships can reduce exposure to volatile international commodity markets while strengthening energy security strategies.

When big ASX news breaks, our subscribers know first

What Economic Forces Drive China's Reduced LNG Import Appetite?

Domestic Production Economics Transform Import Calculations

China's unconventional gas sector has achieved breakthrough production economics, particularly in the Sichuan Basin where shale formations now deliver commercially viable output rates. The transformation represents a dramatic reversal from less than a decade ago when energy companies struggled to achieve commercial production from Chinese shale geology, which differs significantly from U.S. basin characteristics.

Recent production data reveals the scale of this transformation. November 2025 Chinese natural gas production reached 22.1 billion cubic meters, representing a 7.1% year-over-year increase driven by faster-than-expected shale gas developments in the Sichuan Basin. This acceleration enabled total 2025 domestic production of 263 billion cubic meters, with projections indicating growth to 278.5 billion cubic meters in 2026.

| Production Metric | 2025 Actual | 2026 Projection | Growth Rate |

|---|---|---|---|

| Total Gas Production | 263 bcm | 278.5 bcm | +6.0% |

| Monthly Peak (Nov) | 22.1 bcm | – | +7.1% YoY |

| Shale Gas Focus | Sichuan Basin | Sichuan & Shanxi | Accelerating |

The economic implications are profound. Rising domestic production creates an inverse relationship with import requirements, as Chinese state oil and gas majors including CNPC, Sinopec, and CNOOC announce new discoveries and expand production capacity. This domestic supply growth reduces China's exposure to volatile LNG spot pricing while providing supply flexibility that long-term import contracts cannot match.

Pipeline Infrastructure Creates Import Substitution

Russia's Power of Siberia pipeline expansion represents a strategic alternative to LNG spot markets, with 8 billion cubic meters of additional capacity scheduled for 2026. This infrastructure development reduces China's exposure to maritime supply routes and Western-controlled financial systems whilst strengthening bilateral energy relationships that align with broader geopolitical objectives.

Pipeline imports offer several advantages over LNG:

• Price stability through long-term bilateral agreements

• Reduced exposure to maritime chokepoints and sanctions

• Lower transportation costs compared to liquefied gas

• Enhanced supply security through overland routes

The strategic pivot toward pipeline gas reflects China's broader energy security objectives, prioritising supply diversification and reduced dependence on volatile international markets, similar to how the US-China trade war influenced other commodity flows.

How Will China's LNG Demand Decline Impact Global Market Dynamics?

Supply-Demand Rebalancing Accelerates Market Oversupply

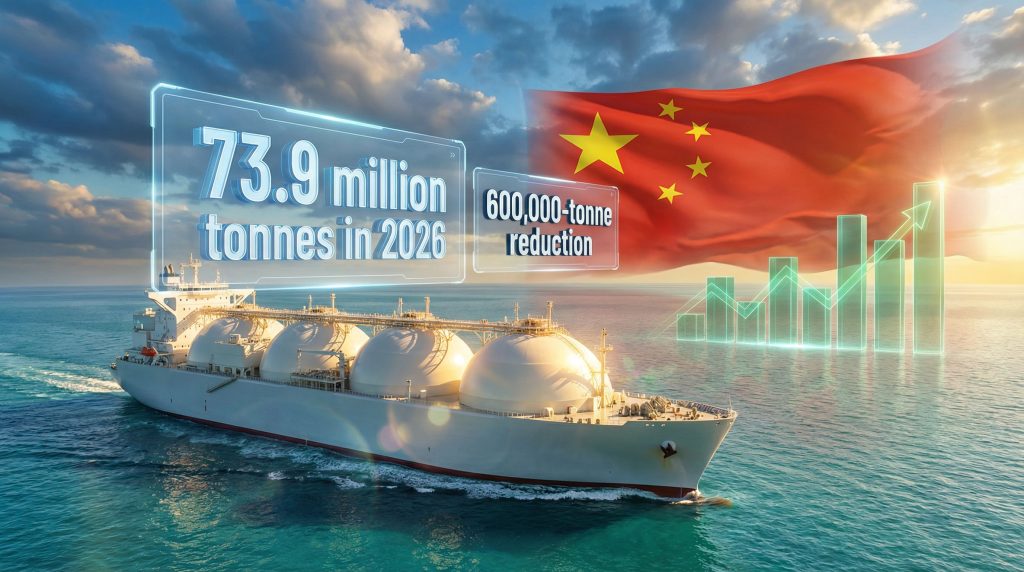

Analytics firm Kpler's revised forecast projects Chinese LNG demand at 73.9 million tonnes in 2026, representing a 600,000-tonne reduction from previous estimates. While this figure appears modest against the backdrop of global LNG trade volumes exceeding 400 million tonnes annually, the timing proves critical for market dynamics.

The demand reduction coincides with approximately 40 million tonnes of new global LNG capacity entering markets between 2025-2027, primarily from United States and Qatar expansions. This confluence creates potential oversupply conditions that could pressure pricing and project economics across the industry, with tariffs impact markets adding additional complexity to global energy flows.

Critical Market Insight: Even modest Chinese demand reductions carry outsized market significance given the capital intensity of LNG infrastructure and the role of Chinese buyers in providing anchor contracts for new projects.

China's LNG demand decline has become evident through six-year lows in 2025 following twelve consecutive monthly declines, demonstrating that reduced appetite extends beyond temporary demand fluctuations to represent structural changes in energy procurement strategy. This trend parallels developments in other commodity markets, particularly as reflected in the US natural gas forecast which shows similar supply-demand rebalancing dynamics.

Asian Spot Price Implications

Reduced Chinese appetite for spot LNG cargoes applies downward pressure on Asian pricing benchmarks, particularly during traditional peak demand seasons. According to data from Investing.com, this structural shift affects:

• JKM (Japan Korea Marker) price formation

• Long-term contract renegotiation dynamics

• Regional price differentials between Atlantic and Pacific basins

• Producer margin compression across existing facilities

The pricing environment may accelerate industry consolidation and force recalibration of project development timelines as developers reassess demand assumptions that historically relied on continued Chinese import growth.

What Alternative Demand Centers Could Offset Chinese Reduction?

Emerging Market Substitution Potential

India's Industrial Expansion represents the most significant potential demand offset, with manufacturing output growth and power generation requirements driving natural gas consumption higher. India's LNG infrastructure expansion and coal-to-gas switching policies create substantial import growth potential, though specific growth projections require verification from official government sources.

Southeast Asian Growth Markets include:

• Vietnam: Economic development and industrial expansion driving energy demand

• Thailand: Power sector modernisation and environmental compliance requirements

• Bangladesh: Infrastructure development and growing electricity generation needs

These markets benefit from declining global LNG prices caused by oversupply conditions, making gas-to-power projects increasingly economically attractive.

European Market Dynamics

European Union plans to implement total bans on Russian energy imports create significant LNG flow redirections. Currently, the EU represents the largest buyer of Russian LNG, with these volumes requiring alternative destinations once restrictions take effect.

The redirection likely targets China and India as primary alternative markets, though European demand patterns differ significantly from Asian consumption profiles regarding seasonality and contract structures. Furthermore, analysts at Reuters report that high prices continue to cap Chinese demand, supporting the structural shift away from imports.

How Do Geopolitical Factors Influence China's LNG Strategy?

Energy Security Through Supply Diversification

China's reduced LNG dependence reflects broader strategic objectives around energy security and supply chain resilience. The approach reduces vulnerability to maritime supply disruptions, international sanctions regimes, and Western-controlled financial systems whilst building stronger relationships with neighbouring energy producers.

Bilateral Energy Partnerships Reshape Trade Flows

Russian LNG exports to China reached record volumes in 2025, sourced from facilities operating under international sanctions. This demonstrates how bilateral energy relationships can circumvent traditional trading mechanisms when pricing and geopolitical incentives align.

The relationship expansion includes:

• Pipeline gas flow increases through Power of Siberia

• LNG imports from sanctioned Russian facilities

• Potential Central Asian supply agreements

• Technology transfer in unconventional gas development

What Investment Implications Emerge from China's LNG Demand Decline?

LNG Project Economics Face Headwinds

New Project Financing challenges emerge as developers reassess demand assumptions, particularly for facilities targeting Asian markets where Chinese buyers historically provided anchor contracts. Projects must identify alternative long-term buyers or accept higher market exposure risks.

Existing Asset Valuations face potential compression as oversupply conditions reduce margins. Publicly traded LNG companies and infrastructure funds may experience earnings pressure if spot pricing remains weak through the oversupply cycle, requiring adaptation of broader investment strategy insights.

Alternative Investment Opportunities

Domestic Chinese Gas Infrastructure benefits from increased production and consumption patterns:

• Pipeline networks connecting production centres to demand centres

• Underground storage facilities enabling supply optimisation

• Distribution systems serving industrial and residential customers

• Processing facilities handling unconventional gas streams

Non-Chinese Asian Markets may offer superior risk-adjusted returns as LNG infrastructure investments target emerging economies with stronger demand growth trajectories.

The next major ASX story will hit our subscribers first

What Long-Term Structural Changes Does This Trend Signal?

Global Energy Trade Pattern Evolution

China's LNG demand decline represents an early indicator of how major energy consumers may prioritise domestic production and regional partnerships over global commodity markets. This challenges assumptions about continued energy trade globalisation and suggests potential fragmentation along geopolitical lines.

Technology Transfer and Production Scaling

Chinese success in unconventional gas development demonstrates how technology transfer, domestic innovation, and strategic investment can rapidly transform energy import dependencies. The model potentially applies to other major consuming nations seeking energy independence through domestic resource development.

Key technological advances enabling Chinese production growth include:

• Hydraulic fracturing adaptations for local geology

• Water management solutions for arid regions

• Drilling efficiency improvements reducing costs

• Production optimisation through data analytics

How Should Market Participants Adapt to These Changing Dynamics?

LNG Producers and Traders

Portfolio Diversification becomes critical for companies heavily exposed to Chinese demand:

-

Target emerging Asian economies with growing LNG requirements

-

Develop flexible contract structures accommodating demand volatility

-

Expand European market presence as Russian supply redirects

-

Invest in smaller-scale LNG solutions for distributed markets

Contract Structure Innovation may better accommodate volatile demand patterns in oversupplied market environments through shorter-term agreements and flexible pricing mechanisms.

Energy Investors and Analysts

Demand Forecast Recalibration requires fundamental revision of traditional LNG models to account for accelerating domestic production capabilities in major consuming nations. Investment strategies must incorporate granular analysis of individual country energy policies rather than broad regional demand assumptions.

Regional Market Analysis priorities include:

• Government policy frameworks affecting LNG demand

• Domestic resource development potential

• Infrastructure investment timelines and capacity

• Economic growth trajectories and energy intensity trends

What Does This Mean for Global Energy Security?

China's LNG demand decline reflects broader trends toward energy localisation and bilateral partnerships that may reshape international energy architecture. The transformation demonstrates how technological advancement and strategic planning can reduce import dependencies whilst maintaining energy security.

Implications for Global Markets:

• Reduced dependence on traditional energy trading hubs

• Increased importance of bilateral energy partnerships

• Technology transfer acceleration for domestic resource development

• Potential fragmentation of global energy commodity markets

Energy Security Considerations:

• Enhanced supply diversity through multiple procurement channels

• Reduced exposure to maritime supply route disruptions

• Stronger energy relationships with neighbouring producer nations

• Improved domestic production capabilities reducing import vulnerability

The implications extend beyond LNG markets to influence global energy investment patterns, geopolitical relationships, and the pace of energy transition planning across major economies. Market participants must adapt strategies to account for China's LNG demand decline whilst identifying alternative demand centres that can absorb redirected global supply flows.

This analysis is for educational purposes only and does not constitute investment advice. Energy market conditions and geopolitical factors can change rapidly, affecting the scenarios discussed above.

Want to Capitalise on Global Energy Market Shifts?

Discovery Alert's proprietary Discovery IQ model provides instant alerts on significant ASX mineral and energy discoveries, helping investors identify actionable opportunities as global market dynamics evolve. Start your 30-day free trial today to position yourself ahead of these transformative market changes.