July 1, 2026

China export controls on tungsten have fundamentally altered global supply dynamics, creating unprecedented market disruptions across critical industries. The coordinated implementation of export restrictions demonstrates sophisticated strategic planning designed to maximise leverage while maintaining market justification. Furthermore, understanding these supply chain vulnerabilities provides crucial context for evaluating how strategic export restrictions can fundamentally alter market dynamics.

Strategic Export Control Architecture in Critical Minerals

China's tungsten export control framework represents a sophisticated policy mechanism designed to maximise strategic leverage while maintaining plausible market justification. The system operates through multiple layers of restriction, beginning with production quotas at the mining level and extending through export licensing requirements for finished products.

Mining Quota Reductions at Source

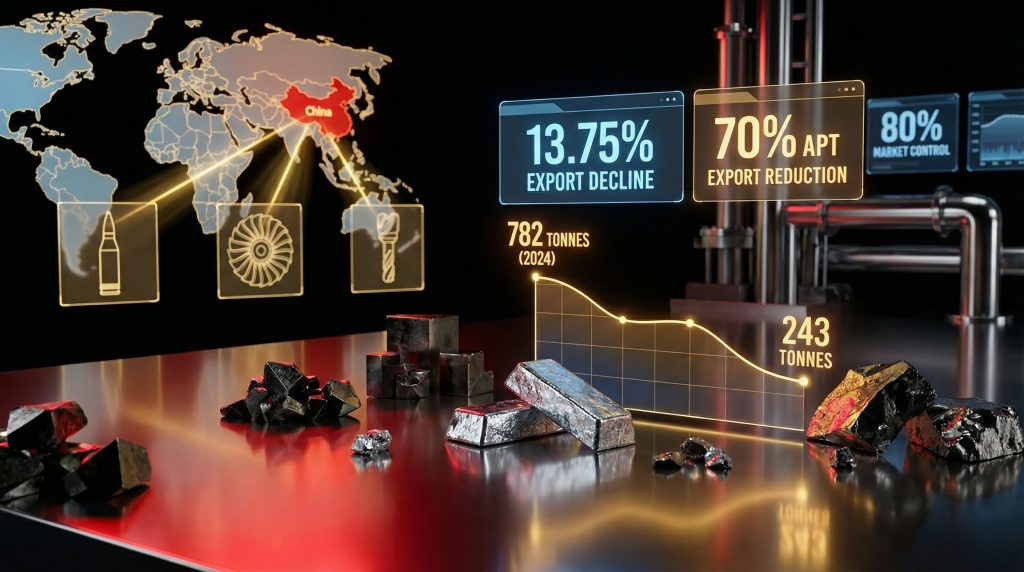

The Ministry of Natural Resources established initial mining quotas at 58,000 tonnes in early 2025, representing a 6.45% year-on-year decrease from previous production levels. This reduction occurred at the primary production stage, creating upstream supply constraints that affect all downstream tungsten products regardless of export licensing policies.

Major producing provinces subsequently implemented additional output cuts ranging from 8% to 10%, according to industry data from Chinese tungsten producers. These provincial-level reductions compound the national quota restrictions, creating a cumulative supply reduction that extends well beyond the initial 6.45% national target.

Export Licensing and Dual-Use Classifications

The dual-use classification system enables selective export approval based on end-use applications rather than simple volume quotas. This mechanism allows Chinese authorities to maintain supply to strategically important partners while restricting access to countries or industries deemed problematic from a geopolitical perspective.

Ammonium paratungstate (APT) faces the most stringent export restrictions, with volumes declining approximately 70% from 782 tonnes in 2024 to 243 tonnes during January-November 2025. This dramatic reduction specifically targets the precursor material required for specialised tungsten processing, effectively controlling access to downstream production capabilities.

Temporal Implementation Strategy

The phased implementation approach demonstrates sophisticated policy planning. Initial export controls began in January 2026, followed by increasingly restrictive measures throughout the year. This graduated approach allows Chinese domestic industries to adjust supply chains while maintaining maximum disruption to international competitors.

When big ASX news breaks, our subscribers know first

Market Concentration and Competitive Dynamics

China's control over more than 80% of global tungsten production represents the culmination of decades of systematic market positioning. This dominance extends beyond simple mining operations to encompass specialised processing capabilities that create natural barriers to competition.

Vertical Integration Advantages

Chinese tungsten operations integrate mining, processing, and manufacturing within coordinated industrial clusters. This vertical integration provides cost advantages and supply chain security that standalone mining operations cannot replicate. When export controls combine with integrated production, the competitive advantage intensifies dramatically.

The processing specialisation barrier proves particularly significant for APT production. Only a limited number of facilities globally possess the technical capability and environmental compliance infrastructure necessary for commercial-scale APT processing. Moreover, this specialisation creates natural bottlenecks independent of policy-driven export restrictions.

Non-Chinese Supply Constraints

Alternative tungsten supply sources face multiple constraints limiting their ability to replace Chinese production. Countries like Russia, Vietnam, Bolivia, and the Democratic Republic of Congo produce tungsten, but at scales insufficient to offset Chinese supply restrictions.

| Alternative Supplier | Estimated Production Capacity | Key Constraints |

|---|---|---|

| Russia | 2,000-3,000 tonnes/year | Sanctions, limited processing |

| Vietnam | 1,500-2,500 tonnes/year | Environmental regulations, scale |

| Bolivia | 1,000-1,500 tonnes/year | Infrastructure, processing gaps |

| DRC | 500-1,000 tonnes/year | Political instability, transport |

The combined capacity of major non-Chinese producers represents less than 15% of global demand, highlighting the structural supply gap that China export controls on tungsten exploit.

Price Formation Mechanisms and Market Response

Tungsten pricing operates through multiple channels that respond differently to supply constraints. Spot market transactions experience immediate price volatility, while long-term contracts may remain temporarily insulated from supply disruptions. This temporal pricing variation creates complex market dynamics during supply constraint periods.

Immediate Price Impact Assessment

Tungsten prices reached record highs throughout 2026 as supply constraints intensified. The price elevation reflects not merely reduced volume but the absence of meaningful substitutes for specialised applications. Defense contractors cannot easily switch to alternative materials for armour-piercing ammunition, and aerospace manufacturers require tungsten strategic importance for turbine blade applications.

Chinese producer stocks have responded positively to supply tightening, with companies like Xiamen Tungsten experiencing stock price gains as markets price in scarcity premiums. This market response demonstrates investor confidence that export controls will sustain elevated pricing levels.

Demand Inelasticity in Critical Applications

Defense sector requirements create highly inelastic demand characteristics. Military procurement contracts specify tungsten-based materials for specific performance requirements that alternative materials cannot meet. This inelasticity means price increases have minimal impact on demand volumes, allowing suppliers to capture significant margin expansion.

Industrial applications show similar inelasticity patterns. Tungsten carbide cutting tools provide productivity advantages that justify premium pricing. Manufacturing operations depend on these tools for precision machining, creating willingness to absorb higher tungsten costs rather than accept reduced manufacturing efficiency.

Industrial Application Dependencies and Substitution Limits

Understanding tungsten's role in critical applications reveals why supply disruptions create disproportionate market impact. The metal's unique properties make substitution extremely difficult or impossible across multiple high-value applications.

Defense Sector Vulnerabilities

Military applications represent the most strategic tungsten demand segment. Key defense uses include:

• Armour-piercing ammunition cores requiring tungsten's density and hardness

• Advanced armour systems utilising tungsten's ballistic protection properties

• Military aircraft components demanding tungsten's high-temperature performance

• Naval vessel systems requiring corrosion-resistant tungsten alloys

These applications typically specify tungsten due to performance requirements that alternative materials cannot meet. Defense contractors face potential supply disruptions that could impact readiness and procurement timelines.

Aerospace Manufacturing Dependencies

Commercial and military aerospace sectors rely heavily on tungsten for specialised components:

• Turbine blade manufacturing requiring tungsten's high-temperature stability

• Engine components utilising tungsten's thermal expansion properties

• Satellite systems incorporating tungsten for radiation shielding

• Advanced propulsion systems demanding tungsten's unique characteristics

The aerospace industry operates under stringent certification requirements that make material substitution extremely challenging. Changing from tungsten to alternative materials typically requires extensive re-certification processes lasting months or years.

Industrial Manufacturing Impact

Manufacturing sectors using tungsten carbide face immediate productivity implications from supply constraints:

The precision machining industry depends on tungsten carbide cutting tools that provide productivity advantages justifying premium pricing, yet supply shortages could force manufacturers to accept reduced efficiency rather than halt production entirely.

Tool manufacturers report that tungsten carbide tools last significantly longer than alternatives while maintaining superior cutting precision. This performance difference translates to measurable productivity gains that justify higher material costs.

Regional Trade Pattern Disruptions

Export control implementation has created selective regional supply disruptions that demonstrate the geopolitical targeting underlying the policy framework. Different regions experience varying degrees of supply constraint based on strategic considerations, particularly regarding northern territory tungsten impacts.

Japan's Supply Constraint Case Study

Japan received 138 tonnes of APT exports during January-November 2025, representing 56.8% of China's total APT exports during this period. This concentration suggests selective supply allocation rather than blanket export restrictions. Japanese industrial manufacturers face particular vulnerability due to limited domestic tungsten resources and high dependence on specialised tungsten applications.

The selective nature of Japan's supply access indicates that export controls operate through diplomatic and strategic considerations beyond simple market mechanisms. Countries with stronger strategic relationships or greater leverage may maintain better supply access.

Alternative Trade Route Development

Supply constraints have accelerated efforts to develop alternative tungsten trade routes. Companies are exploring sourcing arrangements with non-Chinese producers, despite higher costs and lower availability. This supply chain diversification represents a structural shift that may persist beyond current export control periods.

Table: Regional Tungsten Dependency Analysis

| Region | Import Dependence on China | Strategic Vulnerability | Alternative Options |

|---|---|---|---|

| Japan | 85-90% | High defense/aerospace exposure | Limited domestic recycling |

| Europe | 75-80% | Manufacturing tool dependence | African supplier development |

| North America | 70-75% | Defense procurement concerns | Domestic project revival |

Investment Implications and Opportunity Assessment

The tungsten supply crisis creates complex investment dynamics combining immediate pricing benefits for existing producers with long-term opportunities for alternative supply development. However, these opportunities carry significant risks requiring careful evaluation as part of broader critical minerals energy security considerations.

Non-Chinese Project Development Challenges

Tungsten projects outside China face multiple barriers that explain why Chinese dominance developed and persisted. Key challenges include:

• High capital intensity for processing facility development

• Environmental compliance requirements increasing operational costs

• Technical complexity of specialised tungsten processing

• Limited access to downstream markets controlled by Chinese companies

• Extended development timelines creating execution risk

Projects like Viking Mines' Linka Tungsten Project in Nevada demonstrate both the opportunity and challenges. Viking's metallurgical testing achieved 22.9% tungsten trioxide concentration from 1.4% feed grade using simple gravity separation. This 16x concentration factor suggests potentially favourable processing economics, yet the company remains pre-revenue with typical early-stage project risks.

Market Timing and Position Sizing Considerations

Current tungsten supply constraints create elevated pricing that may not persist indefinitely. Investors must consider several timing factors:

- Chinese policy duration: Export controls may be temporary diplomatic tools rather than permanent policy

- Alternative supply response: Higher prices incentivise development of competing supply sources

- Demand substitution: Persistent high prices may accelerate research into alternative materials

- Inventory dynamics: Companies may have built strategic stockpiles that temporarily offset supply constraints

Position sizing becomes crucial given the speculative nature of many tungsten investment opportunities. Viking Mines surged 200% following positive metallurgical results, yet trades at A$0.02 per share with typical micro-cap exploration risks.

The next major ASX story will hit our subscribers first

Technological Processing Barriers and Supply Chain Complexity

Tungsten supply chains involve multiple specialised processing stages that create natural barriers to market entry. Understanding these technical requirements explains why Chinese dominance proved durable and why alternative supply development faces significant challenges.

APT Processing Specialisation

Ammonium paratungstate production represents the critical bottleneck in tungsten supply chains. APT processing requires:

• Specialised chemical processing equipment with corrosion resistance

• Environmental compliance systems for chemical waste management

• Technical expertise in tungsten chemistry and purification

• Quality control systems meeting aerospace and defense specifications

These requirements create high barriers to entry that explain why few facilities globally possess commercial-scale APT production capabilities. Chinese facilities developed these capabilities over decades with government support and environmental flexibility not available in many other jurisdictions.

Downstream Product Differentiation

Different tungsten end-uses require distinct processing pathways and quality specifications:

Defense Applications: Ultra-high purity tungsten with specific grain structures

Aerospace Components: Tungsten alloys meeting stringent certification requirements

Industrial Tools: Tungsten carbide with optimised hardness characteristics

Electronics: Tungsten wire with precise dimensional tolerances

This product differentiation means China export controls on tungsten affect different market segments unequally. Defense and aerospace applications face the greatest substitution challenges due to performance requirements and certification barriers.

Long-Term Strategic Scenario Planning

The tungsten supply crisis represents one component of broader critical minerals competition between major powers. Understanding potential long-term scenarios helps investors and policymakers prepare for various outcomes as part of the broader pivot in critical minerals.

What happens if China maintains sustained export restrictions?

If China maintains current export control levels for multiple years, several outcomes become likely:

• Tungsten prices remain elevated, incentivising alternative supply development

• Western governments increase strategic stockpiling and domestic project support

• Aerospace and defense contractors invest in tungsten recycling capabilities

• Research accelerates into alternative materials for critical applications

This scenario creates the strongest investment case for non-Chinese tungsten projects, despite high development risks and capital requirements.

How would graduated policy normalisation affect markets?

China may gradually increase export quotas in response to diplomatic pressure or economic considerations. This approach would:

• Maintain price premiums while avoiding severe supply disruptions

• Slow development of competing supply sources by reducing incentives

• Preserve Chinese strategic leverage while minimising retaliation risks

• Create uncertainty that complicates investment planning for alternative projects

Could China expand critical minerals control?

China could extend similar export controls to additional critical minerals, creating broader supply chain vulnerabilities:

• Coordinated restrictions on rare earth elements, lithium, and graphite

• Systematic leverage over clean energy and defense supply chains

• Accelerated Western government response through strategic alliances

• Fundamental restructuring of global critical minerals trade patterns

Policy Response and International Coordination Frameworks

Western governments recognise tungsten supply vulnerability as a strategic national security concern requiring coordinated policy response. Multiple initiatives are developing to address critical mineral dependencies, particularly considering US tariff effects on minerals.

Strategic Stockpiling Initiatives

Government stockpiling programmes aim to buffer supply disruptions while alternative sources develop. Key considerations include:

• Optimal stockpile sizes balancing storage costs against supply security

• Product form selection (tungsten ore, APT, or finished products)

• Release mechanisms during supply crises to stabilise markets

• International coordination to avoid competitive stockpiling

Domestic Project Support Mechanisms

Policy support for domestic tungsten projects may include:

• Loan guarantees reducing project financing costs

• Tax incentives for domestic tungsten processing facilities

• Research funding for tungsten processing technology development

• Strategic purchasing commitments providing revenue certainty

These support mechanisms could significantly improve the economics of projects like Viking Mines' Nevada operation, though implementation timelines remain uncertain.

International Alliance Development

Critical mineral security alliances are emerging to coordinate supply chain diversification:

• Technology sharing agreements for tungsten processing

• Joint funding for alternative supply source development

• Diplomatic coordination on export control responses

• Trade agreement provisions protecting critical mineral access

Risk Assessment and Investment Framework

The tungsten investment opportunity combines compelling fundamental drivers with significant execution risks. Successful investment requires careful risk assessment and appropriate position sizing in the context of broader supply chain uncertainties.

What are the primary investment risks?

Policy Reversal Risk: China export controls on tungsten could be relaxed if diplomatic pressures intensify or economic costs become excessive. This policy reversal would likely cause tungsten prices to decline rapidly, negatively impacting alternative project economics.

Technical Execution Risk: Tungsten projects face complex metallurgical challenges that may prove more difficult or expensive than initial testing suggests. Viking Mines' positive metallurgical results, while encouraging, represent early-stage testing that may not translate to commercial-scale operations.

Market Timing Risk: Current elevated tungsten prices create attractive project economics, but development timelines of 3-5 years mean projects will enter production under potentially different market conditions.

Capital Intensity Risk: Tungsten processing requires substantial capital investment with limited flexibility if market conditions deteriorate. Unlike some mining operations, tungsten processing facilities cannot easily pivot to alternative commodities.

How should investors assess opportunities?

Successful tungsten investment requires evaluation across multiple dimensions:

Resource Quality: Projects with high-grade deposits and favourable metallurgy offer the best cost position

Processing Capability: Access to APT processing technology and expertise creates competitive advantage

Market Access: Established relationships with defense and aerospace customers provide revenue security

Government Support: Projects in jurisdictions offering policy support face lower development risk

Management Experience: Teams with proven tungsten development experience improve execution probability

The combination of China export controls on tungsten, limited alternative supply sources, and critical application dependencies creates a compelling investment theme. However, the speculative nature of early-stage projects requires careful position sizing and risk management. Investors should focus on the most advanced projects with proven metallurgy, experienced management teams, and supportive policy environments to maximise success probability while managing downside risk.

Investment decisions involving tungsten projects carry significant risks including commodity price volatility, technical execution challenges, and regulatory uncertainties. Investors should conduct thorough due diligence and consider position sizing appropriate to their risk tolerance and investment objectives.

Looking to Capitalise on Critical Mineral Market Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications when significant ASX mineral discoveries are announced, including strategic metals like tungsten facing global supply constraints. With China's export controls creating unprecedented opportunities for alternative suppliers, subscribers gain immediate access to actionable insights that could position them ahead of major market movements in critical minerals sectors.