July 24, 2026

The Invisible Mineral Holding AI Manufacturing Hostage

Long before a graphics processing unit renders a single AI inference, thousands of microscopic manufacturing steps determine whether it ever reaches a data centre. Among the most chemically demanding of those steps is the deposition of tungsten interconnects, the conductive wiring embedded within chips built on the world's most advanced processing nodes. This process depends entirely on one ultra-pure specialty gas: tungsten hexafluoride (WF₆). Right now, China tungsten export curbs on Japan's AI chip supply chain are fracturing this supply in ways that carry serious consequences for AI hardware production across Asia.

The fracture point is not a factory fire or a shipping accident. It is a deliberate, policy-driven tightening of China's tungsten exports, a move that is exposing just how deeply embedded single-source mineral dependencies remain in advanced semiconductor manufacturing, despite years of supply chain resilience rhetoric following earlier geopolitical shocks.

When big ASX news breaks, our subscribers know first

Tungsten Hexafluoride: The Specialty Gas at the Centre of the Crisis

Why WF₆ Cannot Simply Be Swapped Out

Understanding the severity of this disruption requires first appreciating what makes WF₆ so difficult to replace. This is not a commodity chemical. Semiconductor-grade WF₆ must meet five-nines purity standards, meaning 99.999% chemical purity, before it can be used in chip fabrication. At that specification, the field of qualified global producers is extraordinarily narrow.

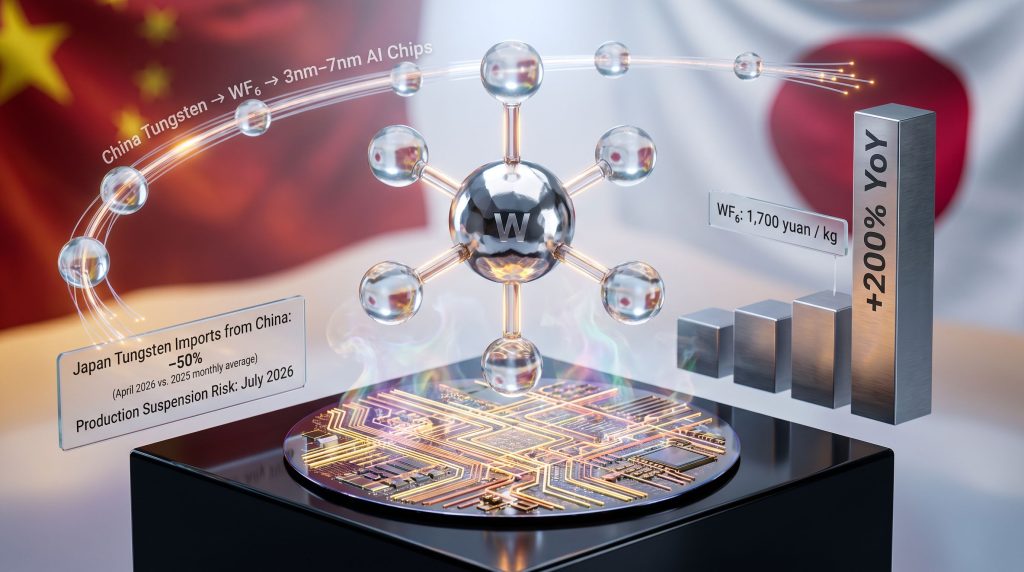

The gas functions as a chemical vapour deposition precursor, enabling the formation of tungsten-based conductive interconnects inside advanced logic chips manufactured on 3nm to 7nm processing nodes. These are the exact technology generations powering modern AI accelerators, high-performance computing chips, and GPU-class processors. Without WF₆ meeting the required purity threshold, the internal wiring of these chips simply cannot be formed using current fabrication architectures.

There is no commercially deployed substitute at scale. Research into alternative interconnect materials exists, however qualification of entirely new process chemistries within active chip production lines is measured in years, not months. Furthermore, processing bottlenecks in critical minerals like tungsten compound this challenge considerably, making rapid pivots even less feasible.

The Cost Structure That Makes China's Position So Powerful

The upstream economics of WF₆ production make the current supply situation particularly acute. Tungsten powder, the raw mineral input refined into the gas, accounts for more than 60% of WF₆ production costs, according to analysis published by Citic Securities earlier this year. This means that whoever controls tungsten powder controls the primary cost lever in the entire specialty gas supply chain.

China controls that lever overwhelmingly. The country accounts for an estimated 80% or more of global tungsten production and holds the world's largest reserve base. Tungsten's strategic importance has consequently become impossible to overstate in the context of modern chip manufacturing.

The pricing consequences of supply tightening have been severe. Five-nines WF₆ has surged to more than 1,700 yuan (approximately US$251) per kilogram, representing a year-on-year increase exceeding 200%, according to data from ibuychem, a Guangzhou-based industry portal. That kind of price movement in a specialty chemical used in high-volume chip production is not an inconvenience; it is a structural cost shock with direct implications for foundry economics.

How China's Export Controls Are Transmitting Through the Supply Chain

From Mineral Restriction to Production Suspension Risk

Japan's April 2026 tungsten imports from China fell approximately 50% compared to the 2025 monthly average, as reported by Nikkei Asia in late May. That figure is not the result of weak demand; Japan's chip-related chemical manufacturers are operating in a period of elevated demand driven by the global AI infrastructure buildout. The import decline reflects constrained supply availability at the source.

The downstream consequences have already reached the level of formal production risk notifications. Showa Denko Kanto and Central Glass, two major Japanese producers of semiconductor-grade specialty gases, have indicated potential production suspensions beginning July 2026 as their WF₆ inventories decline toward critical levels, according to reporting by The Elec, a South Korean electronics industry publication. Both firms have reportedly notified major chip manufacturers, including Samsung Electronics and DB HiTek, of potential supply disruptions.

The transmission pathway from Chinese mineral policy to AI chip production risk looks like this:

- China tightens tungsten export licensing and availability

- Tungsten powder supply to Japanese WF₆ producers tightens

- WF₆ production costs surge as raw material availability falls

- Japanese specialty gas producers exhaust inventory buffers

- Production suspension risk emerges for July 2026

- Supply disruption notifications reach South Korean chip manufacturers

- Advanced node chip output faces potential volume constraints

Japan's Structural Inability to Pivot Quickly

Japanese firms have actively sought alternative tungsten sources, but the structural barriers are formidable. The combination of China's reserve concentration and its processing infrastructure advantages means that non-Chinese producers cannot rapidly absorb displaced demand at competitive pricing or sufficient volume.

Beyond raw availability, there is a qualification problem. Semiconductor-grade material suppliers must pass rigorous qualification processes before their products can be accepted into active chip production lines. These processes are not accelerated simply because a supply emergency exists. Consequently, the institutional inertia of qualification timelines, which can extend across multiple quarters, means that even a willing alternative supplier cannot bridge a near-term supply gap quickly.

China's Critical Mineral Playbook: A Documented Pattern

The tungsten situation does not exist in isolation. China's export restrictions on critical minerals have been employed across several geopolitical episodes, each following a recognisable pattern of supply tightening, price escalation, and downstream production risk.

| Mineral | Year of Restriction | Primary Target | Mechanism |

|---|---|---|---|

| Rare earths | 2010 | Japan | Export embargo during territorial dispute |

| Gallium and germanium | 2023 | Western chip supply chains | Export licensing requirements |

| Antimony and graphite | 2023-2024 | Broad industrial targets | Additional export controls |

| Tungsten | 2025-2026 | Japan, AI chip supply chains | Export constraint contributing to supply tightening |

The 2010 rare earths episode is the most instructive precedent. China's decision to curtail rare earth exports to Japan during the Senkaku Islands territorial dispute demonstrated unambiguously that mineral supply chains could serve as instruments of geopolitical leverage. That event triggered a decade of diversification efforts across multiple governments and industries. Yet despite those efforts, specialty chemical segments serving advanced semiconductor manufacturing have retained significant single-source dependencies on Chinese mineral inputs.

Unlike a formal embargo, which creates a clear and legally defined disruption event, export controls operate through administrative mechanisms including licensing requirements, quota systems, and processing delays. According to analysis from the CSIS, this approach creates sustained uncertainty that is often more economically disruptive than an outright ban, as manufacturers cannot plan inventory strategy around an undefined duration of constraint.

The Dual Pressure System Squeezing Asia's Technology Supply Chain

Two Vectors, One Exposed Region

Japan's tungsten vulnerability exists within a broader dual-pressure framework now defining global semiconductor geopolitics. On one axis, China's export restrictions on critical minerals are creating upstream input risk for chip-adjacent manufacturers across Japan, South Korea, and Taiwan. On the other axis, U.S.-led advanced chip and equipment export controls are restricting China's access to leading-edge semiconductor technology.

| Pressure Vector | Source | Target | Primary Effect |

|---|---|---|---|

| Tungsten and critical mineral export curbs | China | Japan, South Korea, Taiwan | Supply tightening, price escalation, production risk |

| Advanced AI chip and equipment export controls | United States | China | Technology access restrictions |

| Selective equipment export exemptions | United States | Allied nations including Japan | Reinforcement of allied supply chain roles |

Japan occupies a uniquely exposed position within this framework. The country is a critical supplier of chip manufacturing equipment, with companies like Tokyo Electron central to the global semiconductor fabrication ecosystem. Yet Japan simultaneously depends heavily on Chinese mineral inputs for the specialty chemical production that feeds its own chip industry. This creates a complex exposure profile: strategically valuable to allied technology blocs, yet structurally vulnerable to upstream mineral leverage from China.

What the AI Boom Has Changed About Industrial Mineral Risk

One underappreciated dimension of the current crisis is how the AI chip manufacturing boom has fundamentally elevated the strategic profile of minerals that were previously considered low-profile industrial inputs. The broader critical minerals demand surge driven by AI infrastructure investment has concentrated risk in precisely the advanced node technologies most dependent on specialty process chemistries.

This recalibration of strategic mineral importance is likely to extend beyond tungsten. Any chemical element or compound that serves as a non-substitutable input at a critical process step in advanced semiconductor manufacturing is, by definition, a potential leverage point. Indeed, the role of critical minerals in semiconductors is increasingly central to both national security planning and corporate supply chain strategy.

Near-Term and Structural Risk Outlook

Timeline of Escalating Exposure

"Inventory buffers for specialty gases like WF₆ are finite, and the qualification of alternative suppliers cannot be compressed into a single quarter regardless of the urgency of the situation."

- 0 to 3 months: Elevated WF₆ pricing, continued inventory drawdowns at Japanese specialty gas producers, potential production rate reductions at affected foundries, and possible spot shortages

- 3 to 12 months: Accelerated qualification programmes for alternative tungsten suppliers, potential government-to-government raw material negotiations among allied nations, and strategic stockpiling considerations

- 12 months and beyond: Structural reconfiguration of tungsten and WF₆ supply chains, investment in non-Chinese tungsten processing capacity, and long-term research into alternative interconnect chemistries for future technology nodes

Which Parts of the AI Chip Ecosystem Face the Greatest Exposure?

Not all semiconductor products carry equal WF₆ exposure. The risk is most concentrated in segments where advanced node manufacturing and high chip complexity intersect.

- Advanced logic chips at 3nm to 7nm nodes carry the highest WF₆ intensity per unit and face the greatest direct disruption risk

- AI accelerators and GPU-class processors, predominantly manufactured at these advanced nodes, face direct implications for deployment timelines if foundry output is constrained

- High-bandwidth memory and advanced DRAM carry secondary exposure through related process chemistry dependencies

- Mature node chips used in automotive and industrial applications face lower but non-trivial indirect risk as supply chain stress propagates

The next major ASX story will hit our subscribers first

Frequently Asked Questions

What is tungsten hexafluoride and why does it matter for AI chips?

Tungsten hexafluoride is a specialty gas used as a chemical vapour deposition precursor in semiconductor fabrication. It enables the formation of microscopic tungsten-based conductive connections inside advanced chips built on 3nm to 7nm processing nodes, the technology generations used in leading AI accelerators and high-performance processors. At these nodes, WF₆ is a critical and non-substitutable process input under current manufacturing architectures.

Why has the price of WF₆ increased so dramatically?

The more than 200% year-on-year price increase reflects a convergence of supply-side compression and demand-side acceleration. China's export restrictions have tightened tungsten powder availability, the raw material representing more than 60% of WF₆ production costs. Simultaneously, the global AI chip manufacturing boom has driven elevated demand for advanced node fabrication capacity, increasing consumption of WF₆ at precisely the moment supply is being constrained.

Can Japan realistically diversify its tungsten sourcing?

Diversification is a long-term structural project, not a near-term solution. China's dominance of global tungsten reserves and processing infrastructure means alternative producers lack the scale, processing capacity, and qualification history to rapidly absorb displaced Japanese demand at the required purity grades. Furthermore, according to congressional research on supply chain resilience, qualification timelines alone create multi-quarter delays even when willing alternative suppliers exist.

How similar is this to China's 2010 rare earths embargo?

The structural dynamics are closely analogous. Both situations involve China's dominant position in a critical mineral supply chain translating into supply disruption and price escalation for Japanese downstream manufacturers through export restriction mechanisms. The primary distinction is the end-market sensitivity: the China tungsten export curbs on Japan's AI chip supply chain are concentrated in the strategically critical AI chip manufacturing sector, amplifying their geopolitical significance relative to the broader industrial applications affected in 2010.

Key Takeaways for Understanding AI Supply Chain Fragility

- Single-source mineral dependencies remain embedded in advanced semiconductor supply chains despite prolonged diversification efforts following the 2010 rare earths episode

- Specialty chemical intermediaries, particularly process gases like WF₆, represent critically underappreciated chokepoints in AI hardware production

- China's export control toolkit has expanded well beyond rare earths, with tungsten representing the latest critical mineral capable of transmitting supply chain stress into advanced chip manufacturing

- The AI infrastructure boom has elevated the strategic importance of previously overlooked industrial minerals, reconfiguring the risk map for supply chain planners and policymakers

- Japan's dual role as a critical chip equipment supplier and a mineral-import-dependent specialty chemical producer creates a complex and structurally exposed position within the current technology supply chain landscape

This article contains forward-looking assessments and supply chain projections that involve uncertainty. Actual outcomes may differ materially from scenarios described.

Want To Track The Next Critical Mineral Discovery Before The Market Moves?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across tungsten, rare earths, and more than 30 other commodities — turning complex geological data into actionable investment insights. Explore historic discoveries and their exceptional returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next major critical minerals story.