June 10, 2026

China zinc concentrate treatment charges represent a critical pricing mechanism in global base metals markets, where complex negotiations between miners and processors determine value distribution throughout the zinc supply chain. The treatment charge framework operates as a fee structure compensating smelters for converting raw concentrate into refined metal, creating intricate economic relationships that extend far beyond simple cost recovery calculations.

Understanding these dynamics requires examining institutional architectures governing price discovery, particularly where geographic concentration creates asymmetric bargaining power. The zinc concentrate processing industry exemplifies this phenomenon, with smelting capacity concentration in specific regions enabling coordinated approaches that influence global trade flows and mining project economics.

Understanding the Fundamentals of Zinc Concentrate Processing Economics

The treatment charge framework in zinc processing operates as a revenue sharing mechanism between mining companies and smelters. Concentrate typically contains 50-55% zinc content alongside valuable byproducts including silver and lead, creating complex economic calculations extending beyond base metal recovery alone.

Treatment charges function inversely to market conditions. When concentrate supply tightens, smelters compete by reducing charges or offering negative rates, effectively paying miners for superior-grade concentrates. Conversely, abundant availability strengthens smelter negotiating positions, enabling higher treatment charge demands.

Geographic pricing structures add complexity to this framework. Chinese domestic operations quote charges in yuan per metric tonne of zinc content, while imported material trades in USD per dry metric tonne of concentrate. This distinction reflects quality standards, logistics costs, and currency risk factors influencing cross-border trade dynamics.

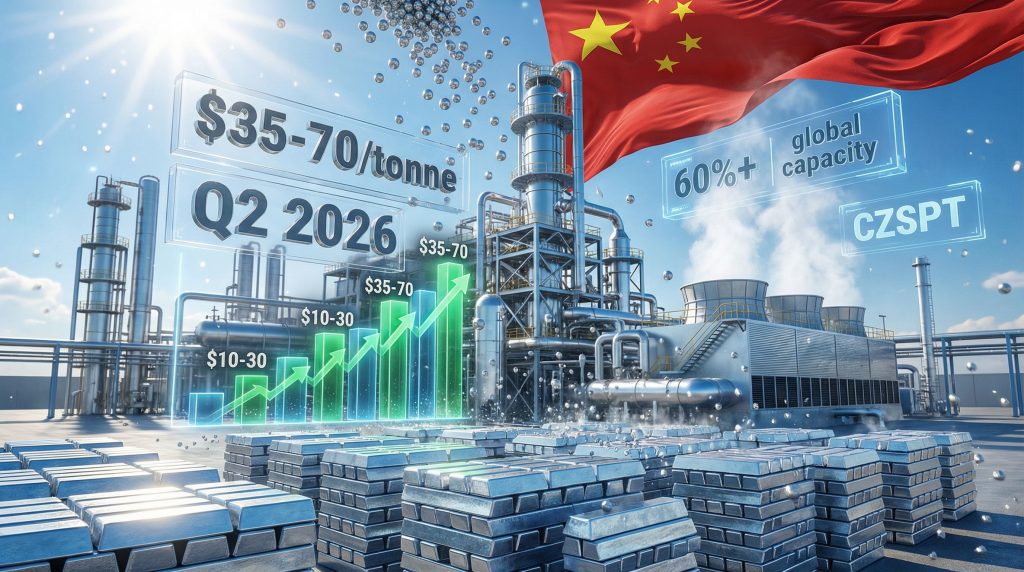

Current market conditions demonstrate these principles practically. China zinc concentrate treatment charges for Q2 2026 were set at $35-70 per tonne by the China Zinc Smelter Purchase Team during their March 25, 2026 meeting in Chengdu. This represents a significant $60 per tonne decline from Q1 2026 guidance of $105-120 per tonne.

Treatment Charges as Market Barometers

Treatment charge movements serve as sensitive indicators of supply-demand balance in concentrate markets. Unlike direct commodity prices impact, treatment charges reflect processing capacity utilization and feed material availability in real-time.

Market participants characterize current conditions as maintaining tight equilibrium without shortage scenarios. This distinction separates balanced markets from genuine scarcity situations that drive charges to minimal levels.

Spot market dynamics reveal this sensitivity clearly. Zinc concentrate spot treatment charges reached $0-30 per tonne cif China by March 13, 2026, declining from $10-50 per tonne on February 27. Some premium-grade concentrates with higher byproduct content traded at zero or negative treatment charges.

The inverse relationship between ore availability and smelter bargaining power creates cyclical patterns. Historical data shows guidance levels rising from $10-30 per tonne in Q1 2025 to peak at $120-140 per tonne in Q4 2025 before moderating to current levels.

When big ASX news breaks, our subscribers know first

China's Zinc Smelting Landscape: Market Structure and Dominance

China's position in global zinc processing extends beyond capacity leadership, encompassing institutional mechanisms shaping international concentrate trade flows. The country operates approximately 60% of global zinc smelting capacity, creating concentrated market power enabling coordinated pricing and procurement strategies.

This dominance stems from integration with massive domestic consumption markets, particularly galvanizing operations supporting construction and infrastructure sectors. Zinc consumption correlates directly with steel production levels and urbanization rates, creating predictable demand patterns supporting large-scale investments.

Furthermore, strategic importance of zinc in infrastructure development provides context for China's market position. Galvanized steel applications generate steady demand justifying significant processing capacity investments. This domestic demand base reduces export dependence and strengthens negotiating positions with international suppliers.

The China Zinc Smelter Purchase Team's Market Influence

The China Zinc Smelter Purchase Team represents a unique institutional mechanism coordinating market expectations and purchasing strategies. This organisation convenes quarterly to establish treatment charge guidance ranges functioning as benchmarks for international pricing.

The CZSPT's March 25, 2026 meeting exemplifies this process, producing the $35-70 per tonne Q2 guidance influencing global trade negotiations. This collective bargaining approach enables Chinese smelters to present unified positions, reducing internal competition and strengthening leverage with mining companies.

Market coordination extends beyond price setting to encompass quality preferences and procurement priorities. Chinese smelters demonstrate clear preferences for concentrates with higher byproduct content, recognising superior economics from silver and lead recovery. This preference structure influences global trade flows as miners adjust marketing strategies.

The CZSPT guidance progression demonstrates institutional responsiveness to changing conditions, particularly considering the broader impact of China commodity trends on processing economics.

| Quarter | TC Guidance (USD/tonne) | Market Conditions |

|---|---|---|

| Q4 2025 | $120-140 | Peak winter stockpiling |

| Q1 2026 | $105-120 | Inventory adjustment period |

| Q2 2026 | $35-70 | Supply rebalancing expectations |

Current Market Dynamics: Analyzing Q2 2026 Treatment Charge Factors

The $35-70 per tonne guidance range reflects multiple converging factors distinguishing current conditions from 2025 patterns. Supply characterisation as tight but balanced indicates equilibrium without shortage conditions, representing middle ground between abundance and scarcity scenarios.

Several key factors underpin this guidance level. Concentrate supply remains constrained relative to 2025 availability but avoids critical shortage conditions. Geopolitical tensions affecting Middle East shipping routes create procurement urgency without eliminating material availability. Domestic Chinese zinc production has stabilised following winter seasonal patterns.

Byproduct economics continue influencing smelter purchasing decisions significantly. Higher silver and lead content concentrates command preferential treatment charges, reflecting superior overall economics from multi-metal recovery operations. This quality differentiation creates tiered pricing structures where premium concentrates trade at substantially different levels.

Real-Time Spot Market Indicators

Spot market pricing reveals real-time supply pressures with greater sensitivity than quarterly guidance mechanisms. Current spot levels trading below official guidance ranges indicate expectations of improving availability or reduced procurement urgency.

Regional pricing variations within China demonstrate localised supply-demand dynamics. These differences reflect distinct logistics networks, smelter concentration patterns, and local demand characteristics. Moreover, concerns about tariffs impact markets add complexity to cross-border trade calculations.

February 27, 2026 Domestic Treatment Charges:

- North China: 1,500-1,700 yuan per tonne ($217-246 USD), down 5.88% month-on-month

- South China: 1,300-1,600 yuan per tonne ($188-231 USD), up 7.41% month-on-month

Negative treatment charge occurrences for premium-grade concentrates highlight quality differentiation in pricing mechanisms. Smelters effectively pay miners for superior feed material when overall economics from byproduct recovery exceed standard treatment charge levels.

Geographic Risk Assessment: Middle East Supply Chain Vulnerabilities

Geopolitical tensions in the Middle East create specific vulnerabilities for zinc concentrate trade flows, particularly affecting Iran-origin material shipments. These disruptions illustrate how geographic concentration of supply sources can amplify market volatility despite relatively small physical impact.

Iran-origin zinc concentrate represents a significant portion of seaborne trade to China, making shipping route disruptions particularly relevant for smelter procurement strategies. Current tensions have created logistical bottlenecks and increased freight costs, though alternative routing options provide mitigation mechanisms.

Market participants distinguish between psychological and physical impact on concentrate availability. While tensions generate procurement concern and risk premium incorporation, actual material shortages have not materialised. One market source noted tensions create psychological concern without preventing smelters from securing necessary feed material.

Geopolitical Risk Impact on Market Liquidity

Uncertainty surrounding geopolitical developments has reduced spot market liquidity as participants adopt more cautious trading approaches. Concerns over potential external disruptions and price volatility discourage aggressive offer acceptance, limiting transaction volumes and reducing price discovery efficiency.

This liquidity reduction manifests in wider bid-offer spreads and reduced transaction frequency, making spot market pricing less reliable as real-time indicators. However, the broader context of ongoing trade war impacts continues influencing strategic decision-making across the industry.

Risk premium incorporation varies by concentrate origin and shipping route exposure. Iran-origin material trades at discounts reflecting logistical complexity and delivery uncertainty, while concentrates from more stable regions command premiums for reliability assurance.

Historical Treatment Charge Evolution: Patterns and Cycles

Treatment charge progression throughout 2025-2026 demonstrates cyclical patterns influenced by seasonal demand, inventory management, and underlying supply-demand fundamentals. The trajectory from $10-30 per tonne in Q1 2025 to current levels reflects market maturation and supply rebalancing.

Peak treatment charges of $120-140 per tonne in Q4 2025 coincided with winter stockpiling activities and seasonal demand strength. This represents the highest levels in the recent cycle, reflecting temporary supply abundance relative to immediate consumption requirements.

The subsequent decline through Q1 2026 and Q2 2026 indicates market correction as inventory positions normalised and consumption patterns returned to sustainable levels. This progression suggests cyclical rather than structural shifts in concentrate availability.

Comparative analysis reveals treatment charge volatility correlates with broader economic cycles and infrastructure investment patterns. During robust construction activity periods, zinc concentrate demand strengthens, reducing treatment charge levels as smelters compete for feed material.

Market Maturity Indicators

Current treatment charge patterns suggest market maturation compared to immediate post-pandemic volatility. The Q2 2026 guidance range indicates moderate volatility expectations rather than extreme price swings characteristic of severely disrupted markets.

Institutional coordination through the CZSPT mechanism provides stability compared to purely spot-market-driven pricing. Quarterly guidance ranges enable market participants to plan procurement strategies with greater predictability, reducing transaction costs and operational uncertainty.

Long-term supply outlook considerations increasingly influence treatment charge expectations. New mine developments require multi-year lead times, making current China zinc concentrate treatment charges important signals for capital allocation decisions throughout the value chain.

Investment Implications and Strategic Considerations

Treatment charge movements directly impact mining company valuations through revenue calculations and project economics assessments. A $60 per tonne treatment charge decline translates to significant revenue changes for zinc producers depending on production volumes and contract structures.

Regional cost curve positioning affects different mining operations' sensitivity to treatment charge fluctuations. Low-cost producers maintain profitability across wider treatment charge ranges, while marginal operations face production decisions when charges rise significantly. Current levels favour mining operations compared to peak conditions.

Capital allocation decisions for expansion projects incorporate treatment charge expectations over project lifespans. Multi-year payback periods require assumptions about long-term treatment charge evolution, making current market signals important inputs for investment analysis and project development timing.

In addition, the broader mining industry evolution continues reshaping how companies approach treatment charge negotiations and operational strategies.

Downstream Industry Impact Assessment

Galvanizing sector margins face pressure from zinc price volatility and treatment charge fluctuations affecting refined metal availability and pricing. Construction industry input costs correlate with zinc market conditions through galvanised steel pricing, though treatment charges represent only one component.

Strategic stockpiling considerations for industrial consumers depend on treatment charge cycle expectations and refined metal price forecasts. Current market conditions suggest potential inventory building opportunities if charges continue declining and refined metal production increases correspondingly.

Supply chain resilience planning increasingly incorporates treatment charge volatility as a factor affecting refined metal availability and pricing predictability. Downstream industries develop procurement strategies balancing cost optimisation with supply security considerations.

The next major ASX story will hit our subscribers first

Risk Management and Hedging Strategies

Mining companies optimise treatment charge exposure through diverse approaches including concentrate quality enhancement, geographic sales diversification, and contract structure negotiation. Byproduct credit maximisation provides partial offset to treatment charge volatility through silver and lead value capture.

Long-term contract versus spot market exposure balancing enables miners to reduce volatility while maintaining flexibility for market optimisation. Current conditions favour increased spot market exposure given guidance levels below recent quarters, though geopolitical risk considerations support term contract preferences.

Operational flexibility in smelter selection provides additional risk management capability, enabling miners to optimise treatment charge terms across different geographic markets and contract timeframes. This requires maintaining relationships with multiple smelter counterparties and understanding regional pricing dynamics.

Financial Risk Mitigation Mechanisms

Treatment charge derivatives markets remain limited compared to base metal futures, restricting financial hedging options for direct exposure management. Most risk mitigation occurs through operational strategies rather than financial instruments specifically targeting treatment charge volatility.

Currency hedging strategies address USD-yuan exchange rate exposure affecting treatment charge calculations and competitiveness between domestic Chinese and imported concentrate pricing. This becomes particularly relevant during periods of significant currency movement affecting relative economics.

Portfolio diversification across multiple concentrate types and markets provides natural hedging against treatment charge volatility in specific regions or product categories. Mining companies with diverse concentrate production capabilities can optimise sales allocation based on differentials.

Future Outlook: Technology and Market Evolution

Electric vehicle battery demand growth creates additional zinc consumption channels through galvanised steel applications in automotive manufacturing and charging infrastructure development. This demand diversification affects long-term treatment charge evolution through consumption pattern changes.

Infrastructure investment cycles in emerging markets provide growth opportunities for zinc consumption, particularly in construction and transportation sectors requiring galvanised steel applications. These demand drivers influence treatment charge expectations through their impact on refined zinc consumption requirements.

Environmental regulations affecting smelter operations create capacity constraints that strengthen treatment charge negotiations for remaining processors. Compliance costs and operational restrictions may reduce effective smelting capacity, improving economics for remaining operators.

Furthermore, recent analysis of zinc market developments and comprehensive market intelligence continue highlighting the evolving landscape.

Technological Disruption Considerations

Alternative smelting technologies and process efficiency improvements affect treatment charge economics through operational cost reduction and byproduct recovery enhancement. Advanced processing techniques may enable economic treatment of lower-grade concentrates currently considered marginal.

Automation impact on labour cost components within treatment charge calculations creates potential for operational cost reduction and improved processing consistency. This technological progression affects competitive positioning among smelting operations globally.

Circular economy trends in zinc recycling represent long-term considerations for treatment charge evolution as secondary material processing competes with primary concentrate smelting for market share. Recycling economics and technology development influence future demand for concentrate processing services.

How do geopolitical tensions affect zinc concentrate markets?

Current Middle East tensions create psychological market impact exceeding physical supply disruption. Alternative shipping routes provide mitigation mechanisms, though uncertainty reduces spot market liquidity and increases risk premium incorporation in pricing decisions.

What determines the difference between domestic and imported zinc concentrate treatment charges?

Domestic Chinese treatment charges quote in yuan per metric tonne of zinc content, while imported material uses USD per dry metric tonne of concentrate. This reflects different quality standards, logistics costs, and currency risk factors affecting cross-border trade economics.

Why do some concentrates trade at negative treatment charges?

Premium-grade concentrates with valuable byproducts command negative treatment charges when overall economics from silver and lead recovery exceed processing costs. Smelters effectively pay for superior feed material that enhances profitability through byproduct credits.

Consequently, China zinc concentrate treatment charges will continue evolving based on supply-demand fundamentals, geopolitical developments, and institutional coordination mechanisms. Market participants must monitor these dynamics closely for strategic decision-making and operational planning purposes.

This analysis represents market conditions and participant perspectives as of April 2026. Treatment charge dynamics continue evolving based on supply-demand fundamentals, geopolitical developments, and institutional coordination mechanisms. Readers should consult current market data and professional analysis for investment and operational decision-making.

Ready to capitalise on the next zinc discovery breakthrough?

Discovery Alert's proprietary Discovery IQ model delivers instant alerts on significant ASX mineral discoveries, including zinc prospects that could benefit from favourable treatment charge conditions and Chinese market dynamics. Explore historic examples of major discoveries that delivered substantial returns to early investors, then begin your 14-day free trial today to position yourself ahead of the market with real-time intelligence on emerging opportunities.