August 6, 2026

The Structural Foundation of Global Resource Dependencies

Strategic control over critical materials rarely emerges from territorial ownership alone. Instead, it develops through systematic capture of processing capacity, technological expertise, and supply chain integration points that transform raw resources into usable industrial inputs. This phenomenon has reached unprecedented scale across global mineral markets, where China's critical minerals dominance has established commanding positions in refining operations for nearly twenty essential materials that underpin modern manufacturing.

The dynamics of this concentration reveal themselves most clearly in the disconnect between extraction geography and processing control. Mining operations may be distributed across multiple continents, yet the conversion of ore into battery chemicals, aerospace alloys, and semiconductor materials flows through remarkably narrow channels of specialised industrial capacity.

When big ASX news breaks, our subscribers know first

The Hidden Architecture of China's Resource Dominance

Beyond Mining: The Processing Monopoly That Matters

China's critical minerals dominance operates through a sophisticated strategy that prioritises control over processing and refining rather than raw material extraction. According to the International Energy Agency's 2024 Critical Minerals Market Review, China maintains leading refining positions across 19 of 20 strategic minerals, with market share concentrations averaging approximately 70% in key materials including lithium, cobalt, graphite, and rare earth elements.

This processing-focused approach creates deeper strategic leverage than mining control because it positions China as the gatekeeper for final products. Raw ore from Australia, Africa, or South America must typically pass through Chinese refineries before reaching battery manufacturers, electronics producers, or aerospace companies worldwide.

| Material | China Mining Share | China Processing Share | Strategic Impact |

|---|---|---|---|

| Lithium | 13% | 70% | Battery chemicals |

| Cobalt | 3% | 65% | Cathode materials |

| Graphite | 65% | 90% | Anode production |

| Rare Earths | 60% | 85% | Permanent magnets |

| Manganese (High-Purity) | 25% | 90% | Battery cathodes |

The processing monopoly creates multiple strategic advantages:

• Quality Control: Specifications for battery-grade chemicals and aerospace alloys require precise manufacturing tolerances that Chinese facilities have optimised over decades

• Cost Structure: Integrated supply chains from ore processing to finished materials provide significant cost advantages

• Supply Chain Lock-In: Downstream manufacturers develop technical relationships and logistics arrangements that become difficult to replicate elsewhere

• Export Control Leverage: Processing operations can be throttled through licensing, quality standards, or direct export restrictions without affecting mining countries

Furthermore, this approach demonstrates how geopolitical influence can be exercised through strategic control mechanisms rather than territorial acquisition.

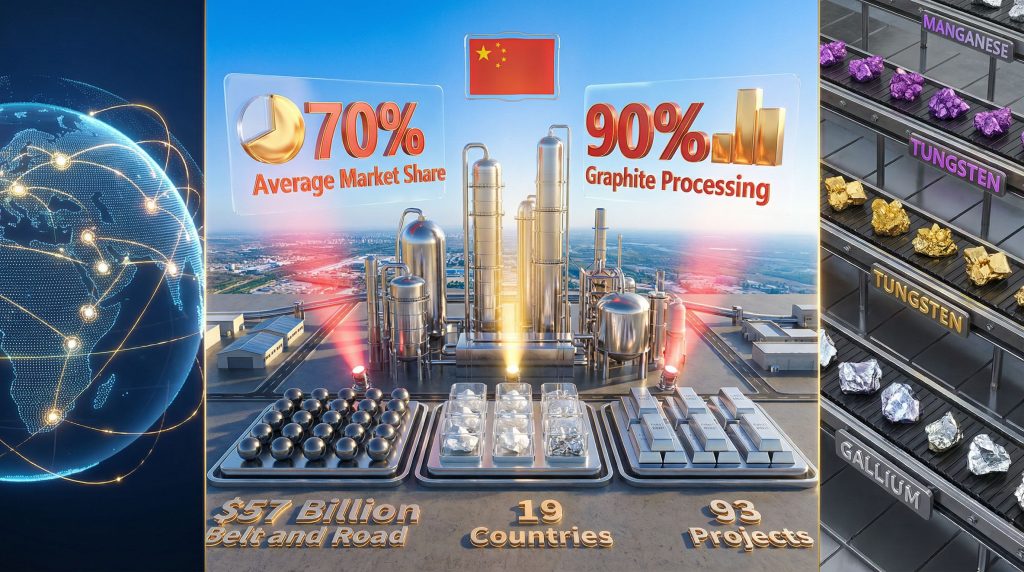

The $57 Billion Belt and Road Minerals Strategy

However, China's upstream mineral investments through Belt and Road Initiative projects have systematically targeted strategic materials across 93 documented mining projects in 19 countries between 2000 and 2021, according to analysis from Johns Hopkins SAIS China-Africa Research Initiative. These investments focus particularly on copper, cobalt, nickel, lithium, and rare earth extraction sites that feed into Chinese processing operations.

Geographic Distribution of Chinese Mining Investments:

• Africa: 47 projects, primarily cobalt (DRC), copper (Zambia), and rare earths (various)

• Southeast Asia: 23 projects, focusing on nickel (Indonesia) and rare earth processing

• Latin America: 15 projects, targeting lithium (Chile/Argentina) and copper operations

• Central Asia: 8 projects, emphasising rare earth and uranium resources

This investment pattern creates vertical integration from extraction through processing, ensuring that even non-Chinese mining operations often channel materials through Chinese-controlled refining capacity. The strategy effectively captures value-added processing stages while distributing political risks associated with resource extraction across multiple jurisdictions.

Which Critical Minerals Give China Maximum Strategic Leverage?

Tier 1 Chokepoint Materials: The "Big Five"

Graphite: The 90% Battery Bottleneck

Natural graphite represents one of China's most complete supply chain monopolies, particularly in battery-grade spherical graphite production where Chinese facilities control approximately 90% of global capacity according to USGS data. This dominance extends beyond simple market share to encompass the specialised technical processes required for lithium-ion battery anodes.

Processing Complexity and Barriers:

The conversion from raw graphite ore to battery-grade spherical graphite involves multiple sophisticated steps:

• Purification: Acid leaching and thermal treatment to achieve >99.95% purity levels

• Spheroidisation: Mechanical shaping to precise particle sizes (~25 micrometers)

• Surface Coating: Silicon oxide or carbon coating for electrochemical performance

• Quality Control: Particle size distribution and surface area verification (5-15 m²/g)

These technical requirements create natural barriers to competition, as the specialised equipment and process knowledge represent significant capital investments with long development timelines. Battery manufacturers require consistent quality specifications that new facilities cannot easily replicate without extensive R&D periods.

Market Impact of Export Controls:

In addition, China's export controls implementation of graphite export licensing in September 2023, maintained through 2024, demonstrated immediate supply chain vulnerability. USGS reported measurable declines in Chinese graphite exports during 2024, leading to price volatility and procurement delays across global battery supply chains.

The graphite shortage particularly affects electric vehicle production, where battery-grade spherical graphite comprises approximately 8-10% by weight of lithium-ion cells. In a typical 70 kWh EV battery, this translates to 560-700 kg of graphite equivalent per vehicle.

Lithium: The 70% Refining Stranglehold

China's critical minerals dominance operates through control of chemical conversion processes rather than mining operations. While Australia produces approximately 50% of global lithium ore (spodumene) and Chile contributes 23% through brine extraction, China controls roughly 70% of global lithium processing capacity for battery chemicals according to IEA analysis.

Processing Pathway Dependencies:

Spodumene Route (Hard-Rock):

- Ore mining and crushing in Australia/other locations

- Beneficiation to 6-8% Li₂O concentrate

- Roasting with lime and sulfuric acid (often in China)

- Leaching, purification, and precipitation

- Final production of lithium carbonate or hydroxide

Brine Route (South American Triangle):

- Brine extraction and evaporation (6-18 months)

- Concentration and chemical separation

- Conversion to battery-grade chemicals (often in China)

Both pathways frequently require Chinese processing capacity for the final conversion to battery-grade chemicals, creating strategic dependency regardless of mining location. This structure means that Australia lithium innovations as the world's largest lithium producer does not translate to supply chain independence for its allies.

Strategic Implications:

The IEA projects lithium demand will increase by 40x between 2020 and 2040 under net-zero scenarios, intensifying pressure on existing processing capacity. Current Chinese dominance in conversion chemistry positions Beijing to influence global electric vehicle deployment rates and energy storage development through processing capacity allocation.

Cobalt: The Congo-Beijing Supply Corridor

Cobalt illustrates how Chinese control extends beyond territorial boundaries through strategic positioning in key supply chains. The Democratic Republic of Congo (DRC) produces approximately 76% of global cobalt ore according to USGS data, yet much of this material flows through Chinese refineries before reaching battery manufacturers.

Supply Chain Structure:

• Primary Mining: DRC Copperbelt operations (76% global share)

• Intermediate Processing: Cobalt concentrate and hydroxide production

• Refining Control: Chinese facilities dominate conversion to battery-grade cobalt chemicals

• End-Use Integration: Battery cathode manufacturing concentrated in Asian facilities

This structure creates multiple dependency points where supply disruptions can propagate quickly through global battery supply chains. Even as battery manufacturers work to reduce cobalt intensity through chemistry modifications, absolute cobalt demand remains substantial due to electric vehicle scaling.

Defence and Aerospace Applications:

Beyond batteries, cobalt serves critical functions in superalloys for jet engines, gas turbines, and high-temperature applications in aerospace and defence manufacturing. Supply disruptions in refined cobalt availability directly impact procurement cycles for defence contractors and aerospace manufacturers.

High-Purity Manganese: The Invisible Dependency

While bulk manganese ore remains relatively abundant globally, battery-grade high-purity manganese represents a specialised product category where China maintains dominant processing positions. The distinction between commodity manganese and battery-grade manganese sulfate or electrolytic manganese metal (EMM) is crucial for understanding strategic vulnerabilities.

Processing Requirements for Battery Grade:

• Purity Standards: >99.9% manganese content for battery applications

• Chemical Form: Conversion to manganese sulfate monohydrate for cathode production

• Particle Specifications: Controlled size distribution and surface characteristics

• Energy Intensity: High-temperature processing requiring substantial electricity inputs

China's advantages in high-purity manganese processing stem from integrated supply chains, energy access, and specialised equipment that smaller producers cannot easily replicate. As battery manufacturers pursue "cobalt thrift" strategies through high-manganese chemistry development, this dependency may deepen rather than diminish.

Tungsten: The Defence Manufacturing Vulnerability

Tungsten represents a traditional strategic material that maintains contemporary relevance through defence manufacturing and industrial tooling applications. USGS data indicates China produces approximately 80% of global tungsten, with limited alternative sources at comparable scale and cost structures.

Critical Applications:

• Tungsten Carbide Tools: Cutting implements for aerospace and automotive manufacturing

• Defence Components: Hard-metal parts for munitions and military equipment

• Industrial Machinery: High-temperature applications in power generation and chemical processing

• Electronics: Specialised applications in semiconductors and lighting

China's 2025 expansion of export controls to include tungsten products demonstrates Beijing's willingness to leverage strategic material advantages. The relative concentration of tungsten supply makes diversification particularly challenging for Western manufacturers dependent on consistent quality and availability.

Tier 2 Strategic Materials Under Chinese Control

| Material | China Processing Share | Primary Applications | Strategic Concern |

|---|---|---|---|

| Gallium | >90% | Semiconductors, LEDs | Electronics manufacturing |

| Germanium | >80% | Fiber optics, infrared | Military and communications |

| Titanium (sponge) | 69-77% | Aerospace alloys | Defence manufacturing |

| Aluminum (primary) | 59% | Transportation, packaging | Industrial capacity |

| Antimony | 85% | Flame retardants, batteries | Fire safety, energy storage |

Recent export control expansions targeting gallium, germanium, and antimony exports to the United States demonstrate escalation patterns where Chinese authorities increasingly view strategic materials as policy tools rather than purely commercial commodities.

How Did China Build This Monopoly Position?

The Three-Phase Domination Strategy

Phase 1: Domestic Resource Development (1990s-2000s)

China's initial strategy focused on developing domestic mining and processing capacity while accepting environmental externalities that Western nations increasingly regulated. Lower environmental compliance costs and state-directed investment enabled rapid capacity scaling in energy-intensive refining processes.

Phase 2: Global Upstream Investment (2000s-2010s)

The Belt and Road Initiative and state-owned enterprise investments systematically targeted overseas mining operations, particularly in Africa and Latin America. These investments secured ore supplies while maintaining processing operations within Chinese territory, creating integrated supply chains under Chinese control.

Phase 3: Processing Capacity Scaling (2010s-Present)

Focus shifted to advanced processing capabilities and technological development in battery chemicals, high-purity materials, and specialised alloys. Chinese facilities achieved scale economies and technical expertise that competitors find difficult to replicate without substantial time and capital investments.

Competitive Advantages That Created Market Control

Regulatory Environment:

Chinese processing operations historically operated under less stringent environmental regulations than Western alternatives, reducing operational costs and permitting timelines. Energy-intensive refining processes benefited from subsidised electricity and fewer emissions constraints.

Integrated Supply Chain Development:

Chinese strategy emphasised vertical integration from mining through finished products, creating cost efficiencies and supply chain coordination that purely market-driven approaches struggled to match. State planning enabled long-term capacity investments without immediate profitability requirements.

Scale Economies and Learning Effects:

Early investments in processing capacity generated learning-by-doing effects and scale economies that reinforced competitive advantages. Technical expertise developed through repetitive production operations became difficult for new entrants to replicate quickly.

Government Subsidies and Strategic Coordination:

State support through subsidised loans, tax incentives, and direct investment enabled capacity development beyond what private market incentives would support. Strategic coordination across state-owned enterprises created integrated supply chains serving national objectives.

Why Western Countries Ceded This Ground

Environmental Regulations and NIMBY Effects:

Environmental regulations in Western jurisdictions pushed energy-intensive and potentially polluting processing operations offshore. Public opposition to mining and refining operations created political barriers to domestic capacity development.

Short-Term Cost Optimisation:

Market-driven decisions prioritised immediate cost savings over long-term supply chain security. Chinese processing offered lower costs, leading Western companies to outsource refining operations without considering strategic implications.

Underestimation of Processing as Strategic Chokepoint:

Policy makers focused on securing diverse mining sources while overlooking processing concentration risks. The assumption that raw materials availability ensured supply chain security proved incorrect when processing capacity became the binding constraint.

Market-Driven vs. State-Directed Resource Policies:

Western approaches relied on market mechanisms and private sector investment decisions, while China pursued state-directed strategic development. This asymmetry enabled China to make long-term investments that private markets would not support without guaranteed returns.

What Are the Real-World Consequences of This Dependency?

Supply Chain Vulnerability Assessment by Industry

Electric Vehicle Manufacturing

EV production depends on battery component supply chains where China's critical minerals dominance creates multiple vulnerability points:

Critical Dependencies:

• Battery Anodes: 90% dependent on Chinese spherical graphite processing

• Cathode Materials: 70% dependent on Chinese lithium chemical conversion

• Battery Systems: Cobalt and manganese processing concentrated in Chinese facilities

• Production Timeline: Supply disruptions can halt battery cell production within 30-90 days

Cost Implications:

Supply disruptions or export restrictions can increase battery material costs by 20-40% according to industry analysis. Alternative sourcing requires premium pricing and longer procurement timelines, directly impacting EV affordability and production targets.

Semiconductor and Electronics Manufacturing

The electronics sector faces concentrated dependencies in specialised materials essential for chip production and device manufacturing:

High-Risk Materials:

• Gallium: >90% Chinese processing for GaAs semiconductors and LEDs

• Germanium: >80% Chinese production for fiber optics and infrared applications

• Rare Earth Elements: 85% Chinese processing for permanent magnets in electronics

Manufacturing Location Misalignment:

While semiconductor fabrication occurs globally, critical input materials remain concentrated in Chinese processing facilities. This geographic mismatch creates strategic vulnerability even for domestic chip manufacturing operations.

Aerospace and Defence Manufacturing

Defence and aerospace industries require materials with precise specifications and consistent availability, making supply chain disruptions particularly problematic:

Critical Material Dependencies:

• Tungsten: 80% Chinese production for hard-metal defence applications

• Titanium Sponge: 70% Chinese processing for aerospace alloys

• Rare Earth Magnets: Essential for guidance systems, communications, and propulsion

National Security Implications:

Defence contractor supply chains face potential disruption scenarios that could affect weapons production, maintenance operations, and military readiness. Long procurement cycles in defence manufacturing amplify the impact of material supply interruptions.

Recent Export Control Demonstrations

December 2024 Comprehensive Restrictions:

China implemented comprehensive export bans on gallium, germanium, and antimony shipments to the United States, demonstrating willingness to weaponise strategic material advantages. These restrictions target semiconductor and defence manufacturing capabilities specifically.

Graphite Licensing and Market Effects:

Export licensing requirements for graphite products, implemented in September 2023 and maintained through 2024, created immediate market disruptions. USGS data documented measurable declines in Chinese graphite exports, leading to supply chain adjustments and price volatility.

Escalation Patterns and Policy Weaponisation:

The progression from informal supply constraints to formal export controls demonstrates systematic escalation. Chinese authorities appear increasingly willing to use strategic material dominance as a foreign policy tool, particularly in response to technology restrictions and trade tensions.

How Are Western Nations Responding to This Challenge?

Trump Administration's 2025 Industrial Policy Pivot

Section 232 Investigation Framework (April 2025):

The Trump administration initiated a comprehensive Section 232 national security investigation targeting processed critical minerals and derivative products. This investigation framework explicitly addresses foreign overcapacity, price distortion, and export restriction concerns, creating legal foundation for potential tariffs, quotas, or import restrictions.

Emergency Powers for Production Acceleration (March 2025):

Executive action invoked emergency powers aimed at accelerating domestic critical minerals production capacity. Consequently, Trump mining permits measures include expedited permitting processes, streamlined environmental reviews, and direct government investment in processing facilities.

DOE Funding Allocation ($355 Million):

The Department of Energy announced $355 million in funding opportunities specifically targeting domestic critical minerals production expansion. Priority areas include:

• Recovery from industrial and coal byproducts

• Advanced processing technology development

• Domestic supply chain integration projects

• Critical minerals recycling and circular economy initiatives

Defence Department Equity Participation:

The Department of Defence committed to a 40% equity stake in a $7.4 billion Tennessee critical minerals smelter project, representing unprecedented direct government participation in strategic material processing infrastructure.

Allied Framework Development

US-Australia Critical Minerals Partnership ($8.5 Billion):

The bilateral framework encompasses a project pipeline valued at $8.5 billion, focusing on lithium, rare earths, and other strategic materials. Key components include:

• Joint processing facility development

• Technology transfer agreements

• Supply chain integration initiatives

• Long-term offtake commitments

EXIM Bank Financing Commitments ($2.2 Billion):

Export-Import Bank letters of interest totalling $2.2 billion support critical minerals infrastructure development. These financing commitments target processing capacity development in allied nations and domestic supply chain strengthening.

Coordinated Response Limitations:

Despite allied coordination efforts, several challenges limit effectiveness:

• Scale Mismatch: Current commitments remain significantly smaller than Chinese processing capacity

• Timeline Constraints: New processing facilities require 5-10 year development periods

• Technology Gaps: Specialised processing knowledge remains concentrated in Chinese operations

• Economic Viability: Higher cost structures in Western jurisdictions challenge competitive positioning

The Infrastructure Reality Check

Timeline Estimates for Meaningful Diversification:

Industry analysis indicates 10-20 year timelines for achieving meaningful supply chain diversification from Chinese processing dominance. Critical factors include:

• Facility Construction: 3-5 years for basic processing infrastructure

• Technology Development: 5-7 years for advanced processing capability

• Supply Chain Integration: 2-3 years for procurement and logistics optimisation

• Workforce Development: 3-5 years for specialised technical expertise

Capital Intensity Requirements:

Processing facility construction requires substantial capital investments, often exceeding $1 billion for large-scale operations. Lithium processing plants typically require $500 million to $2 billion in capital depending on capacity and integration level.

Permitting and Regulatory Barriers:

Environmental permitting processes in Western jurisdictions can extend project timelines by 2-5 years. Regulatory complexity around mining and processing operations creates additional uncertainty for private investment decisions.

Scale Economics Challenges:

Non-Chinese processing operations face significant scale disadvantages due to:

• Higher labour and energy costs

• Smaller market scale and demand concentration

• Limited integration with downstream manufacturing

• Regulatory compliance costs and environmental standards

The next major ASX story will hit our subscribers first

What Does China's Critical Minerals Dominance Mean for Global Markets?

Geopolitical Leverage Assessment

Trade War Weaponisation Potential:

China's critical minerals dominance across 19 strategic materials creates multiple leverage points for economic coercion. Export restrictions can target specific industries or countries without affecting Chinese domestic consumption, providing asymmetric policy tools.

Allied Vulnerability Despite Mining Diversification:

Even successful mining diversification efforts remain vulnerable to processing bottlenecks. Australia's lithium mining expansion, African cobalt production, and Canadian rare earth development still require Chinese processing capacity for final products.

Economic Coercion Capabilities:

Chinese authorities can implement various levels of supply pressure:

• Soft Controls: Licensing delays, quality inspections, administrative procedures

• Medium Restrictions: Export quotas, seasonal limitations, price controls

• Hard Sanctions: Complete export bans, technology transfer restrictions, financial sanctions

Investment and Market Implications

Critical Minerals Sector Investment Opportunities:

Supply chain diversification creates investment opportunities in:

• Processing facility development outside China

• Advanced materials technology and automation

• Recycling and circular economy infrastructure

• Strategic materials stockpiling and inventory management

Supply Chain Resilience as Competitive Advantage:

Companies with diversified supply chains may gain competitive advantages through:

• Reduced supply disruption risks

• Price stability during geopolitical tensions

• Market access in regions with strategic materials restrictions

• Government contract preferences for secure supply chains

Commodity Price Volatility from Concentration Risks:

Market concentration creates inherent price volatility as supply disruption fears drive speculative trading. Critical minerals prices often exhibit greater volatility than traditional commodities due to supply concentration and strategic importance.

Technology Transition Dependencies

Clean Energy Rollout Vulnerability:

Global clean energy deployment targets remain vulnerable to Chinese processing capacity constraints. Solar panel manufacturing, wind turbine production, and electric vehicle scaling all depend on materials processed primarily in Chinese facilities. Furthermore, the energy transition challenges demonstrate how renewable technology deployment rates may be constrained by material supply chains.

EV Adoption Rate Limitations:

Electric vehicle adoption rates may be constrained by battery material supply chains rather than consumer demand or manufacturing capacity. Processing bottlenecks in lithium, graphite, and other battery materials can limit EV production scaling.

Renewable Energy Infrastructure Requirements:

Wind and solar infrastructure requires substantial quantities of rare earth magnets, specialty steels, and other materials processed predominantly in Chinese facilities. Grid-scale energy storage deployment faces similar supply chain dependencies.

Can Western Nations Break China's Critical Minerals Monopoly?

Technical and Economic Barriers to Diversification

Processing Technology Transfer Limitations:

Specialised processing knowledge remains concentrated in Chinese operations, creating technology transfer challenges:

• Proprietary Processes: Chinese facilities have developed optimised processing methods through decades of experience

• Equipment Specialisation: Processing equipment requires specialised design and operation knowledge

• Quality Control Systems: Achieving consistent product specifications requires extensive process optimisation

• Workforce Expertise: Technical personnel with processing experience remain concentrated in existing facilities

Environmental Compliance Costs:

Western processing operations face substantially higher environmental compliance costs:

• Emissions Controls: Advanced pollution control systems add 15-25% to facility capital costs

• Waste Management: Proper disposal and treatment of processing wastes increases operating expenses

• Permitting Complexity: Environmental review processes extend project timelines and add uncertainty

• Community Relations: Public opposition to industrial facilities requires extensive stakeholder engagement

Labour and Energy Cost Disadvantages:

Western processing operations face structural cost disadvantages:

• Labour Costs: Skilled technical workers command higher wages in Western jurisdictions

• Energy Expenses: Electricity costs for energy-intensive processing typically exceed Chinese rates by 50-100%

• Regulatory Compliance: Safety, environmental, and labour regulations increase operational complexity

• Infrastructure Development: New facilities often require significant infrastructure investment

Market Size Requirements for Economic Viability:

Processing facilities require minimum scale to achieve economic viability, often creating chicken-and-egg problems where market development requires capacity, but capacity investment requires market certainty.

Strategic Options for Reducing Dependency

Stockpiling vs. Processing Capacity Trade-offs:

Strategic stockpiling provides short-term supply security but requires ongoing storage costs and inventory management. Processing capacity development offers long-term security but requires substantial capital investment and extended development timelines.

Strategic Stockpiling Advantages:

• Immediate supply security for critical applications

• Lower initial capital requirements than processing facilities

• Flexibility to stockpile multiple materials in centralised locations

• Buffer against temporary supply disruptions

Processing Capacity Advantages:

• Long-term supply independence from foreign sources

• Economic benefits through domestic job creation and industrial capacity

• Technical capability development for future applications

• Strategic autonomy in material specifications and quality control

Allied Coordination Mechanisms:

Multilateral approaches can share development costs and risks:

• Shared Infrastructure: Joint processing facilities serving multiple allied nations

• Technology Cooperation: Shared R&D for advanced processing methods

• Market Coordination: Coordinated procurement to ensure processing facility viability

• Financial Risk Sharing: Multilateral investment frameworks and loan guarantees

Technology Innovation for Material Substitution:

Research into alternative materials and processing methods could reduce dependency:

• Battery Chemistry Innovation: Development of battery chemistries requiring less problematic materials

• Materials Science Advances: New alloys and composites with different input requirements

• Processing Technology: More efficient processing methods reducing cost and environmental impact

• Synthetic Alternatives: Laboratory production of critical materials through advanced manufacturing

Recycling and Circular Economy Potential:

End-of-life recovery could provide alternative sources for critical materials:

• Battery Recycling: Recovery of lithium, cobalt, and other battery materials from end-of-life EVs

• Electronic Waste Processing: Rare earth and precious metal recovery from discarded electronics

• Industrial Scrap Utilisation: Processing of manufacturing waste streams for material recovery

• Urban Mining: Systematic recovery of materials from infrastructure and buildings

Timeline Realities for Supply Chain Independence

Short-Term Projections (2-5 Years):

Current Western initiatives will have limited impact on Chinese processing dominance in the near term:

• Capacity Additions: New processing facilities will provide marginal capacity increases

• Stockpiling Programmes: Strategic reserves will offer temporary supply security

• Allied Cooperation: Framework agreements will begin implementation phases

• Technology Development: R&D programmes will advance but not reach commercial scale

Medium-Term Outlook (5-10 Years):

Meaningful capacity additions become possible with sustained investment and policy support:

• Processing Infrastructure: Major processing facilities will come online in allied nations

• Technology Transfer: Advanced processing capabilities will develop outside China

• Supply Chain Integration: Alternative supply chains will achieve operational status

• Market Competition: Non-Chinese processing will begin competing on cost and quality

Long-Term Potential (10+ Years):

Significant diversification becomes achievable under favourable scenarios:

• Capacity Parity: Western processing capacity could approach Chinese levels in key materials

• Technology Leadership: Advanced processing methods may provide competitive advantages

• Circular Economy: Recycling systems will provide substantial alternative supply sources

• Material Substitution: New technologies may reduce dependency on problematic materials

Critical Decision Points and Investment Requirements:

Success requires sustained commitment across multiple election cycles and market conditions:

• Government Policy Continuity: Consistent policy support through political transitions

• Private Sector Confidence: Investment certainty through long-term contracts and guarantees

• Allied Coordination: Sustained multilateral cooperation despite changing priorities

• Capital Mobilisation: Estimated $50-100 billion investment requirements for meaningful diversification

The Future of Critical Minerals Geopolitics

Scenario Planning for Supply Chain Evolution

Best-Case Scenario: Successful Western Processing Development

Under optimal conditions, Western nations achieve substantial supply chain diversification:

• Processing Capacity: 40-50% of global capacity shifts to Western or allied facilities by 2035

• Technology Innovation: Advanced processing methods reduce costs and environmental impact

• Allied Integration: Seamless supply chain coordination among democratic nations

• Market Stability: Reduced price volatility through diversified supply sources

Probability Assessment: 25-30% likelihood given current policy trajectories and investment levels

Worst-Case Scenario: Expanded Chinese Control and Restrictions

Chinese dominance deepens while export controls become more systematic:

• Market Concentration: Chinese processing share increases to 80-90% across critical materials

• Export Weaponisation: Systematic use of supply restrictions for geopolitical leverage

• Technology Barriers: Chinese advances create insurmountable competitive disadvantages

• Allied Fragmentation: Competing national interests undermine coordinated responses

Probability Assessment: 20-25% likelihood under scenarios of policy inconsistency and insufficient investment

Most Likely Scenario: Partial Diversification with Continued Dependencies

Limited progress on diversification while Chinese dominance persists in key areas:

• Marginal Capacity Additions: Western processing capacity increases but remains secondary to Chinese operations

• Selective Independence: Success in 2-3 critical materials while dependencies persist in others

• Ongoing Vulnerability: Supply chain risks remain elevated despite incremental improvements

• Market Segmentation: Separate supply chains emerge for different geopolitical blocs

Probability Assessment: 45-50% likelihood representing baseline expectations given current trends

Investment and Policy Recommendations

Government-Private Sector Partnership Models:

Effective supply chain development requires innovative financing and risk-sharing arrangements:

Recommended Structures:

• Development Finance Institutions: Government-backed financing for strategic infrastructure

• Public-Private Joint Ventures: Shared ownership models reducing private sector risk

• Long-Term Offtake Agreements: Government purchase commitments ensuring facility viability

• Technology Development Partnerships: Shared R&D costs between government and industry

Strategic Stockpiling vs. Capacity Building Priorities:

Resource allocation should balance immediate security needs with long-term strategic development. In addition, implementing a comprehensive critical minerals strategy requires coordination across multiple government agencies and international partners.

Stockpiling Priorities:

• Materials with longest supply chain development timelines (rare earths, tungsten)

• Critical defence applications requiring immediate supply security

• Materials with highest Chinese market concentration and export restriction risk

Capacity Building Priorities:

• Materials with largest market size and economic impact (lithium, graphite)

• Technologies where Western nations retain competitive advantages

• Materials with existing infrastructure foundations for expansion

Want to Capitalise on the Next Major Mineral Discovery?

China's critical minerals dominance has created unprecedented supply chain vulnerabilities, making individual discovery opportunities more valuable than ever for informed investors. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly transforming complex geological data into actionable investment insights. Begin your 30-day free trial today and position yourself ahead of the market whilst Western nations scramble to secure critical materials independence.