May 12, 2026

Understanding China's Strategic Pricing Authority

Global commodity markets are entering a new phase of strategic competition where pricing authority itself becomes a tool of geopolitical leverage. The establishment of centralized pricing mechanisms within command-capitalist frameworks represents a fundamental shift from traditional market-based discovery processes to state-coordinated reference systems designed to project institutional control beyond national boundaries. The emergence of a China rare earth price index marks a significant development in how critical minerals energy markets operate globally.

When big ASX news breaks, our subscribers know first

Understanding China's New Pricing Architecture

The Baotou Rare Earth Price Index represents a sophisticated attempt to institutionalise pricing authority within China's critical minerals sector. Launched in December 2024, this mechanism extends far beyond simple market transparency, functioning as a strategic instrument for coordinating domestic supply chains while projecting pricing influence across global rare earth markets.

Furthermore, this development occurs amid broader geopolitical tensions where China export controls have become increasingly sophisticated tools for managing strategic resource flows.

The Baotou Rare Earth Price Index Framework

The index operates through Xinhua-affiliated financial platforms, including the China Financial Information Network and Xinhua Finance terminals. This distribution architecture ensures widespread domestic accessibility while maintaining state oversight of pricing dissemination.

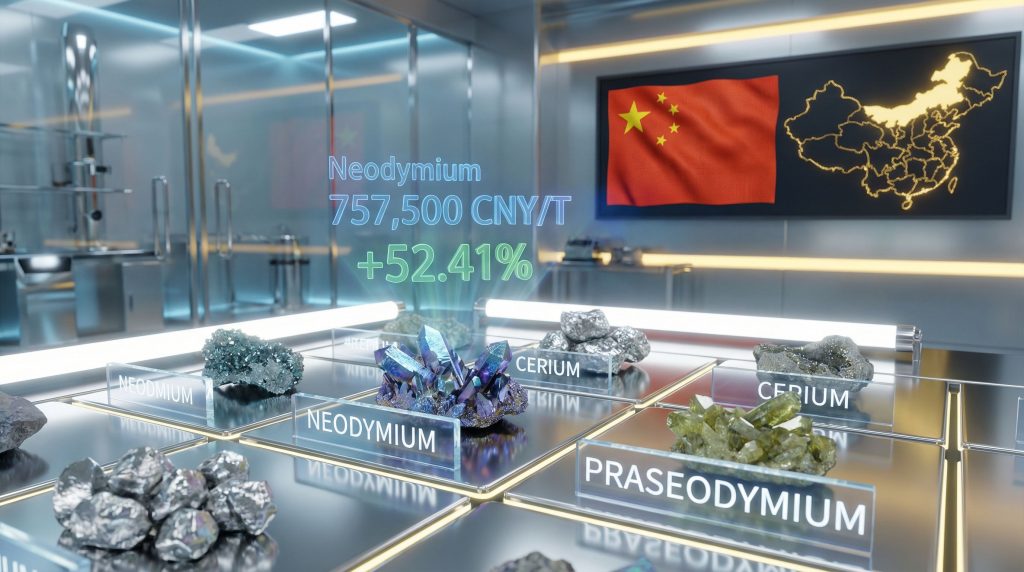

The system tracks four primary rare earth elements: lanthanum, cerium, praseodymium, and neodymium, which collectively represent the most commercially significant light rare earth materials in global supply chains.

The pricing structure encompasses three temporal components designed to serve different market functions:

• Daily transaction prices reflecting immediate exchange activity

• Weekly rare earth price indices providing medium-term trend analysis

• Monthly price expectation indices incorporating forward-looking market assessments

This multi-layered approach distinguishes the system from simple spot pricing mechanisms, creating a comprehensive reference framework that can influence both current transactions and future contract negotiations.

Technical Methodology Behind the Index

The index construction relies on transaction data aggregation from the Baotou Rare Earth Products Exchange combined with what official sources describe as widely collected trade data. Academic institutional collaboration has contributed to the index model development, though specific methodological frameworks remain proprietary.

The system emphasises real and compliant trade data, suggesting quality assurance protocols designed to maintain pricing integrity. However, the verification processes for data inclusion and the weighting mechanisms used in index calculation represent critical technical details that require further transparency for independent assessment.

Quality control measures appear to integrate with China's broader rare earth regulatory framework, ensuring that pricing signals align with production quota systems and export control mechanisms already governing the sector.

How Does China's Rare Earth Exchange System Actually Work?

The infrastructure underlying the China rare earth price index reflects a decade-long evolution from fragmented producer pricing toward centralised exchange mechanisms. Understanding this operational framework reveals how pricing authority has become concentrated within state-coordinated institutions.

The Baotou Exchange Infrastructure

The Baotou Rare Earth Products Exchange, established in 2014, operates as China's singular dedicated rare earth trading platform. Unlike Western commodity exchanges that offer derivatives and financial instruments, this system functions strictly as a physical spot market requiring actual product delivery and RMB settlement.

The exchange has evolved into the central hub of Chinese rare earth commerce, with nearly 1,000 enterprise members participating in transactions totalling approximately 102,400 tons of rare earth oxide equivalent annually.

This volume represents a significant portion of China's domestic rare earth flow, though claims of representing two-thirds of national output require verification against official production statistics.

Critical Infrastructure Integration: The exchange combines online trading with warehousing, quality inspection, logistics, and trade finance services, creating an end-to-end digital marketplace that controls multiple aspects of the physical supply chain.

Market Participation and Ownership Structure

Northern Rare Earth holds approximately 40% equity in the exchange, representing the largest single ownership stake. This state-owned enterprise dominance ensures alignment between exchange operations and national industrial policy objectives.

The Inner Mongolia government provides institutional backing, reinforcing the platform's role as both commercial infrastructure and strategic policy instrument.

The transition from producer-posted prices to exchange-based pricing has fundamentally altered how Chinese rare earth prices are determined. Major producers have abandoned internal pricing mechanisms in favour of daily exchange-based benchmarks, creating a unified pricing environment across nearly all domestic transactions.

This structural transformation reflects broader Chinese industrial consolidation patterns, where state coordination replaces market fragmentation to achieve strategic objectives while maintaining commercial functionality.

What Makes This Different from Western Commodity Indices?

The fundamental distinction between China's rare earth price index and Western commodity pricing mechanisms lies in their underlying institutional frameworks and operational objectives. These differences have profound implications for global supply chain participants attempting to navigate competing pricing systems.

Command-Capitalist Framework Analysis

Western commodity indices typically emerge from independent market participants responding to scarcity, risk, and profit incentives within competitive frameworks. Regulatory oversight maintains separation between government policy and price discovery mechanisms, allowing market forces to determine pricing outcomes.

China's approach integrates production quota systems, export control policies, and strategic industrial objectives directly into pricing mechanisms. This coordination ensures that price signals serve national policy goals while maintaining commercial functionality for domestic transactions.

The system prioritises industrial policy alignment, geopolitical leverage, and long-term strategic positioning over pure profit maximisation. This orientation reflects the broader command-capitalist model where state enterprises balance commercial performance with policy mandate fulfilment.

Administered Pricing Versus Market Discovery

| Western Commodity Indices | China's Rare Earth Index |

|---|---|

| Independent buyer-seller interactions | State-guided participant coordination |

| Regulatory separation from government | Direct government institutional control |

| Profit-maximising price signals | Policy-conditioned strategic signals |

| Open competition framework | Quota-allocated production system |

| Risk-based pricing discovery | Strategic objective prioritisation |

These structural differences create pricing environments that serve fundamentally different purposes. Western indices attempt to reflect market reality through independent price discovery, while China's system uses pricing as a policy tool to achieve strategic coordination and external influence.

Consequently, the implications extend beyond simple price levels to encompass pricing volatility, responsiveness to supply disruptions, and the relationship between domestic and international price signals.

How Could This Index Reshape Global Rare Earth Pricing?

The emergence of a state-coordinated China rare earth price index creates potential pathways for fundamental changes in global pricing authority and supply chain risk assessment. The scope and timeline of these changes depend on adoption patterns and competitive responses from alternative pricing systems.

Potential Benchmark Adoption Scenarios

Domestic contract expansion represents the most immediate adoption pathway. As Chinese industrial users increasingly reference the Baotou index in supply agreements, the pricing mechanism gains institutional momentum and market recognition.

This creates network effects where additional participants adopt the index to maintain pricing consistency across their supply chains.

International supply chain integration presents a more complex scenario. Global manufacturers with significant Chinese rare earth exposure may find practical advantages in using established Chinese pricing references, particularly when negotiating contracts with Chinese suppliers or managing currency risk through RMB-denominated transactions.

The displacement of ex-China pricing mechanisms represents a strategic concern for Western supply chain security. Currently, alternative pricing sources provide competing benchmarks, but the institutional backing and transaction volume supporting China's index could gradually marginalise these alternatives.

Strategic Implications for Non-Chinese Producers

MP Materials and other Western operations face complex positioning decisions regarding pricing benchmark adoption. The company's NdPr price floor contracts represent early attempts to establish alternative pricing frameworks, though these arrangements currently serve limited market segments.

Western rare earth producers must balance several competing considerations:

• Maintaining pricing independence while remaining competitively relevant

• Developing alternative benchmark systems that attract international adoption

• Managing supply chain disruption risks from pricing mechanism conflicts

• Securing government support for pricing authority development initiatives

The creation of bespoke contract negotiation frameworks allows some flexibility, but this approach may become less viable as Chinese pricing mechanisms gain broader institutional acceptance and network effects strengthen.

What Are the Current Rare Earth Price Dynamics?

Recent rare earth price movements reflect the complex interaction between supply constraints, policy changes, and emerging institutional pricing frameworks. Understanding these dynamics provides insight into how new pricing mechanisms may influence market behaviour.

However, these developments must be viewed within the broader context of how the mining industry evolution is responding to geopolitical pressures.

Key Element Performance Metrics

Neodymium pricing has demonstrated significant volatility, with current market data suggesting substantial annual increases. However, these figures require verification through multiple independent sources given the sensitivity of rare earth pricing data and the emergence of competing pricing systems.

Scandium oxide and ytterbium oxide pricing patterns reflect the specialised nature of heavy rare earth markets, where supply constraints and limited production sources create different pricing dynamics compared to light rare earth elements tracked by the Baotou index.

Price movements across different elements reveal the segmented nature of rare earth markets, where individual elements respond to distinct supply-demand fundamentals despite sharing common production and processing infrastructure.

Export Control Impact Assessment

China's expansion of export controls to additional rare earth elements has created temporary supply disruptions and pricing volatility in international markets. The 2025 restrictions affecting multiple rare earth elements demonstrate how regulatory policy directly influences pricing outcomes.

The addition of holmium and erbium to export control lists reflects China's systematic approach to managing critical mineral flows. These policy changes create immediate pricing pressure while establishing longer-term supply chain reconfiguration incentives for international users.

Export control implementation has revealed the interconnected nature of rare earth supply chains, where restrictions on individual elements can create cascading effects across related materials and downstream applications.

The next major ASX story will hit our subscribers first

How Do Alternative Pricing Platforms Compare?

The competitive landscape for rare earth pricing information includes several established platforms, each serving different market segments and analytical needs. Understanding these alternatives provides context for assessing the potential market impact of China's centralised index.

Competing Index Methodologies

TrendForce monthly tracking provides comprehensive rare earth price analysis through independent market research methodologies. This platform serves international users seeking pricing data separate from Chinese institutional sources, though its influence on actual transaction pricing remains limited compared to exchange-based mechanisms.

Asian Metal real-time systems offer detailed oxide and metal price charts with frequent updates reflecting regional trading activity. The platform's accessibility and breadth of coverage make it valuable for market participants monitoring short-term price movements and trend analysis.

Shanghai Metals Market daily updates provide another Chinese perspective on rare earth pricing, though with different methodological approaches compared to the Baotou exchange system. This creates opportunities for price arbitrage and market analysis based on institutional differences.

Regional Pricing Differential Analysis

China domestic versus international price gaps have widened in recent years, reflecting export controls, transportation costs, and processing premiums. These differentials create strategic considerations for supply chain design and sourcing decisions.

Ex-China supply chain premiums compensate for higher production costs, smaller economies of scale, and supply security considerations. Understanding these premium structures helps assess the economic viability of alternative supply sources and the competitive pressure on Chinese pricing.

In addition, currency fluctuation impacts add additional complexity to international pricing comparisons, particularly for companies managing multi-currency exposure across diverse rare earth supply sources.

What Does This Mean for Global Supply Chain Strategy?

The establishment of the China rare earth price index creates new strategic considerations for governments, companies, and investors navigating critical mineral supply chains. These implications extend beyond immediate pricing concerns to encompass longer-term supply security and competitive positioning.

Furthermore, these developments occur within the broader context of the US-China trade war impact on global markets.

Western Government Response Requirements

Alternative supply chain development acceleration becomes increasingly urgent as China consolidates pricing authority alongside production capacity. Government support for domestic rare earth processing capabilities and international supply partnerships requires sustained policy commitment and financial resources.

Strategic reserve policy recalibration must account for pricing mechanism risks in addition to physical supply disruptions. The development of a critical minerals reserve requires careful consideration of pricing authority concentration and potential manipulation risks.

International cooperation frameworks need strengthening to create viable alternatives to Chinese pricing systems. This includes coordination on reserve sharing, joint procurement initiatives, and collaborative benchmark development projects.

Investment and Policy Implications

Key Strategic Insight: Control of commodity markets extends beyond mining and processing to encompass pricing authority and reference benchmark establishment. This represents a new dimension of supply chain security requiring proactive policy responses.

Mining company valuation models must incorporate pricing mechanism risks alongside traditional supply-demand fundamentals. Companies with alternative pricing arrangements or benchmark development capabilities may command strategic premiums.

Technology sector supply security requires comprehensive assessment of pricing risk exposure in addition to physical availability concerns. Supply chain diversification strategies must consider pricing mechanism dependence and potential disruption scenarios.

Government stockpile strategies and corporate inventory management approaches may require adjustment based on pricing authority concentration and the potential for strategic pricing manipulation during geopolitical tensions.

Frequently Asked Questions About China's Rare Earth Price Index

Is This Index Truly Market-Based?

The China rare earth price index operates within a state-coordinated framework where production quotas, export controls, and policy objectives influence pricing alongside commercial considerations. While transactions occur between different enterprises, these participants operate under common state guidance and policy mandates.

The distinction between market-based pricing and state coordination represents a fundamental difference in institutional design. Traditional Western market concepts assume independent participants responding to profit incentives, while China's system integrates commercial activity with strategic policy objectives.

How Reliable Are Chinese Rare Earth Price Signals?

State-linked media reporting and exchange announcements provide official pricing information, though independent verification through multiple sources remains essential for business decision-making. Cross-referencing with alternative pricing platforms and transaction data helps assess reliability and potential bias.

Investment and business conclusions should incorporate comprehensive risk assessment protocols that account for the policy-driven nature of Chinese pricing mechanisms and the potential for strategic manipulation during periods of geopolitical tension.

What Should Stakeholders Monitor Going Forward?

The evolution of China's rare earth price index will likely unfold over several years, with critical developments occurring across multiple dimensions of market structure and international adoption patterns.

Critical Development Indicators

International contract adoption rates represent the most important metric for assessing global influence. Monitoring major supply agreements for index referencing clauses provides insight into institutional acceptance and competitive positioning.

Western alternative pricing mechanism progress includes both private sector initiatives and government-supported benchmark development projects. The success of these alternatives in attracting market participation will determine long-term pricing authority distribution.

Export control policy evolution continues to influence market structure and pricing dynamics. Additional restrictions or liberalisation measures will create new pricing pressures and supply chain adjustment requirements.

Strategic Response Framework Development

Pricing authority competition preparation requires sustained investment in alternative infrastructure, benchmark development, and market maker capabilities. This represents a long-term strategic commitment rather than short-term market positioning.

Supply security enhancement initiatives must address pricing mechanism risks alongside physical availability concerns. Comprehensive supply chain security requires diversification across both sources and pricing systems.

Market intelligence capabilities need enhancement to monitor pricing mechanism competition, assess adoption patterns, and identify strategic opportunities for alternative framework development.

Multilateral cooperation mechanisms offer pathways for coordinated responses to pricing authority concentration. International frameworks for benchmark development, reserve coordination, and joint procurement can provide viable alternatives to Chinese pricing systems.

Disclaimer: This analysis incorporates information from Chinese state-affiliated sources and official announcements that should be independently verified before forming business, policy, or investment conclusions. Rare earth market conditions remain highly dynamic, and strategic assessments require ongoing monitoring of regulatory, technological, and geopolitical developments.

Could You Be Missing Critical Market-Moving Discoveries?

China's strategic control over rare earth pricing demonstrates how quickly fundamental market dynamics can shift, particularly in the critical minerals sector where geopolitical developments create immediate trading opportunities. Discovery Alert's proprietary Discovery IQ model provides instant notifications on significant ASX mineral discoveries, ensuring subscribers can rapidly identify actionable opportunities ahead of broader market awareness. Begin your 30-day free trial today at https://discoveryalert.com.au/ and secure your market-leading advantage in this rapidly evolving landscape.