June 15, 2026

When Geography Becomes Destiny: The Strait That Controls the World's Energy Pulse

Chokepoints have shaped the course of civilisations long before the age of petroleum. The Strait of Hormuz, however, occupies a category entirely its own. No other single geographic feature concentrates so much economic consequence into so little physical space. At its narrowest navigable corridor, a strip of water barely wide enough to accommodate two-way supertanker traffic separates the oil-producing heartland of the planet from the rest of the world's energy consumers. For decades, this structural vulnerability was treated as a manageable risk, priced into shipping insurance and quietly factored into strategic planning documents that most policymakers never expected to dust off. The Hormuz crisis escalation of 2026 has rendered that complacency obsolete.

What makes the current confrontation qualitatively distinct from previous episodes of tension around the strait is not simply its intensity, but its architecture. A combination of direct military exchanges, tanker seizures, naval blockade positioning, and simultaneous diplomatic negotiations has created a crisis structure that has no clean modern precedent. Understanding what is actually happening, why it matters beyond the energy sector, and where it is likely to lead requires moving beyond event-by-event reporting into the strategic logic driving each actor's decisions.

When big ASX news breaks, our subscribers know first

The Chokepoint That Concentrates Global Risk

Approximately one-fifth of all globally traded oil and gas transits the Strait of Hormuz, according to reporting by RFE/RL published via OilPrice.com on May 12, 2026. This figure alone understates the chokepoint's systemic importance. The strait does not merely carry physical barrels of crude. It functions as the primary price-setting mechanism for global energy markets, because the threat of disruption, even partial or temporary, is sufficient to generate immediate commodity price volatility far exceeding the actual volume of oil interrupted.

This is the asymmetry that makes the Hormuz crisis escalation so potent as both a military and economic instrument. Iran does not need to close the strait entirely to impose significant costs. Restricting transit, targeting specific vessel classes, or simply creating uncertainty sufficient to drive up war-risk insurance premiums achieves a comparable economic effect at a fraction of the military cost required for full closure. Furthermore, crude oil price trends in the months leading up to this confrontation had already primed markets for heightened sensitivity to any supply-side shock.

The Historical Baseline

Previous Hormuz tension episodes, including the 1980s Tanker War during the Iran-Iraq conflict and the 2019 tanker seizure incidents, were ultimately contained within diplomatic frameworks that had functional back-channel communication. Both sides in those episodes maintained private lines of communication that allowed de-escalation before economic damage became structural. The critical concern among analysts monitoring the 2026 confrontation is that equivalent back-channel infrastructure may not be reliably operational, raising the miscalculation risk substantially.

Managed Confrontation: A More Dangerous Equilibrium Than Open War

The phrase most commonly applied to the current military environment by strategic analysts is a stalemate. Mark Cancian, a retired US Marine Corps colonel and senior adviser at the Center for Strategic and International Studies (CSIS) who served across multiple major military campaigns including Desert Storm, characterised the situation in precisely these terms during a CSIS discussion held on May 11, 2026. Iran has positioned itself to restrict strait access while the United States maintains naval pressure from outside the waterway, and neither side has achieved conditions for a decisive breakthrough.

This equilibrium is more strategically dangerous than it appears. Open war, while catastrophic in direct human and material terms, typically generates its own termination logic: one party achieves a decisive military advantage, the other accepts unfavourable terms, and a framework for cessation emerges. Managed confrontation lacks this self-correcting mechanism. Each limited exchange is designed not to win but to signal, which means the conflict can persist indefinitely while economic damage accumulates for every country dependent on the strait's operation. According to analysis from the UN on the crisis, the humanitarian and economic consequences of prolonged disruption are already being felt across developing economies.

Iran's Recalibrated Threshold

Tehran's escalation posture has undergone a significant evolution. Rather than maintaining deliberate ambiguity about which US actions would constitute an unacceptable provocation, Iranian leadership has adopted a more explicit deterrence framework, identifying specific categories of external interference in strait navigation as triggers for direct retaliation. This shift from ambiguous deterrence to declared thresholds is strategically double-edged: it reduces the probability of accidental escalation in some scenarios while eliminating Iran's diplomatic flexibility in others.

The dual-track nature of Iranian signalling, combining explicit military warnings with expressions of openness to mediated negotiations, reflects a calculated strategy of maintaining leverage while preserving a diplomatic off-ramp. According to Cancian's assessment shared at the CSIS discussion, both Washington and Tehran are exploring compromise frameworks involving Iran's enriched uranium stockpile, future enrichment restrictions, and phased sanctions relief, with the US reportedly prepared to forgo on-the-ground inspectors in exchange for verifiable physical constraints on uranium stockpiles.

The Inherent Contradiction in Washington's Position

The US approach of maintaining a naval blockade while simultaneously pursuing negotiations presents its own logical tension that Tehran has publicly identified. Negotiating the restoration of free navigation through the strait while a foreign naval force controls access to that same waterway creates a structural asymmetry that complicates Iranian domestic political acceptance of any agreement. Any Iranian leadership team that accepts terms under these conditions faces accusations of capitulating under duress, which limits the political space available for concessions.

According to reporting by RFE/RL via OilPrice.com, pressure exists on both sides to reach an agreement. However, as Cancian noted, the longer the confrontation continues, the greater the military and economic pressure will become for both parties involved.

The Economic Damage Already Accumulating

While diplomatic timelines are measured in weeks, economic damage accumulates daily. Fuel prices have risen approximately 40% since the onset of the crisis, according to RFE/RL reporting via OilPrice.com, and the impact is spreading across transportation, manufacturing, and consumer price indices globally.

The commodity price table below reflects market conditions as of May 12, 2026, based on OilPrice.com live pricing data:

| Market Indicator | Crisis-Period Level | Session Change |

|---|---|---|

| WTI Crude (USD/bbl) | ~$101.70 | +3.66% |

| Brent Crude (USD/bbl) | ~$107.80 | +3.43% |

| Heating Oil (USD/gal) | $4.093 | +3.13% |

| WTI Midland (USD/bbl) | ~$104.00 | +3.92% |

| Global Jet Fuel Exports | 10-year seasonal low | Significant contraction |

| OPEC Oil Output | 26-year low | Historic compression |

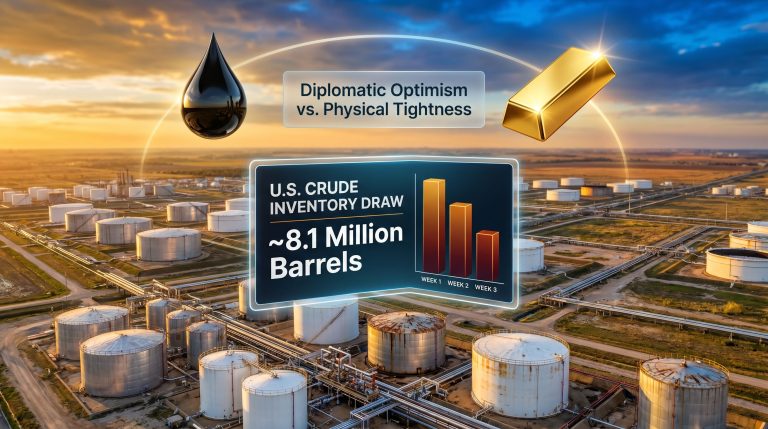

These headline figures, while significant, may still understate the true severity of the market condition. Morgan Stanley has issued analysis warning that global strategic oil reserves and supply buffers could be exhausted before the Strait of Hormuz returns to normal operating conditions, according to OilPrice.com headline reporting dated May 11, 2026. This assessment introduces a critical inflection point that most market participants have not yet fully priced in.

The Risk Premium vs. Physical Scarcity Distinction

Current oil pricing above $100 per barrel reflects a geopolitical risk premium, not physical scarcity. Markets are essentially pricing the probability of eventual diplomatic resolution. Buyers and sellers are factoring in their expectation that some form of agreement will emerge before disruption becomes permanent. This is why, as the RFE/RL reporting noted, financial markets have remained relatively stable despite extreme volatility in spot prices.

The Morgan Stanley warning, however, describes a qualitatively different scenario: the depletion of strategic petroleum reserves before resolution occurs. If this threshold is crossed, oil markets shift from pricing risk to pricing genuine physical unavailability. The mechanisms that currently buffer price spikes, including reserve drawdowns, demand destruction, and alternative supply routing, become unavailable simultaneously. The result is a non-linear price trajectory that could push crude materially beyond current levels.

The distinction matters enormously for investors and policymakers: risk-premium pricing is temporary and mean-reverting. Physical scarcity pricing is structural and self-reinforcing. Once strategic buffers are depleted, there is no comparable stabilisation mechanism readily available to replace them.

Cascade Effects Across Importing Economies

The downstream consequences are already visible across multiple geographies. In addition, the broader oil market disruption caused by ongoing trade tensions has compounded the shock, leaving import-dependent economies with fewer policy tools to absorb the impact:

-

China: Teapot refiners, the independent refining sector that processes a substantial share of China's crude throughput, are slashing output as compressed margins make operations uneconomical, according to OilPrice.com headline reporting. China's Consumer Price Index has accelerated as Middle East energy costs transmit into domestic pricing.

-

India: Inflation is accelerating as high energy prices compound across supply chains. The Modi government has implemented a fuel price freeze, but state retailers are absorbing billions in losses as a direct consequence, per OilPrice.com reporting. More than 40 India-bound vessels remain trapped near Hormuz, representing a significant physical supply disruption to the world's third-largest oil importer.

-

Pakistan: Islamabad has rejected LNG bids as the energy crisis deepens, according to OilPrice.com, signalling that price-sensitive emerging market importers are effectively being priced out of global LNG markets entirely.

-

Global aviation: Jet fuel exports hit a 10-year seasonal low in April, according to OilPrice.com headline data, reflecting the combined impact of route disruption and margin compression across the aviation fuel supply chain.

-

Coal demand: Global coal consumption is surging as industrial consumers switch away from oil and gas, producing an unintended emissions acceleration at precisely the moment climate commitments are under the most institutional scrutiny.

How Asian Economies Are Responding to Their Exposure

The Hormuz crisis escalation is landing with particular severity across East Asia, where energy import dependency ratios leave little buffer against sustained supply disruption. South Korea sources approximately 70% of its energy imports from the Gulf, while Japan's dependency on Gulf crude approaches 95%, according to RFE/RL reporting via OilPrice.com.

These figures represent decades of optimising for cost efficiency at the expense of supply security diversity. The crisis is now extracting the deferred price of that choice. Consequently, OPEC's global influence over pricing and production decisions is being scrutinised more intensely than at any point in recent memory, as member states grapple with historic output compression.

Victor Cha, who serves as president of the geopolitics and foreign policy department at CSIS and is a professor at Georgetown University, has assessed that regardless of how the current crisis resolves, both Japan and South Korea will emerge from this episode with a structural imperative to reduce their dependence on Gulf transit routes. This is not a temporary political reaction but a permanent recalibration of energy security doctrine in both countries.

Cha further identified a consequential secondary effect: alternative supply routes from Central Asia would likely require transit through infrastructure adjacent to Russian territory, creating what he characterised as a geostrategic imperative for both Japan and South Korea to recalibrate their relationships with Moscow. This is a geopolitical ripple effect that extends far beyond energy markets into the broader architecture of Indo-Pacific strategic alignment.

Japan's Supply Diversification in Practice

Japan received its first Central Asian crude shipment since the Iran conflict began, according to OilPrice.com headline reporting, representing a tangible first step in the supply diversification strategy Cha described. The logistical complexity of this routing, which bypasses the Gulf entirely but requires transit through Central Asian infrastructure networks, illustrates both the practical possibilities and the limitations of rapid supply diversification.

Japanese energy companies are also accelerating evaluation of African and Central Asian upstream investment opportunities, though development timelines for new upstream assets typically extend across years rather than months, making these investments a medium-term response rather than an immediate crisis solution.

Currency Pressure Compounding Import Costs

Both the Japanese yen and South Korean won have fallen to multi-year lows against the US dollar, according to RFE/RL reporting via OilPrice.com. Since oil is priced in US dollars, currency depreciation directly magnifies the local-currency cost of energy imports. This creates a compounding pressure: Asian economies that are already facing higher dollar-denominated oil prices are simultaneously experiencing currency weakness that amplifies the cost burden in domestic terms.

The China-Iran Oil Relationship as a Diplomatic Variable

Beijing absorbed approximately 90% of Iran's crude oil exports in the year prior to the current crisis, according to RFE/RL via OilPrice.com. This commercial relationship functions as Iran's primary economic lifeline and simultaneously as the most powerful piece of diplomatic leverage the United States has not yet fully deployed.

The upcoming US-China summit is expected to place Iran's oil purchasing relationship squarely on the agenda, with US officials anticipated to press Beijing to use its economic position to encourage Iranian concessions on both nuclear restrictions and strait access normalisation. China's willingness to exercise this leverage, and the conditions under which it would do so, represents one of the most consequential unknown variables in the current diplomatic landscape.

It is also worth noting that Brazil's oil exports to China have doubled as the Iran conflict upends traditional crude trade flows, according to OilPrice.com reporting, suggesting Beijing is simultaneously diversifying its own supply sources while maintaining the Iran relationship, a two-track approach that complicates US pressure calculations considerably.

Three Trajectories: How This Crisis Could Resolve or Deepen

The scenario framework below maps the three most credible pathways from the current standoff, based on the strategic dynamics described by analysts and the economic indicators visible in market data as of May 12, 2026.

Scenario 1: Negotiated De-escalation

The conditions required for this outcome include Iranian acceptance of a modified version of the US-proposed framework, covering uranium stockpile constraints and phased sanctions relief in exchange for a commitment to normalised navigation access. Cancian's assessment that both sides are exploring compromise elements, including US flexibility on inspection protocols, suggests this pathway remains open.

Market implications would include a retreat in crude prices toward pre-crisis ranges as the geopolitical risk premium deflates. The critical vulnerability is that any single military incident during an active negotiation window could collapse the diplomatic track entirely.

Scenario 2: Protracted Stalemate

If neither side accepts the other's core demands, the managed confrontation equilibrium persists. Military exchanges continue at low intensity, shipping disruption remains chronic but falls short of full closure, and the economic damage continues accumulating for all parties.

This scenario carries an elevated probability precisely because it does not require either party to make a decision. Inaction sustains the stalemate. The strategic danger is that economic pressure builds unevenly, and the party experiencing the most acute domestic political pressure from economic damage may be forced into escalatory action not as a military strategy but as a political necessity.

Scenario 3: Escalation to Full Strait Closure

This scenario carries a lower probability but extreme consequence. Trigger conditions include a miscalculation during a military exchange, severe domestic political pressure in Iran forcing a maximalist response, or an attempted forced reopening of the strait by US naval forces.

The economic implications of full closure would be qualitatively different from current disruption. Crude prices significantly above current levels, global recession risk, collapse of LNG market pricing stability, and emergency acceleration of coal and nuclear energy consumption are all plausible cascade effects.

Qatar has already taken precautionary steps: the country asked vessels at its key LNG export terminal to go dark for safety reasons, according to OilPrice.com breaking news, which suggests regional energy producers are actively risk-managing even the possibility of this scenario. Furthermore, global LNG supply dynamics are already being reshaped as buyers scramble to secure alternative sources and long-term contracts.

The next major ASX story will hit our subscribers first

The Infrastructure Bypass Reality

A frequently cited solution to Hormuz dependency is the existence of alternative pipeline infrastructure. The practical picture is more constrained than the theoretical one.

The UAE's ADNOC has been executing alternative transport operations through the Habshan pipeline corridor, with ADNOC targeting 80% recovery of Habshan capacity by end-2026, according to OilPrice.com reporting. Separately, OilPrice.com has reported that ADNOC moved 6 million barrels via vessels operating without standard transponder signals, an approach characterised as ghost tanker operations designed to bypass transit restrictions.

Saudi Arabia's East-West Petroline pipeline represents the most significant existing bypass infrastructure capable of routing Gulf crude to Red Sea export terminals without Hormuz transit. However, this infrastructure was designed as a contingency asset rather than a primary export corridor, and its capacity ceiling constrains how much volume can realistically be shifted before the strait reopens.

Full bypass capability for the volumes that normally transit Hormuz would require multi-year, multi-hundred-billion-dollar infrastructure investment across multiple jurisdictions, a structural solution that cannot address the immediate crisis but will increasingly attract capital as the medium-term investment thesis becomes clearer. For a comprehensive overview of the implications for global trade, the UNCTAD analysis provides essential context on how disruptions of this scale reverberate across developing and developed economies alike.

What the Crisis Is Doing to the Energy Transition

The Hormuz crisis escalation is producing a paradox for the global energy transition. Over the long term, it is powerfully reinforcing the investment case for domestic renewable energy production that is immune to geopolitical chokepoint risk. Europe's renewable-plus-battery market is projected to quintuple by 2030, according to OilPrice.com headline reporting, and the strategic logic behind accelerating that trajectory has never been more clearly demonstrated than by the current crisis.

In the short term, however, the immediate response to supply disruption is defaulting to the highest-emission available alternative. Global coal demand is surging, per OilPrice.com reporting, as industrial consumers switch away from disrupted oil and gas supplies. This temporary emissions acceleration is an unintended consequence of the crisis that complicates near-term climate commitments. However, energy transition dynamics suggest that the long-term structural shift toward renewables is being reinforced, not reversed, by the very instability the crisis has exposed.

The IEA had already projected that tight gas markets would persist through 2030, per OilPrice.com headline reporting dated approximately five days before May 12, 2026. That forecast was made before the full scale of the Hormuz crisis escalation became apparent, suggesting the actual market tightness through the decade may exceed even those already cautious projections.

Frequently Asked Questions: Hormuz Crisis Escalation

What percentage of global oil and gas moves through the Strait of Hormuz?

Approximately one-fifth of all globally traded oil and gas transits the Strait of Hormuz, according to RFE/RL reporting via OilPrice.com (May 12, 2026). No alternative route exists that can absorb this volume at comparable cost or logistical efficiency within current timeframes.

Why haven't oil markets collapsed if the strait is disrupted?

Markets are currently pricing the probability of eventual diplomatic resolution rather than permanent closure. Strategic petroleum reserve drawdowns, alternative supply routing, and demand destruction are collectively buffering the immediate physical shock. The Morgan Stanley warning that buffers could run out before the strait reopens, reported via OilPrice.com, signals that this stabilisation mechanism has a time limit.

What is the US-backed proposal to Iran?

The reported framework involves Iran accepting constraints on its enriched uranium stockpile and future enrichment activity, in exchange for phased sanctions relief and a commitment to normalised shipping access. The US has reportedly indicated flexibility on the question of on-the-ground inspectors in favour of verifiable physical constraints on uranium material, according to Cancian's analysis at the CSIS discussion on May 11, 2026.

How dependent are Japan and South Korea on Gulf energy?

Japan sources approximately 95% of its crude oil imports from the Gulf region, while South Korea's dependency is approximately 70%, according to RFE/RL via OilPrice.com. Both nations are accelerating diversification strategies, with Japan having already received its first Central Asian crude shipment since the Iran conflict began, per OilPrice.com reporting.

What role is China playing in the crisis?

China absorbed approximately 90% of Iran's crude oil exports in the year prior to the crisis, according to RFE/RL via OilPrice.com, making it Iran's primary economic support structure. The US is reportedly seeking to leverage the upcoming US-China summit to encourage Beijing to use this economic relationship to press for Iranian concessions. China has simultaneously been increasing imports from alternative suppliers including Brazil, whose oil exports to China have doubled since the conflict began, according to OilPrice.com.

Could bypass infrastructure replace Hormuz transit?

Existing alternatives, including the UAE Habshan pipeline and Saudi Arabia's Petroline, can handle a portion of normal Hormuz throughput. ADNOC is targeting 80% Habshan recovery by end-2026, per OilPrice.com, while also employing ghost tanker operations for near-term volume movement. Full replacement of Hormuz capacity through alternative infrastructure would require multi-year construction programmes and coordinated investment across multiple sovereign entities.

The Structural Lesson That Cannot Be Unlearned

Whatever diplomatic resolution eventually emerges from the current standoff, the Hormuz crisis escalation of 2026 will be studied as the moment when decades of deferred energy security risk arrived simultaneously. The optimisation of global energy supply chains for cost efficiency rather than strategic resilience created a system that functions brilliantly under normal conditions and catastrophically under stress.

The key takeaways for energy market participants are becoming increasingly clear:

-

Supply security doctrine is being permanently recalibrated across Asian importing economies, with structural investment in alternative corridors now a strategic priority rather than a contingency consideration.

-

Price risk architecture must distinguish between risk-premium pricing and physical scarcity pricing, as these two market conditions have fundamentally different implications for duration, magnitude, and policy response.

-

Diplomatic timing is now the single most consequential variable: the pace of economic damage is running faster than the pace of negotiation, and that gap is widening daily.

-

Infrastructure investment cycles in alternative transit corridors, LNG terminal diversification, and strategic reserve expansion are entering a new phase of capital allocation intensity that will reshape global energy logistics for a generation.

-

Energy transition investment is being reinforced by the crisis as a strategic imperative for import-dependent economies, even as short-term fossil fuel demand spikes create a temporary emissions paradox.

The Strait of Hormuz has always been geography with consequences. The 2026 crisis has revealed, with painful clarity, just how many of those consequences were being quietly deferred rather than genuinely managed.

This article is intended for informational purposes only and does not constitute financial or investment advice. Commodity price data and market figures are subject to rapid change given evolving geopolitical conditions. Readers should consult qualified financial and energy market professionals before making investment decisions based on the information contained herein. The scenario analysis presented reflects analyst assessments as of May 12, 2026, and should not be interpreted as predictive certainty.

Want To Position Yourself Ahead of the Next Major Commodity Discovery?

The Hormuz crisis is reshaping global energy markets in real time, and Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries across more than 30 commodities — translating complex market shifts into clear, actionable opportunities for investors at every level. Explore how historic discoveries have generated substantial returns and begin your 14-day free trial today to ensure you're positioned before the broader market catches on.