August 5, 2026

What Makes China's Rare Earth Supply Chain Dominance So Comprehensive?

China's rare earth supply chain dominance emerges from a carefully orchestrated industrial strategy spanning three decades, built around technological mastery, vertical integration, and state-directed consolidation. This comprehensive control extends far beyond simple mining operations to encompass every critical stage of the value chain. Furthermore, the critical minerals strategy implemented by various governments highlights the strategic importance of these materials.

The Four Pillars of Strategic Control

The foundation of China's market position rests on state-orchestrated consolidation under two mega-corporations that manage approximately 95% of domestic production. China Northern Rare Earth (Group) High-Tech Co., Ltd. controls roughly 70% of operations, while China Minmetals Rare Earth Co., Ltd. manages secondary operations. This duopoly structure emerged following consolidation mandates from 2011-2015 under Chinese Ministry of Industry and Information Technology directives, creating unprecedented coordination across the supply chain.

Technology mastery represents the second pillar, achieved through cumulative R&D investment exceeding $40 billion over thirty years. Chinese state-sponsored research institutions, particularly the Chinese Academy of Sciences and affiliated research centers, have maintained dedicated rare earth research programs since the 1990s. This sustained investment has created proprietary separation technologies refined through decades of industrial application, generating institutional knowledge not easily replicated in newer Western facilities.

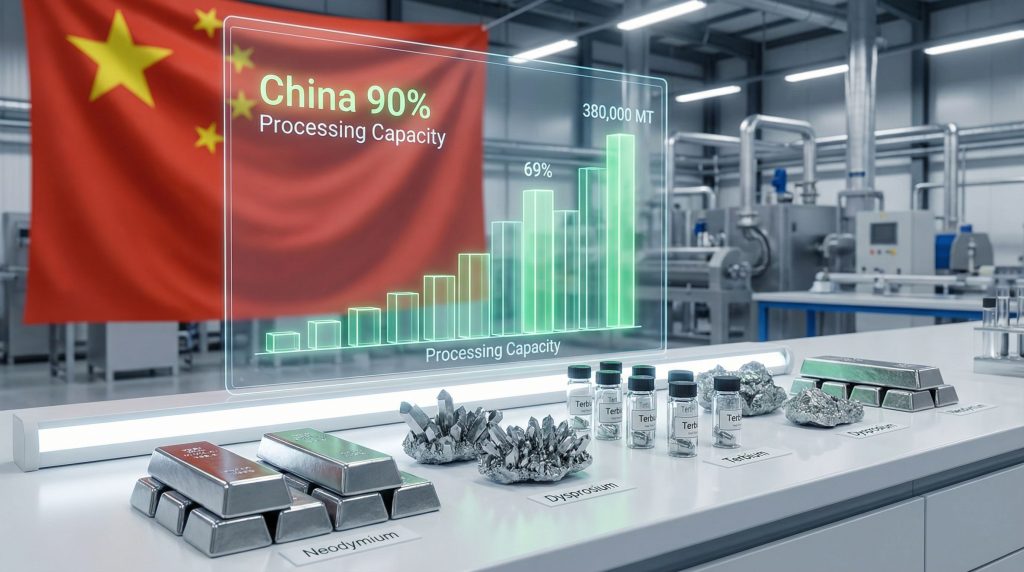

Vertical integration from mining to finished products constitutes the third strategic pillar. Chinese operations span mining in Inner Mongolia, Guangdong, and Sichuan provinces, primary processing through calcination and roasting, separation and purification where the 90% global monopoly exists, secondary processing converting materials to oxides and alloys, downstream manufacturing of magnets and catalysts, and final product assembly for motors and electronic components.

Export licensing serves as the fourth pillar, functioning as a geopolitical leverage tool. China implements export quotas through the Ministry of Commerce, with 2024 quotas set at approximately 270,000 MT compared to 290,000 MT in 2023. This quota system enables price manipulation capabilities and supply chain discipline across global markets.

Scale That Defies Competition

| Metric | China's Share | Global Total | Strategic Implication |

|---|---|---|---|

| Mining Production | 69% | 380,000 MT | Controls raw material access |

| Processing Capacity | 90% | N/A | Technological chokepoint |

| Heavy REE Processing | 95%+ | N/A | Critical defense applications |

| Export Quota Control | 270,000 MT | China-only | Price manipulation capability |

China produced approximately 270,000 tonnes of rare earth oxide equivalent in 2024, representing roughly 69% of global production capacity according to the U.S. Geological Survey. However, the processing capacity advantage proves more significant than raw production numbers suggest.

The separation technology complexity creates the highest technical barrier in the supply chain. The process involves acid or alkaline leaching of rare earth ores to create soluble compounds, selective precipitation using organic extractants such as tributyl phosphate, solvent extraction with multiple cascading stages typically requiring 15-30 extraction steps, and crystallisation and calcination to produce final products. Each stage requires precise environmental controls, waste acid management, and specialised equipment that Chinese facilities have optimised to reduce costs by 30-40% compared to newly constructed Western facilities.

China's dominance in heavy rare earth element processing reaches 95%+, particularly for dysprosium and terbium processing critical for defence applications. This concentration creates strategic vulnerabilities for Western defence contractors and technology manufacturers who require these materials for high-performance applications but lack alternative processing sources.

When big ASX news breaks, our subscribers know first

Why Traditional Trade Pressures Failed to Dent China's Market Position

Trade policy interventions designed to pressure China's manufacturing sector have largely failed to reduce the country's rare earth supply chain dominance, revealing structural resilience built into China's industrial ecosystem. The $1.037 trillion trade surplus achieved in the first eleven months of 2024 demonstrates this resilience despite sustained pressure from tariff regimes and export restrictions. In addition, the US‑China trade war impact has shown how China adapts its strategies to maintain market control.

The Transshipment Strategy Revolution

China's response to tariff pressure involved sophisticated route optimisation rather than production reduction. Chinese exports grew 5.4% year-over-year in the first eleven months of 2024 despite increased tariff pressures from the United States and European Union. This growth occurred through strategic redirection of trade flows rather than direct confrontation with tariff barriers.

Exports from China to Southeast Asia increased approximately 8% in 2024, significantly outpacing direct-to-Western markets routes. Vietnam, Thailand, and Malaysia have emerged as transshipment centres where intermediate processing adds minimal value before re-export to EU and USA markets. Singapore and Port Klang in Malaysia registered 12-15% increases in containerised trade flows containing Chinese components and finished goods destined for Western markets.

The transshipment mechanism operates through a four-step process:

• Goods manufactured in China shipped to Southeast Asian hub countries

• Light processing or value-addition occurring at hub facilities including assembly, repackaging, or labelling

• Re-export to final destination with certificate of origin from hub country

• Circumvention of origin-based tariff rules while maintaining supply chain efficiency

Third-country assembly models bypass direct restrictions whilst demonstrating supply chain flexibility that traditional trade policy cannot effectively counter. Vietnamese factories, predominantly owned or operated by Chinese entities, reported exporting approximately 1.2 million EV-related components to EU markets in 2024, representing a 45% year-on-year increase, despite Vietnam's domestic rare earth processing capacity remaining below 100 tonnes annually.

The $1 Trillion Surplus as Strategic Indicator

The record trade surplus signals manufacturing ecosystem strength embedded within broader industrial infrastructure. China's rare earth processing operates within this larger manufacturing complex, benefiting from shared infrastructure, workforce expertise, and financial systems that create mutual reinforcement across sectors.

Export growth acceleration of 5.4% despite international pressure demonstrates that structural advantages compound over cyclical policy interventions. Chinese export-import banks provide preferential lending rates 2-3% below market rates for rare earth and critical mineral exports, enabling Chinese exporters to absorb tariff costs whilst maintaining margins. Estimated annual subsidy value reaches $5-8 billion according to World Bank reporting on Chinese development finance.

The Chinese yuan maintained relative stability at 7.0-7.3 USD per CNY throughout 2024, combined with capital controls preventing depreciation to maintain price competitiveness despite higher input costs. This monetary stability, supported by People's Bank of China foreign exchange management, insulates Chinese exporters from currency-based competitive pressure.

Downstream product embedding represents perhaps the most significant factor in tariff policy failure. Rather than exporting raw rare earths, China strategically shifted export composition toward value-added products. Direct rare earth oxide exports constitute approximately 15% of total rare earth-related exports in 2024, whilst rare earth-containing products including magnets, alloys, and finished components represent 45%, and EV components, motors, generators, and electronics account for 40%.

This composition shift reduces tariff exposure because tariffs on assembled products typically remain lower than tariffs on raw materials or intermediate products. When Europe imports assembled EVs, tariff classification becomes technically difficult since Chinese EV manufacturers build permanent magnet motors directly into vehicles, making separation of Chinese rare earth processing from final assembled vehicles problematic for customs enforcement.

How China's EV Export Boom Deepens Global Rare Earth Dependency

China's electric vehicle export surge creates unprecedented rare earth dependency layers that extend far beyond the vehicles themselves. Chinese EV exports to Europe increased 53% in November 2024 compared to November 2023, whilst cumulative 2024 exports reached approximately 1.56 million vehicles globally, representing 56% year-over-year growth according to the China Association of Automobile Manufacturers. However, this growth follows broader patterns in the mining industry evolution across critical materials.

The Embedded Supply Chain Problem

Each Chinese EV exported carries multiple layers of rare earth processing that importing countries cannot replicate at scale. Every NdFeB permanent magnet motor installed in Chinese EVs contains 1-2 kg of rare earth elements, with dysprosium and terbium comprising 8-12% of magnet composition according to Magnetics Technology International specifications.

The embedded processing steps create asymmetric dependency structures:

• Primary processing converting rare earth ores to oxides requires acid leaching infrastructure typically unavailable outside China and Malaysia

• Separation steps converting oxides to individual rare earth chlorides and fluorides require solvent extraction capabilities monopolised by China at 90% global capacity

• Alloy preparation combining rare earths with iron, boron, and cobalt requires specialised metallurgical facilities

• Magnet manufacturing involving sintering, coating, and magnetisation remains 80% controlled by Chinese facilities

• Motor assembly integrating components into EV powertrains represents the final value-addition step

When Europe imports assembled EVs, it acquires only the final assembly step whilst depending on Chinese control of the preceding four processing stages. This creates vulnerability where China can restrict rare earth exports and disrupt European EV production, whilst Europe cannot easily substitute processing capacity without multi-year capital investment exceeding $1 billion per integrated facility.

European permanent magnet production capacity stands at approximately 8,000-10,000 MT annually, insufficient to supply EV motor demand estimated at 180,000+ MT equivalent by 2024. The EU imported approximately 95,000 MT of rare earth-containing components and finished magnets in 2024, with China supplying 87% of volume according to European Commission trade statistics.

Beyond Vehicles: The Downstream Multiplication Effect

The multiplication effect extends beyond automotive applications into industrial infrastructure that amplifies dependency relationships across multiple sectors simultaneously.

Wind turbine generators require 200-600kg of rare earth magnets per unit, creating additional dependency layers in European renewable energy infrastructure. China controls approximately 75% of global wind turbine magnet production capacity, meaning European climate goals depend on Chinese rare earth processing capabilities.

Industrial automation systems embed Chinese-processed materials throughout manufacturing infrastructure. European factories installing Chinese-manufactured robotics and automation equipment create long-term maintenance and replacement part dependencies on Chinese supply chains.

Consumer electronics maintain rare earth component dependencies that compound automotive sector exposure. European imports of smartphones, laptops, and consumer appliances contain Chinese-processed rare earth materials, creating parallel dependency structures across consumer and industrial sectors.

European EV production targets of 18+ million vehicles annually by 2030 would require 360,000-540,000 MT of rare earth magnets according to European Commission projections. Current European production capacity including operational and planned facilities totals only 35,000-40,000 MT, creating a structural gap that cannot be filled without sustained investment programmes extending beyond 2030.

Chinese manufacturers have strategically positioned themselves to supply not just vehicles but entire technological ecosystems. Battery management systems, charging infrastructure, and grid integration components all contain Chinese-processed rare earth materials, creating comprehensive dependency relationships that extend across energy transition infrastructure.

What Strategic Vulnerabilities Exist in China's Rare Earth Fortress?

Despite comprehensive market dominance, China's rare earth empire contains structural vulnerabilities that create potential pressure points for competitors and geopolitical leverage opportunities for other nations. These vulnerabilities span supply chain dependencies, economic sustainability challenges, and resource constraints that could reshape market dynamics. Furthermore, recent developments regarding China's rare earth export controls highlight how China uses these materials for strategic advantage.

The Myanmar Supply Chain Achilles' Heel

China sources approximately 50% of its heavy rare earth inputs from northern Myanmar, creating a critical dependency relationship that introduces supply instability into China's processing operations. Armed group control in Myanmar's northern regions creates operational uncertainties that Chinese processors cannot fully control through standard commercial relationships.

Heavy rare earth elements including dysprosium and terbium prove essential for high-performance permanent magnets used in defence applications, wind turbines, and electric vehicle motors. Myanmar supplies concentrate primarily through informal mining operations that lack environmental oversight and operate outside standard international commercial frameworks.

Illegal mining operations pose reputational and operational risks for Chinese processors who rely on Myanmar inputs. International sanctions targeting Myanmar's military government create compliance challenges for Chinese companies processing Myanmar-sourced materials, particularly when selling finished products to Western markets.

Supply chain disruption scenarios in Myanmar could force Chinese processors to rely more heavily on domestic deposits, which contain lower heavy rare earth concentrations and require more intensive processing. This would increase production costs and potentially reduce China's competitive advantage in heavy rare earth processing.

Economic Sustainability Questions

China's market dominance relies partly on below-cost production strategies designed to maintain market share rather than maximise profitability. State subsidies enable Chinese processors to undercut international competitors by 15-25%, but this approach creates long-term financial sustainability challenges.

Chinese rare earth processing generates significant environmental liabilities including acid waste and radioactive thorium tailings that impose cleanup costs potentially reaching $50-100 billion over coming decades. These environmental costs are currently externalised through regulatory frameworks that may face pressure for reform as environmental awareness increases in China.

Oversupplied markets create pricing pressure that reduces profitability across Chinese rare earth operations. Global rare earth oxide prices declined 15-25% in 2024 despite strong demand growth, indicating that supply expansion has outpaced market absorption capacity.

Resource depletion concerns emerge in key domestic deposits including Inner Mongolia's Bayan Obo mine, which has supplied rare earths for over 30 years. Declining ore grades require more intensive processing and higher energy consumption, gradually eroding cost advantages that support China's export pricing strategies.

State-owned enterprise efficiency challenges compound sustainability pressures. Chinese rare earth companies operate under political objectives that prioritise market share maintenance over profit optimisation, creating potential conflicts between commercial viability and strategic policy goals.

Long-term demographic trends in China including workforce aging and rising labour costs will gradually increase operational expenses for rare earth processing facilities. These cost pressures may require productivity improvements or price increases that could create opportunities for international competitors.

How Diversification Efforts Stack Against China's Strategic Advantages

Western diversification initiatives face substantial structural challenges when competing against China's established rare earth supply chain advantages. Despite significant investment commitments and policy support, alternative supply sources struggle to achieve cost parity and technological equivalence with Chinese operations. Moreover, the establishment of a critical raw materials facility represents efforts to address these challenges.

Western Response Timeline Analysis

| Project | Country | Status | Expected Production | Timeline Gap |

|---|---|---|---|---|

| Mountain Pass | USA | Operational | 38,000 MT/year | Processing limited |

| Lynas Malaysia | Australia/Malaysia | Operational | 22,000 MT/year | Heavy REE deficit |

| MP Materials | USA | Expanding | 50,000 MT target | 2026-2027 |

| European projects | Various | Planning | 15,000 MT combined | 2028+ |

MP Materials operates Mountain Pass, the largest rare earth mine in the Western hemisphere, producing 38,000 MT annually by 2024. However, the facility relies on contract processing agreements with Chinese entities for 85% of separation work, creating circular dependency where only approximately 6,000 MT undergoes domestic processing. Full domestic processing requires capital investment exceeding $1.5 billion and 8-10 year development timelines according to SEC filings.

Lynas Rare Earths operates processing facilities in Malaysia and expansion projects in Texas, currently processing approximately 22,000 tonnes per annum. Despite being the largest non-Chinese processor, heavy rare earth processing capacity remains below 5,000 tonnes annually, separation efficiency lags Chinese competitors by 15-20%, and production costs run 25-35% higher than Chinese equivalents according to ASX announcements and annual reports.

European rare earth projects remain primarily in planning phases with combined expected production of 15,000 MT not anticipated before 2028. These projects face regulatory approval timelines extending 3-5 years, environmental compliance requirements that add 15-25% to operational costs, and skilled workforce development challenges in regions without existing rare earth expertise.

The Processing Technology Gap

Separation technology mastery requires 20-30 years to achieve competitive efficiency levels comparable to Chinese operations. Western facilities attempting to replicate Chinese separation processes face knowledge gaps in process optimisation, equipment calibration, and waste stream management that cannot be bridged through capital investment alone.

Environmental compliance adds substantial cost and complexity to Western rare earth processing. EPA regulations in the United States and equivalent standards in Europe require waste acid neutralisation, tailings containment, and radioactive material handling procedures that Chinese facilities operate under less stringent oversight. These compliance requirements typically add 15-25% to operational costs.

Skilled workforce development takes decades in regions without existing rare earth industrial infrastructure. Chemical engineers, metallurgical specialists, and equipment operators require specialised training programmes and practical experience that cannot be rapidly scaled. Chinese facilities benefit from multi-generational workforce experience accumulated over 30+ years of continuous operations.

Capital requirements for integrated rare earth processing facilities exceed $1 billion according to industry assessments. These investments require long-term capital commitment with uncertain returns given China's ability to respond with increased production or price competition. Financial risk assessment complicates project financing for Western rare earth initiatives.

Technology transfer restrictions limit Western access to proven Chinese processing methods. Intellectual property controls and national security considerations prevent direct technology acquisition, forcing Western projects to develop proprietary processes through time-intensive research and development programmes.

Supply chain integration challenges emerge when Western processing facilities attempt to secure reliable feedstock supplies. Long-term offtake agreements with mining operations require coordination across multiple countries and regulatory jurisdictions, creating complexity that integrated Chinese operations avoid through domestic supply chain control.

What Scenarios Could Reshape Global Rare Earth Supply Chains?

Multiple potential disruption scenarios could fundamentally alter rare earth supply chain dynamics over the next decade. These scenarios range from coordinated Western industrial policy responses to technological breakthroughs and geopolitical supply disruptions that would force rapid market restructuring. However, as demonstrated by the critical minerals executive order, government intervention continues to play a crucial role in shaping these markets.

Scenario 1: Accelerated Western Industrial Policy

Coordinated US-EU-Japan investment programmes could mobilise sufficient capital to establish meaningful alternative processing capacity by 2030. This scenario involves Defence Production Act-style rare earth mandates requiring domestic content quotas for defence contractors and critical infrastructure projects.

Strategic petroleum reserve model implementation for critical materials would create government-backed demand for Western rare earth production. National stockpiles requiring 90-180 day supply buffers would provide guaranteed offtake agreements that justify large-scale capital investment in processing facilities.

Technology sharing agreements between allied nations could accelerate separation technology development and reduce individual country investment requirements. Collaborative research programmes combining US Department of Energy resources, European Horizon programmes, and Japanese industrial partnerships could compress technology development timelines from 20+ years to 10-15 years.

Timeline projections for this scenario suggest meaningful production shifts beginning 2025-2027 with substantial market share redistribution completed by 2030. Success requires sustained political commitment across election cycles and coordination mechanisms that override individual country commercial interests.

Scenario 2: Alternative Technology Breakthroughs

Rare earth-free permanent magnet development represents the highest-impact potential disruption for China's supply chain dominance. Multiple research programmes including ferrite-based alternatives, organic permanent magnets, and hybrid magnetic systems could eliminate neodymium and dysprosium requirements in key applications.

Recycling technology achieving commercial scale could provide 20-30% of rare earth demand by 2035 according to industry projections. Advanced separation techniques for end-of-life electronics, automotive components, and wind turbine magnets could create domestic supply sources in consuming countries that bypass primary mining and processing.

Substitution materials in key applications particularly for automotive and renewable energy sectors could reduce rare earth intensity per unit of production. Alternative motor designs, improved ferrite magnets, and electromagnetic alternatives could maintain performance whilst reducing rare earth content requirements.

Timeline estimates for technology disruption suggest proof-of-concept demonstrations by 2026-2028 with commercial deployment potential reaching market scale between 2028-2035. However, technology adoption faces performance trade-offs and capital investment requirements that may slow market penetration.

Scenario 3: Geopolitical Supply Disruption

Taiwan conflict scenarios could severely impact rare earth supply chains through multiple transmission mechanisms. Naval blockade operations could disrupt Chinese export capabilities, whilst Taiwan semiconductor manufacturing disruption would reduce demand for rare earth-intensive electronic components, creating complex supply-demand imbalances.

Myanmar instability cascading effects could eliminate 50% of China's heavy rare earth feedstock, forcing reliance on domestic deposits with lower ore grades and higher processing costs. Armed conflict expansion in northern Myanmar could physically disrupt mining operations for extended periods.

Export restriction escalation patterns could emerge if trade tensions intensify beyond current tariff regimes. China could implement rare earth export licensing requirements similar to historical 2010-2012 restrictions that created 300-400% price increases for certain elements.

Emergency stockpile activation requirements would test government preparedness for supply disruption scenarios. Current strategic reserves in the United States, Japan, and Europe provide 30-90 day supply buffers that prove insufficient for extended disruption periods requiring 6+ months to resolve.

Supply chain regionalisation could accelerate rapidly under geopolitical pressure scenarios. Emergency policies might prioritise regional suppliers despite higher costs, creating opportunities for Australian, Canadian, and other allied nation projects that currently lack commercial competitiveness.

The next major ASX story will hit our subscribers first

How Should Investors and Policymakers Prepare for Supply Chain Realities?

The persistent nature of China's rare earth supply chain dominance requires strategic preparation acknowledging realistic timelines for alternative supply development whilst building resilience against potential disruption scenarios. Investment strategies and policy interventions must balance long-term diversification goals with near-term supply security requirements.

Investment Strategy Implications

Diversification projects face 5-10 year development timelines that require patient capital and sustained management commitment through multiple commodity price cycles. Investors in Western rare earth projects must prepare for extended development periods with uncertain returns given China's ability to respond with competitive production increases.

Chinese downstream dominance continues expanding whilst Western efforts focus on upstream mining and processing. Investment opportunities increasingly concentrate in specialised applications, recycling technologies, and alternative materials research rather than direct competition with Chinese separation capacity.

Technology transfer restrictions limit Western access to proven processing methods, creating opportunities for companies developing proprietary separation technologies or alternative approaches to rare earth processing. Intellectual property development in separation chemistry and equipment design could generate substantial returns.

Resource security premiums justify higher cost alternatives in specific market segments including defence applications, critical infrastructure, and high-reliability industrial systems. Premium pricing for certified non-Chinese supply sources creates market opportunities for Western producers despite cost disadvantages.

Vertical integration strategies prove essential for Western rare earth projects to achieve competitive positioning. Companies controlling mining through processing to finished products can capture value across the supply chain and reduce exposure to Chinese intermediate processing.

Policy Intervention Effectiveness Analysis

The most effective rare earth supply chain diversification requires simultaneous investment in mining, processing technology, and downstream manufacturing capabilities, with realistic timelines extending 10-15 years for meaningful market share shifts. Policy programmes addressing only individual supply chain segments prove insufficient to create competitive alternatives.

Strategic stockpiling for 90-180 day supply buffers provides essential short-term resilience against supply disruption scenarios whilst longer-term diversification develops. Government stockpile programmes create guaranteed demand that supports Western processing facility development.

Dual-sourcing requirements for critical applications force defence contractors and infrastructure operators to develop alternative supply relationships despite higher costs. Regulatory mandates requiring non-Chinese supply percentages create market demand that justifies investment in Western processing capacity.

Technology development incentives for alternatives including rare earth-free permanent magnets, improved recycling processes, and substitution materials could reduce overall dependence on primary rare earth supply chains. Research funding targeting breakthrough technologies offers potentially higher returns than incremental processing capacity expansion.

International cooperation agreements for supply security enable burden-sharing across allied nations whilst avoiding duplication of expensive processing infrastructure. Coordinated investment in complementary capabilities across multiple countries could achieve collective supply security more efficiently than individual national programmes.

Risk Management Framework

Supply chain risk assessment must incorporate both gradual competitive pressure and sudden disruption scenarios that could eliminate Chinese supply access within months. Emergency preparedness requires contingency planning for multiple disruption types including trade restrictions, geopolitical conflict, and natural disasters affecting Chinese operations.

Inventory management strategies should balance carrying costs against supply disruption risks through optimised safety stock levels tailored to specific applications and supply chain characteristics. Critical applications requiring guaranteed supply availability justify higher inventory investment.

Alternative material qualification processes for key applications reduce dependency on specific rare earth elements whilst maintaining performance requirements. Engineering programmes developing approved alternatives create supply chain flexibility that reduces exposure to single-source disruptions.

Financial hedging instruments for rare earth price volatility provide protection against sudden cost increases resulting from supply disruptions or export restrictions. Commodity hedging strategies must account for limited liquidity in rare earth futures markets.

Supply chain monitoring systems tracking Chinese production capacity, export policies, and alternative supply development enable early warning for potential disruptions. Intelligence gathering on Chinese industry consolidation and policy changes provides strategic planning inputs for Western companies and governments.

What Does the Future Hold for Global Rare Earth Supply Chain Control?

Long-term projections for rare earth supply chain evolution suggest gradual diversification rather than dramatic shifts away from Chinese dominance. Structural advantages built over three decades cannot be rapidly replicated, but sustained investment in alternative capacity will eventually create meaningful competition and supply security improvements.

The 2030 Projection Landscape

China maintains 60-70% market share despite diversification efforts as processing technology gaps and cost advantages prove durable competitive barriers. Western processing capacity reaches 25-30% of global demand through successful project development in Australia, United States, and Europe, but remains concentrated in light rare earth processing with heavy rare earth dependency persisting.

Heavy rare earth dependency remains concentrated in China through 2030 despite Myanmar supply concerns and Western government investment programmes. Alternative heavy rare earth sources including Canadian deposits and deep-sea mining exploration require longer development timelines extending beyond 2030 for meaningful production.

Downstream product embedding strategies continue expanding as China moves further up the value chain into finished components and assembled products. Chinese manufacturers increasingly export permanent magnet motors, battery systems, and electronic assemblies rather than raw materials, making trade policy interventions less effective.

Regional supply chain networks emerge around Chinese, American, and European processing hubs with limited cross-regional material flows. Trade policy pressures accelerate regionalisation trends that create parallel supply chains serving different geographic markets rather than globally integrated competition.

Technology development programmes in recycling and alternative materials begin commercial deployment by 2028-2030, providing 15-20% of rare earth demand through secondary sources. However, growing overall demand for electrification and renewable energy continues requiring primary supply expansion.

Long-term Strategic Equilibrium

Multipolar supply chain emergence by 2035 creates more balanced global rare earth processing capacity distributed across multiple regions and countries. Chinese market share declines to 50-55% as Western and allied nation capacity reaches commercial scale through sustained investment programmes.

Technology diffusion enables broader processing capability as separation knowledge spreads through research collaboration, workforce mobility, and technology licensing agreements. Processing cost gaps narrow but persist due to scale advantages and accumulated expertise in Chinese operations.

Resource nationalism increases across producing countries as governments recognise rare earth strategic value and implement policies requiring domestic processing before export. New mining operations increasingly include processing requirements that fragment global supply chains.

Supply chain regionalisation accelerates post-2030 as trade tensions and security concerns drive geographic concentration of critical materials within allied nation networks. Regional processing capacity serves local manufacturing whilst reducing dependency on cross-regional material flows.

Alternative technology adoption reaches 30-40% market penetration by 2040 as rare earth-free permanent magnets, advanced recycling systems, and substitution materials achieve cost competitiveness with traditional applications. Technology substitution reduces overall rare earth demand growth despite continued electrification trends.

Investment patterns shift toward specialised applications and high-purity processing as commodity rare earth markets become increasingly competitive. Value creation concentrates in technology development, specialised grades, and application-specific materials rather than large-scale commodity production.

What Are the Key Challenges in Breaking China's Rare Earth Dominance?

Breaking China's rare earth supply chain dominance requires overcoming multiple interrelated challenges that compound over time. Processing technology gaps represent the most significant barrier, as Chinese facilities benefit from 30+ years of continuous optimisation and accumulated expertise that cannot be rapidly replicated through capital investment alone.

Environmental compliance costs in Western jurisdictions add 15-25% to operational expenses compared to Chinese facilities operating under different regulatory frameworks. This cost differential makes it difficult for Western processors to achieve price competitiveness without sustained subsidies or protected market access.

Workforce development challenges emerge in regions without existing rare earth industrial infrastructure. Chemical engineers, metallurgical specialists, and equipment operators require specialised training programmes and hands-on experience that cannot be rapidly scaled to support new processing facilities.

How Do Geopolitical Tensions Affect Rare Earth Supply Chains?

Geopolitical tensions create both risks and opportunities within rare earth supply chains through multiple transmission mechanisms. Export restriction escalation could replicate China's 2010-2012 rare earth embargo that caused 300-400% price increases for certain elements and accelerated Western diversification efforts.

Taiwan conflict scenarios would severely disrupt both supply and demand sides of rare earth markets. Chinese export capabilities could face disruption whilst semiconductor manufacturing reductions would reduce demand for rare earth-intensive electronic components, creating complex market imbalances.

Trade policy interventions including tariffs and investment restrictions have shown limited effectiveness in reducing China's market share, as Chinese companies adapt through transshipment strategies and downstream product embedding that circumvents origin-based trade barriers.

Can Alternative Technologies Reduce Rare Earth Dependence?

Alternative technologies offer the most promising pathway for reducing structural dependence on Chinese rare earth processing, though commercial deployment timelines extend to 2028-2035 for meaningful market impact. Rare earth-free permanent magnet development represents the highest-impact potential disruption, with multiple research programmes exploring ferrite-based alternatives and hybrid magnetic systems.

Recycling technology achieving commercial scale could provide 20-30% of rare earth demand by 2035, creating domestic supply sources in consuming countries that bypass primary mining and processing dependencies. However, recycling cannot eliminate primary production requirements due to growing demand and material losses during processing.

Substitution materials in automotive and renewable energy applications could reduce rare earth intensity per unit whilst maintaining performance characteristics. Alternative motor designs and improved ferrite magnets show promise for reducing rare earth content requirements in key applications.

Disclaimer: This analysis contains forward-looking projections and scenario assessments that involve significant uncertainty. Actual market developments may differ materially from projections due to technological, political, and economic factors not fully predictable at present. Investment decisions should incorporate additional research and professional consultation.

Want to Capitalise on Mining's Next Major Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications when significant mineral discoveries hit the ASX, transforming complex mining announcements into actionable investment insights. With growing demand for critical minerals and rare earths creating unprecedented opportunities, discover how historic finds like De Grey Mining and WA1 Resources generated substantial returns by exploring Discovery Alert's dedicated discoveries page showcasing exceptional market outcomes. Begin your 30-day free trial today and position yourself ahead of the market when the next transformative discovery emerges.