July 5, 2026

China's rare earth supply chain leverage has emerged as one of the most significant strategic vulnerabilities facing Western economies in the modern era. Looking at the global critical materials landscape reveals a complex web of interdependencies where resource control translates directly into strategic advantage. While traditional geopolitical power once flowed from military might or economic output, today's influence increasingly stems from controlling the materials essential to modern technology, energy systems, and defense capabilities.

This shift represents more than simple market dynamics. Nations that command critical mineral supply chains wield unprecedented leverage over industries spanning electric vehicles to renewable energy infrastructure. Understanding these dependencies and their implications has become essential for investors, policymakers, and business leaders navigating an increasingly resource-constrained world.

Understanding China's Critical Materials Dominance Strategy

The foundation of China's strategic materials advantage rests on four interconnected pillars that create a comprehensive system of control across the entire value chain. This architecture reflects decades of coordinated industrial policy rather than market-driven development, particularly as the mining industry evolution has shifted towards strategic resource concentration.

The Four Pillars of Resource Control

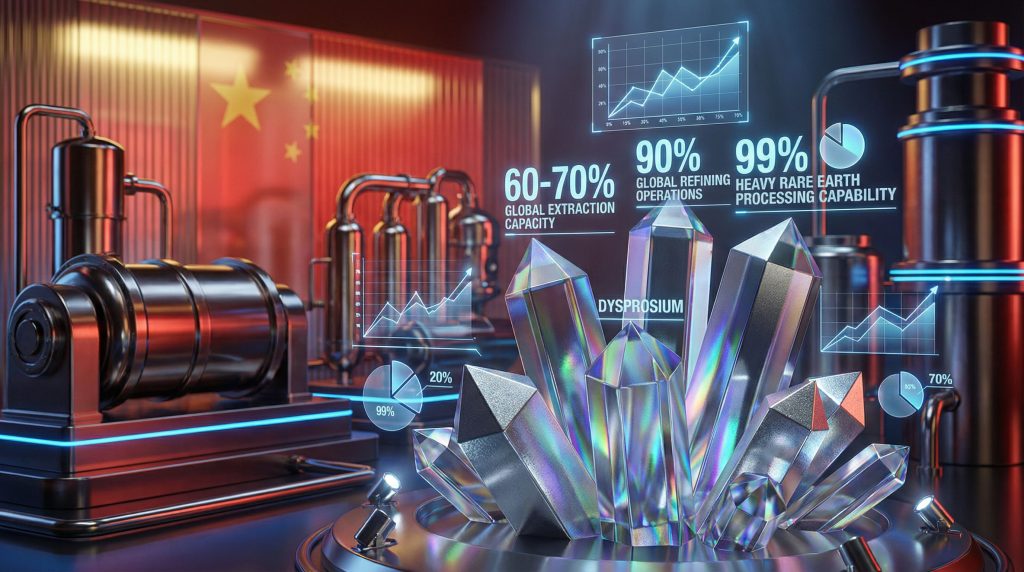

China's dominance extends far beyond simple mining operations to encompass the entire critical materials ecosystem. The country controls approximately 60-70% of global rare earth extraction capacity, providing the foundation for downstream advantages. More significantly, China maintains 90% of global rare earth refining operations, creating a chokepoint that even countries with domestic mining cannot easily bypass.

Manufacturing integration represents the third pillar, with China producing 85% of global lithium-ion batteries and commanding similar market shares in permanent magnet production. The fourth pillar involves technology gatekeeping, particularly in heavy rare earth processing where China maintains 99% of global processing capability for elements like dysprosium and terbium.

This vertical integration creates what industry analysts describe as a strategic moat. Unlike traditional commodity markets where production can shift between regions based on cost advantages, rare earth supply chains require specialised processing facilities, environmental permits, and technical expertise that take years to develop.

Strategic Timeline of Market Capture (2000-2026)

China's market control has evolved through distinct phases, with strategic implications becoming more apparent over time. The following data illustrates this progression:

| Year | Mining % | Refining % | Magnet Production % |

|---|---|---|---|

| 2000 | 85% | 95% | 90% |

| 2010 | 95% | 97% | 95% |

| 2020 | 70% | 90% | 90% |

| 2026 | 60% | 90% | 90% |

This timeline reveals several critical patterns. The peak control period occurred around 2010, when China maintained near-monopoly positions across all segments. The subsequent decline in mining share reflects both resource depletion in some Chinese deposits and the development of alternative sources like Mountain Pass in the United States and Mount Weld in Australia.

However, China's refining and manufacturing dominance has remained largely intact. This persistence highlights the distinction between raw material extraction and value-added processing. While mining operations can be established relatively quickly given sufficient capital, building refining capacity requires overcoming technical, environmental, and regulatory barriers that favour established players.

The 2026 figures represent current market conditions, where China has transitioned from overwhelming dominance to strategic control. This evolution suggests a more sophisticated approach focused on maintaining leverage while avoiding the vulnerabilities that come with excessive concentration. Furthermore, Zijin mining expansion demonstrates how Chinese companies continue to strengthen their global positions.

When big ASX news breaks, our subscribers know first

How Does China Exercise Supply Chain Leverage?

China's approach to supply chain leverage operates through multiple mechanisms that extend beyond traditional export controls. These tools create layers of influence that can be activated individually or in combination, depending on strategic objectives. Consequently, China's rare earth supply chain leverage has become increasingly sophisticated in recent years.

Export Control Mechanisms and Their Applications

The evolution of China's export control system demonstrates increasing sophistication in applying supply chain pressure. Licensing requirements for critical grade materials create administrative barriers that can slow or redirect trade flows without triggering formal trade disputes. These systems particularly affect high-purity materials used in defence and semiconductor applications.

Technology transfer restrictions represent another layer of control, particularly affecting separation and processing technologies. Foreign companies seeking to establish rare earth processing facilities often find themselves dependent on Chinese technical expertise, creating ongoing relationships that extend beyond simple buyer-seller dynamics.

Quota systems targeting specific applications have emerged as particularly effective tools. By differentiating between civilian and military end-uses, China can maintain normal commercial relationships while creating pressure points for strategic industries.

Recent 2025 export controls specifically target applications with dual-use potential, creating immediate supply vulnerabilities for Western defence contractors while maintaining commercial availability for civilian applications.

The 2025 export control tightening represented a significant escalation in China's willingness to use supply chain leverage as a geopolitical tool. These controls specifically targeted high-performance magnets and battery-grade materials, affecting industries central to both the critical minerals energy transition and national security.

Price Manipulation Through Strategic Stockpiling

State reserve management provides China with tools to influence global pricing independent of production decisions. Strategic releases can dampen prices when Chinese manufacturers need cheaper inputs, while reserve accumulation can support prices when domestic producers require higher margins.

The coordination of release timing with geopolitical objectives creates additional leverage. Market psychology plays a significant role in rare earth pricing, with traders and manufacturers often adjusting purchasing patterns based on perceived political risks rather than fundamental supply-demand dynamics.

This psychological impact amplifies China's influence beyond its actual market share. Even the prospect of export restrictions can drive panic buying and inventory building, creating artificial scarcity that benefits Chinese suppliers while imposing costs on foreign manufacturers.

Which Industries Face the Greatest Vulnerability?

Understanding sectoral vulnerabilities requires examining both the criticality of rare earth inputs and the availability of alternatives. Industries with the greatest exposure combine high technical performance requirements with limited substitution options.

Electric Vehicle Manufacturing Exposure

The electric vehicle sector represents perhaps the most significant concentration of rare earth dependency in modern manufacturing. Neodymium-iron-boron magnets account for roughly 15-20% of the material cost in high-performance EV traction motors, with no viable alternatives delivering comparable power density and efficiency.

Battery cathode material dependencies create additional vulnerabilities, particularly for lithium iron phosphate and nickel-cobalt-manganese chemistries. While raw lithium can be sourced from multiple regions, the processing required to produce battery-grade compounds remains heavily concentrated in China.

Chinese EV manufacturers benefit from integrated supply chains that provide both cost advantages and supply security. Companies like NIO have demonstrated the strategic value of this integration, achieving 18% gross margins in Q4 2025 while Western competitors struggle with supply chain costs and uncertainty.

The competitive implications extend beyond individual companies to entire national automotive industries. European and American automakers increasingly function as assemblers of Chinese components, capturing diminishing value while their Chinese competitors control the most profitable segments of the supply chain.

Defence and Aerospace Critical Dependencies

Defence applications create unique vulnerabilities due to their specific performance requirements and limited supplier qualification processes. Precision-guided munitions rely on rare earth magnets for guidance systems that cannot accept performance compromises for supply chain diversification.

Fighter jet permanent magnet motor systems present similar challenges, requiring materials that meet stringent specifications for temperature, magnetic field strength, and reliability. The long development timelines for military systems make rapid supplier changes particularly difficult.

Satellite and radar component dependencies create additional strategic risks. These systems often operate in extreme environments where material performance cannot be compromised, limiting the effectiveness of substitution strategies.

The defence sector's vulnerability is compounded by security clearance requirements that limit supplier options even when alternative materials are available. This creates a strategic paradox where national security considerations restrict the supply chain diversification needed to enhance national security.

Renewable Energy Infrastructure Risks

Wind turbine generator magnet supplies represent one of the largest volume applications for rare earth materials outside of electric vehicles. Direct-drive wind turbines require 600-1,000 kilograms of rare earth magnets per megawatt of capacity, creating massive material requirements for renewable energy buildouts.

Solar panel rare earth component dependencies, while smaller in volume, affect critical performance characteristics. Rare earth elements in photovoltaic cells enhance light absorption and conversion efficiency, with substitutes often requiring design compromises that reduce overall system performance.

Grid-scale energy storage systems increasingly rely on advanced battery chemistries that incorporate rare earth materials. As energy storage becomes essential for renewable energy integration, these dependencies will expand throughout the electricity system.

What Are the Economic Implications of This Leverage?

China's rare earth supply chain leverage creates both direct cost advantages for Chinese manufacturers and structural disadvantages for competitors. These effects compound over time as integrated supply chains enable reinvestment in R&D and capacity expansion, particularly as US–China trade impacts continue to reshape global supply chains.

Cost Structure Advantages for Chinese Manufacturers

Vertical integration in rare earth supply chains provides Chinese manufacturers with 15-25% cost advantages compared to competitors dependent on market purchases. This advantage stems from eliminating margin stacking at each processing stage and reducing transaction costs associated with supplier management.

Environmental externalisation creates additional pricing gaps, as Chinese rare earth operations historically accepted environmental costs that would be prohibitive in Western jurisdictions. While environmental standards have tightened in China, the legacy cost structure advantages remain embedded in existing facilities.

State subsidy amplification of competitive positioning extends beyond direct financial support to include infrastructure investment, preferential energy pricing, and regulatory streamlining. These advantages create sustainable cost differentials that persist even when direct subsidies are reduced.

Western Industrial Response Patterns

The response to China's rare earth leverage has varied significantly across regions and industries, reflecting different strategic priorities and resource availability:

| Region | Investment ($B) | Timeline | Capacity Target |

|---|---|---|---|

| United States | 12.8 | 2026-2030 | 25% independence |

| European Union | 8.4 | 2025-2029 | 30% independence |

| Japan/Australia | 6.2 | 2024-2028 | 40% independence |

These investment levels, while substantial, remain modest compared to China's decades of accumulated investment in rare earth infrastructure. The timeline for meaningful capacity additions reflects the technical complexity and regulatory requirements for establishing alternative supply chains.

Regional variations in targets reflect different strategic approaches. Japan and Australia's higher independence targets reflect geographic proximity to Chinese supply chain disruption risks, while the United States and European Union balance supply security concerns against economic efficiency considerations. In addition, European CRM facility development efforts aim to reduce dependency through strategic investments.

How Effective Are Current Countermeasures?

Evaluating countermeasures requires understanding both the technical feasibility and economic viability of alternative approaches. Current efforts span supply diversification, recycling enhancement, and substitution research, each with distinct advantages and limitations.

Alternative Supply Development Challenges

Building alternative rare earth supply capacity faces significant barriers that extend beyond simple capital requirements. Capital intensity requirements of $2-5 billion per integrated facility reflect the complexity of establishing both mining and processing capabilities.

Environmental permitting timelines averaging 5-8 years create additional barriers, particularly for refining facilities that handle radioactive materials and generate toxic waste streams. These timelines exceed typical business planning horizons, making private investment difficult to justify.

Technical expertise gaps in processing technologies represent perhaps the most significant challenge. Rare earth separation and purification require specialised knowledge that developed over decades in Chinese operations. Building this expertise in Western countries requires substantial time and investment in human capital development.

Building meaningful rare earth supply independence requires 7-10 years and $50+ billion in coordinated Western investment across mining, processing, and manufacturing capabilities.

Recycling and Substitution Limitations

Current recycling rates for rare earth materials remain below 5% for most elements, reflecting both technical challenges and economic constraints. Rare earth recycling requires sophisticated separation processes similar to primary production, limiting cost advantages.

Performance trade-offs in alternative magnet materials create additional barriers to substitution. Ferrite magnets can replace rare earth magnets in some applications but require significantly larger volumes to achieve equivalent performance, affecting system design and efficiency.

Economic viability thresholds for secondary recovery depend heavily on rare earth prices, which China can influence through supply policy decisions. This creates a strategic vulnerability where China can potentially undermine alternative supply development by reducing prices during critical investment periods.

What Are the Long-Term Strategic Scenarios?

Analysing potential future scenarios requires considering technological developments, geopolitical dynamics, and economic incentives that will shape rare earth markets over the next decade. However, the impact of rare earth restrictions continues to reshape strategic planning across sectors.

Scenario 1: Sustained Chinese Dominance (Probability: 60%)

This scenario assumes China maintains current levels of supply chain control through 2035, leveraging continued cost advantages and technical expertise. Key characteristics include:

- Continued cost advantages through vertical integration and scale economies

- Selective leverage application during geopolitical tensions rather than comprehensive export bans

- Western acceptance of strategic dependency in exchange for economic efficiency

- Chinese investment in next-generation processing technologies that maintain technological leadership

Under this scenario, rare earth supply chains remain concentrated but stable, with China using leverage strategically rather than disruptively. Western countermeasures achieve limited success in reducing dependency while imposing higher costs on domestic industries.

Scenario 2: Gradual Diversification Success (Probability: 30%)

This scenario envisions successful Western investment in alternative supply chains achieving 40-50% supply independence by 2035. Key enabling factors include:

- Sustained government support for alternative supply development despite higher costs

- Technological breakthroughs that reduce processing complexity and environmental impact

- Effective coordination between allied nations in sharing development costs and risks

- Chinese acceptance of reduced market share in exchange for continued profitability

Under this scenario, global rare earth markets evolve toward bifurcated supply chains, with Chinese and Western systems operating in parallel. Higher cost structures in Western systems are offset by supply security benefits and strategic autonomy.

Scenario 3: Technology Breakthrough Disruption (Probability: 10%)

This low-probability scenario involves fundamental technological changes that reduce rare earth dependencies or enable entirely new production methods. Potential developments include:

- Alternative magnet technologies achieving cost and performance parity with rare earth magnets

- Synthetic rare earth production through advanced materials science or biotechnology

- Breakthrough recycling technologies that enable closed-loop material cycles

- Quantum materials research yielding superior alternatives to traditional rare earth applications

While unlikely in the near term, such breakthroughs could fundamentally alter leverage dynamics by reducing the strategic value of traditional rare earth supply chains.

The next major ASX story will hit our subscribers first

Investment and Policy Implications for Stakeholders

The strategic importance of rare earth supply chains creates investment opportunities and policy challenges across multiple stakeholder groups. Understanding these implications requires considering both defensive and offensive positioning strategies.

Government Strategic Responses

National security stockpiling programmes represent the most immediate policy response to supply chain vulnerabilities. Strategic reserves can provide short-term supply security during disruptions while alternative supply chains are developed.

Industrial policy coordination with allies offers opportunities to share development costs and reduce duplication of effort. Key initiatives include:

- US Critical Materials Institute: $200 million annual funding for rare earth research and development

- EU Raw Materials Alliance: 15-member coordination framework for supply chain resilience

- Japan-Australia critical minerals partnership: Joint development of processing capabilities in Australian locations

- Five Eyes critical minerals cooperation: Intelligence and policy coordination on supply chain vulnerabilities

Research funding for alternative technologies addresses long-term supply security by developing substitutes and improving recycling capabilities. Government investment can support basic research that private companies cannot justify economically.

Corporate Risk Management Strategies

Supply chain mapping and vulnerability assessment enable companies to understand their rare earth dependencies and develop appropriate risk mitigation strategies. This process often reveals indirect dependencies through suppliers that were previously unrecognised.

Long-term contract diversification requirements balance supply security against cost optimisation. Companies increasingly negotiate supply agreements that specify geographic diversification targets and alternative supplier qualifications.

Technology investment in efficiency improvements can reduce absolute rare earth requirements while maintaining performance. Design optimisation and material substitution research offer paths to reduce dependency without compromising product functionality. For instance, understanding critical dependence on minerals helps inform strategic decision-making processes.

Frequently Asked Questions

How quickly could China implement rare earth export restrictions?

China possesses administrative mechanisms that enable rare earth export restrictions within 30-60 days of policy decisions. The export licensing system already in place can be modified to restrict specific materials, grades, or end-use applications without requiring new legislation.

Historical precedent demonstrates China's willingness to use these tools rapidly. The 2010 dispute with Japan over territorial issues resulted in rare earth export restrictions implemented within weeks, causing immediate supply disruptions and price increases.

However, economic incentives favour selective rather than comprehensive restrictions. Complete export cutoffs would harm Chinese rare earth producers and downstream manufacturers, limiting the attractiveness of comprehensive bans except during severe geopolitical crises.

Which rare earth elements provide China with the greatest leverage potential?

Heavy rare earth elements, particularly dysprosium and terbium, provide China with maximum leverage potential due to 99% Chinese control of global processing capacity. These elements are essential for high-temperature magnet applications and cannot be substituted without significant performance compromises.

High-purity neodymium for defence applications represents another critical leverage point. Military specifications often require purity levels and consistency standards that only a few qualified suppliers can meet, creating concentrated dependencies.

Processed compounds versus raw ore concentrates create additional leverage opportunities. Even countries with domestic rare earth mining often depend on Chinese processing facilities to convert ore into usable materials, extending China's influence beyond raw material exports.

What would be the economic impact of a comprehensive rare earth supply disruption?

Economic modelling suggests that a comprehensive Chinese rare earth export restriction would create immediate price increases of 300-500% within six months, based on historical precedent and current market structure.

Production delays in affected industries would likely extend 12-18 months as companies exhaust existing inventories and struggle to secure alternative supplies. Electric vehicle and renewable energy sectors would face the most severe disruptions due to high rare earth content and limited substitution options.

GDP impact estimates for developed economies range from 0.1-0.3% in the first year, with larger effects possible if disruptions extended to defence and aerospace sectors. These estimates assume partial substitution and demand destruction rather than complete production cessation.

Strategic Materials Landscape Navigation

Key Takeaways for Decision Makers

China's rare earth supply chain leverage represents a genuine strategic vulnerability for Western economies, but this leverage operates within constraints that limit its application. Understanding these dynamics enables more effective policy and investment responses.

The leverage is real but time-limited as alternative supply chains develop. China's current dominance reflects decades of investment and policy support that created sustainable competitive advantages, but these advantages can be overcome with sufficient commitment and resources.

Strategic patience proves essential for effective diversification. Attempts to rapidly reduce rare earth dependencies through crash programmes are likely to fail due to technical complexity and capital requirements. Successful diversification requires sustained commitment over multiple economic cycles.

Coordination between allied nations remains essential for reducing vulnerabilities efficiently. The scale of investment required to build alternative supply chains exceeds what individual countries can justify economically, making multilateral approaches necessary for success.

Timeline for Reduced Dependency

The path toward reduced rare earth dependency follows predictable phases that reflect both technical constraints and economic realities:

2026-2028: Emergency Preparedness and Initial Capacity

- Strategic stockpiling programmes reach meaningful inventory levels

- Initial mining projects in Australia, United States, and Canada reach production

- Demonstration-scale recycling and processing facilities prove technical feasibility

- Research programmes identify promising substitution technologies for further development

2028-2032: Meaningful Alternative Supply Development

- Commercial-scale rare earth processing facilities begin operations outside China

- Recycling systems achieve economic viability for high-value applications

- Advanced magnet designs reduce rare earth requirements while maintaining performance

- Supply chain diversification reduces Chinese market share to 60-70% across key segments

2032-2035: Potential Strategic Independence Achievement

- Western supply chains achieve 40-50% independence from Chinese rare earth supplies

- Technology breakthroughs enable further substitution and efficiency improvements

- Competitive rare earth industries emerge in multiple geographic regions

- Chinese leverage becomes manageable rather than strategically threatening

This timeline assumes sustained political commitment and investment across multiple Western nations. Delays in funding, permitting, or technology development could extend these phases significantly, while breakthrough technologies or increased Chinese restrictions could accelerate alternative development.

Investment and policy decisions made in the next three years will largely determine whether this timeline can be achieved, making the current period critically important for establishing long-term supply chain resilience.

Disclaimer: This analysis contains forward-looking statements and scenarios based on current market conditions and policy trends. Actual developments in rare earth supply chains may differ materially from these projections due to technological, economic, or geopolitical factors not currently anticipated. This content is for informational purposes only and should not be considered investment or policy advice.

Looking to Navigate Strategic Resource Opportunities?

China's rare earth supply chain leverage creates immediate vulnerabilities but also generates compelling investment opportunities for savvy investors monitoring ASX-listed critical materials companies. Discovery Alert's proprietary Discovery IQ model instantly identifies significant mineral discoveries across strategic commodities, delivering real-time alerts that help investors capitalise on supply chain diversification trends and emerging Western alternatives to Chinese dominance. Start your 30-day free trial with Discovery Alert to gain immediate market advantage when the next critical materials breakthrough is announced.