May 22, 2026

The Invisible Metal at the Heart of American Defence

Few industrial transitions carry as much strategic weight as the slow disappearance of a country's refining capacity. Over three decades, the United States systematically shed its alumina processing infrastructure, driven out by lower-cost competition and shifting industrial economics. At the time, the loss appeared to be a straightforward manufacturing story. In retrospect, it was the quiet erasure of something far more consequential: the entire domestic foundation for gallium production.

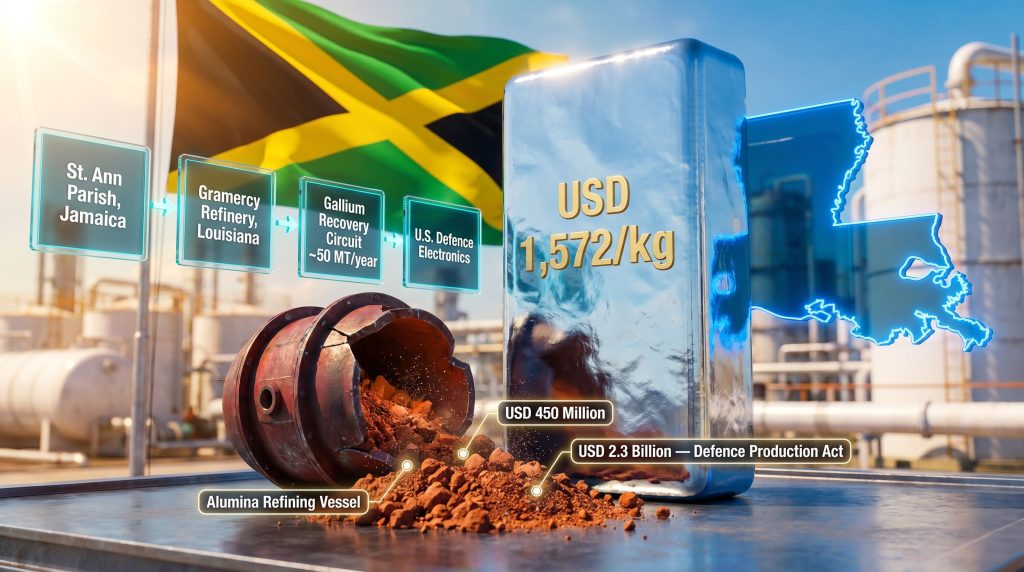

Today, as Washington scrambles to rebuild what was lost, the path to American gallium independence runs not through domestic geology, but through a Caribbean island. The US gallium strategy depends on Jamaica bauxite supply in ways that expose both the ambition and the structural fragility of the country's critical minerals recovery effort.

When big ASX news breaks, our subscribers know first

What Makes Gallium So Difficult to Replace

Gallium occupies an unusual position in the periodic table of strategic importance. Unlike lithium or cobalt, which can be directly mined from dedicated deposits, gallium has no primary ore of its own. It exists in trace concentrations within bauxite and zinc ores and only becomes recoverable during large-scale industrial refining, specifically through the Bayer process used to convert bauxite into alumina.

This byproduct nature creates a fundamental economic constraint: gallium production cannot simply be switched on through new mining projects. It requires active, high-volume alumina refining infrastructure operating at scale. Without that underlying industrial base, there is no gallium to recover, regardless of how critical the metal becomes or how high its price climbs.

The applications that drive gallium's semiconductor importance are concentrated in two compound families:

- Gallium arsenide (GaAs): Used in high-frequency radar systems, satellite communications arrays, and military-grade microwave electronics

- Gallium nitride (GaN): The material of choice for next-generation 5G base station semiconductors, power amplifiers, and advanced electronic warfare systems

More than 11,000 individual US defence components incorporate gallium-based materials, according to reporting from AL Circle. This figure reframes gallium not as an industrial curiosity but as a material embedded throughout the operational backbone of American military capability.

The Chemistry That Creates Strategic Dependency

Within the Bayer process, bauxite ore is dissolved in hot caustic soda to produce an aluminium hydroxide solution. Gallium, present at concentrations typically between 50 and 80 parts per million in bauxite, enters this liquor and can be extracted through a series of ion exchange or solvent extraction steps before final alumina precipitation.

The critical technical insight here is one that policymakers often overlook: gallium recovery efficiency depends heavily on the specific chemistry of the bauxite feedstock. High-silica bauxites create processing complications that reduce gallium recovery yields. Low-silica bauxites with high alumina availability, precisely the profile of Jamaican deposits, allow for cleaner refining chemistry and more efficient trace metal extraction. This is not a minor operational detail. It directly explains why bauxite supply importance means Jamaican bauxite is not interchangeable with other global sources from the perspective of gallium recovery planning.

How China Built an Unassailable Position

China's dominance over global gallium supply was not the result of unique geological endowment. Chinese bauxite reserves, while substantial, are not inherently superior to those found in Guinea, Australia, or Jamaica. What China built was an industrial system that combined massive alumina refining scale with deliberate investment in byproduct recovery circuits at a time when Western producers were exiting the sector entirely.

The timeline of that dominance, and its eventual weaponisation, charts a clear arc:

| Milestone | Year | Strategic Impact |

|---|---|---|

| US alumina refinery closures accelerate | 1990s to 2010s | Domestic gallium recovery capacity eliminated |

| China reaches approximately 98 to 99% of global low-purity gallium supply | Pre-2023 | US becomes fully import-dependent |

| China introduces gallium export licensing controls | August 2023 | Global supply tightens, prices begin rising |

| China bans gallium exports to the United States | December 2024 | Acute supply crisis confirmed |

| Gallium spot price reaches approximately USD 1,572 per kilogram | January 2026 | Price more than triples from pre-restriction levels |

The price trajectory warrants particular attention. A tripling of spot price within roughly two years signals not merely market tightness but a genuine structural supply dislocation. Markets had previously treated Chinese gallium dominance as a background condition rather than an active risk. The export ban converted that background condition into a foreground crisis.

Furthermore, as the critical minerals demand surge continues to intensify across defence and technology sectors, the consequences of this dislocation are likely to deepen before they ease.

China's gallium dominance was constructed through industrial economics, not geology. That distinction matters because it means other nations with sufficient refining infrastructure can theoretically replicate the model, but only if they are willing to make the long-term industrial investments that Western economies consistently deferred.

The Gramercy Refinery: America's Last Industrial Anchor

The Gramercy alumina refinery in Louisiana is, at this point, less an industrial facility than a national strategic asset. Commissioned in 1957 and currently supplying approximately 40% of remaining US alumina consumption, it represents the sole surviving thread connecting American manufacturing to domestically processed alumina. Every other refinery that once operated across the United States has closed.

The refinery's age introduces a layer of operational risk that any honest strategic assessment must acknowledge. Infrastructure designed and built in the late 1950s carries inherent maintenance demands and capital requirements that newer facilities do not face. The USD 450 million partnership announced by the US Department of Defence in January 2026 addresses this reality directly, combining operational continuity investment with the construction of a new gallium recovery circuit.

The financial structure of that partnership breaks down as follows:

- USD 150 million in preferred equity contributed directly by the Pentagon through the Atlantic Alumina Company (ATALCO) vehicle

- More than USD 300 million from Concord Resources, a subsidiary of Pinnacle Asset Management, which also holds a commercial stake in the Jamaican upstream supply chain

- Total commitment: USD 450 million, representing one of the largest single-facility critical minerals investments in US industrial history

The planned gallium recovery circuit is designed to produce approximately 50 metric tonnes annually, a volume that project proponents suggest could satisfy the entirety of current US domestic gallium demand. Whether that demand figure remains static as defence electronics requirements expand is a reasonable question for investors and policymakers to consider. In addition, Defense Production Act support has been instrumental in providing the federal framework that makes commitments of this scale possible.

The Rare Earth Dimension Adjacent to Gramercy

An often-overlooked feature of the Gramercy site is the accumulated legacy of decades of alumina refining: approximately 30 million tonnes of bauxite residue, commonly referred to as red mud, stored on the refinery grounds. This residue, a byproduct of the Bayer process, contains recoverable concentrations of rare earth elements and other strategic minerals that were not extracted during original refining operations.

A separate initiative by Element USA, backed by a USD 29.9 million Department of Defence grant, is planning to construct a rare earth processing facility adjacent to the Gramercy site specifically to extract value from this residue stockpile. The broader project has been valued at approximately USD 850 million, positioning the Gramercy complex as a potential multi-mineral strategic hub rather than a single-product facility.

This rare earth dimension adds a second layer of strategic rationale to preserving Gramercy's operational continuity, one that extends beyond gallium alone. Consequently, the site's importance to critical minerals for semiconductors and wider defence applications is increasingly difficult to overstate.

Jamaica's Central and Often Underestimated Role

The Gramercy refinery does not source bauxite from within the United States. Its entire feedstock supply flows from Jamaica, specifically from the Discovery Bauxite Partners joint venture operating in St. Ann parish on the island's northern coast. This single upstream dependency means that the US gallium strategy depends on Jamaica bauxite supply in the most direct and literal sense possible.

Jamaican bauxite carries a chemical profile that makes it particularly well-matched to the Bayer refining process used at Gramercy:

- Low silica content: Reduces scaling and processing complications within refining circuits

- Alumina availability exceeding 46%: Provides high extraction efficiency relative to many competing bauxite sources

- Established export infrastructure: The Discovery Bauxite Partners operation can export up to 5.2 million tonnes of bauxite annually

The ownership structure of that joint venture introduces an important geopolitical dimension that is frequently glossed over in US-centric coverage of the Gramercy deal:

| Stakeholder | Ownership | Role |

|---|---|---|

| Jamaica Bauxite Mining Limited (JBM) | 51% | State-controlled entity; majority partner |

| Concord Resources | 49% | Private commercial operator; also investor in Gramercy refinery |

The Jamaican government, through JBM, holds majority ownership of the upstream supply source that feeds the only refinery capable of producing domestic US gallium. This is not a passive commercial arrangement. It places Jamaica in the position of a sovereign node within the US defence industrial supply chain, a status that carries genuine economic and diplomatic weight. The Pentagon's strategic approach to this arrangement has attracted growing analytical attention precisely because of that asymmetry.

Jamaica's 51% majority stake in the upstream bauxite joint venture gives Kingston structural leverage over a supply chain that Washington has designated as critical to national security. The diplomatic implications of that asymmetry have likely not yet been fully priced into US-Jamaica bilateral relations.

Mapping the Complete Supply Chain

Understanding how Jamaican bauxite ultimately reaches US defence electronics requires tracing a multi-step industrial process:

- Bauxite is extracted at Discovery Bauxite Partners operations in St. Ann parish, Jamaica

- Bauxite is shipped to the Gramercy refinery in Louisiana

- The Bayer process converts bauxite into alumina, with gallium-bearing liquors separated during processing

- The planned gallium recovery circuit captures gallium from refinery liquors, producing approximately 50 metric tonnes of refined gallium annually

- Gallium is processed into gallium arsenide and gallium nitride compounds by downstream manufacturers

- Compounds are incorporated into radar systems, missile guidance electronics, satellite communications hardware, and 5G semiconductors used across US defence and commercial applications

Each step in this chain represents a potential failure point. The concentration of the entire sequence through a single refinery receiving feedstock from a single offshore source creates a risk profile that strategic planners should treat with considerable seriousness.

Scenario Analysis: Where the Strategy Can Fail

The USD 450 million investment represents a meaningful commitment, but it does not resolve the fundamental structural vulnerability of a supply chain built on sequential single points of failure. The following scenarios illustrate the key risk dimensions:

Scenario 1: Jamaican Supply Disruption

A major hurricane, infrastructure failure, or political instability affecting St. Ann parish operations could halt bauxite exports to Gramercy. Without feedstock, alumina production stops and the gallium circuit produces nothing. Jamaica sits within an active hurricane belt, making this scenario less hypothetical than it might appear.

Scenario 2: Gramercy Operational Failure

Infrastructure commissioned in 1957 carries inherent reliability risk. A sustained technical failure, regulatory shutdown, or financial difficulty at the sole US alumina refinery would collapse the entire domestic gallium plan with no backup facility available.

Scenario 3: Jamaican Geopolitical Recalibration

Jamaica's 51% state ownership in Discovery Bauxite Partners gives Kingston the structural ability to renegotiate supply terms, restrict export volumes, or redirect bauxite to competing buyers as strategic value becomes more explicit. Jamaica is a sovereign nation with its own economic interests, and those interests may not always align perfectly with Washington's supply chain priorities.

Scenario 4: Allied Nation Competition

As Australia, Canada, and European Union members accelerate their own critical minerals strategies, competition for high-quality bauxite feedstock and for downstream gallium recovery capacity could intensify. The US may find itself competing with allied nations for the same Caribbean supply sources.

The current US gallium strategy replaces dependence on an adversarial supplier with dependence on a friendly one. That represents a genuine geopolitical improvement. It does not, however, constitute supply chain resilience in any structural sense.

The next major ASX story will hit our subscribers first

The Wider US Critical Minerals Context

The Gramercy investment sits within a substantially larger federal effort to reshore critical mineral supply chains. Under the Defence Production Act, total US government direct investments in critical mineral projects have reached approximately USD 2.3 billion since 2025, signalling a deliberate shift from market reliance to state-directed industrial policy.

Gallium's position within the broader critical minerals landscape illustrates both the scope of the challenge and the unevenness of current US vulnerability:

| Mineral | Dominant Supplier | US Domestic Status | Primary Strategic Application |

|---|---|---|---|

| Gallium | China (~98 to 99%) | No production prior to 2026 plan | Defence electronics, 5G, semiconductors |

| Rare Earths | China (~60%+ of processing) | Limited domestic processing capacity | Magnets, defence systems, EV motors |

| Bauxite and Alumina | Australia, Guinea, Jamaica | One operating refinery (Gramercy) | Aluminium production, gallium feedstock |

| Lithium | Australia, Chile | Emerging domestic capacity | EV batteries, energy storage systems |

The gallium column stands out for the severity of its pre-2026 position. Complete import dependency combined with zero domestic production capacity and a single refinery capable of producing any domestic supply at all represents an extreme concentration of strategic risk in a single point of geopolitical exposure. However, America's mineral potential remains considerable, provided the policy frameworks to unlock it are sustained over the long term.

What Genuine Resilience Would Require

Industry analysts and defence planners who have studied critical mineral supply chain vulnerability consistently identify several conditions necessary for genuine supply resilience, none of which the current Gramercy-centred strategy fully satisfies:

- Geographic diversification of refining capacity: Multiple facilities in different regions reduce single-point failure risk

- Feedstock source diversification: Access to bauxite from multiple supply origins limits exposure to any single sovereign decision

- Downstream processing redundancy: Multiple gallium compound manufacturers reduce concentration risk within the production-to-application chain

- Strategic stockpiling: Maintaining national gallium reserves capable of sustaining defence production for a defined period provides a buffer against supply disruptions

The current plan addresses the first requirement partially, through Gramercy alone, while leaving the remaining three largely unaddressed. Whether subsequent phases of the US critical minerals strategy extend beyond Gramercy to build distributed refining capacity will be a defining test of whether the policy represents a structural solution or a tactical response.

Jamaica's Elevated Strategic Profile

For Jamaica, the implications of this arrangement extend well beyond the economics of bauxite export pricing. The island has effectively been elevated from commodity supplier to strategic supply chain partner in a US defence industrial programme of national significance.

The potential economic implications for Jamaica are substantial:

- Greater long-term demand certainty for bauxite exports as US gallium production plans create a durable off-take requirement

- Strengthened negotiating position on pricing as the strategic value of Jamaican bauxite's specific chemical profile becomes more widely understood

- Potential to attract additional downstream investment given the island's elevated geopolitical profile within critical mineral supply chain discussions

The geopolitical considerations are more complex. Deeper integration into US defence industrial supply chains may constrain Jamaica's diplomatic flexibility with other major powers that have competing interests in Caribbean resource access. The island's bauxite resources, long treated primarily as an economic asset, have acquired a geopolitical character that will increasingly shape how external powers engage with Kingston.

Frequently Asked Questions

Why can gallium not simply be mined directly?

Gallium has no primary ore deposits of economic significance. It occurs only in trace concentrations within bauxite and zinc ores, at levels typically between 50 and 80 parts per million. Economically viable gallium recovery requires processing these ores at large industrial scale, making the metal an inherent byproduct of aluminium or zinc refining rather than a standalone mining product.

What volume of gallium does the Gramercy circuit plan to produce?

The planned gallium recovery circuit at Gramercy is designed to produce approximately 50 metric tonnes annually, a figure that project proponents describe as sufficient to meet current total US domestic demand.

What makes Jamaican bauxite specifically suited to Gramercy?

Jamaican bauxite's low silica content and alumina availability above 46% create refining conditions well-matched to Bayer process operations. The Gramercy refinery was effectively designed around this feedstock profile, making substitution with other bauxite sources a technically complex and potentially costly adjustment.

How significant is the price increase in gallium since China's export restrictions?

Gallium prices reached approximately USD 1,572 per kilogram by January 2026, representing an increase of more than three times compared to levels prevailing before China's progressive export restrictions, which began in August 2023 and escalated to a full US export ban in December 2024.

Does the US have any backup if the Gramercy refinery fails?

Currently, no. Gramercy is the only operating alumina refinery in the United States. If it were to cease operations for any reason, the US would have no domestic pathway for alumina production or gallium recovery, reverting entirely to import dependency.

This article is intended for informational and educational purposes only. It does not constitute financial, investment, or strategic advice. Forecasts, scenario analyses, and price projections referenced herein involve inherent uncertainty and should not be relied upon as predictive of future outcomes. Readers should conduct independent research and consult qualified advisers before making any investment or policy decisions.

Want to Track the Next Major Critical Minerals Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across gallium, rare earths, and more than 30 other commodities — explore historic examples of what major discoveries can return and begin your 14-day free trial at Discovery Alert to gain an actionable market edge ahead of the broader investment community.