June 4, 2026

Understanding China's Strategic Materials Dominance

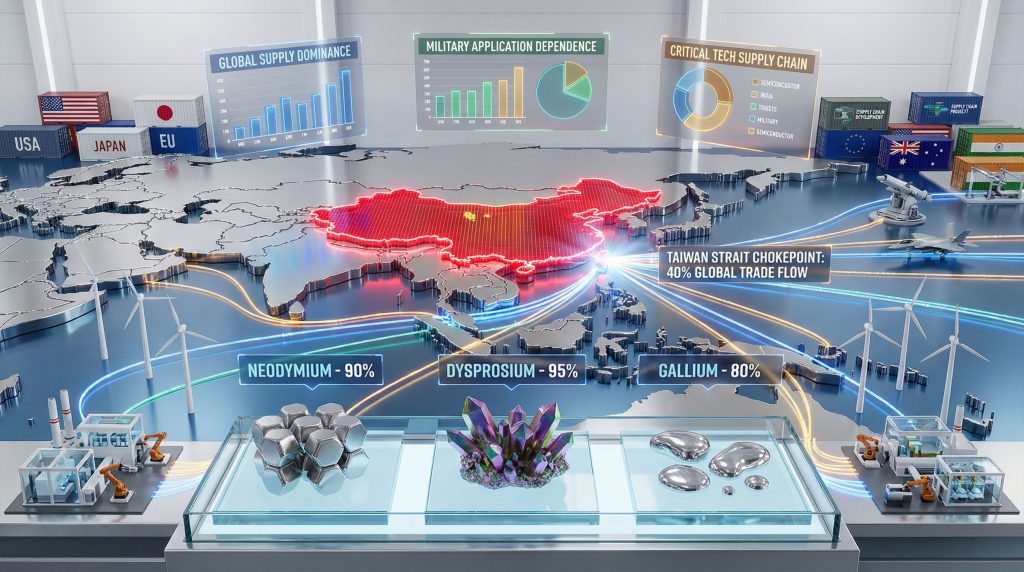

The architecture of modern technological supremacy rests upon a foundation of rare earth elements, where market concentration has created unprecedented strategic leverage. China's export controls extend across the entire value chain, from extraction through final product manufacturing, establishing what analysts describe as a materials hegemony unprecedented in modern industrial history.

The Mathematics of Market Control

China's grip on rare earth supply chains transcends simple mining statistics. The nation commands 90% of global neodymium refining capacity and 95% of dysprosium production, while maintaining 80% control over gallium supply with only Japan and Germany offering limited alternatives. This vertical integration from raw materials to finished magnets amplifies China's leverage exponentially, creating single points of failure across multiple industries simultaneously.

Furthermore, the trace control policy represents perhaps the most sophisticated supply chain weapon ever deployed. This mechanism allows China to restrict exports of any product containing even minimal Chinese-origin rare earths, creating cascading impacts across global manufacturing networks. Companies discovering Chinese materials in their supply chains can face retroactive compliance requirements, effectively weaponizing regulatory mechanisms against international competitors.

| Element | Chinese Market Share | Military Applications | Supply Alternatives |

|---|---|---|---|

| Neodymium | 90% | Guidance systems, motors | Limited processing outside China |

| Dysprosium | 95% | High-temperature magnets | Virtually no alternatives |

| Gallium | 80% | Semiconductor substrates | Japan, Germany (limited capacity) |

| Terbium | 94% | Precision electronics | Australia (emerging) |

| Samarium | 85% | Missile guidance | U.S. stockpiles only |

Critical Elements at Risk

The strategic implications of this concentration become clear when examining military applications. Hypersonic weapons systems require dysprosium for high-temperature magnet operations, while precision-guided munitions depend on neodymium-iron-boron magnets for guidance systems. Gallium arsenide semiconductors, essential for radar and communications equipment, face similar dependencies.

Export licensing mechanisms function as geopolitical tools rather than trade regulations. China can delay permits for months, impose technology transfer requirements, or enforce compliance standards retroactively, creating uncertainty that disrupts long-term planning across entire industries. This approach demonstrates how the critical minerals energy transition has become a strategic battleground.

When big ASX news breaks, our subscribers know first

What Are the Primary Supply Chain Vulnerability Points?

The rare earth supply chain in a Taiwan conflict scenario reveals vulnerabilities that extend beyond direct material sources. Physical infrastructure, regulatory frameworks, and financial systems create multiple points where disruption can cascade through global networks.

Physical Infrastructure Chokepoints

Taiwan Strait shipping lanes carry 40% of global trade, including critical rare earth intermediates essential for semiconductor fabrication. The ports of Kaohsiung and Keelung handle specialised materials that require temperature-controlled transport and precise timing for manufacturing processes.

Semiconductor fabrication facilities operate on just-in-time principles, maintaining minimal inventory to preserve material quality and reduce costs. Any disruption lasting more than 30 days could force production shutdowns across multiple continents, affecting everything from automotive manufacturing to defence systems.

Licensing and Regulatory Weaponisation

China's trace control policy creates a regulatory web where any product containing Chinese-origin materials becomes subject to export restrictions, regardless of where final assembly occurs.

The sophistication of these mechanisms extends beyond simple export controls. Companies face:

- Retroactive compliance audits requiring documentation of material origins dating back years

- Technology transfer mandates as conditions for continued access to materials

- Financial penalties for non-compliance with evolving regulatory standards

- Supply chain transparency requirements that expose competitive intelligence

How Resilient Are Current Taiwan Semiconductor Supply Buffers?

Taiwan's semiconductor industry has developed sophisticated risk management strategies, yet fundamental dependencies on Chinese-processed materials remain largely unaddressed. The resilience of current buffers depends critically on conflict duration and scope.

Inventory Analysis and Strategic Reserves

TSMC maintains 12-24 month inventories of critical materials, representing one of the most robust buffer systems in global manufacturing. However, this stockpile assumes normal consumption patterns and does not account for accelerated military production demands that could emerge during conflict.

The company has diversified sourcing through European and Japanese intermediaries, yet these suppliers ultimately depend on Chinese-refined feedstock for their operations. This creates an illusion of supply chain independence while maintaining structural dependence on Chinese processing capabilities.

Alternative Sourcing Pathways

Current mitigation strategies include:

- European rare earth processing facilities with combined capacity representing less than 5% of global needs

- U.S. Defense Production Act stockpiling targeting 6-month military consumption requirements

- Australian mining partnerships for upstream security, though processing remains limited

- Recycling programmes for magnet recovery achieving 15% material recovery rates

The timeline for alternative sourcing remains problematic. New refining facilities require 3-5 years for construction and $200-500 million in capital investment, while mining operations demand 5-10 years and $500 million to $2 billion per project.

What Military Technologies Face the Greatest Supply Risk?

Modern warfare increasingly depends on materials-intensive technologies where rare earth elements enable capabilities that conventional materials cannot achieve. The military applications most vulnerable to supply disruption represent the cutting edge of contemporary defence systems.

Hypersonic Systems and Precision Munitions

Hypersonic weapons rely on neodymium-iron-boron magnets for guidance systems and dysprosium for high-temperature motor applications. These materials enable the precision and speed that define next-generation weapons systems, yet both elements face 90%+ Chinese supply concentration.

Precision-guided munitions require consistent magnet performance across extreme temperature and stress conditions. Alternative magnetic materials exist but sacrifice 20-40% performance, reducing accuracy and range significantly.

Naval and Aerospace Platform Dependencies

Scenario A: 30-day supply disruption

- Immediate impact on guidance system production

- 15% reduction in precision munitions manufacturing

- Rationing of critical components to priority programmes

Scenario B: 6-month sustained embargo

- Complete halt of new hypersonic system production

- 60% reduction in submarine motor manufacturing

- Emergency activation of strategic material reserves

Scenario C: Complete decoupling timeline

- 3-7 years for alternative supply chain development

- $50-100 billion investment requirement

- Performance compromises in interim systems

Gallium arsenide semiconductors essential for radar and communications face similar risks, with 80% Chinese control threatening the electronics backbone of modern military systems.

Which Economic Sectors Would Experience Cascading Effects?

The rare earth supply chain in a Taiwan conflict extends beyond military applications into civilian sectors that underpin economic stability. The interconnected nature of modern manufacturing means disruptions cascade through multiple industries simultaneously.

Automotive Industry Transformation

Electric vehicle production faces immediate bottlenecks from magnet shortages, with permanent magnet motors requiring 1-2 kilograms of rare earths per vehicle. The transition to electric transportation, already challenging existing supply chains, would face severe constraints in a conflict scenario.

Battery chemistry alternatives would accelerate out of necessity rather than optimisation, potentially setting back performance standards and increasing costs. Supply chain regionalisation imperatives would force automakers to abandon just-in-time manufacturing principles that have defined industry efficiency for decades.

Renewable Energy Infrastructure

Wind turbine generators represent one of the largest consumers of rare earth magnets outside military applications. A single 3-megawatt wind turbine requires approximately 600 kilograms of rare earth materials, primarily neodymium and dysprosium.

Solar panel inverter systems depend on gallium-based semiconductors for power conversion efficiency. Alternative materials exist but reduce conversion efficiency by 15-25%, increasing system costs and reducing renewable energy competitiveness.

Consequently, grid storage systems face component constraints affecting both battery technologies and power management systems, potentially slowing the transition to renewable energy infrastructure precisely when energy security becomes most critical.

How Are Allied Nations Preparing for Supply Chain Disruption?

International coordination efforts recognise that rare earth supply security requires multilateral approaches extending beyond traditional military alliances. The response frameworks emerging reveal both the scale of the challenge and the complexity of solutions.

United States Strategic Response Framework

The U.S. approach combines emergency preparedness with long-term industrial development:

- Defense Production Act rare earth facility funding totalling $3.4 billion allocated in 2024-2025

- Critical Materials Security Program expansion targeting 30% supply diversification by 2030

- Allied partnership agreements for supply diversification with Australia, Japan, and EU partners

- Emergency stockpile target increases to 18-month military consumption requirements

- Domestic processing capability development through public-private partnerships

European Union and Japan Coordination Mechanisms

The European CRM facility mandates that 10% of annual consumption come from recycling by 2030, while requiring diversified sourcing for strategic materials. Japan-Australia partnerships focus on upstream mining development, with Japanese technology enabling Australian resource development.

Quad alliance supply chain resilience initiatives include India-Australia collaboration on rare earth processing, leveraging India's chemical expertise and Australia's mineral resources. These partnerships aim to create alternative processing networks outside Chinese influence, particularly as the US-China trade war impact continues to reshape global supply chains.

The next major ASX story will hit our subscribers first

What Investment Opportunities Emerge from Supply Chain Restructuring?

The restructuring of rare earth supply chains creates investment opportunities across multiple sectors, from traditional mining and processing to innovative recycling technologies and material substitution research.

Mining and Processing Infrastructure Development

Non-Chinese rare earth mining projects face $500 million to $2 billion capital requirements with 5-10 year development timelines. However, these projects benefit from strategic government support and long-term supply contracts that reduce traditional mining investment risks.

Processing facility construction in allied nations represents a $200-500 million investment opportunity per facility, with 3-5 year construction timelines. The technical expertise gap creates opportunities for companies with separation and refining capabilities. Similarly, Australia's critical minerals reserve initiatives are creating substantial investment potential.

Technology Substitution and Efficiency Gains

Companies developing rare earth-free alternatives or improving material utilisation efficiency represent significant value creation opportunities as supply constraints drive innovation demand.

Iron-nitride permanent magnets offer potential alternatives to rare earth magnets in some applications, though performance remains 15-20% below neodymium-iron-boron systems. Recycling technology development achieves 85% material recovery rates in laboratory conditions, with commercial scaling representing major market opportunities.

Magnet efficiency improvements through better design and manufacturing processes can reduce rare earth consumption by 30-40% while maintaining performance, creating substantial cost savings and supply security benefits.

How Long Would Supply Chain Reconstruction Take?

The timeline for reconstructing rare earth supply chains independent of Chinese processing reveals the long-term nature of supply security challenges. Multiple parallel development tracks are required to achieve meaningful supply diversification.

Timeline Analysis for Alternative Infrastructure

| Infrastructure Type | Development Timeline | Capital Requirements | Technical Challenges |

|---|---|---|---|

| Mining Operations | 5-10 years | $500M-2B per project | Environmental permitting |

| Refining Facilities | 3-5 years | $200M-500M | Technical expertise gaps |

| Magnet Production | 2-3 years | $50M-200M | Quality control systems |

| Recycling Systems | 1-3 years | $10M-50M | Collection infrastructure |

| R&D Programmes | 5-15 years | $100M-1B | Scientific uncertainties |

Interim Mitigation Strategies

While long-term supply chains develop, interim strategies become critical for maintaining operational capabilities:

- Strategic reserve deployment protocols activating government stockpiles during supply disruptions

- Rationing systems for critical applications prioritising military and essential infrastructure needs

- Temporary substitution material acceptance allowing performance compromises for supply security

- International sharing agreements among allied nations for emergency resource allocation

Furthermore, technical expertise transfer programmes represent a critical bottleneck, as rare earth processing requires specialised knowledge that takes years to develop. Training programmes and international exchanges become essential for building processing capabilities outside China.

What Lessons Can Be Drawn from Historical Supply Disruptions?

Historical analysis of supply chain disruptions reveals patterns that inform current rare earth vulnerability assessments. The scale and duration of impacts provide frameworks for understanding potential Taiwan conflict scenarios.

Comparative Analysis with Previous Crises

The 2010 China-Japan rare earth embargo provides the most relevant precedent, with rare earth prices spiking 600% within six months. Japan's response included emergency stockpiling, alternative supplier development, and material efficiency improvements that reduced rare earth consumption by 30% over five years.

COVID-19 semiconductor shortages demonstrate how supply chain disruptions cascade through interconnected industries. Automotive production faced months-long shutdowns, while consumer electronics saw price increases of 15-25% that persisted for over two years.

However, oil embargo supply chain adaptation models from the 1970s show that strategic reserves can buffer short-term disruptions effectively, but adaptation to long-term supply changes requires fundamental industrial restructuring taking 5-10 years for completion.

Resilience Building Best Practices

Successful supply chain resilience requires redundancy, diversification, and strategic reserves, but the timeline for implementation often exceeds the duration of acute geopolitical crises.

Best practices from historical disruptions include:

- Multi-source supply strategies reducing dependency on single suppliers or regions

- Strategic inventory buffers sized for 6-18 month consumption periods

- Alternative material development programmes initiated before supply crises occur

- International cooperation frameworks established during stable periods

- Rapid response protocols for emergency resource allocation and rationing

The U.S. COVID-19 response through Defense Production Act activation demonstrates how government intervention can accelerate private sector adaptation, though effectiveness depends on existing industrial capacity and technical expertise. These dynamics mirror broader patterns described in conflict drones rare earths supply chain analysis.

Preparing for an Uncertain Geopolitical Future

The analysis of rare earth supply chain in a Taiwan conflict scenarios reveals the intersection of materials science, geopolitics, and economic security. The concentration of processing capabilities creates systemic risks that extend far beyond traditional military considerations.

Strategic Imperatives for Stakeholders

Immediate actions required include:

- Comprehensive supply chain auditing to identify Chinese material dependencies at all levels

- Inventory buffer expansion targeting 12-18 month consumption requirements

- Alternative supplier qualification programmes accepting performance compromises for security benefits

- Investment in recycling infrastructure to create domestic material sources

Long-term development priorities encompass:

- Domestic processing capability development through public-private partnerships

- Technology innovation programmes targeting material substitution and efficiency improvements

- International cooperation frameworks for supply chain diversification

- Educational programmes developing technical expertise in rare earth processing

Policy Coordination Requirements

Effective response to rare earth supply vulnerabilities requires coordination across multiple levels of government and international partnerships. Emergency response protocols must include standardised procedures for strategic reserve activation, supply rationing, and international resource sharing.

Investment incentive alignment between allied nations prevents competitive bidding for limited resources while encouraging collaborative development of alternative supply chains. The EU-U.S. Trade and Technology Council's critical materials working group represents one model for this coordination.

In addition, regulatory frameworks must balance environmental protection with supply security imperatives, potentially requiring expedited permitting processes for strategic material projects during crisis periods. These considerations are increasingly relevant as detailed in China's mineral dominance analysis.

The rare earth supply chain in a Taiwan conflict scenario illustrates how modern economies have created dependencies that transcend traditional security considerations. Material control has become a form of geopolitical leverage comparable to traditional military power, requiring new frameworks for understanding and managing international risks.

Disclaimer: This analysis is based on publicly available information and should not be considered as investment advice or definitive predictions of future events. Geopolitical scenarios involve numerous uncertainties, and actual outcomes may differ significantly from theoretical assessments.

Want to Capitalise on Critical Minerals Market Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant critical minerals discoveries across the ASX, transforming complex geological announcements into actionable investment insights. With China's rare earth dominance creating unprecedented supply chain risks, understanding historic mineral discovery returns becomes essential for positioning ahead of market shifts in the critical materials sector.