June 13, 2026

The Financial Trap That Explains Everything About Chinese Gold Demand

Throughout modern economic history, periods of capital immobility have reliably produced the same outcome: savers deprived of meaningful alternatives converge on hard assets. The Roman denarius, the Weimar mark, post-Plaza Accord Japan, and now the managed financial architecture of contemporary China all demonstrate the same principle. When the pathways to wealth preservation are narrowed by design, gold fills the vacuum.

Understanding why Chinese citizens are buying gold at historically elevated rates requires more than a surface-level look at commodity markets. It demands an examination of the structural constraints that define everyday financial life inside China, where capital controls, near-zero deposit returns, a collapsing property sector, and a distrusted equity market have systematically eliminated every conventional alternative.

When big ASX news breaks, our subscribers know first

A Closed Financial System With No Exit Valve

China's financial architecture is fundamentally different from that of open economies. While investors in the United States, Europe, or Australia can freely allocate capital across global asset classes, the Chinese household saver operates within a tightly bounded system. The mechanisms of control are both institutional and administrative.

The People's Bank of China (PBoC) does not operate primarily through market-based signalling the way the U.S. Federal Reserve does. Rather than nudging behaviour through interest rate guidance and open market operations, the PBoC functions through direct lending mandates, administrative guidance to state-owned banks, and explicit exchange rate management. This distinction matters enormously for understanding the investment environment ordinary Chinese citizens face.

The currency architecture compounds this constraint. China operates a dual-currency system:

- The onshore yuan (CNY), which is tightly managed, capitally controlled, and cannot be freely exchanged into foreign currencies or deployed into offshore assets.

- The offshore yuan (CNH), traded in international markets primarily through Hong Kong, which moves within a defined band and remains indirectly shaped by Beijing's domestic policy choices.

This separation is not accidental. It allows Beijing to participate in global trade while retaining complete control over domestic capital flows. For the average Chinese saver, it means that moving money abroad, whether into foreign equities, foreign real estate, or foreign currencies, is simply not a realistic option. The capital controls are not theoretical. They are enforced and consequential.

With offshore diversification blocked, Chinese savers are left evaluating a very short list of domestic options, all of which carry serious structural problems.

Financial Repression: What Is It and How Does It Work Inside China?

The concept of financial repression is central to understanding why Chinese citizens are buying gold, yet it remains poorly understood outside specialist circles.

Financial repression describes a policy environment in which governments use a combination of mechanisms to suppress real returns on savings, trap capital within domestic systems, and gradually erode purchasing power through inflation. The tools vary by context, but the outcome is consistent: ordinary savers are unable to protect the real value of their money through conventional means.

| Mechanism | How It Operates | Effect on Savers |

|---|---|---|

| Interest rate suppression | Bank deposit rates held below inflation | Savings lose real purchasing power |

| Capital controls | Restrictions on moving money abroad | No access to higher-yielding foreign assets |

| Currency management | Exchange rate fixed within narrow bands | Reduced diversification options |

| State-directed lending | Credit channelled to government priorities | Market returns distorted; private sector starved |

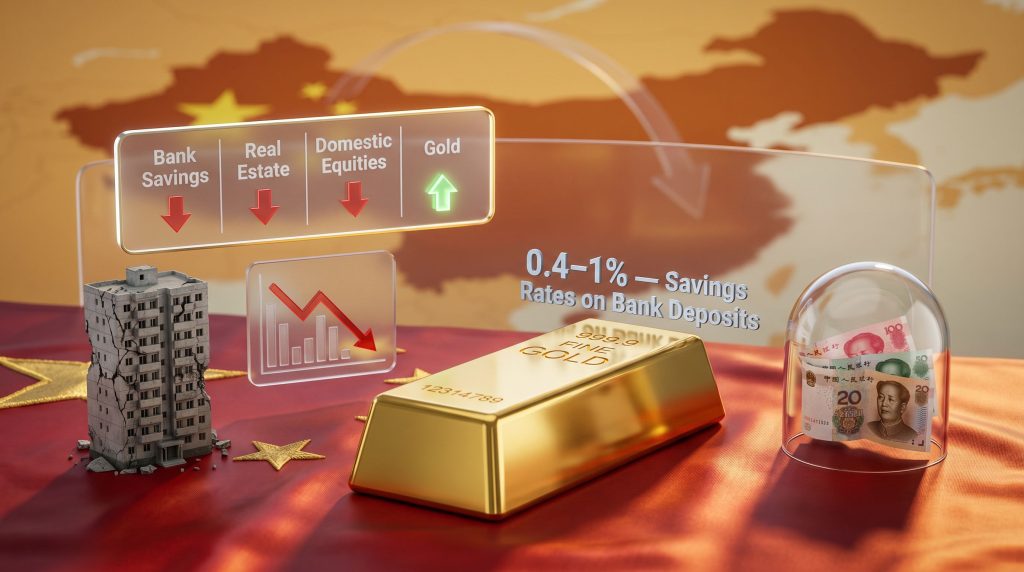

Inside China, this framework has real, quantifiable consequences. Standard savings deposit rates at Chinese commercial banks currently sit around 0.4% to 1%, well below any meaningful inflation-adjusted return. For context, academic economists who study political economy and monetary systems have noted that Chinese citizens trying to preserve wealth through bank savings are essentially locked into a guaranteed real loss over time, particularly during periods of even modest price inflation.

This is not a new phenomenon. The United States experienced its own version of financial repression during the 1970s, when regulatory caps on savings account interest rates held returns well below inflation, ultimately driving capital offshore into Eurobond markets and Latin American debt instruments. However, the difference is that China's repression is more comprehensive, longer-running, and reinforced by capital controls that prevent the kind of capital flight that eventually forced liberalisation in the U.S.

Why Chinese Real Estate Stopped Being a Safe Haven

For roughly two decades, residential property was the default wealth-building instrument for Chinese households. Local governments, which historically funded public services through land sales to developers, had structural incentives to keep property prices elevated. Developers needed buyers. Buyers needed the belief that prices would continue rising. The system fed itself.

That model has now broken down in ways that appear structural rather than cyclical.

The comparison most frequently drawn by political economists who study China's fiscal architecture is to Japan following the Plaza Accords of the mid-1980s. Under pressure from Washington to revalue the yen upward, Japan's export-driven economy redirected an enormous volume of capital into domestic real estate, inflating a debt-fuelled bubble that burst spectacularly in the early 1990s. This initiated what became known as the lost decades, a prolonged period of deflation, stagnant growth, and economic stagnation from which Japan has never fully recovered.

China's property correction is more likely to follow the Japan trajectory than the U.S. 2008 experience. Rather than a sharp Lehman-style collapse, the more probable outcome is a long, slow deflation that weighs on household wealth for decades. The Chinese government has both the tools and the political motivation to prevent a sudden crash, but it cannot manufacture genuine demand in oversupplied markets.

Several structural factors distinguish China's property crisis:

- Local government fiscal dependency on land sales created a systemic incentive to inflate property values well beyond sustainable demand.

- Major developer insolvencies exposed the fragility of a model built on pre-sales, leverage, and perpetual price appreciation.

- Ghost city inventory, real estate built in low-demand inland regions primarily to generate local government revenue, represents stranded capital with limited recovery prospects.

- The Chinese government lacks the external currency pressure that forced Japan's revaluation, meaning the deflation may be slower but no less persistent.

For ordinary Chinese households, the practical implication is clear: property is no longer a reliable store of value, and the expectation of price appreciation that justified illiquidity and high entry costs has evaporated.

The Chinese Stock Market's Trust Deficit

If property represents the slow-motion failure, the domestic equity market represents a more acute psychological wound.

Chinese domestic stock markets have consistently underdelivered as wealth-building vehicles for retail investors. The structural reasons are well-documented:

- Weak corporate governance standards, with financial disclosure requirements significantly less rigorous than in developed market equivalents.

- Limited investor protections, with regulatory frameworks that have repeatedly failed to identify or contain speculative excess before damage was done.

- State intervention risk, where policy changes can fundamentally alter asset values without warning, creating unpredictable environments for private investors.

- History of speculative bubbles, most notably the 2015 equity market collapse.

The 2015 episode deserves particular attention. Chinese indices fell more than 30% within weeks, erasing savings accumulated by millions of retail participants. Subsequent investigations revealed widespread corporate malfeasance that had been obscured by opaque reporting standards. The combination of governance failure, regulatory inadequacy, and the loss of actual savings produced a lasting and rational distrust of domestic equities among ordinary Chinese investors.

Foreign institutional participation in Chinese domestic equity markets remains significantly lower than in comparable emerging market contexts, a direct reflection of the same transparency and governance concerns that have burned retail participants at home.

Gold as the Rational Default: A Process of Elimination

When each alternative is evaluated honestly, gold emerges not as a speculative bet but as the logical conclusion of a process of elimination.

| Asset Class | Core Problem for Chinese Savers | Gold's Advantage |

|---|---|---|

| Bank deposits | 0.4–1% return; real value erodes | Preserves purchasing power over time |

| Residential property | Structural deflation; illiquidity | Highly liquid; globally fungible |

| Domestic equities | Governance opacity; volatility; burned investors | No counterparty risk |

| Offshore investment | Blocked by capital controls | Physically holdable domestically |

| Foreign currency | Restricted by yuan management | Universally recognised; outside CNY system |

The financial logic is reinforced by cultural foundations that operate independently of short-term economic conditions. Gold has carried centuries of meaning in Chinese society as a symbol of prosperity, security, and social continuity. Furthermore, wedding traditions, Lunar New Year gifting, and intergenerational wealth transfer practices all generate baseline demand for gold that persists even when financial motivations are absent. The preference for tangible, physically held assets over paper financial instruments, reinforced by repeated institutional failures, makes gold culturally and financially compelling simultaneously. China's gold market dominance reflects just how deeply embedded these dynamics have become.

The next major ASX story will hit our subscribers first

How Sovereign Gold Buying Amplifies Private Demand

China's gold accumulation story operates on two parallel tracks: private household demand and sovereign reserve building by the PBoC. While the motivations differ, they interact in ways that reinforce each other.

The PBoC's strategic rationale for gold accumulation became significantly clearer following the freezing of Russian sovereign assets held within Western financial infrastructure after 2022. This event sent a consequential signal to reserve managers globally: assets held within U.S.-aligned financial systems carry political risk that is not captured in any conventional risk model. Gold, by contrast, operates entirely outside this framework. It cannot be frozen, sanctioned, or devalued by a foreign government's policy decision.

For Beijing, which maintains substantial dollar-denominated reserve holdings while simultaneously seeking to reduce systemic exposure to Washington's financial architecture, central bank gold reserves represent a reserve asset with unique properties: immediately fungible, highly liquid, politically neutral, and immune to the kind of asset-freeze risk that the Russian precedent demonstrated.

This sovereign accumulation creates a confidence multiplier effect for private Chinese savers:

- The PBoC buys gold at scale, signalling institutional conviction in the asset class.

- State media coverage of central bank gold buying increases public awareness and legitimacy.

- Retail demand rises, further supporting domestic gold prices.

- Rising prices validate the original decision, creating additional demand momentum.

According to analysts at International Banker, China's accumulation strategy is far more deliberate and multi-layered than many Western commentators acknowledge.

Why a Gold-Backed Yuan Is More Theory Than Reality

Within gold investment communities, speculation about a gold-backed yuan has circulated for years. The argument typically holds that China's accumulation programme is preparation for a currency architecture shift that would displace the U.S. dollar. The evidence, however, points in a different direction.

A formal gold standard requires the issuing government to redeem currency for gold on demand, a convertibility discipline that would fundamentally compromise the PBoC's ability to manage monetary conditions administratively. China's entire economic development model depends on maintaining a competitive, effectively undervalued currency to support export manufacturing. A gold-backed yuan would almost certainly appreciate sharply, undermining the export competitiveness that remains central to economic growth and, by extension, the political legitimacy of the CCP.

Furthermore, the CCP's political survival depends on delivering continued prosperity. Restricting monetary flexibility through gold convertibility introduces the kind of economic rigidity that could destabilise growth during downturns, precisely the scenario Beijing is most motivated to avoid. Critically, Chinese authorities have provided no policy signals of any kind suggesting movement toward gold convertibility.

The accumulation of gold by the PBoC is most accurately understood as strategic reserve diversification and systemic risk reduction, not as preparation for a monetary architecture shift. These are fundamentally different things, and conflating them misrepresents both China's strategic motivations and gold in the monetary system.

Structural Scenarios That Could Intensify Chinese Gold Demand

Several plausible developments could accelerate already-elevated Chinese demand for gold in the years ahead:

- Further yuan depreciation pressure, which would increase the appeal of a non-currency store of value.

- Continued property market deterioration, eliminating the last major competing domestic asset class for household wealth.

- Escalating geopolitical tensions, raising the perceived risk of exposure to any asset class connected to international financial infrastructure.

- Additional sovereign asset freezing events globally, reinforcing gold's unique properties as an asset that exists outside any single jurisdiction's control.

- Tightening of capital controls, which would further reduce available alternatives and concentrate domestic savings into accessible hard assets.

What is notable about this list is that most of these scenarios are continuations of trends already underway rather than speculative ruptures. The structural case for Chinese gold demand does not require a crisis. It requires only the persistence of the conditions that already exist.

What China's Gold Demand Means for Global Markets

China and India together account for over half of global consumer gold demand in most years. Within that combined figure, Chinese private demand has demonstrated a consistently counter-cyclical relationship with Western investment flows, rising precisely when domestic financial conditions deteriorate rather than when global risk appetite is elevated. This counter-cyclicality makes Chinese gold demand a stabilising and structural force in global precious metals markets rather than a speculative one.

The central bank demand adds a sovereign demand floor that is largely insensitive to short-term price movements, providing additional support beneath market pricing that operates independently of the sentiment-driven flows that dominate Western gold investment.

For investors monitoring the gold market globally, China's demand profile represents something qualitatively different from the typical investment thesis. It is not driven by inflation expectations, interest rate differentials, or portfolio allocation theory in any conventional sense. Instead, it is driven by the systematic elimination of alternatives inside a managed financial system, reinforced by cultural affinity for physical assets and amplified by sovereign accumulation that signals institutional confidence at the highest level.

As Bloomberg's analysis of Chinese consumer gold trends illustrates, this demand pattern reflects deep-rooted economic and cultural motivations that are likely to persist well into the future.

That combination — structural necessity, cultural demand, and sovereign validation — is not a short-term trade. It is a durable feature of global precious metals markets that shows no signs of reversing.

Disclaimer: This article is intended for informational and educational purposes only. It does not constitute financial, investment, or legal advice. References to historical data, economic trends, and market conditions involve analysis that may not reflect future outcomes. Readers should conduct their own research and consult qualified professionals before making any investment decisions.

Want to Stay Ahead of Major Mineral Discoveries Driving Gold Market Movements?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly transforming complex mineral data into actionable investment insights for both new and experienced investors — explore the historic returns major discoveries have generated and begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.