July 21, 2026

When Western Miners Retreat, Who Steps In?

Throughout modern mining history, the withdrawal of one dominant capital bloc from a resource-rich region has rarely left a vacuum for long. Capital flows toward geology, and West Africa's geology is among the most compelling on the planet. What is unfolding across Ghana, Côte d'Ivoire, Guinea, and their neighbours in 2026 is less a sudden shift than the acceleration of a trend years in the making: a Chinese miner hunts West Africa gold assets that Western companies are choosing, or being forced, to abandon.

Understanding why this transfer is happening, who benefits, what risks are embedded in the process, and what it means for the long-term ownership of one of the world's most productive gold regions requires looking beyond individual transactions and examining the structural forces reshaping the entire sector.

Disclaimer: This article contains forward-looking statements, production forecasts, and transaction details sourced from publicly available reporting. These should not be construed as financial advice. Investors should conduct independent due diligence before making any investment decisions.

When big ASX news breaks, our subscribers know first

West Africa's Gold Belt: Why Every Major Mining Power Wants a Piece

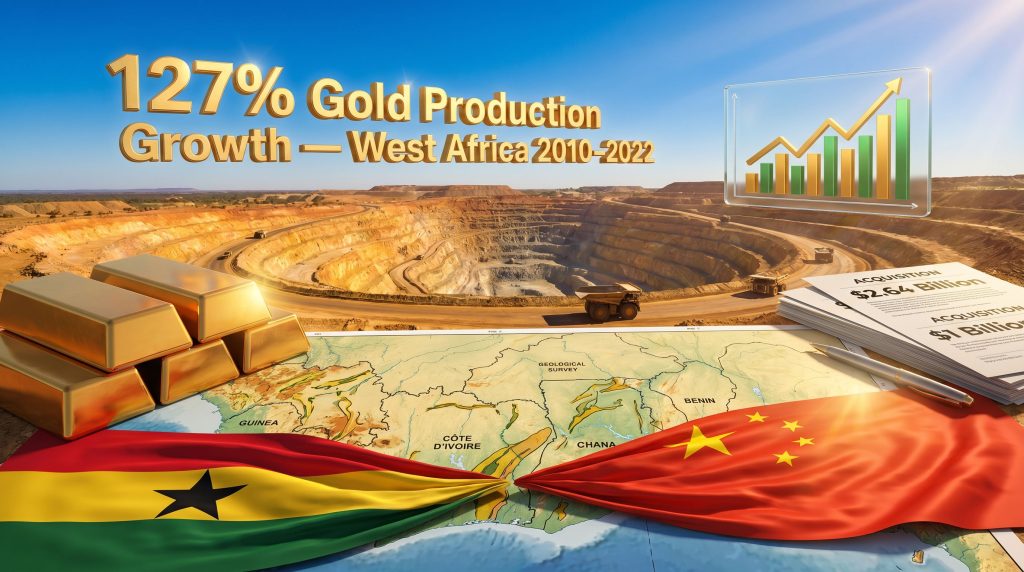

Few geological formations have generated more sustained interest from global mining capital than the West African Birimian greenstone belts. Stretching across Ghana, Côte d'Ivoire, Guinea, Mali, Burkina Faso, and Senegal, these ancient volcanic and sedimentary sequences have produced world-class gold deposits for decades, and remain significantly under-explored relative to their prospective extent.

The region recorded gold production growth of approximately 127% between 2010 and 2022, a rate that substantially outpaced established producers including China, Russia, and Australia over the same period. This trajectory reflects not just geological endowment but also the maturation of infrastructure, the development of experienced local workforces, and the cumulative investment in processing facilities that make new projects faster and cheaper to advance than comparable greenfield developments elsewhere.

Several characteristics make West African gold assets disproportionately attractive compared to other emerging jurisdictions:

- Ore grades across major deposits tend to be economically robust, reducing the processing intensity required per ounce of recovered gold

- Existing road, power, and water infrastructure in established mining corridors dramatically reduces capital development timelines

- Proven metallurgical characteristics across many deposits reduce processing risk for acquirers of existing operations

- Proximity to established export channels lowers logistics costs relative to landlocked alternatives in Central Asia or Central Africa

Elevated gold safe-haven demand has fundamentally altered the calculus of acquisition versus development. At current price levels, acquiring an operating or near-production asset in a stable West African jurisdiction generates compelling free cash flow from day one, without the multi-year permitting, feasibility, and construction timelines associated with building a mine from scratch. For Chinese miners specifically, this dynamic is amplified by access to long-duration, competitively priced capital that allows them to tolerate longer payback horizons than their Western counterparts are typically required to accept.

Zhaojin Mining Industry's chief investment officer, Xu Jianzhuo, articulated this logic plainly in comments to Bloomberg News, noting that gold sector mergers and acquisitions remain highly active and that the momentum is expected to intensify rather than subside, even given elevated gold prices, as companies continue pursuing scale. This perspective from inside one of China's most aggressive international acquirers confirms that the acquisition wave is driven by deliberate corporate strategy rather than opportunistic deal-making.

The Three Forces Pushing Western Miners Toward the Exit

The framing of Chinese acquisition as simply opportunistic misses an equally important dynamic: Western miners are not being outcompeted in deals they want to win. In many cases, they are actively seeking buyers for assets that no longer fit their strategic frameworks or risk tolerances.

Three structural forces are driving Western portfolio rationalisation across West Africa.

First, cost inflation has materially compressed margins. The All-In Sustaining Cost (AISC) metric, which captures the full cost of producing an ounce of gold including capital maintenance, has risen sharply across African operations for major producers. Gold Fields, one of the sector's largest operators with significant African exposure, has publicly flagged inflation-driven AISC deterioration at multiple operations. When cost structures rise faster than productivity gains, even assets in geologically attractive regions become candidates for divestment.

Second, regulatory complexity is increasing across multiple jurisdictions simultaneously. Governments across West Africa have been revising fiscal frameworks, royalty regimes, and environmental compliance requirements. For companies operating across multiple African countries, the cumulative compliance burden has grown significantly, particularly for operators whose shareholders apply rigorous environmental, social, and governance (ESG) screening.

Third, and most consequentially, mining geopolitical risks have repriced sharply. Barrick Mining's experience in Mali, where operational disputes over taxation and mining rights resulted in a nine-month shutdown of its gold operations following government intervention, served as a sector-wide warning about the asymmetric downside of operating in jurisdictions undergoing political transitions. That episode demonstrated that even world-class assets with decades of reserve life are not insulated from sovereign risk in unstable governance environments.

Resource Nationalism: The Burkina Faso Precedent

No single development has reshaped Western risk perceptions of West African mining more dramatically than Burkina Faso's aggressive nationalisation programme. The government's seizure of the Boungou and Wahgnion mines through state mining entity SOPAMIB, assets with a combined valuation of approximately $300 million that were reportedly compensated at roughly $80 million, crystallised what had previously been theoretical concern about sovereign expropriation into documented financial reality.

That compensation gap, representing more than 73% below stated asset value, effectively demonstrated the practical limits of contractual and legal protections in jurisdictions where state power is exercised outside normal institutional frameworks.

A separate demand for a 35% stake in West African Resources' Kiaka project triggered a trading halt that rattled investor confidence across the broader Sahel region. The message transmitted to global mining capital was unambiguous: operating in certain West African jurisdictions now carries a category of risk that cannot be adequately priced into a conventional mining investment framework.

The pattern across the Sahel is consistent. Countries with military-led governments or active insurgencies, most notably Mali, Burkina Faso, and Niger, are experiencing the most pronounced Western retreat. Meanwhile, Côte d'Ivoire, Ghana, and Guinea are being repositioned as the more stable tier of West African gold jurisdictions by operators reassessing continental exposure.

China's Two-Track Presence: Corporate Capital and the Informal Sector

What makes China's expanding footprint in West African gold distinct from previous waves of foreign mining investment is its dual nature. Two fundamentally different categories of Chinese participation operate simultaneously in the region, with very different characteristics, scales, governance standards, and consequences.

Corporate Acquisitions: Zijin, Zhaojin, and the Race for Production Scale

At the corporate level, major Chinese publicly listed mining companies are executing a deliberate, well-capitalised strategy to acquire existing West African gold operations rather than developing greenfield projects. The preference for acquiring operating assets reflects a strategic logic that prioritises immediate production contribution over long-term development optionality.

Zijin's global expansion has established it as perhaps the most aggressive Chinese acquirer in African gold. Its $1 billion acquisition of Ghana's Akyem mine in April 2025 was followed by the absorption of Chifeng Jilong Gold Mining in a transaction valued at approximately $2.64 billion (18.26 billion yuan), adding Ghana's Wassa mine to its portfolio. The Wassa asset alone carries an estimated 3.5 million ounces of gold resources with over six years of declared reserves, providing a substantial long-duration production base. Zijin also acquired Allied Gold Corp, extending its operational footprint simultaneously into Mali, Côte d'Ivoire, and Ethiopia.

The Bankan gold project in Guinea, being advanced by Predictive Discovery with Zijin holding a minority stake, targets approximately 250,000 ounces of annual production over a mine life exceeding 12 years. At steady-state output, this implies cumulative production of more than 3 million ounces over the project's life, positioning it as a significant long-duration asset in a jurisdiction that remains relatively under-penetrated by large-scale formal mining investment.

Zhaojin Mining's international expansion began in earnest in 2024 with its entry into Côte d'Ivoire. The company's Abujar mine is projected to deliver between 4 and 5 tonnes of gold output in 2026, establishing a meaningful production base in West Africa's most actively developing gold corridor. Xu Jianzhuo has indicated that Zhaojin's acquisition criteria explicitly prioritise politically stable jurisdictions with existing operational infrastructure, a strategic filter that reduces both execution risk and the time required to move from acquisition completion to material cash flow generation.

The table below summarises the major Chinese corporate gold transactions recorded across West Africa and the broader African region since 2024:

| Company | Target / Asset | Jurisdiction | Transaction Value | Key Resource Metric |

|---|---|---|---|---|

| Zijin Mining | Akyem mine | Ghana | ~$1 billion | Major operating gold mine |

| Zijin Mining | Chifeng Jilong / Wassa mine | Ghana | ~$2.64 billion | 3.5M oz resources, 6+ year reserves |

| Zijin Mining | Allied Gold Corp | Mali, Côte d'Ivoire, Ethiopia | Undisclosed | Multi-jurisdiction footprint |

| Zhaojin Mining | Abujar mine | Côte d'Ivoire | Undisclosed | 4-5 tonnes projected 2026 output |

| Predictive Discovery / Zijin (minority) | Bankan project | Guinea | Undisclosed | ~250,000 oz/year, 12+ year mine life |

Furthermore, beyond gold, Zhaojin has signalled interest in copper assets in Namibia and Botswana, though Xu Jianzhuo has noted that high capital costs in copper development demand a measured and phased approach rather than simultaneous aggressive deployment across multiple commodities.

The Informal Layer: Galamsey, Governance Gaps, and Environmental Cost

Running in parallel to the corporate acquisition wave is a far less visible and far more damaging form of Chinese mining participation: the illegal artisanal sector, known in Ghana as galamsey. This informal layer operates outside any regulatory framework and has produced some of the most severe environmental and social damage associated with gold extraction in West Africa.

An estimated 50,000 or more Chinese nationals entered Ghana's informal gold mining sector between 2008 and 2013, many traced to Shanglin County in Guangxi Province following crackdowns on illegal mining within China. These operators typically circumvent Ghana's legal prohibition on non-citizen small-scale mining participation by working through local intermediaries, with proceeds channelled back through informal networks outside formal banking systems.

The scale of environmental destruction attributable to these operations is staggering. More than 100,000 acres of cocoa farmland in Ghana have been estimated as destroyed or severely degraded, with cascading consequences for food security, rural livelihoods, and one of Ghana's most economically significant agricultural export industries. River systems have suffered mercury contamination from artisanal processing methods, forest cover has been stripped, and communities previously dependent on agricultural land have been displaced without compensation or recourse.

The environmental consequences of unregulated artisanal gold extraction in West Africa extend well beyond the mining sites themselves. The destruction of cocoa farmland, contamination of water sources, and displacement of agricultural communities represent a form of economic harm that persists long after any mining activity ceases.

This informal dimension creates a diplomatic and reputational complication for China's official engagement with West African governments. Ghana's 2026 enforcement raids on illegal mining operations in forest reserves, resulting in the arrest of foreign nationals, placed Beijing in an uncomfortable position, tasked with managing citizen welfare for individuals operating illegally while simultaneously protecting the reputational interests of state-linked corporate investors pursuing legitimate large-scale operations.

How Chinese and Western Mining Strategies Diverge

The contrast between Chinese and Western approaches to West African gold investment is not simply a matter of appetite for risk. It reflects fundamentally different institutional frameworks, financing structures, strategic time horizons, and stakeholder accountability mechanisms.

| Dimension | Chinese Operators | Western Operators |

|---|---|---|

| Primary capital source | State-affiliated financing + private equity | Public equity markets + project finance |

| Asset preference | Existing operations with near-term cash flow | Mix of greenfield, brownfield, and operating assets |

| Risk tolerance | Higher in stable jurisdictions | Significantly reduced post-Mali and Burkina Faso incidents |

| ESG accountability | Variable; less formally mandated | Institutionally mandated through shareholder frameworks |

| Investment time horizon | Long-term strategic hold | Portfolio optimisation with active divestment discipline |

| Informal sector presence | Material and documented | Negligible at corporate level |

| Community engagement | Highly variable | Structured through mandatory ESG frameworks |

The structural advantage Chinese acquirers hold in current conditions flows primarily from their capital access. State-affiliated financing mechanisms provide access to patient capital at competitive costs, allowing longer payback horizons that Western listed companies, accountable to quarterly earnings cycles and institutional ESG mandates, are structurally unable to match. Consequently, this is not a temporary competitive edge; it is a durable architectural difference in how the two systems approach long-duration resource investment. Indeed, gold M&A activity globally continues to reflect this fundamental asymmetry.

Security Risks: The Threat Landscape Facing Formal and Informal Operations

Chinese mining interests across West Africa face a threat landscape that is increasingly difficult to manage through conventional corporate risk frameworks. Armed groups operating across the Sahel have demonstrated both the capability and the willingness to target mining operations regardless of national origin.

Chinese mining personnel have been subjected to kidnappings, armed ambushes, and equipment destruction across Mali, the Central African Republic, Ghana, and the Democratic Republic of Congo. A documented attack on Chinese mining operations approximately 100 kilometres from Bamako, Mali, following the 2020 coup prompted evacuation advisories from China's embassy to its nationals working in the mining sector.

The security risk is compounded by the role of illicit gold in financing armed groups. Revenue streams from artisanal and illegal gold mining operations have been identified as funding sources for armed networks including Boko Haram affiliates and criminal organisations operating across Nigeria's Zamfara state. Gold trafficking routes through Burkina Faso, Mali, and Niger intersect with broader weapons and human trafficking corridors, creating a systemic security environment that no formal corporate governance structure can fully insulate operations from.

For formal Chinese corporate operators, this creates a paradox: their preference for existing, operating assets reduces development risk, but the geographic concentration of those assets in some of Africa's most security-stressed regions elevates operational risk in ways that are difficult to hedge.

The next major ASX story will hit our subscribers first

Country-Level Exposure: Which Markets Will Define the Next Decade

Not all West African gold jurisdictions are equal in terms of the opportunity or risk they present to Chinese acquirers. The divergence between stable-tier and high-risk jurisdictions has widened considerably since 2020.

Ghana has emerged as the primary destination for large-scale Chinese corporate capital, attracting multiple billion-dollar transactions from Zijin Mining alone. It simultaneously remains the epicentre of the illegal artisanal mining crisis, creating a bifurcated investment environment where formal and informal Chinese mining activity coexist in uncomfortable proximity. Government enforcement actions signal increasing regulatory assertiveness that may reshape operating conditions for both categories of operator.

Côte d'Ivoire represents the clearest example of a jurisdiction successfully positioning itself as a stable alternative to the Sahel. Zhaojin's explicit identification of the country as a preferred acquisition destination, combined with the projected output of the Abujar mine, suggests continued deal flow from multiple Chinese-affiliated entities pursuing assets along the country's proven gold corridors. In addition, African mining finance trends indicate that Côte d'Ivoire is attracting an increasing share of structured investment across the continent.

Guinea offers long-duration geological opportunity, particularly through projects like Bankan, but requires careful investment structuring to account for governance uncertainty under military-led administration. Chinese operators with higher risk tolerance and flexible financing structures may be comparatively better positioned to navigate Guinea's regulatory environment than Western peers operating under more rigid institutional constraints.

Mali and Burkina Faso remain the clearest examples of jurisdictions where even the risk tolerance advantage held by Chinese operators is not sufficient to make formal corporate investment straightforward. Asset seizures, military governance, and the expulsion of Western security forces have created a risk-reward profile that deters most formal capital, though some Chinese operators maintain presence leveraging China's non-interventionist diplomatic posture.

The Long-Term Ownership Shift and What It Means

The combined effect of Western divestment and Chinese acquisition is producing a measurable and accelerating transfer of gold asset ownership across West Africa. This is not simply a financial transaction; it carries long-term consequences for how royalties flow, what environmental standards are applied, how employment is structured, and what governance leverage host countries retain.

Three scenarios define the plausible range of outcomes over the next decade:

| Scenario | Enabling Conditions | Likely Outcome |

|---|---|---|

| Accelerated Consolidation | Gold prices remain elevated; Western exit continues | Chinese entities controlling a significantly larger share of formal West African gold output within a decade |

| Regulatory Pushback | Host governments implement stricter local ownership requirements | Deal structures shift toward joint ventures and minority stakes; acquisition pace moderates |

| Security Deterioration | Sahel instability spreads to coastal states | Operational disruptions accelerate; informal sector violence intensifies; formal capital pauses |

China's interest in West African resources extends beyond gold. The same strategic logic that drives a Chinese miner hunts West Africa gold assets applies to the continent's lithium, cobalt, and copper endowment. As reported by Africa Business Insider, this systematic pursuit of assets abandoned by Western firms is reshaping the continent's mining ownership landscape at speed. Zhaojin's stated interest in copper assets in Namibia and Botswana signals that the resource acquisition strategy is a component of a broader continent-wide framework rather than a narrowly defined gold play.

Host governments across the region face a strategic question that has no simple answer: the short-term revenue benefits of Chinese-funded acquisitions are real, but the long-term implications for governance leverage, technology transfer, environmental standards, and supply chain control require careful navigation. The countries that develop the institutional capacity to structure Chinese investment on terms that serve their long-term development interests will be materially better positioned than those that simply accept the terms available in the current M&A cycle.

This article draws on publicly available reporting and industry data for analytical purposes. All transaction valuations, production forecasts, and resource estimates should be verified against primary company disclosures and regulatory filings. Nothing in this article constitutes investment advice.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex geological data into actionable investment insights for both short-term traders and long-term investors — explore historic examples of major discoveries and their returns to understand the opportunity, then start your 14-day free trial at Discovery Alert to position yourself ahead of the market.