July 11, 2026

The Two-Decade Supply Gap That Made U.S. Chrome Metal a Strategic Priority

Specialty metals markets operate on long cycles. Unlike bulk commodities where supply can be scaled relatively quickly, the infrastructure, process knowledge, and raw material networks required to produce high-purity metals take years to rebuild once dismantled. The AMG Chrome US expansion is a precise illustration of this dynamic. When the last U.S. domestic production facility ceased operations in 2006, the country did not simply lose a manufacturing asset. It severed a critical link in the supply chain feeding aerospace engines, industrial turbines, and high-performance alloys. Nearly two decades later, the consequences of that decision have become impossible to ignore.

The re-emergence of domestic chrome metal production in 2025, led by AMG Chrome's newly commissioned Pennsylvania facility, is not an isolated industrial development. It reflects a fundamental recalibration in how Western economies think about material sovereignty, and which metals are genuinely too important to leave entirely in the hands of foreign suppliers.

When big ASX news breaks, our subscribers know first

Understanding Chrome Metal's Role in the U.S. Critical Materials Framework

Why Chrome Metal Was Classified as Critical

Chrome metal occupies a specific and technically demanding position within the broader critical materials landscape. Unlike chromium compounds used in pigments or surface treatments, chrome metal itself is a high-purity elemental form processed specifically for metallurgical applications. Its primary function is as an alloying agent in nickel-chromium superalloys, which are indispensable for jet engine components, gas turbine blades, and other parts operating under extreme heat and stress conditions.

The U.S. critical materials designation for chrome metal is not decorative. It signals that domestic procurement and downstream industrial sectors cannot sustainably function without a reliable supply, and that the absence of domestic production creates genuine national security exposure. This classification places chrome alongside more prominently discussed materials like lithium, cobalt, and rare earth elements within the framework of U.S. supply chain resilience policy. Furthermore, the critical minerals demand surge across allied economies has amplified the urgency of securing domestic production of metals like chrome.

What makes chrome metal's situation particularly acute is the duration of the supply gap. A two-decade absence of domestic production means that not only was physical capacity lost, but process knowledge, trained workforces, and supplier relationships were also substantially eroded. Rebuilding this foundation requires deliberate investment rather than a simple restart of mothballed equipment.

The Geopolitical Pressure Accelerating Onshoring

Resource nationalism, shifting trade dynamics, and the growing use of commodity supply as a geopolitical lever have collectively concentrated the minds of both industrial buyers and policymakers. The recognition that import dependency in critical metals can be weaponised, or at minimum disrupted by events entirely outside a buyer's control, has reshaped procurement strategies across aerospace, defence, and energy infrastructure sectors.

Chrome metal fits squarely into this reconfiguration. Aerospace original equipment manufacturers and defence contractors increasingly view domestically sourced critical materials not simply as a cost variable but as a supply security requirement. The strategic supply chain importance of these metals has driven the availability premium that U.S. buyers are prepared to pay for onshore material, reflecting a genuine willingness to prioritise reliability over marginal cost savings.

Inside AMG Chrome's Pennsylvania Facility: Specifications and Production Logic

Facility Snapshot: New Castle, Pennsylvania

| Attribute | Detail |

|---|---|

| Location | New Castle, Pennsylvania (co-located with AMG Titanium operations) |

| Capital Investment | $15 million |

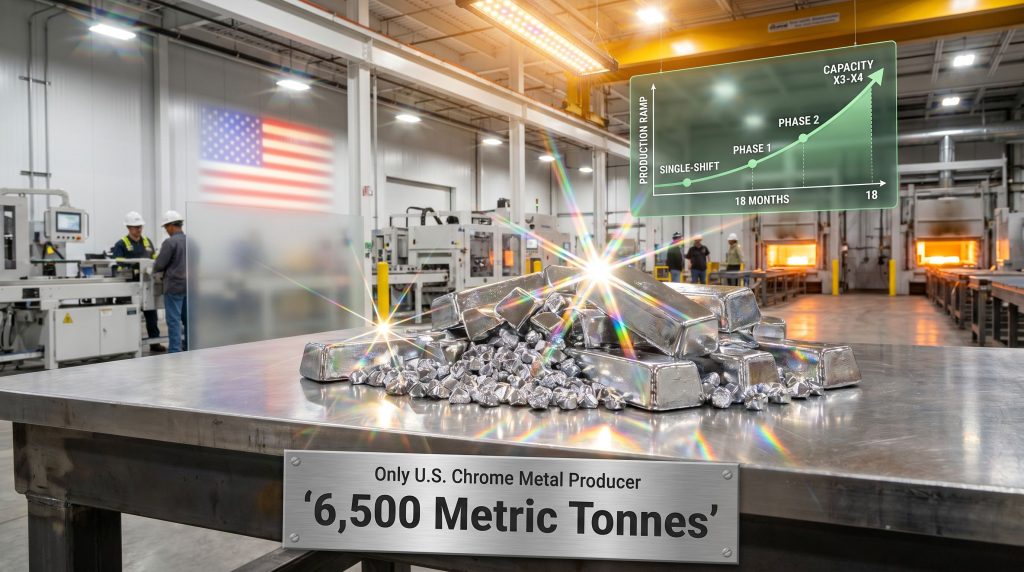

| Annual Production Capacity | 6,500 metric tonnes |

| Production Method | Aluminothermic reduction |

| Operational Status | Opened 2025; targeting full capacity within ~8 weeks of mid-2026 commissioning |

| Market Focus | Exclusively U.S. domestic customers |

| Workforce | Expanding from 10 to 29 employees by end of 2025 |

| U.S. Market Position | Sole operational chrome metal producer in the United States |

How Aluminothermic Reduction Actually Works

The production method at the heart of AMG Chrome's Pennsylvania facility is aluminothermic reduction, a process less familiar to general audiences than conventional smelting but technically well-suited to producing the high-purity chrome metal grades demanded by advanced manufacturing sectors.

The process involves the following sequence:

-

Feedstock preparation: Chromium oxide, sourced from chromite ore processing, is combined with fine aluminium powder in precise ratios.

-

Ignition and thermite reaction: The mixture is ignited, triggering an intensely exothermic reaction in which aluminium reduces the chromium oxide, releasing elemental chrome metal and producing aluminium oxide (corundum) as a byproduct slag.

-

Metal separation: The molten chrome metal, being denser than the slag, settles to the bottom of the reaction vessel and is separated after cooling.

-

Crushing and grading: The solidified chrome metal is crushed and screened to produce the lump, granule, and chip grades required by different end users.

The purity levels achievable through aluminothermic reduction make this process particularly valued for superalloy production, where even trace contaminants can affect the mechanical properties of finished components operating at extreme temperatures. Typical aluminothermic chrome metal grades achieve purities of 99% or above, meeting the specifications demanded by aerospace alloy producers.

The Vertical Integration Advantage: Owning the Aluminium Powder Supply

One strategically underappreciated aspect of AMG Chrome's operational structure is its ownership of an aluminium powder manufacturing plant. In aluminothermic reduction, aluminium powder is not a peripheral consumable but the central chemical reactant. Its quality, particle size distribution, and purity directly affect the efficiency of the reaction and the purity of the resulting chrome metal.

Producers relying on third-party aluminium powder suppliers face both cost exposure and potential availability constraints. AMG Chrome's in-house powder production provides meaningful insulation from spot market pricing volatility. However, as AMG Chrome's leadership has noted, the specific aluminium grade required for this process has become moderately tight in the current market, with premiums rising. Long-term supply agreements provide coverage, but the dynamic underscores why feedstock self-sufficiency is a genuine competitive differentiator rather than a simple operational convenience.

Operational Division Between Pennsylvania and Rotherham

AMG Chrome operates a parallel production facility in Rotherham, United Kingdom, which has historically served global customers across multiple geographies and product lines, including chrome powder products in addition to standard chrome metal grades. The strategic logic underpinning the Pennsylvania investment was to create a geographically separate, dedicated domestic supply node for U.S. customers.

This separation is more than administrative. By routing U.S. customer supply exclusively through a domestic facility, AMG Chrome removes the exposure to international logistics disruptions, shipping cost volatility, and import dependency that would otherwise remain inherent in a UK-only supply model. Notably, both the Rotherham and New Castle facilities are currently reported as sold out, a market signal that aggregate demand across both plants exceeds available combined capacity.

Ramp-Up Timeline: From Training Phase to Full Output

Phase-by-Phase Capacity Build

The ramp-up trajectory for the New Castle facility follows a deliberately staged approach, prioritising process control and workforce competency before pushing for maximum throughput.

-

Phase 1 – Training and Process Control: Initial operations run on a single shift. The emphasis is on embedding process safety protocols and building operator familiarity with aluminothermic production before optimising output rates.

-

Phase 2 – Full Single-Shift Capacity: The facility is targeting the full 6,500 t/yr capacity run rate within approximately eight weeks of commissioning, operating on a four-day production week. This scheduling structure is not arbitrary; a four-day week at single-shift operation still achieves the rated annual capacity, whilst preserving operational flexibility.

-

Phase 3 – Dual-Shift Operations: Transitioning to two shifts would activate the remaining three production days and unlock throughput meaningfully above the initial capacity ceiling without requiring new capital investment.

-

Phase 4 – Capacity Expansion: If commercial offtake agreements and investment decisions are finalised, a programme to expand output to three or four times the current 6,500 t/yr level has been identified as achievable within an 18-month fast-track timeline.

The preference expressed by AMG Chrome's leadership is to keep any expansion within the New Castle industrial area, citing established community relationships, an existing trained workforce, and the region's industrial heritage as factors supporting continuity over greenfield development.

What a Capacity Tripling or Quadrupling Would Mean for the Market

If AMG Chrome were to execute an expansion programme bringing output to three to four times current capacity, total production from the Pennsylvania facility alone could approach or exceed 20,000 to 26,000 metric tonnes per year. Given that this would still represent a fraction of total U.S. chrome metal consumption requirements, it illustrates the scale of the structural supply deficit that currently exists in the domestic market.

The offtake discussions referenced by AMG Chrome's leadership suggest that customer demand could absorb this expanded volume without difficulty, a remarkable statement about the depth of unmet demand for domestically sourced material.

Demand Drivers: Aerospace Recovery and the Fuel Cell Inflection

Demand Sector Comparison

| Demand Sector | Growth Trajectory | Chrome Application | Key Growth Catalyst |

|---|---|---|---|

| Aerospace | Moderate, recovering | Ni-Cr superalloys for jet engines | Boeing build rate recovery; Airbus order book expansion |

| Fuel Cell / Data Centres | Exponential | Chrome components for stationary fuel cells | Data centre energy independence; off-grid power systems |

| Defence and Space | Steady | High-performance alloys for military and space applications | Critical material designation; domestic sourcing requirements |

The Fuel Cell Market: A Non-Traditional Demand Channel Growing Faster Than Aerospace

Perhaps the most consequential and least widely understood development in chrome metal demand is the emergence of stationary hydrogen fuel cells as a significant and rapidly scaling consumption channel. This is not a traditional market for chrome, and its growth trajectory is materially different from the cyclical patterns that have historically governed chrome demand.

Stationary fuel cells, particularly those deployed by data centre operators seeking reliable off-grid or backup power, incorporate chrome-containing components that perform under sustained electrochemical stress. The proliferation of large-scale data centre infrastructure, driven by cloud computing expansion and artificial intelligence workload growth, has created a new and structurally uncorrelated demand stream for chrome metal.

AMG Chrome's leadership has characterised fuel cell market growth as expanding at an exponential rate compared to the more measured recovery underway in aerospace. This distinction matters for how producers and downstream processors think about long-term capacity planning. A demand base built on fuel cell deployment is less sensitive to aircraft delivery cycles and more anchored to technology infrastructure investment, which has shown remarkable durability across economic cycles.

Aerospace Recovery and the Supply Chain Timing Problem

The aerospace sector's recovery from the production constraints that plagued Boeing through the early 2020s is translating into improved demand for nickel-chromium superalloy materials. Both Boeing's gradually recovering build rates and Airbus's expanding order book represent genuine tailwinds for chrome metal consumption.

However, a technically important nuance that is often overlooked is the multi-stage lag between chrome metal procurement and final aircraft delivery. The sequence runs from chrome procurement through alloy production, component manufacturing, engine assembly, and ultimately aircraft delivery. This pipeline means that demand signals visible at the chrome metal level today may not translate into delivered aircraft for eighteen months to three years. Procurement teams at superalloy producers and aerospace OEMs must therefore read chrome demand with a significant lead time, and any tightening in chrome availability will cascade through the supply chain with a delay that can create acute shortages at individual production stages.

The order book for aerospace is described as very solid by industry participants, but the distinction between solid orders and actual production pull-through remains an important nuance for chrome metal producers managing capacity decisions.

Supply Chain Security: Aluminium Feedstock and Global Disruption Risks

Supply Chain Risk Assessment

| Risk Factor | Severity | Mitigation in Place |

|---|---|---|

| Aluminium grade availability | Moderate | Long-term supply agreements provide coverage |

| Aluminium price premiums | Low-to-moderate | Partially absorbed; contracts limit spot exposure |

| Geopolitical disruption to aluminium supply | Low (near-term) | Self-sufficient powder production; diversified sourcing |

| Chromite ore supply (upstream) | Low | Established global sourcing relationships |

| Logistics and shipping disruptions | Low (domestic focus) | Pennsylvania plant serves domestic customers only |

The EGA Al Taweelah Incident as a Case Study in Upstream Fragility

The March 2026 suspension of alumina production at Emirates Global Aluminium's Al Taweelah refinery in Abu Dhabi, triggered by Iranian attacks on the Khalifa Economic Zone, offers a precise illustration of how geopolitical events can rapidly propagate through aluminium supply chains. The refinery, which produced 2.4 million tonnes of alumina in 2025 and supplied approximately 46% of EGA's own alumina requirements, was forced to halt operations for months before beginning a phased restart.

As of July 2026, EGA has restarted alumina production and is targeting approximately 50% of refinery capacity within days, with full technical capability to return to full production targeted by end of 2026. The episode demonstrates that even large, well-capitalised producers in politically stable-seeming environments are not immune to rapid supply disruption.

For chrome metal producers dependent on aluminium as a primary chemical reactant, this upstream fragility reinforces the strategic value of in-house powder production capability. The ability to manufacture aluminium powder internally does not eliminate exposure to aluminium market tightness, but it does provide a meaningful buffer against spot market disruptions that can affect external powder suppliers more acutely. In addition, the broader focus on energy security in critical minerals underscores why feedstock resilience has become a non-negotiable priority for producers in this space.

The next major ASX story will hit our subscribers first

Is the U.S. Chrome Metal Market Structurally Undersupplied?

Reading the Signals Embedded in a Sold-Out Market

When both the only domestic U.S. chrome metal producer and its UK sister facility are simultaneously sold out, the market is communicating something specific: available supply is insufficient to meet current demand at prevailing terms, and no meaningful surge capacity exists to bridge the gap in the near term.

This sold-out condition is not simply a reflection of temporary demand spikes. The depth of the offtake discussions underway, reportedly involving volumes that could necessitate tripling or quadrupling current combined capacity, implies a demand base substantially larger than what existing production can serve. If total customer demand under discussion requires output at three to four times the current 6,500 t/yr Pennsylvania capacity, the implied demand from AMG's customer base alone approaches a scale that the entire facility's expansion programme would still only partially address.

Several intersecting forces support the view that this undersupply is structural rather than cyclical:

-

The absence of other domestic U.S. producers means new competitive supply cannot emerge quickly.

-

The fuel cell sector's exponential growth trajectory creates demand that was not present in previous chrome market cycles.

-

Aerospace recovery adds incremental demand on top of a base that never fully recovered from pandemic-era disruptions.

-

Defence and space sector sourcing requirements increasingly favour or require domestically produced critical materials, further supported by US critical minerals production policies driving onshoring commitments.

The Availability Premium: What Buyers Are Actually Paying For

One dimension of the domestic chrome metal market that deserves specific attention is the concept of the availability premium. U.S. buyers sourcing domestically produced chrome metal are not simply paying for the metal itself. They are paying for guaranteed delivery timelines, reduced exposure to import logistics disruptions, and the assurance of a supply relationship not subject to foreign policy risk.

For defence contractors and aerospace OEMs operating under strict production schedules and domestic sourcing requirements, this premium represents a rational economic decision. The cost of a production halt caused by import disruption far exceeds any savings achievable through lower-cost imported material. This dynamic creates a durable pricing floor for domestically produced chrome metal that insulates producers like AMG Chrome from purely price-driven import competition.

Frequently Asked Questions: AMG Chrome US Expansion

What is AMG Chrome and where does it operate?

AMG Chrome is a subsidiary of Netherlands-headquartered AMG Critical Materials. It operates a chrome metal production facility in Rotherham, United Kingdom, and opened a second facility in New Castle, Pennsylvania in 2025, making it the only company currently producing chrome metal within the United States.

Why did the U.S. have no domestic chrome metal production for nearly 20 years?

The last domestic chrome metal producer ceased U.S. operations in 2006. The closure reflected a combination of cost pressures and the availability of lower-cost imported material, particularly from producers in Russia and Kazakhstan. The structural vulnerability created by this gap only became fully apparent as geopolitical tensions elevated supply security concerns across critical material categories.

What is the aluminothermic reduction process?

Aluminothermic reduction involves reacting chromium oxide with aluminium powder at high temperature. The aluminium displaces the chromium through an intensely exothermic reaction, yielding high-purity chrome metal and an aluminium oxide slag byproduct. The process is well-suited to producing the purity levels required for aerospace-grade superalloy applications.

How quickly can AMG Chrome reach full capacity at the Pennsylvania plant?

The facility is targeting its full 6,500 t/yr capacity within approximately eight weeks of initial commissioning, operating on a single shift across a four-day production week. Transitioning to dual-shift operations would open additional throughput, and a larger expansion programme could be completed within 18 months of a final investment decision.

Which sectors are driving the strongest chrome metal demand growth?

The fuel cell sector, particularly stationary fuel cells serving data centre power requirements, is currently exhibiting the fastest demand growth. Aerospace represents a solid and recovering demand base, whilst defence and space applications provide steady incremental consumption anchored to domestic sourcing requirements.

Could the Pennsylvania facility expand beyond 6,500 t/yr?

AMG Chrome has indicated that commercial discussions could necessitate a significant capacity expansion, with output potentially reaching three to four times the current level. The company's preference is to expand within the existing New Castle industrial footprint, with an 18-month development timeline cited as achievable once investment and commercial decisions are finalised.

What AMG Chrome's Expansion Signals for the Broader Chrome Metal Market

Structural Implications for Global Trade Flows

The AMG Chrome US expansion will gradually redirect trade flows that have historically channelled imported chrome into U.S. markets. As major aerospace and energy sector buyers shift toward domestic offtake agreements, traditional supplying regions will face displacement of their U.S. customer relationships, even if global demand growth partially offsets this reorientation.

The simultaneous sold-out condition across AMG's entire production network suggests that global demand is currently outrunning available supply from established producers, which supports a constructive pricing environment and reduces the risk that new U.S. production would face aggressive import competition in the near term.

The Industrial Sovereignty Dimension

AMG Chrome's Pennsylvania investment is one data point within a significantly larger pattern of critical mineral onshoring visible across allied economies. The strategic logic that has driven lithium refinery investments, rare earth processing initiatives, and cobalt supply chain restructuring in North America and Europe applies with equal force to chrome metal. Consequently, the critical minerals executive order framework has provided additional policy momentum that validates precisely this kind of domestic production investment.

What distinguishes chrome metal from some other critical materials is the maturity of the end markets it serves. Aerospace and defence are established, high-value, specification-driven industries where supply security commands a genuine and sustained premium. The fuel cell sector adds a growth dimension to this demand profile that positions chrome metal at the intersection of legacy industrial applications and emerging energy infrastructure.

This combination makes the AMG Chrome US expansion more than a simple onshoring story. It is an early indicator of where critical specialty metals investment is headed as material sovereignty becomes a defining feature of industrial policy across Western economies. As Assembly Magazine has noted, new domestic chrome production directly strengthens the broader U.S. manufacturing supply chain in ways that extend well beyond the metals sector alone.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts, capacity projections, and market demand estimates involve inherent uncertainty and should not be relied upon as guarantees of future outcomes. Readers should conduct independent research and consult qualified advisors before making investment decisions.

Want to Stay Ahead of Critical Mineral Discoveries Driving the Next Industrial Shift?

As chrome metal, rare earths, and other strategic materials reshape global supply chains, Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts the moment significant mineral discoveries are announced — turning complex data across 30+ commodities into clear, actionable opportunities for both traders and long-term investors. Explore historic discovery returns on Discovery Alert's discoveries page and begin your 14-day free trial today to position yourself ahead of the market.