June 9, 2026

The Structural Flaw in Linear Metal Systems: Why the Old Model Is Failing

The physics of metal extraction have always been unforgiving, but for much of the twentieth century, abundant high-grade deposits and cheap energy masked the true cost of linear production. That era is drawing to a close. Average copper ore grades across major producing regions have declined from roughly 1 to 2 percent in the early 1900s to well below 1 percent in many contemporary large-scale operations, with some mines processing material closer to 0.5 percent or lower. The circular economy in metal supply chains is emerging as the structural response to this deterioration, offering a systemic alternative to a model that is reaching its economic and environmental limits.

This grade deterioration is not a minor operational inconvenience. It means dramatically more rock must be blasted, hauled, crushed, and processed to yield the same unit of refined metal, compounding energy consumption and waste generation at every stage.

The emissions footprint of this model is substantial. Iron and steel production alone accounts for approximately 7 to 9 percent of global energy-related CO₂ emissions, while aluminium smelting contributes roughly a further 2 percent (International Energy Agency, Iron and Steel Technology Roadmap, 2020). Combined with copper, nickel, and other base metal production, primary metal manufacturing constitutes a meaningful share of total global industrial emissions, making it a central target for both climate regulation and corporate decarbonisation commitments.

Geographic concentration compounds these pressures. A significant proportion of global critical minerals demand originates from a small number of countries, creating systemic fragility whenever trade relationships shift or political stability wavers. For industries dependent on uninterrupted mineral flows, including electric vehicle manufacturing, clean energy infrastructure, and advanced electronics, the structural risks embedded in linear, geographically concentrated supply chains represent a growing strategic liability.

"The linear model was engineered for an era of abundant, low-cost resources. In a world of declining ore grades, tightening environmental regulation, and geopolitical supply concentration, it functions as a structural liability rather than a competitive framework."

When big ASX news breaks, our subscribers know first

What Does a Circular Economy in Metal Supply Chains Actually Mean?

Defining Circularity Beyond Recycling

The circular economy in metal supply chains is frequently reduced in public discourse to the act of recycling, but this framing understates the concept's scope and undersells its transformative potential. True circularity encompasses a much broader set of interventions: designing products for disassembly from the outset, enabling component-level reuse and remanufacturing, creating transparent material provenance systems, valorising process residues and mine tailings, and configuring regional material loops that keep recovered metals geographically proximate to reprocessing infrastructure.

Metals are uniquely positioned within circular economy frameworks because, unlike most polymers or organic materials, they do not chemically degrade through multiple processing cycles. Steel, aluminium, copper, cobalt, and many other metals retain their fundamental metallurgical properties after recycling, making them inherently suited to repeated recovery without significant loss of material quality.

This characteristic is what separates true closed-loop circularity, where recovered metal re-enters equivalent-grade applications, from open-loop recycling, where material is progressively downgraded into lower-value uses and eventually lost from productive industrial flows. Furthermore, secondary raw materials, when positioned correctly within supply chain strategy, cease to be a waste management output and become a proprietary industrial asset.

The Five Pillars of a Circular Metal Supply Chain

| Pillar | Description | Strategic Benefit |

|---|---|---|

| Design for Circularity (DfC) | Products engineered for disassembly, modularity, and recyclability | Reduces end-of-life material loss |

| Scrap Recovery and Recycling | End-of-life metals reintroduced as secondary feedstock | Reduces dependence on virgin ore |

| Material Transparency | Tracking composition and provenance of recovered metals | Enables safe, efficient re-entry into supply chains |

| Waste Valorisation | Mine tailings, process residues, and by-products redeployed as inputs | Converts environmental liability into resource value |

| Regional Material Loops | Keeping recovered materials geographically close to reprocessing | Lowers transport emissions and improves supply resilience |

How Is Technology Accelerating the Shift to Circular Metal Supply Chains?

Advanced Sorting and Separation: Precision at Scale

One of the most consequential technical bottlenecks in secondary metal production is the ability to accurately identify and separate complex alloy compositions from mixed post-consumer waste streams. Contaminated or misidentified scrap introduces quality problems downstream that can compromise the usability of recovered material in high-specification applications.

AI-driven robotic sorting systems are beginning to address this constraint at commercial scale. These platforms combine machine learning-based object recognition with high-speed mechanical separation, enabling processing facilities to distinguish between alloy grades that were previously impossible to separate economically at volume. X-ray sorting technology provides real-time elemental composition data, allowing processors to route material streams with precision and improve recovery purity without sacrificing throughput speed.

The strategic importance of sorting precision extends beyond operational efficiency. Higher-purity secondary feedstocks command premium pricing, attract more demanding downstream customers, and enable recycled metals to compete for applications previously reserved exclusively for primary material.

Digital Traceability: Blockchain and Digital Product Passports

The provenance problem in secondary metals has historically been a barrier to broader adoption of recycled content in regulated or safety-critical applications. Without a verifiable chain of custody, manufacturers face uncertainty about composition, contamination history, and regulatory compliance status of recovered material.

Blockchain-enabled record systems create tamper-resistant provenance trails that follow recovered metals from collection through processing and reintroduction into supply chains. This architecture supports compliance verification, simplifies auditing, and reduces the due diligence burden for manufacturers integrating secondary feedstock.

Digital product passports extend this logic upstream by embedding material composition and processing history data into products at the design and manufacturing stage. When a product reaches end of life, its passport enables disassembly teams and recycling processors to immediately identify material types, separation requirements, and hazardous substance content. Under regulatory frameworks such as the EU Critical Raw Materials Act, traceability capabilities are increasingly a compliance requirement rather than an optional enhancement.

Next-Generation Recycling Processes

Conventional pyrometallurgical smelting, while effective for bulk base metals, generates significant thermal energy demand and faces inherent limitations when processing chemically complex feedstocks such as lithium-ion battery black mass or mixed electronic waste streams. The battery recycling process is consequently evolving toward more targeted approaches that can handle these complex compositions efficiently.

Hydrometallurgical recovery methods, which use aqueous chemical solutions to dissolve and selectively precipitate target metals, operate at lower temperatures and generate fewer combustion emissions. Their particular advantage lies in treating low-grade or compositionally complex feedstocks that conventional smelting cannot process efficiently or economically.

Bioleaching takes this further, employing microbial organisms to extract metals from waste streams through biological oxidation and reduction processes, an approach that holds particular promise for recovering cobalt, nickel, and lithium from battery waste.

"Hydrometallurgical and bioleaching methods are gaining traction precisely because they unlock metal recovery from feedstock categories that conventional high-temperature smelting either cannot process or processes at prohibitive cost."

Emerging research in critical raw materials transition is particularly significant given the trajectory of battery deployment globally. The International Energy Agency projects that demand for lithium could increase by more than 40 times by 2040 in a Paris-aligned scenario, with cobalt and nickel demand rising by 20 to 25 times (IEA, The Role of Critical Minerals in Clean Energy Transitions, 2021).

What Role Does Design for Circularity Play in Metal Supply Chain Transformation?

Rethinking Product Architecture from the First Sketch

Design for Circularity represents perhaps the highest-leverage intervention point in circular metal supply chains because it shapes material recovery outcomes decades before a product reaches end of life. Products designed without disassembly in mind, where dissimilar materials are bonded, welded, or encapsulated together, impose significant cost and complexity penalties on recycling operators attempting to separate valuable metal fractions.

Modular component design addresses this by enabling part-level recovery and remanufacturing rather than forcing whole-product disposal. A motor component engineered with standardised fastening and clear material identification can be extracted, assessed, reconditioned, and redeployed at a fraction of the energy cost of smelting the same mass of metal and reprocessing it into new components.

Material selection strategies under DfC prioritise recyclability alongside structural and functional performance, avoiding material combinations that create inseparable contamination problems in downstream processing. The economic case is increasingly compelling, as reducing end-of-life material loss means lower future raw material procurement costs and stronger ESG positioning for financing and customer relationships.

From Product Ownership to Material Stewardship

A structural shift accompanying Design for Circularity is the evolution of business models from transactional product sales toward service-based and product-as-a-service arrangements. Under these models, manufacturers retain legal or commercial responsibility for the material content of their products throughout the full use cycle, creating a direct financial incentive to optimise for end-of-life recovery.

Take-back programmes operationalise this responsibility through organised collection logistics, condition assessment protocols, and defined reprocessing pathways. Heavy industrial equipment manufacturers have begun piloting remanufacturing-as-a-service approaches, where major components such as hydraulic systems and drivetrain assemblies are systematically recovered, remanufactured to original specification, and redeployed.

How Are Reverse Logistics Networks Enabling Closed-Loop Metal Recovery?

Building the Infrastructure for Material Return

The physical infrastructure of circular metal supply chains is built on reverse logistics networks: the systems of collection hubs, transport routing, and pre-processing facilities that move end-of-life material from dispersed generation points to centralised recovery operations. Designing this infrastructure efficiently requires careful analysis of material flow density, transport economics, and the spatial relationship between collection zones and processing capacity.

Industrial metals present specific reverse logistics challenges compared to consumer packaging or electronics. Bulk weights, irregular geometries, and mixed material composition require specialised handling equipment and sorting capabilities that are not yet uniformly available across all geographies.

Urban Mining: Treating Cities as Secondary Ore Bodies

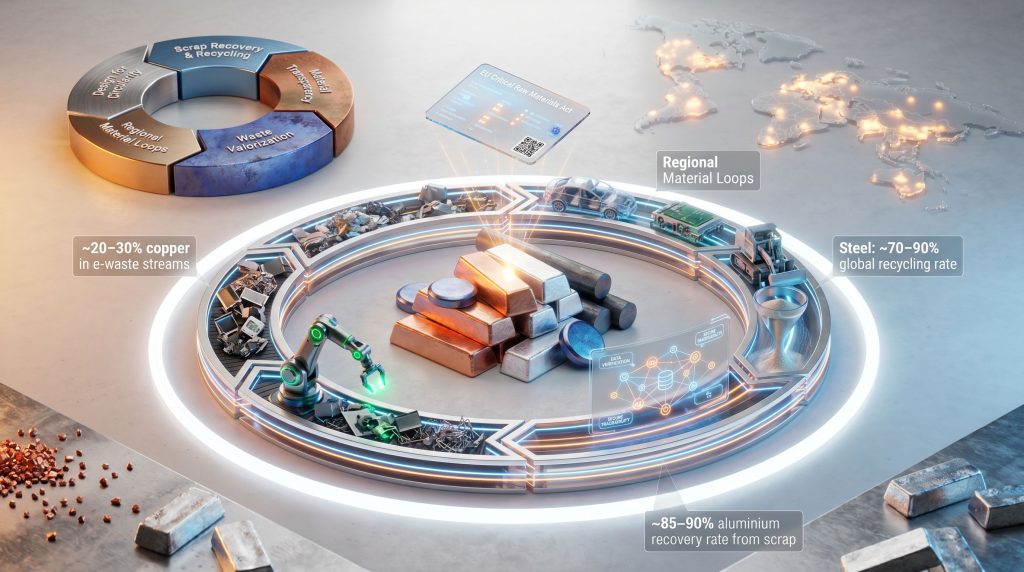

Urban mining reframes built environments and end-of-life product stockpiles as secondary ore bodies, recognising that the metal concentrations embedded in discarded electronics, infrastructure, vehicles, and industrial equipment frequently exceed the grades available in primary ore at operating mines. According to the Ellen MacArthur Foundation, this approach is central to delivering a genuinely circular model for critical minerals at scale.

The figures below illustrate the contrast between urban mine concentrations and primary ore grades for key metals:

| Metal | Estimated Urban Mine Concentration | Primary Ore Grade (Typical) |

|---|---|---|

| Copper | 20 to 30% in e-waste streams | 0.5 to 1.5% in ore |

| Aluminium | 85 to 90% recovery rate from scrap | Bauxite processing intensive |

| Cobalt | 5 to 10 kg per tonne of lithium-ion battery black mass | 0.1 to 0.5% in primary ore |

| Steel | 70 to 90% global recycling rate | Iron ore dependent |

Figures are indicative estimates based on published industry research ranges.

As primary ore grades continue their long-term structural decline, the relative resource intensity advantage of urban mining will strengthen. The energy savings of recycling compared to primary production are substantial. Secondary aluminium production requires approximately 95 percent less energy than smelting primary aluminium from bauxite, a differential that translates directly into cost economics and carbon footprint at scale (International Aluminium Institute, 2021).

What Are the Regulatory and Policy Frameworks Shaping Circular Metal Supply Chains?

The EU's Legislative Architecture for Circular Metals

The European Union has constructed the most comprehensive legislative architecture currently in force for circular metal supply chains. The EU Circular Economy Action Plan establishes mandatory recycled content targets across product categories, extends producer responsibility to cover end-of-life collection and processing obligations, and embeds ecodesign requirements that progressively mandate Design for Circularity principles across regulated product families.

The Critical Raw Materials Act adds a strategic sovereignty dimension, positioning secondary material supply chains as a mechanism for reducing dependence on geographically concentrated primary sources. The Act's recycled content benchmarks and traceability requirements create structural market demand for certified secondary materials, generating regulatory pull rather than relying solely on voluntary industry adoption.

International Harmonisation: The Missing Link in Global Circular Supply Chains

A persistent structural barrier to global circular metal supply chain development is the inconsistency of cross-border classification frameworks for secondary raw materials. When a recovered metal stream is classified as waste rather than a secondary raw material, it becomes subject to waste transport regulations that significantly increase the cost, complexity, and lead time of international trade in recycled feedstocks.

This regulatory fragmentation creates arbitrage risks and impedes the flow of recovered materials to the processing facilities best equipped to handle them, regardless of geography. Achieving meaningful international harmonisation of secondary material classifications is a precondition for a genuinely global circular metal economy.

Policy Gaps and Emerging Regulatory Frontiers

Several areas remain underdeveloped in current policy frameworks:

- Extended Producer Responsibility schemes for industrial metals are unevenly adopted across jurisdictions, leaving significant material flows outside formal recovery obligations.

- Carbon border adjustment mechanisms interact with circular supply chain economics in complex ways, potentially advantaging secondary metal producers in low-carbon markets.

- Incentive structures for private sector investment in recycling infrastructure remain insufficient relative to the scale of material flows that circular systems need to capture.

The next major ASX story will hit our subscribers first

What Are the Economic Benefits and Business Case for Circular Metal Supply Chains?

Value Retention Economics: Keeping High-Value Metals Productive

The cost differential between secondary and primary metal production for key commodities presents a compelling economic argument independent of environmental or regulatory considerations. Secondary aluminium production's 95 percent energy saving over primary smelting translates into a structural cost advantage that makes recycled aluminium economically competitive across a wide range of commodity price environments.

Beyond unit economics, circular supply chains provide a meaningful buffer against commodity price volatility. Companies with established closed-loop scrap integration programmes maintain partial insulation from spot market price spikes, because they can source a proportion of their metal requirement from internally recovered material at predictable processing costs rather than market rates.

Competitive Advantages for Early Adopters

The commercial incentives for early adoption of circular supply chain principles are compounding across multiple dimensions:

- Reduced raw material procurement costs through closed-loop scrap integration and secondary feedstock development.

- ESG performance improvements that lower financing costs and improve access to sustainability-linked debt instruments.

- OEM supply chain sustainability mandates are progressively requiring upstream suppliers to demonstrate recycled content and carbon footprint credentials, making circular capability a market access prerequisite.

- Brand differentiation and regulatory risk mitigation function as compounding commercial incentives that strengthen over time as policy frameworks tighten.

"Companies integrating circular supply chain principles now are not simply managing environmental risk. They are building secondary material flows as proprietary competitive assets in a market where critical mineral security will be increasingly contested."

What Are the Key Challenges Limiting Circular Economy Adoption in Metal Supply Chains?

Technical Barriers

Several genuine technical constraints limit the pace of adoption in the circular economy in metal supply chains:

- Contamination and alloy complexity in post-consumer scrap remain a persistent quality challenge, restricting application range for recovered material.

- The energy intensity of certain recycling processes relative to primary production varies significantly by metal, with some critical mineral recovery pathways currently more energy-intensive than virgin production at scale.

- Emerging recovery technologies for battery materials and electronic waste remain at limited commercial volumes, with scaling challenges related to feedstock consistency and product quality certification.

Economic and Market Barriers

- Price competition between virgin and secondary materials during periods of low commodity prices can erode the economic rationale for recycling investment.

- Fragmented scrap collection markets and the absence of standardised quality grading systems reduce market transparency and increase transaction costs.

- Total investment in global recycling infrastructure remains insufficient relative to the scale of material flows that an energy transition-aligned circular economy would require.

Systemic Limitations: Why Recycling Alone Cannot Close the Loop

A critical but frequently understated reality is that recycled content cannot mathematically substitute for primary production given current demand growth trajectories. As noted by the International Council on Mining and Metals, circular strategies must complement rather than replace responsible primary mining — both streams are necessary, and framing them as substitutes misrepresents the supply challenge.

The material balance arithmetic is straightforward: when global lithium demand is projected to increase by more than 40 times by 2040, a recycling system capturing 90 percent of existing stock still operates on a base that is orders of magnitude smaller than what new demand trajectories require.

Cross-Industry Collaboration: Who Needs to Work Together to Close the Loop?

The Ecosystem Required for Systemic Circularity

No single actor in the value chain can close material loops unilaterally. Systemic circularity in metal supply chains requires coordinated action across the following ecosystem participants:

- Metal producers, responsible for designing primary material characteristics that support secondary recovery compatibility.

- Manufacturers and OEMs, embedding circularity requirements into procurement specifications and product design standards.

- Waste management and recycling operators, providing the logistics and processing backbone through which material recovery is physically executed.

- Research institutions and technology developers, advancing sorting, hydrometallurgical recovery, bioleaching, and traceability capabilities toward commercial viability.

- Policymakers and regulators, constructing the market conditions and incentive structures that make circularity economically rational for private sector participants.

Collaborative Models in Practice

Industry consortia are emerging as a practical mechanism for competitors to collaborate on pre-competitive circularity challenges without compromising commercial positioning. Public-private investment vehicles for recycling infrastructure development are addressing the capital deployment gap that market mechanisms alone have not resolved. Knowledge-sharing frameworks for advancing Design for Circularity standards across sectors reduce duplication of effort and accelerate the diffusion of best practices from early-adopting industries to sectors where circular adoption remains nascent.

Frequently Asked Questions: Circular Economy in Metal Supply Chains

What is the circular economy in the context of metal supply chains?

It refers to a systemic approach where metals are retained in productive use through design for longevity, component reuse, remanufacturing, and closed-loop recycling, replacing the linear extraction-use-disposal model with one where material value is preserved across multiple cycles.

Which metals are most compatible with circular supply chain models?

Steel and aluminium are currently the most widely recycled metals at industrial scale, supported by established secondary markets and well-developed collection infrastructure. Copper, nickel, and cobalt are increasingly targeted for circular recovery given their critical importance to energy transition technologies and the high concentrations available in urban mine feedstocks.

Can recycled metals fully replace primary mining?

No. While high recycling rates meaningfully reduce primary demand, the projected scale of global metal consumption growth driven by electrification and clean energy infrastructure means primary production remains essential. Circular strategies reduce the primary supply requirement but cannot eliminate it given current demand trajectories.

What technologies are most important for advancing circular metal supply chains?

AI-powered sorting systems, digital product passports, blockchain traceability, hydrometallurgical processing, bioleaching, and IoT-enabled material flow monitoring represent the most impactful enabling technologies currently being deployed or scaled across the sector.

How do regulatory frameworks support circular metal supply chains?

Frameworks including the EU Circular Economy Action Plan and the Critical Raw Materials Act establish mandatory recycled content targets, extended producer responsibility obligations, and digital traceability requirements that create compliance-driven demand for certified secondary materials and structured market incentives for circular infrastructure investment.

The Strategic Horizon: Where Are Circular Metal Supply Chains Headed?

Emerging Trends Reshaping the Circular Metals Landscape

Several converging developments are accelerating the pace of circular transformation across metal supply chains:

- AI and predictive analytics are improving material recovery yields by optimising scrap routing decisions and predicting feedstock composition variability.

- The convergence of circular economy principles with net-zero industrial decarbonisation strategies is strengthening the business case for secondary metal production in regulated markets.

- Battery-grade secondary material markets are emerging as a distinct and high-value segment as lithium-ion battery end-of-life volumes begin to scale materially.

- Digital twin applications are being deployed in recycling facility design and operational optimisation, enabling operators to model process configurations and identify efficiency improvements before committing capital to physical changes.

The Long-Term Vision: A Fully Integrated Circular Metals Economy

The long-term architecture of a fully circular metal economy rests on several interdependent foundations. Material passports, standardised and globally interoperable, provide the data infrastructure through which secondary materials can be verified, priced, and traded across jurisdictions without the classification ambiguity that currently fragments international secondary material flows.

Service-based industrial models, where material ownership never formally transfers from producer to customer, enable perpetual recovery by maintaining continuous manufacturer accountability throughout the product lifecycle. Urban mining matures from a niche recovery activity into a mainstream industrial sector with dedicated capital investment, specialised processing infrastructure, and professional workforce development.

The strategic outcome for jurisdictions that invest seriously in circular metal supply chain infrastructure is meaningful improvement in critical mineral security without proportional increases in primary extraction. For industries navigating a tightening critical mineral market while facing escalating environmental and regulatory obligations, that combination represents one of the most substantive competitive advantages available in the decade ahead.

This article incorporates statistical data from the International Energy Agency, the International Council on Mining and Metals, the International Aluminium Institute, and published academic research. All projections and forward-looking estimates involve uncertainty and should not be treated as definitive forecasts. Readers are encouraged to consult primary source materials directly for investment or operational decision-making purposes.

Want to Track ASX Mineral Discoveries Before the Broader Market Does?

As the circular economy reshapes critical mineral demand and primary ore grades continue their structural decline, identifying significant new discoveries early has never been more consequential. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on major ASX mineral discoveries — instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore historic discovery returns to understand the scale of opportunity, and begin your 14-day free trial today to position yourself ahead of the market.