June 17, 2026

The narrow waterway between Iran and the Arabian Peninsula represents the single most important energy transit route in the global economy, making the closure of the Strait of Hormuz a scenario that would trigger unprecedented global economic disruption. Recent analysis indicates that approximately 20 percent of global oil and liquefied natural gas trade passes through this strategic corridor, making any disruption immediately consequential for worldwide energy markets and creating cascading effects that would reveal how deeply interconnected modern economies have become.

What Makes the Strait of Hormuz the World's Most Critical Energy Chokepoint?

The narrow waterway between Iran and the Arabian Peninsula represents the single most important energy transit route in the global economy. Recent analysis indicates that approximately 20 percent of global oil and liquefied natural gas trade passes through this strategic corridor, making any disruption immediately consequential for worldwide energy markets.

Geographic Vulnerability and Strategic Control

Iran's territorial control over the northern coastline provides significant leverage over maritime traffic passing through these waters. The country's ability to influence shipping operations stems from both legal maritime authority and practical enforcement capabilities. This geographic advantage allows Iran to effectively control one of the world's most critical economic lifelines.

The physical constraints of the waterway create natural bottlenecks that amplify vulnerability. Vessel traffic must navigate through relatively confined waters where interdiction becomes operationally feasible, unlike broader oceanic shipping lanes where maritime control proves more challenging.

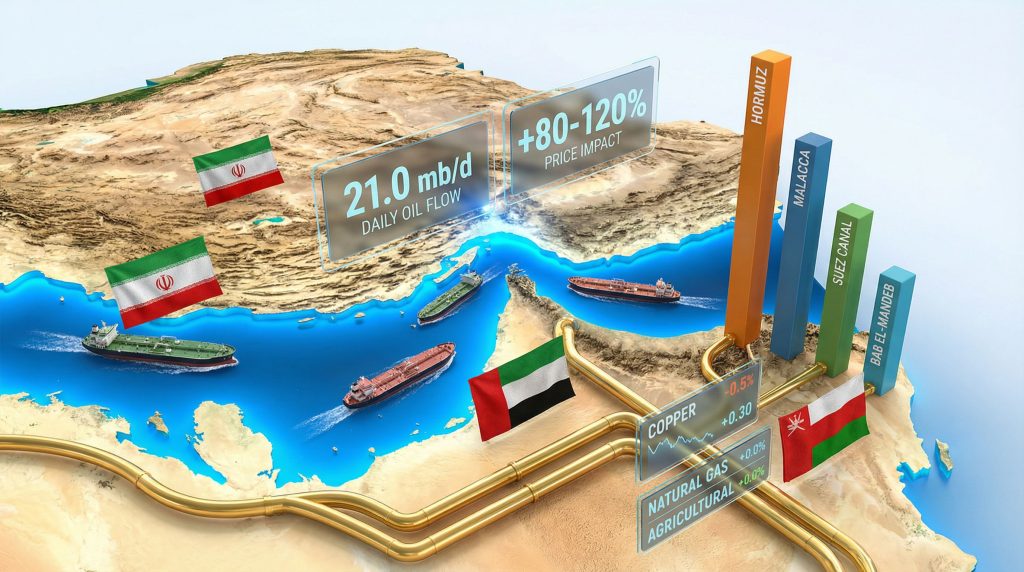

Daily Energy Flow Statistics and Global Dependencies

Current energy flow through this chokepoint demonstrates the magnitude of global dependency. In a complete closure of the Strait of Hormuz scenario, analysis suggests a supply deficit of 17.5 million barrels per day would emerge, representing a shortfall that existing alternative infrastructure cannot adequately compensate.

| Chokepoint | Daily Oil Flow (mb/d) | Alternative Routes | Closure Risk Level |

|---|---|---|---|

| Strait of Hormuz | 21.0 | Limited pipeline capacity | Extreme |

| Strait of Malacca | 16.0 | Longer shipping routes | Moderate |

| Suez Canal | 5.5 | Cape of Good Hope | Low-Medium |

| Bab el-Mandeb | 6.2 | Cape of Good Hope | Medium |

Iran's Territorial Advantage and Maritime Control Mechanisms

Iran's strategic position allows for multiple levels of maritime interdiction, ranging from diplomatic pressure to physical obstruction of shipping lanes. The country's naval capabilities, combined with coastal missile systems and patrol vessels, create a comprehensive enforcement mechanism that can escalate from warning signals to active interference with commercial vessels.

This control extends beyond military assets to include regulatory authority over vessel inspections, navigation requirements, and safety protocols that can significantly slow or halt maritime traffic even without overt military action.

When big ASX news breaks, our subscribers know first

How Would a Complete Strait Closure Impact Global Oil Markets?

A complete closure of the Strait of Hormuz would trigger immediate and severe disruptions across global energy markets, with price volatility beginning within hours of confirmed closure. Historical precedent from early 2026 demonstrates this sensitivity, when closure threats drove oil prices to $120 per barrel during initial panic selling, before partially stabilising around $100 per barrel following political intervention attempts.

Immediate Price Shock Scenarios and Market Volatility

Market psychology plays a crucial role in amplifying price movements during supply disruption scenarios. The March 2026 example revealed how quickly sentiment can shift between panic and cautious optimism based on political statements rather than fundamental supply changes. However, continued military escalation demonstrated that sentiment-based stabilisation proves transitory when underlying geopolitical conditions continue deteriorating.

The transition from efficiency-optimised to scarcity-driven pricing creates a new market regime where traditional price elasticity assumptions break down. Furthermore, oil market disruption scenarios show that energy consumers face limited substitution options in the short term, reducing demand responsiveness to higher prices and amplifying price volatility.

Strategic Petroleum Reserve Deployment Limitations

Government strategic reserves provide 60-90 days of cushioning for major economies, but this buffer represents a finite resource with limited market impact duration. Analysis suggests that announced strategic reserve drawdowns produce minimal sustained price effects because the underlying supply deficit remains unresolved.

Reserve deployment also faces logistical constraints, as stored oil must be transported from storage facilities to refineries and distribution networks. This process requires weeks to months for full implementation, during which time supply shortages can manifest in operational disruptions rather than just price signals.

Alternative Pipeline Capacity vs Maritime Volume Gaps

Existing pipeline infrastructure, including Saudi Arabia's East-West Pipeline (Petroline), provides only 15-20% coverage of normal Strait volumes. This capacity limitation means that even maximum utilisation of alternative routes leaves an insurmountable supply gap that requires 18-24 months of new infrastructure development to address.

The pipeline alternative also faces capacity bottlenecks at loading terminals and receiving facilities that were not designed to handle dramatically increased throughput. These infrastructure constraints compound the supply deficit beyond the simple pipeline capacity calculations.

Which Industries Face the Greatest Supply Chain Disruption Risk?

Beyond direct energy sector impacts, the closure of the Strait of Hormuz creates cascading disruptions across multiple industrial sectors through interconnected supply chain dependencies. Early-phase disruption escalates from maritime logistics failures into chemical and mining industry bottlenecks, with secondary effects following as shipping and energy constraints cascade through manufacturing supply chains.

Petrochemical Manufacturing and Chemical Feedstock Dependencies

The loss of sour crude oil creates a critical sulphur deficit that disrupts sulphuric acid production processes. This disruption specifically impacts copper and cobalt extraction operations in Africa and Chile, where sulphuric acid serves as an essential input for ore processing. The resulting shortage of industrial metals then affects downstream manufacturing across multiple sectors.

Chemical manufacturing facilities dependent on Middle Eastern feedstocks face immediate production constraints, particularly those producing speciality chemicals that require specific crude oil compositions. These facilities often cannot quickly substitute alternative feedstock sources without significant process modifications and quality control adjustments.

Semiconductor Production Vulnerabilities in Asia-Pacific

Taiwan's heavy dependence on LNG imports for power generation creates immediate vulnerability for semiconductor manufacturing operations. Reports from March 2026 indicated initial power rationing implementation with risks of TSMC factory shutdowns and wafer production failures.

The semiconductor industry's geographic concentration in Asia-Pacific regions with high LNG dependency amplifies systemic risk. Power-intensive manufacturing processes cannot easily reduce consumption without compromising production quality, making these facilities particularly vulnerable to energy supply disruptions.

Mining Operations Dependent on Sulphuric Acid Supplies

Mining operations, particularly copper and cobalt extraction facilities, depend on consistent sulphuric acid supplies for ore processing. The disruption of sour crude oil supplies eliminates a major source of sulphur for acid production, creating bottlenecks that cannot be quickly resolved through alternative sourcing.

This creates a compound supply chain crisis where energy supply disruption leads to chemical input shortages, which then constrain mining output of metals essential for renewable energy infrastructure, electric vehicles, and industrial equipment manufacturing. Additionally, concerns over critical minerals energy security become paramount during such disruptions.

What Are the Cascading Effects on Global Financial Markets?

Financial market impacts extend far beyond energy sector equity performance to encompass currency pressures, credit market stress, and inflation transmission across multiple economies. The disruption creates synchronised policy challenges requiring central bank intervention across developed and emerging markets simultaneously.

Currency Devaluation Patterns in Oil-Importing Nations

Oil-importing economies face immediate current account pressures as energy import costs surge whilst export revenues remain stable. This dynamic creates downward pressure on currencies, particularly in emerging markets with limited foreign exchange reserves relative to energy import requirements.

Foreign exchange reserves in emerging markets come under stress as governments attempt to stabilise domestic fuel prices through subsidies whilst maintaining currency stability. This dual pressure often proves unsustainable, forcing policy makers to choose between currency defence and domestic energy price stability.

Inflation Transmission Mechanisms Across Sectors

A sustained closure creates a 3-4x multiplier effect where initial energy price increases trigger secondary inflation in transportation, manufacturing, and food production, ultimately requiring central bank intervention across multiple economies simultaneously.

Energy price increases propagate through the economy via transportation costs, affecting goods distribution and logistics networks. Manufacturing sectors face both direct energy cost increases and indirect pressures from higher material and transportation expenses, creating broad-based inflationary pressures that extend beyond energy-intensive industries.

This inflationary environment often coincides with gold prices record highs as investors seek hedges against currency debasement and economic uncertainty.

Credit Market Stress and Emerging Market Debt Pressures

Credit spreads expand significantly across multiple debt categories as investors reassess default risks in an environment of higher energy costs and economic stress. Emerging market sovereign debt faces particular pressure as governments confront higher import costs whilst dealing with currency depreciation and reduced fiscal flexibility.

Corporate debt markets experience differentiated impacts based on energy intensity and geographic exposure. Companies with significant Middle Eastern operations or high energy consumption face immediate credit quality deterioration, whilst firms with pricing power or energy-efficient operations may maintain more stable credit profiles.

How Do Regional Powers Respond to Energy Security Threats?

Regional responses to energy supply threats reveal the limitations of existing emergency protocols and highlight the inadequacy of current strategic reserve systems. Major energy-importing nations face difficult choices between market intervention and reserve conservation, whilst energy-exporting countries outside the affected region gain significant leverage.

Strategic Reserve Utilisation and Emergency Protocols

Government intervention through strategic petroleum reserve releases provides psychological market support but limited fundamental supply relief. The March 2026 experience demonstrated that reserve deployment announcements create temporary price moderation, but markets quickly refocus on underlying supply fundamentals when closure threats persist.

Coordination between major reserve-holding nations becomes essential but politically complex. Different countries face varying exposure levels to supply disruption, creating misaligned incentives for reserve deployment timing and volumes.

Alternative Energy Source Acceleration Programmes

Energy security threats accelerate existing renewable energy investment programmes, but these initiatives require years for meaningful capacity additions. Short-term alternatives focus on maximising utilisation of existing non-Middle Eastern energy sources, including increased nuclear plant utilisation and coal facility reactivation despite environmental concerns.

Emergency energy sourcing often involves politically sensitive arrangements with countries previously subject to sanctions or trade restrictions. In addition, the US natural gas outlook becomes increasingly important as alternative supply scenarios are evaluated.

Military Escort Operations and Maritime Security Costs

Naval protection for commercial shipping creates significant cost increases for maritime transport, with insurance premiums and charter rates experiencing dramatic escalation. War risk premiums can increase vessel operating costs by 100-300%, adding substantial expense to any goods requiring maritime transport.

Military escort operations require international coordination and burden-sharing arrangements that prove politically complex during active conflicts. The logistics of protecting commercial vessels whilst avoiding military escalation creates operational constraints that limit the effectiveness of maritime security measures.

What Long-Term Structural Changes Could Emerge?

Sustained energy supply disruption accelerates structural economic changes that persist beyond crisis resolution. These shifts include energy infrastructure diversification, supply chain regionalisation, and fundamental changes in international trade patterns that reshape global economic geography.

Accelerated Energy Transition Investment Patterns

Energy security concerns drive increased investment in domestic renewable energy capacity, energy storage systems, and alternative fuel infrastructure. These investments often receive expedited permitting and enhanced government support, accelerating deployment timelines that would otherwise require decades.

The crisis creates political consensus for energy independence initiatives that face reduced opposition during periods of supply vulnerability. Long-term infrastructure projects gain approval and funding that might not otherwise achieve political support during stable energy market conditions.

Supply Chain Regionalisation and Deglobalisation Trends

Companies reassess global supply chain strategies, prioritising supply security over cost optimisation. This shift toward regionalisation reduces efficiency but improves resilience against geographic disruptions, fundamentally altering the risk-return calculations that drove globalisation over previous decades.

Manufacturing capacity relocates closer to end markets, reducing dependence on long-distance shipping through vulnerable chokepoints. This trend reverses decades of specialisation and geographic optimisation, with significant implications for global trade volumes and patterns.

New Maritime Route Development and Infrastructure Investment

Alternative shipping routes receive enhanced investment and development priority, including Arctic passages, overland rail connections, and expanded pipeline networks. These infrastructure projects often involve significant government funding and international cooperation arrangements.

Port infrastructure development accelerates in regions that can serve as alternative routing hubs, creating new geographic centres for global trade. Investment in port capacity, storage facilities, and transportation connections reshapes maritime logistics networks over multi-year timeframes.

The next major ASX story will hit our subscribers first

Which Commodities Beyond Oil Experience Price Volatility?

Energy supply disruption creates price volatility across multiple commodity categories through direct energy content, transportation dependencies, and industrial input requirements. The interconnected nature of commodity production means that oil supply disruption cascades through agricultural, metals, and manufactured goods markets.

Natural Gas and LNG Market Disruptions

LNG markets experience immediate disruption as Asian importers compete for alternative supplies outside the Middle Eastern region. Shipping constraints compound supply limitations, as LNG carriers require specialised terminals and cannot easily substitute for pipeline gas in many applications.

Natural gas price volatility affects electricity generation costs, industrial heating applications, and petrochemical feedstock supplies. Regions heavily dependent on gas-fired power generation face immediate electricity price increases that propagate through all economic sectors.

| Commodity | Direct Impact | Indirect Impact | Recovery Timeline |

|---|---|---|---|

| Crude Oil | +80-120% | Transportation costs | 6-12 months |

| Natural Gas | +60-90% | Heating/power generation | 4-8 months |

| Copper | +15-25% | Mining operation costs | 3-6 months |

| Agricultural Products | +20-40% | Fertiliser/transport costs | 12-18 months |

Industrial Metals Supply Chain Bottlenecks

Copper and cobalt extraction face immediate constraints due to sulphuric acid supply disruption, creating shortages in metals essential for electrical infrastructure and renewable energy systems. Mining operations cannot quickly substitute alternative acid sources without significant process modifications and quality impacts.

Other industrial metals experience indirect pressure through higher energy costs for extraction, processing, and transportation. Energy-intensive metals like aluminium and steel face particular pressure as production costs increase substantially with higher energy prices.

Agricultural Commodity Price Transmission Effects

Fertiliser production disruption creates immediate cost pressures for agricultural producers, with nitrogen, phosphate, and potash prices increasing significantly. These input cost increases translate into higher food prices with a lag time of one to two growing seasons, depending on crop cycles and inventory levels.

Transportation cost increases affect agricultural commodity distribution, with bulk commodities like grains experiencing significant shipping cost inflation. Refrigerated transport for perishable goods faces even higher cost pressures due to energy-intensive cooling requirements.

How Do Insurance and Shipping Markets Adapt to Crisis Conditions?

Maritime insurance markets experience dramatic repricing as war risks and cargo losses increase substantially. Shipping companies face difficult decisions between route alternatives, insurance coverage levels, and cargo selectivity as operating economics deteriorate rapidly.

War Risk Premium Calculations and Coverage Limitations

Marine insurance premiums increase by multiples rather than increments, with war risk coverage potentially becoming unavailable for certain shipping routes or cargo types. Insurance companies may require government backing or specialised coverage arrangements for vessels transiting high-risk areas.

Coverage limitations expand beyond traditional exclusions to encompass broader conflict-related risks, cargo delays, and port access restrictions. Shippers face increased liability exposure as standard insurance coverage proves inadequate for crisis-level disruptions.

Alternative Routing Costs and Time Penalties

Shipping companies must choose between higher-risk direct routes with elevated insurance costs versus longer alternative routes with increased fuel consumption and time delays. The Cape of Good Hope routing adds approximately 15-20 days to Asia-Europe shipping times whilst substantially increasing fuel costs.

Port congestion increases at alternative routing terminals as vessel traffic redirects to avoid conflict zones. This congestion creates additional delays and demurrage costs that compound the direct routing expenses.

Vessel Availability and Charter Rate Explosions

Available vessel capacity decreases as ships avoid high-risk areas and alternative routing requires longer voyage times. This capacity reduction drives charter rates significantly higher across all vessel categories, not just those serving Middle Eastern routes.

Specialised vessel types like LNG carriers and oil tankers face particular availability constraints as owners become selective about voyage acceptance and routing. Long-term charter agreements may include force majeure provisions that allow owners to avoid high-risk deployments.

What Economic Modelling Reveals About Recovery Scenarios?

Economic recovery from sustained energy supply disruption depends heavily on conflict resolution timing and the extent of infrastructure damage during the closure period. Multiple recovery scenarios require different policy responses and create varying timelines for economic normalisation.

Best-Case Resolution Timeline and Market Normalisation

Optimistic scenarios assume conflict resolution within 3-6 months with minimal infrastructure damage and rapid resumption of shipping traffic. Even under these conditions, market normalisation requires additional months as supply chains rebuild inventory buffers and shipping schedules normalise.

Financial market recovery typically precedes physical market normalisation as traders anticipate supply restoration. However, risk premiums remain elevated for extended periods as market participants reassess the reliability of Middle Eastern supply sources.

Prolonged Conflict Economic Damage Assessment

Extended closure scenarios lasting 12-18 months create permanent changes to global economic structure as alternative supply sources and trade routes achieve established market positions. Recovery becomes more complex as temporary adjustments transform into permanent structural changes.

Economic damage from prolonged disruption includes permanent demand destruction in energy-intensive industries, accelerated automation to reduce energy dependence, and geographic relocation of manufacturing capacity to reduce vulnerability to supply disruption. These changes align with global market recession insights regarding fundamental economic restructuring.

Permanent Geopolitical Realignment Implications

Long-term disruption accelerates the development of alternative international monetary and trade systems that bypass traditional Western-controlled financial infrastructure. Energy trade increasingly occurs through bilateral arrangements and alternative currencies, reducing the dominance of dollar-based energy markets.

The crisis could catalyse the emergence of a multipolar energy system where regional powers develop independent supply chains and payment mechanisms, fundamentally altering global economic integration patterns that have prevailed for decades. According to the Guardian's analysis, such geopolitical shifts could reshape international relations permanently.

Q: How long can global oil markets function with Strait closure?

Strategic reserves provide 60-90 days of cushioning for major economies, but price volatility begins immediately and supply shortages emerge within 30-45 days without alternative sources.

Q: Which countries are most vulnerable to Strait disruption?

Japan, South Korea, China, and India face the highest vulnerability due to heavy reliance on Gulf oil imports, with limited alternative supply routes and insufficient strategic reserves.

Q: Can pipeline alternatives fully replace maritime transport?

Existing pipeline capacity covers only 15-20% of normal Strait volumes, creating an insurmountable supply gap that requires 18-24 months of new infrastructure development.

Investment Implications and Portfolio Protection Strategies

Energy supply disruption fundamentally alters investment risk-return calculations across multiple asset classes. Traditional portfolio diversification strategies prove inadequate when supply chain interdependencies create correlated failures across seemingly unrelated sectors and geographic regions.

Energy Sector Equity Performance During Supply Shocks

Energy companies outside the Middle Eastern region benefit from higher commodity prices and reduced competition from affected suppliers. However, companies with significant Middle Eastern operations or supply chain dependencies face operational disruption that can offset price benefits.

Renewable energy infrastructure companies experience accelerated demand growth as energy security concerns drive increased investment in domestic energy sources. Battery storage, solar, and wind power equipment manufacturers face both opportunity from increased demand and challenges from supply chain disruption affecting component sourcing.

Safe Haven Asset Allocation and Currency Hedging

Traditional safe haven assets like government bonds face complex dynamics as energy-driven inflation creates pressure for interest rate increases whilst economic disruption supports flight-to-quality demand. Gold and precious metals typically benefit from both inflation hedging demand and currency debasement concerns.

Currency hedging becomes essential for international portfolios as energy-importing countries face currency depreciation whilst energy-exporting nations experience appreciation. The US dollar often strengthens during global crises, creating additional pressure on emerging market assets and commodity-dependent economies.

Infrastructure Investment Opportunities in Alternative Routes

Infrastructure projects that reduce dependence on Middle Eastern energy sources attract enhanced investment interest and government support. Pipeline projects, renewable energy installations, and alternative transportation routes receive priority treatment and expedited development timelines.

Port and logistics infrastructure in alternative routing locations experience increased investment and development activity. Companies positioned to benefit from supply chain regionalisation and trade route diversification represent potential long-term investment opportunities beyond the immediate crisis period.

Moreover, Oxford Energy's research indicates that infrastructure investments in alternative energy routes could fundamentally reshape global energy markets for decades.

Disclaimer: This analysis is based on publicly available information and industry reports. Commodity and financial market investments carry substantial risk, including potential loss of principal. Past performance does not guarantee future results. Readers should conduct independent research and consult qualified financial advisers before making investment decisions. The scenarios discussed represent potential outcomes that may not materialise, and actual events may differ significantly from projections presented.

Could Energy Market Disruptions Reveal the Next Major Investment Opportunity?

The global interconnectedness revealed by energy supply vulnerabilities highlights the critical importance of staying ahead of market-moving events, particularly in resource-dependent sectors. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, enabling investors to identify actionable opportunities precisely when resource security becomes paramount and alternative supply sources gain strategic importance.