June 5, 2026

When a Single Mine Stoppage Reveals a System Under Strain

The global copper market has entered a period where the distance between adequate supply and structural deficit has narrowed to an uncomfortable margin. Decades of underinvestment in new mine development, steadily declining ore grades at legacy operations, and a demand curve reshaped by electrification have collectively produced a market environment where disruption at even a single tier-one asset carries consequences that ripple far beyond its immediate geography. It is within this context that the June 2026 CMOC Congo copper mine strike demands serious examination, not merely as an industrial relations incident, but as a revealing window into the structural fragilities embedded within one of the world's most important mineral supply corridors.

The DRC's emergence as the world's second-largest copper producer has been among the most consequential developments in global commodities over the past decade. That ascent was built almost entirely on a foundation of Chinese capital, Chinese technology, and Chinese operational management, with CMOC occupying the commanding heights of that investment wave. Yet the very speed and scale of that transformation has outpaced the development of the governance frameworks, labour relations infrastructure, and stakeholder engagement mechanisms needed to sustain it without recurring disruption.

The TFM strike of June 2026 is the most recent manifestation of that gap, and understanding it requires examining the mine's market position, the anatomy of the dispute, its historical precedents, and its implications across market, geopolitical, and ESG dimensions simultaneously.

When big ASX news breaks, our subscribers know first

The Scale That Makes TFM Impossible to Ignore

Production Figures That Define Market Significance

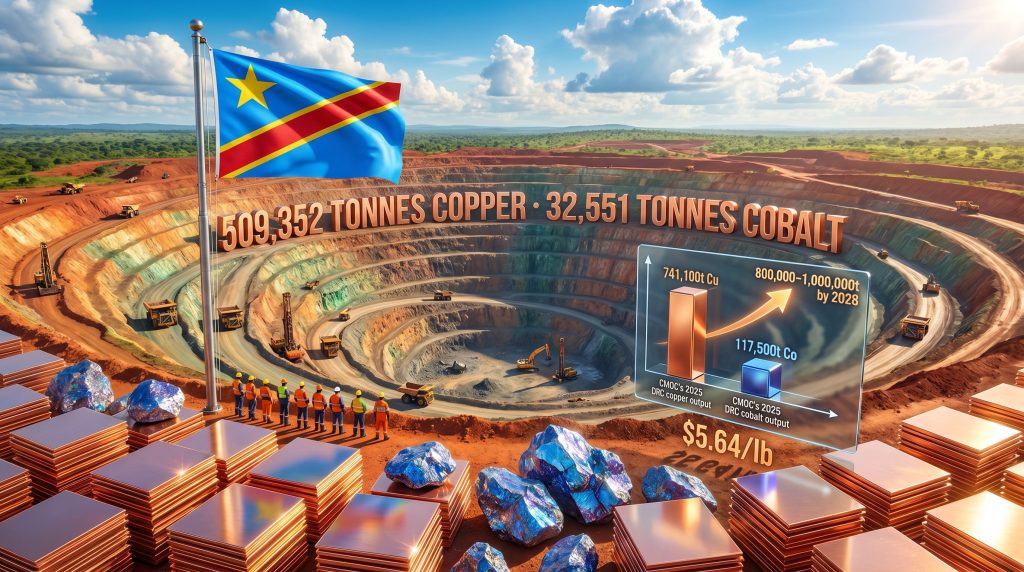

Tenke Fungurume Mining's output statistics belong in a category shared by very few mining operations anywhere in the world. The mine produced approximately 519,000 tonnes of copper in 2025, a figure that represents roughly 15% of the DRC's entire national copper output for that year, according to reporting by Bloomberg News. When assessed against global copper production benchmarks, TFM's annual output places it firmly among the top tier of copper-producing assets worldwide, a status that transforms any operational disruption from a local labour story into a globally relevant supply chain event.

The cobalt dimension adds another layer of strategic weight. TFM is not merely a copper mine that produces cobalt as an incidental byproduct; it is one of the world's premier cobalt-producing assets, generating output volumes that matter materially to battery supply chains for electric vehicles and grid storage systems. When considered alongside CMOC's second Congolese operation, the Kisanfu mine (KFM), the company's combined DRC footprint extracted nearly 750,000 tonnes of copper in 2025 from these two assets alone, alongside substantial cobalt volumes that position CMOC as a dominant supplier of both metals to global industrial markets.

To appreciate why these numbers carry the weight they do, consider the market environment surrounding them. Copper was trading near $5.64 per pound at the time of the strike, close to historical highs, reflecting a structural tightening that has been building for years as electrification demand has accelerated faster than new mine supply has materialised. The DRC's copper output has been a primary force preventing a more severe copper supply crunch from developing, and TFM sits at the centre of that output story.

CMOC's DRC Ambitions and the Stakes Involved

CMOC has publicly committed to growing its DRC copper output to between 800,000 and 1 million tonnes per year by 2028, a target that underscores just how central these Congolese assets are to the company's long-term strategic positioning. Achieving that target requires not just capital investment in extraction and processing infrastructure, but sustained, uninterrupted operational continuity at both TFM and KFM across a multi-year horizon.

Furthermore, labour disputes that idle equipment, block access roads, or trigger dismissal proceedings for experienced workers represent direct threats to that expansion trajectory, regardless of how quickly individual incidents are resolved. CMOC has committed to invest over $1 billion to expand the TFM operation, making the stakes of repeated disruption even more significant for the company's overall capital programme.

The following table summarises the operational and ownership structure of CMOC's DRC footprint:

| Asset | CMOC Ownership Stake | 2025 Output (Copper) | Key Co-Products |

|---|---|---|---|

| Tenke Fungurume Mining (TFM) | 80% | ~519,000 tonnes | Cobalt |

| Kisanfu Mining (KFM) | 71.25% | Significant additional volume | Cobalt |

| Combined DRC Operations | Various | ~750,000 tonnes | Cobalt (world top-tier) |

| 2028 Production Target | N/A | 800,000–1,000,000 tonnes | Cobalt |

The gap between current combined output and the 2028 target is substantial, representing a ramp-up of between 7% and 33% from 2025 levels. Delivering that growth while simultaneously managing complex stakeholder relationships in one of the world's most politically challenging mining jurisdictions is an operational challenge of considerable difficulty.

Anatomy of the June 2026 Strike at TFM

What Workers Actually Objected To

The CMOC Congo copper mine strike that began on June 1, 2026, did not emerge from a sudden flashpoint or an unexpected operational event. It was the product of accumulated grievances crystallised around a specific process failure: the negotiation of a new collective bargaining agreement (CBA) that workers believed had been conducted without meaningful participation from the workforce it was meant to govern.

According to reporting by Radio Okapi, the United Nations-backed news organisation that covers the DRC, workers protested that the CBA had been negotiated between TFM management and a designated union delegation, with the broader workforce excluded from the discussions that shaped the agreement's terms. The objection was not purely to the content of the agreement, though workers also raised substantive concerns about pay, housing allowances, and healthcare access. The more fundamental complaint was procedural: that a governance mechanism intended to represent workers had functioned instead as a management-facilitated channel that bypassed authentic worker input.

The specific demands workers advanced during the strike included:

- Improved base wages and overtime compensation structures

- Formal housing allowance provisions as part of the compensation package

- Enhanced access to healthcare benefits for workers and their dependants

- Greater and more transparent worker participation in future collective bargaining processes

These demands are not unusual within the context of large-scale mining operations in southern and central Africa, where labour relations frameworks have historically lagged behind operational growth. What makes the TFM situation distinctive is the scale of the operation involved and the degree to which the mine's output matters to global supply chains.

Management's Response: Incentives and Ultimatums

TFM's response to the strike combined financial incentives with explicit threats of disciplinary action in a manner that resolved the immediate disruption but raised questions about whether the underlying conditions had been addressed. According to a letter sent by TFM to its employees and contractors, which was reviewed by Bloomberg News, the company characterised the strike as illegal and acknowledged significant operational disruption and production interference.

The financial response differentiated between workers based on their participation in the strike action:

- Workers who did not participate in the strike received a $500 loyalty bonus

- Workers who reportedly resisted pressure to join the strike received $1,000, described as recognition of their demonstrated commitment under pressure

TFM set a deadline of Wednesday evening (approximately June 4, 2026) for striking workers to return to their posts, with the company indicating that those who returned by the deadline would face no disciplinary action, while those who did not comply would be subject to immediate dismissal proceedings. TFM subsequently confirmed that striking workers had resumed work and that operations had returned to normal conditions. Additionally, labour unrest at TFM has prompted an internal investigation to identify workers responsible for alleged aggression against colleagues and damage to company equipment, with findings to be referred to Congolese authorities.

The combination of financial rewards for non-participation and dismissal threats for continued action represents a dual-pressure resolution mechanism that addresses the symptom of industrial action without resolving the governance deficit that produced it.

The timeline of events during the strike period:

| Date | Key Development |

|---|---|

| June 1, 2026 | Strike action commences at TFM |

| Early June 2026 | Equipment idled; operational disruption acknowledged by management |

| ~June 4, 2026 | TFM deadline issued for workers to return to posts |

| Post-deadline | Workers resume duties; operations return to normal |

| Ongoing | Internal investigation into equipment damage and alleged worker aggression initiated |

Recurring Instability: This Was Not TFM's First Disruption

The 2022 Export Suspension and What It Established

The June 2026 CMOC Congo copper mine strike is best understood not as an isolated event but as the most recent episode in a pattern of operational disruption at TFM that stretches back several years. In 2022, TFM experienced an extended export suspension arising from a dispute involving a government-appointed administrator and the state mining company Gécamines. That earlier incident halted shipments for a prolonged period, revealing the same fundamental reality: TFM operates in an environment where multiple vectors of risk can interrupt production in ways that are difficult to anticipate through conventional operational planning.

The 2022 episode demonstrated that the DRC's regulatory and political environment creates genuine sovereign risk exposure for foreign-operated mining assets, even those as large and strategically important as TFM. The involvement of Gécamines, the state mining entity that retains partial ownership interests across many DRC mining operations, illustrated how quickly government-company disputes can escalate to the point of halting exports entirely. For investors and supply chain planners, that episode established a precedent that has not been forgotten.

The recurrence of significant disruption in 2026, this time originating from labour relations rather than regulatory conflict, suggests that TFM has not developed the comprehensive stakeholder engagement frameworks needed to prevent recurring interruptions. Two major disruptions within four years at the same asset, driven by different causes but sharing the common thread of inadequate stakeholder management, indicates a systemic pattern rather than a sequence of unrelated incidents.

What Recurring Disruptions Signal to the Market

For institutional investors and supply chain managers with exposure to copper markets, the pattern of disruptions at TFM presents a specific category of risk: the gap between a mining asset's production potential and its actual realised output due to non-geological, non-technical factors. TFM's ore body is world-class by any measure. Its disruption history is not a reflection of geological limitations or processing challenges; it reflects the complexity of operating at massive scale in a jurisdiction with elevated political risk and limited institutional capacity.

This distinction matters for market positioning. A mine disrupted by declining ore grades requires capital solutions. A mine disrupted by labour unrest and regulatory conflict requires governance solutions. The latter are often slower to implement and harder to verify from the outside, making them a persistent source of uncertainty for markets that are otherwise inclined to price TFM's output as reliable baseline supply.

Chinese Investment and Labor Dynamics in the Congo Copper Belt

The Structural Architecture of Chinese Mining Dominance in the DRC

The DRC's transformation into the world's second-largest copper producer is, at its core, a story about Chinese capital allocation and industrial strategy. Chinese mining companies, led by CMOC but including other major players, provided the investment capital, technical expertise, and operational management that unlocked production growth from the DRC's vast copper-cobalt deposits at a scale and pace that Western mining companies had been unable or unwilling to match. However, that transformation has also produced structural asymmetries that shape the labour relations environment in ways that are not always visible from outside the sector.

Considering the broader context of DRC mineral wealth, three structural dynamics define the labour relations context at Chinese-operated mines in the DRC:

- Host government leverage constraints: The DRC's economic dependence on Chinese mining investment limits the government's practical ability to impose labour standards that might deter further Chinese capital deployment, creating a regulatory environment where worker protections may lag behind operational growth.

- Limited worker bargaining power: High unemployment rates across the Congolese Copper Belt and limited alternative employment opportunities for workers with mining-specific skills constrain the leverage that organised labour can exercise in disputes with large mining operators.

- Union structure limitations: The collective bargaining framework at operations like TFM relies on designated union delegations that may not fully represent the breadth and diversity of the workforce's concerns, particularly when those delegations interact primarily with management rather than maintaining genuinely independent relationships with the workers they nominally represent.

These three dynamics do not excuse management practices that workers find inadequate or unfair, but they help explain why labour disputes at Chinese-operated mines in the DRC tend to follow a specific pattern: workers accumulate grievances over an extended period, formal channels prove insufficient to address those grievances, and industrial action eventually becomes the only available mechanism for forcing management attention.

The Geopolitical Layer: DRC Minerals in a Multipolar Resource Competition

The strategic significance of TFM has been dramatically amplified by the geopolitical competition between China and the United States over critical minerals supply chains. The DRC is simultaneously navigating competing overtures from both Washington and Beijing regarding mineral partnership arrangements. Consequently, the metals geopolitics surrounding this competition place Congolese copper and cobalt at the intersection of two of the most consequential dynamics of the current era: the global energy transition and the US-China strategic rivalry.

For Chinese-operated mines like TFM, this geopolitical context creates a specific reputational risk dimension. Labour disputes and governance failures at Chinese mining operations in Africa are increasingly being used in Western policy and media narratives to argue that Chinese critical mineral supply chains carry unacceptable social and governance risks. Whether or not those narratives are entirely fair, they carry real consequences for the DRC's positioning as a minerals supplier to Western markets and for the long-term sustainability of the Chinese-dominated production model that currently prevails in the Congo Copper Belt.

Market and Supply Chain Implications of the TFM Strike

Short-Term Resolution, Long-Term Concern

The June 2026 CMOC Congo copper mine strike was resolved relatively quickly, with workers returning to posts within days of the management deadline and TFM confirming that operations had normalised. In immediate market terms, this rapid resolution limited the supply impact to a manageable level, and copper prices did not experience dramatic disruption specifically attributable to this event. However, the market calculus around TFM disruptions becomes significantly more complex when evaluated across different time horizons.

| Risk Dimension | Short-Term (0–3 Months) | Medium-Term (3–12 Months) | Long-Term (12–24 Months) |

|---|---|---|---|

| Copper supply impact | Marginal; operations normalised quickly | Moderate if unresolved grievances resurface | Significant if disruptions delay 2028 expansion |

| Cobalt supply impact | Limited disruption reported | Noteworthy given TFM's top-tier cobalt position | Material if output growth trajectory is interrupted |

| CMOC production targets | On track post-resolution | At risk if labour relations remain structurally unresolved | Potentially compromised relative to 800,000-1M tonne goal |

| DRC sovereign risk premium | Slightly elevated | Dependent on broader regulatory developments | Reflects trajectory of stakeholder management improvements |

| Market price sensitivity | Muted given rapid resolution | Elevated if next disruption extends longer | High, given copper market structural tightening |

The copper market's near-term tolerance for TFM disruptions reflects a broader market psychology: investors and traders have internalised the DRC's reputation for periodic operational disruption and built a modest risk premium into copper pricing accordingly. However, this tolerance has limits. A disruption of longer duration, or one that coincides with other supply constraints—pipeline delays, weather events at Chilean operations, or processing bottlenecks—could produce a significantly larger market response than the brief June 2026 episode generated. In fact, the global copper supply gap means any extended outage at a mine of TFM's scale would be felt across multiple downstream industries simultaneously.

Understanding the Cobalt Co-Product Dimension

A less commonly examined aspect of TFM disruptions is their potential impact on cobalt supply. The DRC accounts for approximately 70% of global cobalt mine supply, and TFM is one of the country's premier cobalt-producing assets. While copper tends to receive primary attention in discussions of DRC mining disruptions due to its larger market size and more liquid price discovery, cobalt's market is far smaller and considerably less liquid, making it more sensitive to production interruptions at key assets.

Cobalt markets have experienced significant price volatility in recent years, driven by shifting battery chemistry preferences, oversupply concerns from DRC production growth, and periodic demand spikes from battery manufacturers seeking to secure long-term supply agreements. In this environment, disruptions at top-tier cobalt producers like TFM carry asymmetric market significance: they may not move cobalt prices dramatically during brief episodes, but they contribute to a broader narrative of supply vulnerability that influences long-term contracting decisions and pricing expectations.

The next major ASX story will hit our subscribers first

Labour Governance as an Underpriced ESG Risk Factor

What the TFM Dispute Reveals About Collective Bargaining Quality

The ESG investment community has spent considerable energy developing frameworks for evaluating mining companies' environmental performance and their relationships with local communities, but the quality of collective bargaining processes at large-scale operations has received comparatively less systematic attention. The TFM strike exposes this as a meaningful gap. The workers' central complaint was not simply about the outcomes of the CBA negotiation; it was about the process itself and the degree to which the designated union delegation genuinely represented their interests rather than facilitating a management-preferred outcome.

Several specific governance concerns emerge from the TFM dispute:

- The transparency of union delegation selection processes and whether representatives were genuinely elected or effectively management-facilitated

- Worker access to independent legal and advisory support during CBA negotiations, which is often limited or absent in mining operations in developing country contexts

- The adequacy of internal grievance mechanisms, given that workers resorted to strike action rather than resolving concerns through established channels

- The independence of unions from management influence, which is difficult to verify externally but critically important to the genuine functioning of collective bargaining

The management response, combining loyalty bonuses for non-participants with dismissal threats for strikers, reflects a crisis-management approach that addresses the immediate production disruption without building the institutional capacity needed to prevent recurrence.

ESG Investor Considerations and Supply Chain Due Diligence

For institutional investors with direct exposure to CMOC or indirect exposure through funds tracking mining sector indices, the TFM strike raises questions that go beyond short-term production impact. The sustainability of the social licence to operate at a mine of TFM's scale is a material factor in long-term value assessment, and a pattern of recurring disruptions suggests that social licence is not as robustly maintained as production figures alone might imply.

Key considerations for ESG-focused investors include:

- Alignment of TFM's labour relations practices with established international frameworks such as the IFC Performance Standards on labour and working conditions

- The adequacy of supply chain due diligence conducted by downstream copper consumers, including electric vehicle manufacturers and grid infrastructure developers, regarding labour governance at their primary metal suppliers

- The degree to which CMOC's publicly stated commitments to responsible operations are reflected in verifiable operational practices at the mine level, as distinct from corporate-level reporting

For downstream industries that have made public commitments to responsible sourcing, the TFM situation represents a concrete test of whether supply chain due diligence frameworks are sufficiently granular to capture labour governance risks at specific operations.

What Sustainable Labour Relations Would Actually Require

A Framework for Structural Improvement

Resolving the immediate disruption through bonuses and ultimatums is not the same as building the institutional infrastructure for sustainable labour relations at a mine producing 519,000 tonnes of copper annually. CMOC's pathway to achieving its ambitious 2028 production targets without repeated disruption cycles runs directly through improvements in the governance mechanisms that determine how workers experience their relationship with management.

Independent union verification requires establishing transparent processes through which CBA negotiating delegations are selected by workers through genuine democratic mechanisms, rather than through management-facilitated processes that may produce representatives more attuned to management preferences than worker concerns.

Multi-tiered grievance escalation protocols would create formal pathways for workers to raise concerns through progressively senior channels before industrial action becomes the only available recourse. The fact that TFM workers moved directly to strike action suggests that existing internal channels were perceived as insufficient or ineffective.

Compensation benchmarking against regional mining sector standards would reduce the perception that workers at Chinese-operated mines receive below-market compensation packages relative to workers at comparable operations, a perception that consistently appears in labour disputes across the Chinese-operated segment of African mining.

Transparency in social investment reporting would help build broader community trust by publicly documenting local employment rates, supplier spending with community businesses, and social investment commitments, creating external accountability for commitments that might otherwise remain unverifiable.

The Production Continuity Argument for Proactive Investment

The business case for proactive investment in labour relations infrastructure is, ultimately, a production continuity argument. Each disruption episode at TFM carries direct costs in lost production, management time, investigation expenses, and bonus payments designed to restore normal operations. It also carries indirect costs in the form of reputational damage, elevated risk premiums in financing arrangements, and the cumulative erosion of worker trust.

For CMOC specifically, the arithmetic of disruption becomes increasingly unfavourable as its 2028 targets approach. Missing production targets at a moment of near-record copper prices is expensive. Missing them due to a third major disruption at TFM within a five-year period would raise serious questions about the company's operational management capabilities, affecting investor confidence, downstream customer relationships, and the DRC government's assessment of CMOC as a reliable partner for further concession development.

Frequently Asked Questions About the CMOC Congo Copper Mine Strike

What is Tenke Fungurume Mining?

TFM is one of the largest copper-cobalt mining operations in the Democratic Republic of Congo, majority-owned by Chinese mining group CMOC with an 80% stake. The mine produced approximately 519,000 tonnes of copper in 2025, representing roughly 15% of the DRC's total annual copper output.

Why did workers at CMOC's TFM mine go on strike in June 2026?

Workers initiated strike action on June 1, 2026, objecting to a new collective bargaining agreement they say was negotiated between TFM management and a union delegation without adequate direct worker participation. Their substantive demands included better base wages, housing allowances, and improved healthcare access.

How did CMOC respond to the TFM strike?

TFM characterised the strike as illegal and issued a deadline for workers to return to their posts. Workers who did not participate received a $500 loyalty bonus, while those who reportedly resisted pressure to join the strike received $1,000. Those who did not return by the deadline faced immediate dismissal proceedings. TFM subsequently confirmed operations had normalised.

Has TFM experienced previous major disruptions?

Yes. In 2022, TFM experienced an extended export suspension related to a dispute involving a government-appointed administrator and state mining company Gécamines, establishing a precedent for significant operational risk at the asset.

What is CMOC's copper production target for its DRC operations?

CMOC has publicly targeted between 800,000 and 1 million tonnes of copper per year from its combined DRC operations (TFM and KFM) by 2028.

How significant is TFM to global copper supply?

TFM's 2025 output of approximately 519,000 tonnes represented roughly 15% of DRC copper production. Given the DRC's position as the world's second-largest copper producer, TFM constitutes a globally material asset whose disruptions carry real supply chain significance.

The Bigger Picture: Governance, Geopolitics, and the Future of DRC Copper

The June 2026 CMOC Congo copper mine strike is best understood as a diagnostic event rather than a defining one. It was resolved quickly enough to avoid leaving a lasting mark on copper supply statistics, and it will likely not appear in annual production figures as more than a marginal footnote. However, its diagnostic value is considerable, because it confirms that the structural conditions that make TFM vulnerable to recurring disruption remain in place despite years of operational experience at this facility.

The intersection of three converging pressures makes this moment particularly consequential. Copper's role in the global energy transition has elevated its strategic importance to a level that transforms mining governance failures from industry-specific concerns into matters of broader economic and geopolitical significance. The geopolitical competition over DRC minerals has placed every operational disruption at Chinese-operated mines under a spotlight that connects labour relations incidents to narratives about supply chain resilience. And near-record copper prices have made the cost of disruptions, measured in foregone revenue at prevailing market prices, higher than at almost any point in the metal's history.

For CMOC, the path to realising its 2028 production ambitions runs through TFM's stable operation. For the global copper market, TFM's reliability as a production asset matters increasingly as demand from electrification, grid expansion, and technology infrastructure continues to accelerate. And for the workers at TFM who initiated the June 2026 strike, the question that remains unanswered is whether the resolution of this dispute represents the beginning of a genuine improvement in labour governance, or merely a temporary restoration of operational normalcy that leaves the underlying conditions for future disruption intact.

This article contains forward-looking assessments regarding production targets, market conditions, and supply chain dynamics that involve inherent uncertainty. Investors and market participants should conduct independent analysis before making decisions based on information presented here. Production targets cited are those publicly communicated by CMOC and do not constitute guarantees of future operational performance.

Want to Know When the Next Major Copper Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including copper and cobalt — so subscribers can act ahead of the broader market. Start your 14-day free trial today, or explore Discovery Alert's dedicated discoveries page to see how historic finds have generated extraordinary returns for early investors.