June 9, 2026

Understanding the Coal Consumption Paradox in 2025

The global energy transition presents an extraordinary contradiction as we approach 2030: coal consumption reaches unprecedented heights while simultaneously beginning its irreversible structural decline. This global coal demand decline phenomenon reflects the complex interplay between economic development pressures, energy security imperatives, and technological advancement across diverse regional markets.

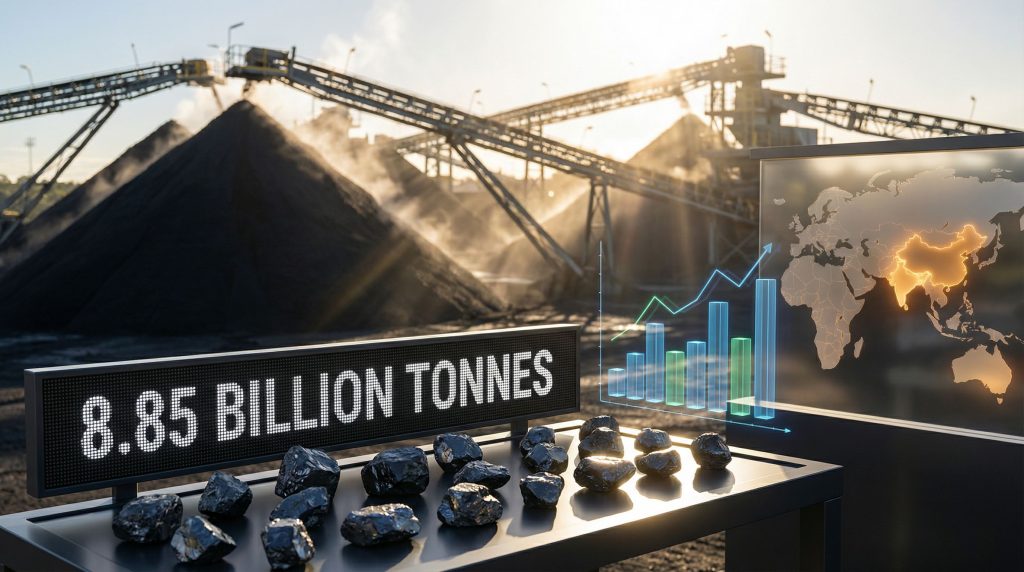

According to the International Energy Agency's Coal 2025 report, global coal demand reached a record 8.85 billion tonnes in 2025, representing a 0.5% increase year-over-year. However, this peak marks the culmination of a decades-long growth trajectory that began with 3.8 billion tonnes in 1990, now transitioning toward projected decline to approximately 8.5 billion tonnes by 2030.

This contradiction emerges from three distinct technical mechanisms operating simultaneously across global energy systems. First, renewable energy capacity deployment scales faster than coal plant retirements, creating temporary overlap periods where new generation sources coexist with legacy coal infrastructure. Furthermore, nuclear energy expansion and liquefied natural gas infrastructure development provide alternative baseload generation, reducing coal's monopoly on reliable power supply.

In addition, industrial efficiency improvements decrease per-unit energy intensity while absolute coal volumes persist, temporarily sustaining demand despite productivity gains. This energy security analysis becomes crucial for understanding these transitional dynamics.

Key Global Coal Demand Metrics 2025-2030

| Metric | 2025 Figure | 2030 Projection |

|---|---|---|

| Global Coal Demand | 8.85 billion tonnes | ~8.5 billion tonnes |

| Annual Growth Rate | +0.5% | Declining trend |

| China's Market Share | ~55% of global demand | Gradual reduction |

| India's Annual Growth | +3% | 200MT absolute increase |

| Southeast Asia Growth | +4% annually | Fastest regional expansion |

When big ASX news breaks, our subscribers know first

How Regional Economics Drive Coal Consumption Patterns

China's Strategic Energy Transition Framework

China's dominance in global coal markets, accounting for approximately 55% of total consumption, positions the nation as the primary variable affecting worldwide demand trajectories. The government's commitment to peak domestic coal consumption by 2030 represents calculated economic positioning rather than environmental pressure alone.

Keisuke Sadamori, Director of Energy Markets and Security at the IEA, emphasizes the uncertainty surrounding China's trajectory: "There are many uncertainties affecting the outlook for coal, most notably in China, where developments from economic growth and policy choices to energy market dynamics and weather will continue to have an outsize influence on the global picture."

China's transition operates through four sequential displacement mechanisms:

- Wind and solar capacity additions exceeding new coal plant construction

- Nuclear power expansion reducing baseload coal dependency

- Liquefied natural gas imports providing transition fuel alternatives

- Industrial efficiency improvements lowering per-unit energy intensity

The nation simultaneously deploys renewable energy at unprecedented rates while maintaining coal consumption through 2030. This apparent contradiction reflects technical grid integration constraints rather than policy inconsistency. Battery storage production scales at approximately 50 GWh annually while renewable capacity additions reach 150+ GW annually, creating mismatches that sustain coal's grid stabilization role despite theoretical overcapacity in renewable generation.

Steel and cement industries, collectively accounting for roughly 30% of global coal demand decline potential, face distinct transition challenges. Consequently, these sectors require technological breakthroughs in hydrogen-based or electric arc furnace technologies for steel production, and alternative technologies like solar thermal or hydrogen systems for cement manufacturing.

India's Industrial Growth Engine

India represents the strongest coal demand growth vector through 2030, with consumption forecast to rise 3% annually, generating a 200 million tonne absolute increase. This expansion exceeds any other nation's net coal growth during the same period and reflects India's positioning as the final major economy transitioning from agricultural to manufacturing-based economic models.

Unlike China, which completed primary industrialization, or developed economies with post-industrial energy structures, India confronts simultaneous pressures. For instance, the nation must provide electricity access to 700+ million citizens without reliable power whilst developing manufacturing capacity for global export markets.

India's Coal Consumption Drivers:

- Steel production expansion from 150 MT annually toward 300+ MT capacity by 2030

- Cement manufacturing growth driven by infrastructure development and urbanisation

- Export processing zones requiring dedicated power generation for industrial competitiveness

- Infrastructure development including highway, railway, and port expansion programmes

India's electricity grid experiences specific integration challenges that sustain coal's role beyond economic considerations. However, seasonal variability driven by monsoon hydroelectric availability requires baseload capacity providing reliable output regardless of weather patterns.

What Economic Forces Shape Coal's Declining Trajectory?

Competitive Energy Economics

The global coal demand decline trajectory reflects fundamental shifts in energy economics rather than policy mandates alone. Coal faces intensifying competitive pressure from alternative energy sources through multiple channels simultaneously transforming market dynamics.

Solar photovoltaic technology has achieved cost reductions exceeding 80% over the past decade, now reaching cost competitiveness with coal in most geographies without subsidy support. Moreover, wind power costs declined over 40% during the same period, whilst coal power plant operational costs rise due to environmental compliance requirements.

Energy Source Competitive Analysis:

| Energy Source | Cost Trajectory | Market Position | Technical Advantages |

|---|---|---|---|

| Solar PV | Declining rapidly | Competitive globally | Modular deployment |

| Wind Power | Stable/declining | Cost-effective at scale | High capacity factors |

| Natural Gas | Variable regionally | Bridge fuel status | Grid flexibility |

| Coal | Rising operational costs | Legacy baseload role | Existing infrastructure |

Investment Capital Reallocation Patterns

Financial markets increasingly redirect capital away from coal infrastructure toward renewable energy projects, creating self-reinforcing decline cycles. This capital flight operates through multiple mechanisms:

- Reduced access to development financing for new coal projects

- Higher insurance costs and operational expenses for coal facilities

- Stranded asset risks for existing coal infrastructure

- Regulatory compliance expenses increasing operational burdens

New coal plant construction requires $3-5 billion per GW compared to $1-2 billion per GW for solar and wind installations. Furthermore, coal plants built 30-50 years ago now face retirement decisions, whilst new coal capacity cannot compete with renewable alternatives on total cost basis.

How Will Southeast Asia's Energy Demand Impact Global Coal Markets?

Southeast Asia emerges as the fastest-growing coal consumption region globally, with 4% annual growth projected through 2030. This expansion reflects distinct development dynamics compared to China or India's industrialization pathways.

Manufacturing Base Development

Vietnam, Indonesia, and Thailand are establishing export processing zones requiring reliable baseload power generation. Unlike renewable-dependent systems requiring sophisticated grid integration technologies, coal-fired power plants provide lowest-cost reliable generation for industrial parks and manufacturing clusters. This regional development connects directly to green transition strategies being implemented across these economies.

Southeast Asian Coal Demand Drivers:

- Export processing zone expansion across Vietnam, Indonesia, Thailand

- Manufacturing competitiveness requirements for reliable power supply

- Infrastructure construction driving cement and steel demand

- Economic development priorities emphasising energy security over environmental concerns

Energy Infrastructure Constraints

Limited renewable energy infrastructure and grid integration capabilities force temporary reliance on coal-fired power generation. However, this represents transitional rather than permanent market dynamics, as these nations simultaneously invest in renewable capacity and grid modernisation programmes.

The region's rapid economic growth creates immediate electricity demand that renewable infrastructure cannot yet satisfy at required scales and reliability levels. Consequently, coal provides interim solutions while renewable capacity scales to displacement thresholds.

What Scenarios Could Alter Coal Demand Projections?

Upside Risk Factors

The International Energy Agency identifies several scenarios potentially increasing coal consumption beyond current projections, primarily centred on China's economic and energy market developments. These factors could delay the anticipated global coal demand decline.

China Economic Acceleration Scenarios:

- Faster GDP growth increasing industrial energy demand beyond renewable supply capacity

- Slower renewable integration due to grid stability or technology constraints

- Increased coal gasification investments for chemical production applications

- Weather-related hydroelectric shortfalls requiring coal-fired backup generation

Global Economic Disruption Factors:

- Supply chain disruptions affecting renewable energy equipment availability

- Natural gas price volatility driving coal substitution in flexible generation markets

- Geopolitical tensions limiting international energy trade flows

- Technology deployment delays postponing renewable capacity targets

Downside Acceleration Scenarios

Conversely, several technological and policy developments could accelerate coal demand decline beyond baseline projections:

- Breakthrough energy storage technologies enabling higher renewable penetration rates

- Expanded carbon pricing mechanisms increasing coal's relative cost disadvantage

- Accelerated electric vehicle adoption reducing oil demand and freeing natural gas for power generation

- Enhanced climate policy coordination tightening emission constraints across major consuming nations

For instance, effective implementation of canada energy transition challenges could serve as a model for other developed economies.

Analyst Note: These scenarios illustrate the range of uncertainty surrounding global coal demand decline projections, emphasising the importance of monitoring technological advancement rates, policy implementation effectiveness, and economic development trajectories across key consuming regions.

How Should Investors Position for Coal Market Evolution?

Portfolio Strategy Framework

The coal demand peak presents distinct investment implications requiring sophisticated analysis across different market segments and geographic regions. Understanding mining decarbonisation benefits becomes essential for strategic positioning.

Thermal Coal Investment Considerations:

- Focus on lowest-cost producers with shortest payback periods

- Prioritise operations with diversification potential into renewable energy or critical minerals

- Evaluate stranded asset risks in long-term capital allocation planning

- Consider geographic positioning relative to demand centres and transport infrastructure

Metallurgical Coal Asset Evaluation:

- Steel production requirements provide longer demand visibility than thermal coal

- Quality premiums likely to increase as supply rationalises through mine closures

- Geographic proximity to steel production centres becomes critical competitive advantage

- Technology substitution risks from hydrogen-based steelmaking require monitoring

Infrastructure and Logistics Positioning

Coal transport and logistics assets face fundamental utilisation challenges requiring strategic repositioning. Furthermore, implementing a comprehensive critical minerals strategy can help companies transition their operations effectively.

- Coal transport assets face declining utilisation and potential conversion requirements

- Port facilities may require infrastructure conversion for alternative commodities

- Rail networks need diversification strategies toward critical minerals or renewable energy logistics

- Storage and handling systems require flexibility for multiple commodity types

Investment Risk Assessment Matrix:

| Asset Category | Risk Level | Time Horizon | Mitigation Strategy |

|---|---|---|---|

| Thermal Coal Mines | High | 5-10 years | Cost leadership focus |

| Metallurgical Coal | Medium | 10-15 years | Quality differentiation |

| Transport Infrastructure | High | Immediate | Diversification planning |

| Processing Equipment | Medium | Variable | Technology upgrades |

The next major ASX story will hit our subscribers first

What Does This Transition Mean for Global Energy Security?

Supply Chain Resilience Considerations

The global coal demand decline peak forces nations to fundamentally reconsider energy security frameworks beyond traditional fossil fuel supply chain management.

Emerging Energy Security Challenges:

- Renewable energy supply chain vulnerabilities concentrated in specific geographic regions

- Critical mineral dependencies for clean energy infrastructure development

- Grid stability requirements during transition periods between energy systems

- Strategic reserve policies requiring updates for diversified energy portfolios

Countries historically dependent on coal face complex transition management requiring simultaneous development of alternative energy sources, grid infrastructure modernisation, and economic diversification strategies. However, this creates temporary vulnerability periods where coal retirement outpaces renewable capacity deployment.

Economic Development Balance

Developing economies encounter particular challenges balancing industrial growth objectives with environmental commitments. The coal transition timeline affects national competitiveness in global manufacturing markets, creating tensions between climate objectives and economic development priorities.

Policy Framework Requirements:

- Managed transition timelines preventing economic disruption

- Technology transfer mechanisms accelerating renewable adoption

- Financial support systems for renewable energy infrastructure development

- Industrial competitiveness preservation during energy system transitions

These considerations highlight the complexity of achieving global coal demand decline whilst maintaining economic stability and energy security across diverse national contexts. Current global coal demand projections reflect these multifaceted challenges.

Navigating the Coal Demand Inflection Point

The 2025 global coal demand decline peak represents a fundamental transformation in energy economics extending far beyond temporary market cycles. This inflection point reflects the convergence of technological advancement, economic competition, policy frameworks, and development priorities reshaping how nations approach energy security and industrial competitiveness.

Understanding regional demand patterns becomes essential for stakeholders across energy value chains. China's managed transition timeline, India's industrial growth imperatives, and Southeast Asia's rapid development create distinct market dynamics requiring nuanced strategic approaches rather than uniform global assumptions.

The transition creates both investment risks and opportunities demanding sophisticated analysis of technological substitution rates, policy implementation effectiveness, and economic development trajectories. Coal's declining trajectory is established, but the pace and regional variation of this decline will determine market outcomes across commodity, infrastructure, and technology sectors.

Energy security frameworks must evolve beyond traditional fossil fuel supply chain management toward comprehensive approaches addressing renewable energy supply chains, critical mineral dependencies, and grid modernisation requirements. This evolution requires coordinated policy development, technology advancement, and investment allocation across multiple timeframes and stakeholder groups.

Recent analysis by the IEA indicates that whilst coal demand reaches plateau levels, the trajectory toward gradual decline becomes increasingly evident across major consuming economies.

Disclaimer: This analysis contains forward-looking projections based on current market trends and policy frameworks. Actual outcomes may vary significantly due to technological breakthroughs, policy changes, economic disruptions, or other unforeseen factors affecting global energy markets. Investors should conduct independent research and consider multiple scenarios when making investment decisions related to energy sector assets.

The global coal demand decline trajectory reflects irreversible structural changes in energy economics, technology capabilities, and policy priorities. Successfully navigating this transition requires understanding the complex interplay between development needs, environmental objectives, and economic competitiveness across diverse regional contexts.

Ready to Capitalise on Energy Transition Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including critical energy transition commodities driving the post-coal economy. As global energy markets transform and coal demand peaks, investors gain crucial advantages by identifying mining discoveries in lithium, rare earths, and other critical minerals that power renewable energy infrastructure through Discovery Alert's dedicated discoveries page.