May 22, 2026

The Underground Energy Race Reshaping China's Gas Future

Unconventional gas development has a history of arriving slowly, then transforming entire energy systems almost overnight. The United States shale revolution took decades of incremental technology refinement before it reshaped global LNG markets. China appears to be following a similar trajectory with coal rock gas in China, a resource that until recently existed only as a geological curiosity on the fringes of coalbed methane programmes. Today, it sits at the centre of one of the most consequential domestic energy strategies Beijing has pursued in a generation.

Understanding why this resource matters requires looking past the headline production numbers and examining the structural forces pushing China toward deeper, more technically demanding gas extraction than it has ever attempted at scale.

When big ASX news breaks, our subscribers know first

Why Deep Gas Is Becoming China's Strategic Priority

China consumes approximately 430 billion cubic metres (bcm) of natural gas annually, a figure analysts project will climb to a peak of 600 to 650 bcm by 2040. That demand trajectory creates an increasingly urgent supply gap, particularly as conventional gas fields mature and coalbed methane output plateaus at a modest contribution of roughly 5% of national production.

The geopolitical context sharpens this urgency considerably. Back-to-back supply shocks, including the disruptions stemming from the Russia-Ukraine conflict and the Iran war, demonstrated in concrete terms how exposed import-dependent energy systems can be to external events far beyond Beijing's control. Furthermore, the US-China trade war impacts have amplified these vulnerabilities, reinforcing Beijing's determination to build genuine energy self-sufficiency.

As the world's largest energy importer, China has watched LNG spot prices and pipeline politics create economic turbulence twice in four years. The natural gas price trends in global markets have further underscored how quickly external pricing dynamics can affect domestic energy costs, making indigenous supply development a top strategic priority.

The strategic response has been to accelerate development of every viable domestic gas resource simultaneously. Shale gas now contributes around 10% of national output, establishing a meaningful domestic supply pillar. Tight gas and coalbed methane add smaller but meaningful volumes. Coal rock gas (CRG) has emerged as what PetroChina's internal planning documents describe as the strategic next-phase fuel, a resource with the geological scale and production potential to materially reduce China's structural import dependency.

As Huang Tianshi, principal gas analyst at S&P Global Energy, has observed, CRG currently offers stronger growth potential than alternative domestic gas sources, reflecting both the resource's scale and the maturity of the extraction technology being applied to it.

Coal Rock Gas vs. Coalbed Methane: Why Depth Changes Everything

The terminology around China's unconventional gas resources creates genuine confusion, and the distinction between coalbed methane and coal rock gas matters both technically and commercially.

Coalbed methane (CBM) is extracted from relatively shallow coal seams, typically at depths of less than 1,500 metres, using a dewatering process that reduces reservoir pressure and allows adsorbed gas to escape from the coal matrix. China invested heavily in CBM for decades, building significant infrastructure and institutional expertise. The disappointing result — only around 5% of national gas output despite enormous effort — stemmed from high per-well costs, low flow rates, and geological complexity that limited commercial scalability.

Coal rock gas occupies a fundamentally different part of the geological column. CRG formations exist at depths ranging from 1,500 metres to 6,000 metres, where significantly higher reservoir pressures create denser gas concentrations per unit of rock. Critically, gas exists in both adsorbed and free states within these deeper formations, a dual-state storage mechanism that is absent in shallower CBM systems and that substantially increases the recoverable resource per well.

The table below summarises the key technical distinctions across China's three main unconventional gas categories:

| Feature | Coalbed Methane (CBM) | Shale Gas | Coal Rock Gas (CRG) |

|---|---|---|---|

| Depth | Shallow (<1,500 m) | Varies (1,500–4,000 m) | Deep (1,500–6,000 m) |

| Gas State | Primarily adsorbed | Free gas in pores | Adsorbed + free |

| Extraction Method | Dewatering + vertical wells | Horizontal drilling + fracking | Horizontal drilling + fracking |

| Commercial Status (China) | Mature but underperforming | Commercially established | Rapidly emerging |

| China Output Contribution | ~5% of national gas | ~10% of national gas | Growing toward 10%+ |

This comparison reveals a critical insight that is not widely appreciated: CRG development is less a technological leap than a geological extension. China did not need to invent a new extraction paradigm. It needed to apply existing shale gas fracking expertise to a deeper, higher-pressure version of the geology its engineers had spent decades studying.

The Geology Behind China's Coal Rock Gas Endowment

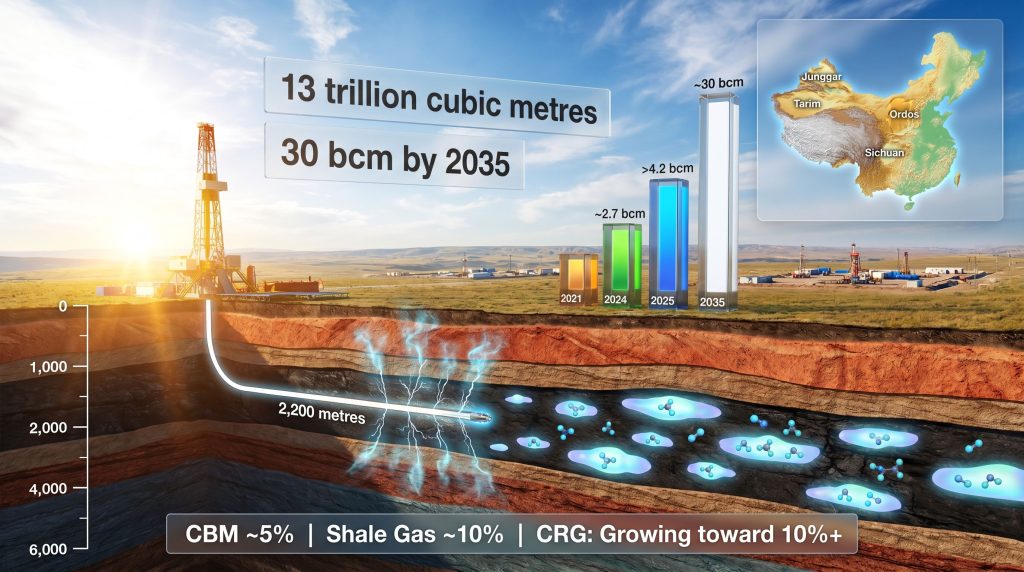

China's 14 major coal basins collectively represent one of the largest unconventional gas endowments on the planet. Total geological CRG resources are estimated to exceed 50 trillion cubic metres (tcm), with technically recoverable reserves across these basins assessed at approximately 13 tcm according to a 2025 CNPC seminar presentation reviewed by Reuters. Proven geological reserves had surpassed 700 billion cubic metres by late 2025.

The Ordos Basin, which spans portions of Shaanxi, Shanxi, Inner Mongolia, Ningxia, and Gansu provinces, hosts the most advanced commercial CRG development in the country. The Daji gas field within the Ordos Basin is China's flagship CRG project, generating more than 75% of national coal rock gas output and achieving annual production capacity exceeding 4 billion cubic metres, making it the world's first commercially scaled CRG operation of its kind.

Beyond the Ordos, a geographic spread of emerging basins is expanding the resource frontier:

- Sichuan Basin (southern China): Active exploration breakthroughs with early appraisal activity

- Junggar Basin: New appraisal programmes underway

- Bohai Bay Basin: Early-stage commercial interest from multiple operators

- Tarim Basin: Identified as a high-potential frontier zone

- Turpan-Hami Basin: Geological surveys progressing

- Yunnan-Guizhou and Hailar: Exploration-stage discoveries with preliminary resource assessments

The geographic distribution of these formations across China's interior basins is itself a strategically important characteristic. Unlike resources concentrated in a single region, a multi-basin CRG endowment distributes development risk, reduces single-point infrastructure bottlenecks, and creates the foundation for provincial-level supply security. This multi-basin picture reflects the broader global resource landscape in which diverse geological endowments increasingly determine long-term energy competitiveness.

Senior geologist Zhang Junfeng of CNPC's Exploration and Development Institute has stated that China is the first and only country commercially developing CRG, attributing this unique position to China's specific geological conditions and the ceiling reached by its traditional coal seam gas programmes.

How the Jishen 6-7 Well Changed Everything

The commercial history of coal rock gas in China traces back to a single pivotal moment in 2021, when PetroChina applied shale gas fracking methodology to the Jishen 6-7 well in the Daji field of the Ordos Basin. The well involved drilling a horizontal section of approximately 3,000 metres at a depth of around 2,200 metres below the surface, using high-pressure injection of water, sand, and chemical additives to fracture the surrounding coal rock and release trapped gas.

The result was a daily output of 100,000 cubic metres, a flow rate that crossed the threshold of commercial viability and triggered a multi-billion-dollar drilling campaign. From that single well success, China's CRG programme expanded to more than 700 drilled wells by the end of 2025, with production reaching 4.2 bcm for the full year.

The extraction process itself follows a well-established sequence:

- A vertical wellbore is drilled to the target depth, typically 2,000 to 6,000 metres, before turning horizontal

- The horizontal section extends approximately 3,000 metres through the coal-bearing rock formation

- Hydraulic fracturing is performed in multiple stages along the horizontal section, injecting pressurised fluid to create fracture networks in the rock

- Gas flows from both the fracture network and the coal matrix itself, with the dual adsorbed-and-free gas state improving per-well recovery compared to CBM

- Surface processing separates gas from water and other fluids before pipeline injection

The technology transfer from shale to CRG was not seamless but it was far more efficient than building a new industry from scratch. China's existing shale gas supply chain, including drilling rigs, fracturing fleets, completion expertise, and pipeline infrastructure, is directly applicable to CRG operations. As Yu Baihui of S&P Global Energy has noted, China already possesses a mature shale gas supply chain, from rigs to fracturing fleets, and that capability is directly transferable to coal rock gas development.

What Does Advanced Stimulation Research Offer?

Research currently underway at the Chinese Academy of Sciences is exploring next-generation stimulation methods, including gas pulse stimulation and electric pulse stimulation, as potential lower-cost alternatives to conventional hydraulic fracturing. If successful, these techniques could reduce both per-well completion costs and the environmental footprint of CRG operations considerably.

The Production Trajectory: From Pilot Wells to Industrial Scale

The pace of CRG production growth since the 2021 breakthrough has been exceptional by any measure of unconventional gas development.

| Year | CRG Production | Key Milestone |

|---|---|---|

| 2021 | Pilot stage | First commercial fracking at Jishen 6-7 well, 100,000 m³/day flow rate |

| 2024 | ~2.7 bcm | Rapid ramp-up from Daji field expansion |

| 2025 | >4.2 bcm | Daji surpasses 4 bcm annual capacity; 700+ wells drilled nationally |

| 2035 (PetroChina forecast) | ~30 bcm | Internal production target, potentially exceeding current shale gas output |

PetroChina's internal planning targets CRG output reaching 30 bcm annually by 2035. At current consumption levels, this would represent approximately 7% of China's total gas demand and could exceed 10% if consumption growth moderates. Critically, CRG could account for more than half of China's total incremental domestic gas supply growth over the coming decade, a contribution that would fundamentally alter the import dependency equation.

The next major ASX story will hit our subscribers first

The Cost Challenge: Deep Gas Economics and the Path to Competitiveness

The most significant near-term constraint on CRG scale-up is production cost. Drilling to depths of 2,000 to 6,000 metres is inherently more capital-intensive than shallower operations, and the industry is still in the early phase of the cost learning curve that has historically driven unconventional gas from frontier economics to commercial competitiveness.

For context, benchmark break-even costs across China's gas supply portfolio currently stand at:

- Conventional gas (China): 0.60 to 0.80 yuan per cubic metre

- Shale gas (Sichuan Basin): 1.70 to 1.80 yuan per cubic metre, equivalent to approximately $6.80 per million Btu, according to Rystad Energy analyst Chen Lin

- CRG: Full-cycle costs not yet formally benchmarked, but current estimates place them above shale gas levels

Three strategic pathways are being pursued to bring CRG costs down toward competitive levels:

- Infrastructure Integration: Co-developing CRG alongside existing tight gas and CBM projects in the Ordos Basin, including deepening older wells to access CRG-bearing formations rather than drilling full greenfield wells from surface

- Fracking Technology Optimisation: Reducing sand and chemical volumes consumed per well, which directly reduces per-well completion costs without compromising reservoir stimulation quality

- Advanced Stimulation Research: Applying gas pulse and electric pulse stimulation techniques currently being researched, which could ultimately replace or supplement hydraulic fracturing in certain geological settings

Analysts at S&P Global Energy project that CRG full-cycle costs should converge toward or potentially below shale gas levels as the resource base scales and China's existing gas development infrastructure is more efficiently leveraged across a larger number of producing wells.

One less-discussed cost reduction pathway involves the integration angle more specifically: many of China's Ordos Basin tight gas and CBM wells were drilled to depths that sit immediately above known CRG-bearing formations. Deepening these existing wellbores rather than spudding new surface locations could materially reduce the capital cost per unit of new CRG production, a concept with parallels to dual-zone completions in U.S. tight oil plays.

It is worth noting that coal rock gas does not currently fall within China's existing subsidy framework for unconventional gas, which covers shale gas and coalbed methane. Analysts broadly expect subsidy mechanisms to be introduced as more commercial fields reach viable output thresholds, though neither China's Ministry of Natural Resources nor the National Development and Reform Commission has announced a formal CRG subsidy policy.

Global Implications: What China's CRG Success Means for Energy Markets

The downstream consequences of successful CRG scale-up extend well beyond China's domestic energy balance. China is the world's third-largest natural gas consumer and one of the dominant buyers in global LNG markets. Consequently, a structural reduction in China's import requirements carries material implications for global spot pricing, long-term contract dynamics, and the investment case for LNG export projects currently in development. The global LNG supply outlook through 2035 and beyond will be increasingly shaped by whether China's domestic alternatives, including CRG, deliver on their production promises.

Every 10 bcm of domestic CRG production substitutes for approximately 7.3 million tonnes per annum (mtpa) of LNG imports, a volume equivalent to a sizeable mid-scale LNG export facility. If PetroChina achieves its 30 bcm target by 2035, the implied LNG displacement exceeds 22 mtpa, representing a meaningful reduction in China's annual LNG import demand from a market that is already structurally long supply through the 2030s.

The geopolitical dimension is equally significant. A credible domestic CRG supply trajectory materially strengthens Beijing's negotiating position in ongoing discussions about the proposed Power of Siberia 2 pipeline, which would bring additional Russian gas volumes into China. In addition, the China energy supply pressures already shaping broader commodity markets will evolve considerably if CRG scaling reduces the urgency of external energy arrangements. When domestic supply alternatives are real rather than aspirational, the urgency of concluding pipeline deals on terms favourable to Moscow diminishes considerably.

PetroChina's international ambitions for CRG technology extend to Australia. The company drilled two appraisal wells in Queensland's Bowen Basin during 2025, testing whether the geological conditions there are compatible with CRG extraction methods. Early results are being evaluated. If the technology proves transferable to Australian geology, it would mark the first international application of China-developed CRG methodology and signal the beginning of what could become an exported technical capability.

Five Conditions for CRG to Deliver on Its 2035 Promise

Whether CRG achieves its projected 30 bcm production target depends on the convergence of several conditions, each of which carries execution risk. Yu Baihui of S&P Global Energy has outlined the requirements clearly: high capital investment, faster technological progress, unified industry standards, expansion into new basins, and strong policy support must all materialise in roughly the right sequence.

Expanding on those requirements:

- Capital at scale: Moving from 700 wells to the thousands required for 30 bcm output demands sustained investment across multiple business cycles, including periods when gas prices may not justify marginal well economics

- Technology cost reduction: The transition from current above-shale-gas costs to competitive full-cycle economics requires both incremental fracking optimisation and potential step-change innovations from pulse stimulation research

- Unified standards: CRG-bearing formations in the Sichuan, Junggar, and Tarim basins have different geological characteristics from the Ordos. Well design, completion parameters, and reservoir characterisation frameworks developed at Daji will need adaptation rather than direct replication

- Basin expansion execution: Commercial development outside the Ordos requires new infrastructure, gathering systems, and pipeline connections that require long lead times and regulatory coordination

- Policy framework: Subsidy support comparable to existing shale gas incentives would materially improve the economics of early-stage basin development outside the Daji core area

Frequently Asked Questions: Coal Rock Gas in China

What is coal rock gas and how does it differ from regular natural gas?

Coal rock gas is an unconventional natural gas resource trapped within deep coal-bearing rock formations at depths of 1,500 to 6,000 metres. Unlike conventional natural gas, which accumulates in porous sandstone or carbonate reservoir rocks, CRG is stored in both adsorbed and free states within the coal matrix itself, requiring horizontal drilling and hydraulic fracturing to extract economically.

How much coal rock gas does China have?

Total geological coal rock gas resources are estimated to exceed 50 trillion cubic metres, with technically recoverable reserves across 14 major coal basins assessed at approximately 13 tcm. Proven reserves surpassed 700 billion cubic metres by late 2025.

Is coal rock gas the same as coalbed methane?

No. While both originate in coal-bearing geology, coalbed methane comes from shallower formations typically less than 1,500 metres deep and is extracted using conventional dewatering. Coal rock gas targets substantially deeper, higher-pressure formations and requires hydraulic fracturing technology adapted from shale gas development.

What is China's production target for coal rock gas?

PetroChina's internal forecasts project CRG output reaching 30 bcm annually by 2035, roughly a sevenfold increase from 2025 production levels of 4.2 bcm and potentially exceeding current shale gas output volumes.

Will CRG development reduce China's LNG imports?

Analysts broadly expect successful CRG scale-up to structurally reduce China's LNG import requirements, with meaningful downstream effects on global gas market pricing and long-term LNG trade flows. Each 10 bcm of domestic CRG production displaces approximately 7.3 mtpa of LNG imports.

Which country leads coal rock gas development globally?

China is currently the only country commercially producing CRG at scale. No other nation has replicated China's development model, though PetroChina is conducting early-stage appraisal in Australia's Bowen Basin to test international transferability of the technology.

Disclaimer: This article contains forward-looking statements, production forecasts, and analyst projections that are subject to significant uncertainty. Production targets, cost trajectories, and market impact estimates represent current expectations and assumptions that may not be realised. This content is intended for informational purposes only and does not constitute financial or investment advice.

Want to Stay Ahead of the Next Major Resource Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex resource data into actionable investment insights the moment announcements hit the exchange. Explore how historic discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the broader market.