May 21, 2026

Cobalt in deep-sea mining represents a critical frontier for addressing unprecedented supply chain challenges as battery manufacturers worldwide grapple with surging demand alongside electric vehicle adoption. The concentration of cobalt production in politically unstable regions, combined with ethical concerns surrounding artisanal mining practices, creates systemic vulnerabilities that threaten the clean energy transition. While terrestrial cobalt resources remain finite and geographically constrained, a transformative alternative lies beneath 4,000 meters of ocean water in the form of polymetallic nodules benefits scattered across abyssal plains.

The Economic Foundation of Ocean Floor Cobalt Extraction

Resource Density and Multi-Metal Value Creation

The economic viability of cobalt in deep-sea mining operations fundamentally differs from conventional terrestrial extraction through its multi-metal revenue model. Polymetallic nodules contain approximately 0.25-0.30% cobalt by weight, comparable to many land-based operations, but simultaneously yield manganese (23-30%), nickel (1.0-1.5%), and copper (0.8-1.2%) from the same source material.

This diversified metal content transforms project economics significantly. For a theoretical 10 million tonne annual nodule processing operation, the combined revenue streams would generate:

| Metal Component | Annual Recovery | Price Range | Revenue Potential |

|---|---|---|---|

| Cobalt | 25,000-30,000 tonnes | $35-45/kg | $875M-$1.35B |

| Nickel | 80,000-100,000 tonnes | $8-12/kg | $640M-$1.2B |

| Copper | 60,000-80,000 tonnes | $8-10/kg | $480M-$800M |

| Manganese | 2,000,000-2,500,000 tonnes | $1.50-2.50/tonne | $3M-$6.25M |

The combined gross revenue potential of $2.0-3.36 billion annually demonstrates why seabed mining economics cannot be evaluated solely on cobalt pricing. This multi-metal approach provides revenue diversification that terrestrial cobalt operations, typically extracting cobalt as a copper byproduct, cannot match.

Capital Investment and Operating Cost Analysis

Deep-sea cobalt extraction requires substantially higher initial capital investment compared to terrestrial alternatives. First-generation collection systems demand $2.8-5.2 billion in capital expenditure, significantly exceeding the $400 million to $2.5 billion range for new terrestrial cobalt operations.

However, operating cost projections tell a more complex story. According to deep‑sea mining concerns, the financial implications extend beyond simple extraction costs:

• Terrestrial cobalt operations (DRC): $12-18/kg cobalt (as copper byproduct)

• Seabed mining projections: $28-55/kg cobalt (assuming 75-85% collection efficiency)

• Break-even analysis: Seabed operations become profitable at cobalt prices of $32-42/kg

The higher operating costs reflect the technological complexity and energy requirements of deep-water operations. Yet these figures exclude the geopolitical risk premium that cobalt purchasers currently pay, estimated at $3-8/kg during supply uncertainty periods, making the true cost differential smaller than surface comparisons suggest.

Resource Longevity and Sustainability Considerations

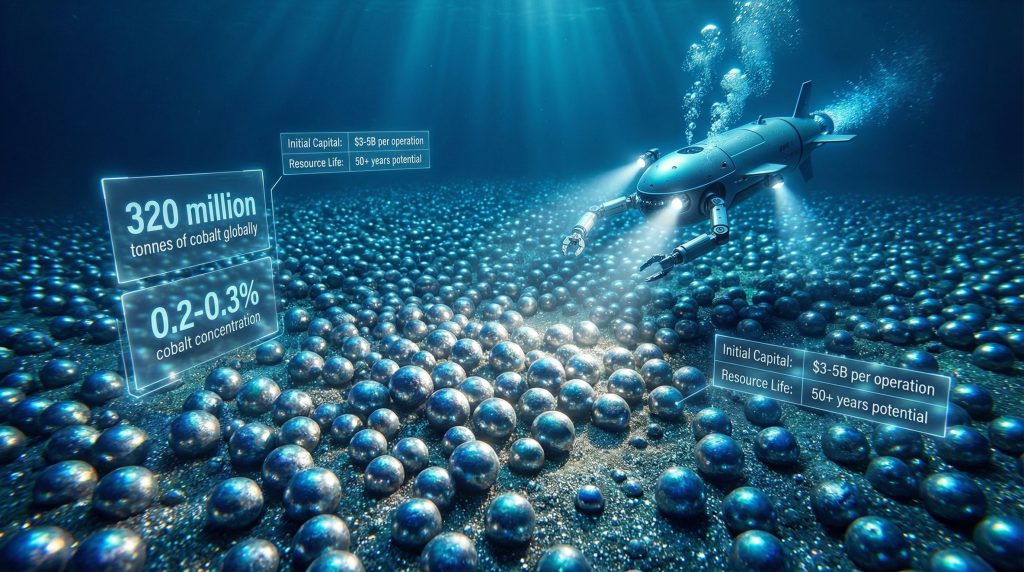

The scale advantage of seabed cobalt resources becomes apparent when examining long-term supply potential. The Clarion-Clipperton Zone alone contains an estimated 320 million tonnes of contained cobalt within polymetallic nodules, compared to global terrestrial reserves of approximately 7.1 million tonnes.

This resource abundance creates a fundamental shift in supply dynamics:

• Terrestrial mine life: 15-40 years typical operational period

• Nodule field operations: 50+ years potential production from single areas

• Global resource scale: Sufficient cobalt in nodules to supply projected demand for centuries

However, sustainability concerns arise from nodule regeneration timeframes. Scientific consensus indicates that polymetallic nodules require 1-10 million years to reform under normal deep-sea conditions, making these resources effectively non-renewable on human timescales despite their vast scale.

When big ASX news breaks, our subscribers know first

Supply Chain Transformation Through Maritime Resources

Breaking Concentrated Supply Dependencies

Current cobalt supply chains exhibit dangerous concentration levels that cobalt in deep-sea mining could fundamentally restructure. The Democratic Republic of Congo supplies 65-75% of global cobalt production, creating a Herfindahl-Hirschman Index score of 4,850 for cobalt supply, indicating severe monopolistic concentration.

Market analysis suggests that introducing 15-20% of global supply from geographically distributed seabed sources would reduce this concentration index to approximately 3,200-3,400, while still maintaining concerning but less severe concentration levels. This diversification would provide several strategic advantages:

• Reduced single-point failures: Weather-independent operations versus seasonal terrestrial mining disruptions

• Enhanced bargaining power: Battery manufacturers gain alternative sourcing options

• Price volatility mitigation: Historical analysis shows geographic diversification reduces pricing volatility by 15-25%

Regional Strategic Positioning

The geographic distribution of deep-sea cobalt resources creates new strategic advantages for different regions compared to terrestrial supply chains. Furthermore, companies like those involved in the Halls Creek cobalt project are recognising the importance of diversified supply sources.

Pacific Rim nations benefit from proximity to the Clarion-Clipperton Zone, located 8,000-12,000 kilometers from major Asian processing facilities versus 14,000-18,000 kilometers for European processors. This proximity advantage translates to 8-15% cost reduction through reduced transportation expenses.

Japan, South Korea, China, and Singapore currently hold 6 of 31 exploration contracts in the CCZ, representing 19% of total exploration rights in the zone. Combined with 78% of global battery manufacturing capacity located in Asia-Pacific, this creates integrated supply chain efficiency that could further consolidate Asian dominance in battery production.

Western markets gain different advantages through alternative supply routes that bypass traditional chokepoints including the Strait of Malacca, Suez Canal, and Panama Canal. This geographic diversification reduces supply chain vulnerability to maritime disruptions that have historically affected cobalt pricing.

Ethical Sourcing and ESG Premium Capture

Deep-sea cobalt extraction, once environmental concerns are addressed through proper regulation, offers certified conflict-free sourcing narratives that align with ESG investment mandates. Current terrestrial cobalt supply includes 20-25% from artisanal mining in the DRC, raising ongoing ethical concerns about labour practices and environmental degradation.

Battery manufacturers have demonstrated willingness to pay 5-12% premiums for cobalt certified as conflict-free and ethically sourced. Seabed cobalt could command similar premiums by eliminating concerns about artisanal mining practices, child labour, and community displacement associated with terrestrial operations.

This premium pricing potential improves project economics beyond raw metal value, potentially adding $2-5/kg to cobalt revenue from ESG-focused purchasers willing to pay for verified sustainable sourcing.

Technology Infrastructure and Processing Capabilities

Collection System Engineering

Harvesting cobalt in deep-sea mining requires fundamentally different technological approaches compared to conventional mining equipment. The collection process operates across three distinct phases: seafloor harvesting, vertical transport, and surface processing.

Seafloor harvesting vehicles utilise autonomous underwater systems designed for selective nodule collection while minimising sediment disturbance. These systems must operate continuously at depths of 4,000-6,000 meters under extreme pressure conditions equivalent to 400-600 times atmospheric pressure.

Key technical specifications include:

• Operating depth capability: 4,000-6,000 meters below sea level

• Collection efficiency targets: 75-85% nodule recovery from designated areas

• Selective harvesting: Differentiation between high-grade and low-grade nodules

• Sediment minimisation: Advanced washing systems to reduce environmental discharge

Vertical transport systems employ riser pipe technology to move collected nodules from the seafloor to surface processing vessels. These systems must handle continuous material flow while managing pressure differentials and maintaining structural integrity across extreme depth ranges.

Metallurgical Processing Innovation

Processing polymetallic nodules requires specialised hydrometallurgical techniques distinct from sulfide ore processing used in terrestrial cobalt extraction. The technology pathway involves several critical stages designed to maximise metal recovery while managing multi-metal separation.

Primary separation processes include:

- Screening and classification: Size separation of collected nodules

- Magnetic separation: Removal of ferromanganese components

- Gravity concentration: Isolation of high-density metal fractions

Hydrometallurgical extraction employs acid leaching using sulfuric acid solutions followed by selective precipitation and electrowinning for high-purity cobalt recovery. The process must achieve metal recovery rates above 85% to maintain economic viability while simultaneously extracting nickel, copper, and manganese.

Critical processing challenge: Managing sediment contamination in nodule processing requires advanced washing systems that minimise environmental discharge while maintaining high metal recovery efficiency across all target metals.

Floating Processing Platform Design

Surface processing vessels represent floating industrial facilities capable of handling continuous nodule flow while operating in open ocean conditions. These platforms must integrate metallurgical processing equipment with marine operational systems.

Design requirements include:

• Processing capacity: 10,000-20,000 tonnes nodules per day

• Weather resistance: Operations in sea states up to 4-5 meters significant wave height

• Environmental controls: Closed-loop water systems and waste containment

• Power generation: 50-100 MW electrical capacity for processing equipment

The technological complexity of these integrated systems contributes to the high capital requirements but enables continuous processing that terrestrial operations cannot match through elimination of seasonal weather disruptions. Moreover, according to the US deep-sea mineral processing plant initiatives, technological advancement continues to drive innovation in this sector.

Environmental Risk Framework and Mitigation Strategies

Deep-Sea Ecosystem Impact Assessment

Environmental considerations represent the primary uncertainty factor affecting the viability of cobalt in deep-sea mining projects. Unlike terrestrial mining impacts that occur in well-studied ecosystems, deep-sea mining affects environments that remain largely unknown to science.

Immediate operational impacts include sediment plume generation affecting filter-feeding organisms across 10-100 kilometer radius from collection sites. These sediment clouds can persist for weeks or months, potentially affecting organisms adapted to the extremely low-sediment conditions of abyssal plains.

Habitat destruction involves the complete removal of nodule fields that provide unique deep-sea ecosystems. Polymetallic nodules serve as hard substrate for sessile organisms in environments otherwise dominated by soft sediments, creating biodiversity hotspots in otherwise sparse deep-sea environments.

Long-term ecosystem implications present even greater uncertainties:

• Species extinction: Unknown rates of endemic species loss in poorly studied deep-sea environments

• Recovery timeframes: Ecosystem restoration impossible due to million-year nodule reformation periods

• Carbon cycle disruption: Potential interference with deep-ocean carbon sequestration processes

• Food web effects: Cascading impacts on deep-sea food chains dependent on nodule-associated organisms

Regulatory Compliance Cost Structure

Environmental compliance for deep-sea mining operations requires unprecedented baseline studies and monitoring systems that significantly impact project economics.

| Environmental Requirement | Estimated Cost Impact |

|---|---|

| Baseline ecosystem surveys | $50-100 million per project |

| Real-time monitoring systems | $20-40 million annually |

| Mitigation measures | 15-25% of operational costs |

| Environmental bonds | $500 million-1 billion per operation |

These environmental costs represent additional expenses not faced by terrestrial mining operations, potentially adding $15-25/kg to cobalt production costs depending on the stringency of regulatory requirements imposed by the International Seabed Authority.

Noise Pollution and Marine Life Disruption

Continuous deep-sea mining operations generate underwater noise that can affect marine mammal migration patterns and deep-sea acoustic communication. Industrial noise levels from collection systems, riser operations, and surface processing create acoustic pollution across broad ocean areas.

Marine mammals, particularly deep-diving species like sperm whales and beaked whales, utilise deep-ocean acoustic environments for navigation and communication. Mining operations could disrupt these behaviours across migration routes and feeding areas, requiring operational modifications or temporal restrictions that affect production efficiency.

Mitigation technology development focuses on:

• Noise reduction systems: Engineering quieter collection and processing equipment

• Seasonal restrictions: Operational timing to avoid peak migration periods

• Acoustic monitoring: Real-time detection and response systems for marine mammal presence

• Exclusion zones: Protective buffers around sensitive habitats and migration corridors

Investment Analysis and Financial Modelling

Risk-Return Profile Assessment

Investment analysis for cobalt in deep-sea mining requires evaluation across multiple risk categories with extended development timelines that differ substantially from conventional mining projects.

Technical risks remain high due to unproven commercial-scale extraction technologies and deep-water equipment reliability challenges. Current pilot projects operate at small scales that do not demonstrate the continuous production capabilities required for economic viability.

Regulatory risks present the highest uncertainty factor, with International Seabed Authority approval processes still evolving and potential for international moratoriums on deep-sea mining activities. Environmental protection standards continue developing as scientific understanding of deep-sea ecosystems improves.

Market risks include shifts in cobalt demand due to battery chemistry evolution toward reduced cobalt content and increased competition from recycling sources. Current projections suggest battery recycling breakthrough technologies could reach 10-15% of annual demand by 2030, potentially reducing new supply requirements.

Financial Return Scenarios

Investment modelling produces three distinct scenarios based on regulatory, technical, and market outcome probabilities:

Base Case Scenario (40% probability):

- Internal Rate of Return: 12-15%

- Net Present Value: $2-4 billion over 25-year project life

- Cobalt price assumption: $35-45/kg long-term average

Optimistic Case (25% probability):

- Internal Rate of Return: 18-22%

- Net Present Value: $6-10 billion

- Premium pricing for conflict-free cobalt sources adds $3-8/kg revenue

Pessimistic Case (35% probability):

- Internal Rate of Return: 5-8%

- Net Present Value: -$1-2 billion

- Regulatory delays and environmental compliance costs exceed projections

The high probability assigned to the pessimistic scenario reflects substantial regulatory and environmental uncertainties that could prevent project development entirely.

Comparative Investment Analysis

Deep-sea cobalt projects require evaluation against alternative investment opportunities in battery materials and critical minerals.

Terrestrial cobalt development offers lower capital requirements ($400 million-2.5 billion) and proven technologies but faces increasing environmental restrictions and community opposition. Geopolitical risks in primary producing regions create supply security concerns that justify investment in alternative sources.

Cobalt recycling investments require $100-500 million capital expenditure for commercial-scale facilities but offer steady feedstock from growing electric vehicle battery waste streams. Recycling operations achieve 85-90% cobalt recovery rates with lower environmental impact than primary extraction.

Battery chemistry diversification through investment in lithium iron phosphate and other reduced-cobalt technologies offers demand-side risk mitigation. However, high-energy density applications still require cobalt-based chemistries for performance optimisation.

Furthermore, the mining industry innovation trends suggest that technological advancement will continue to shape investment decisions across all extraction methods.

Market Evolution and Strategic Scenarios

Accelerated Development Pathway

The optimistic scenario for cobalt in deep-sea mining envisions first commercial operations beginning by 2028 with rapid scale-up to 5-7 major projects operational by 2035. This pathway requires successful resolution of environmental concerns and streamlined regulatory approval processes.

Under accelerated development, seabed sources could supply 15-20% of global cobalt demand by 2035, fundamentally reshaping market dynamics. Increased supply availability would likely stabilise cobalt prices in the $30-40/kg range, reducing price volatility that currently affects battery manufacturing cost predictability.

Market concentration effects under this scenario would reduce the Herfindahl-Hirschman Index from current levels above 4,800 to approximately 3,200-3,400, improving but not eliminating supply concentration concerns. Battery manufacturers would gain significant bargaining power through diversified sourcing options.

Constrained Growth Framework

A more conservative development scenario involves limited pilot projects with strict environmental controls, resulting in 2-3 commercial operations by 2035 supplying 5-8% of global cobalt demand. This pathway reflects cautious regulatory approaches prioritising environmental protection over resource development.

Under constrained growth, cobalt from deep-sea mining would command premium pricing for certified sustainable sources, potentially adding $5-12/kg to base metal prices. This premium would support project economics despite higher environmental compliance costs and restricted production volumes.

Supply chain benefits would remain limited, with continued dependence on terrestrial sources maintaining current concentration risks and geopolitical vulnerabilities.

Development Moratorium Scenario

The pessimistic scenario involves international restrictions or complete moratoriums on deep-sea mining activities, redirecting focus toward terrestrial exploration and recycling capacity expansion. This outcome reflects successful environmental opposition campaigns and precautionary regulatory approaches.

Under moratorium conditions:

• Continued DRC dominance: 65-75% supply concentration persists

• Price volatility maintenance: $40-60/kg cobalt pricing with continued speculation

• Alternative source acceleration: Increased investment in recycling and reduced-cobalt battery chemistry

• Supply security risks: Enhanced geopolitical vulnerabilities for battery manufacturers

Strategic Implications for Market Participants

Battery manufacturers must develop flexible sourcing strategies that account for all potential scenarios. Risk mitigation approaches include:

• Diversified sourcing agreements across terrestrial and potential seabed sources

• Technology investment in cobalt-reduced battery chemistries as demand hedge

• Direct partnerships with seabed mining companies for preferential supply access

• Strategic cobalt reserves to buffer supply disruption periods

Mining companies face strategic decisions between seabed exploration investment and terrestrial asset development. Balanced approaches involve:

• Portfolio diversification across terrestrial and seabed cobalt projects

• Environmental expertise development for regulatory compliance and social licence

• Technology partnership formation with deep-sea equipment specialists

• Extended timeline preparation for regulatory approval processes

Government stakeholders must develop national positions on deep-sea mining regulations while considering supply security implications for clean energy transitions. Policy frameworks should address:

• Environmental research investment for science-based regulatory decisions

• Strategic mineral reserves for supply security during transition periods

• International coordination on deep-sea mining governance frameworks

• Domestic processing capacity for critical mineral value chain control

The next major ASX story will hit our subscribers first

Navigating the Deep-Sea Transition

The development of cobalt in deep-sea mining represents both transformative opportunity and substantial risk for global battery supply chains. While polymetallic nodules contain enormous cobalt resources that could diversify supply away from concentrated terrestrial sources, successful extraction requires resolution of complex environmental, technical, and regulatory challenges.

The strategic value extends beyond cobalt production to encompass supply chain resilience, reduced geopolitical dependence, and potential premium pricing for conflict-free sourcing. However, the extended development timeline, uncertain regulatory environment, and environmental risks require careful risk management across all stakeholder categories.

Success in deep-sea cobalt development will depend on demonstrating environmental sustainability through rigorous scientific study, achieving technical reliability at commercial scale, and maintaining social licence to operate in international waters. According to comprehensive analyses of deep-sea mining, the organisations and nations that successfully navigate these challenges will gain significant competitive advantages in the global transition toward clean energy technologies.

The evolution of this industry over the next decade will fundamentally shape cobalt markets and battery supply chains for generations. Whether deep-sea mining becomes a sustainable solution to critical mineral supply challenges or remains a controversial proposition will depend on balancing resource development with environmental protection in some of Earth's least understood ecosystems.

Investment Consideration: Stakeholders evaluating deep-sea cobalt opportunities should prepare for extended development timelines, substantial environmental compliance costs, and regulatory uncertainties while positioning for potential first-mover advantages in a transformed cobalt market.

Ready to Discover the Next High-Potential ASX Mining Opportunity?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex geological announcements into actionable investment insights across all commodities including cobalt and battery materials. Explore Discovery Alert's dedicated discoveries page to see why historic mineral discoveries have generated exceptional returns, and begin your 14-day free trial today to position yourself ahead of the market.