May 21, 2026

The Geopolitical Economics of Mineral Dependency

For decades, the prevailing assumption underpinning Western industrial strategy was that globalised markets would reliably deliver raw materials to whoever could pay for them. That assumption has been systematically dismantled. When a single nation controls the processing of materials that underpin everything from fighter jet guidance systems to electric vehicle motors, the economics of efficiency collide headlong with the realities of geopolitical risk. Europe has absorbed this lesson at significant cost, and its response, centred on the EU stockpiling of tungsten, rare earths, and gallium, signals a structural transformation in how the continent intends to manage resource security in an era defined by strategic competition rather than cooperative interdependence.

The decisions now being made in Brussels, Paris, Berlin, and Rome will shape the economics of critical mineral markets for years, potentially decades, to come. Understanding the architecture of this initiative, its priorities, its governance challenges, and its investment implications requires moving beyond headline figures to examine the deeper mechanics of European import dependency and the specific properties of the minerals now designated as first-tier stockpile targets.

When big ASX news breaks, our subscribers know first

What Minerals Is the EU Prioritising, and Why These Six?

Tungsten, Rare Earths, and Gallium: The First-Tier Targets

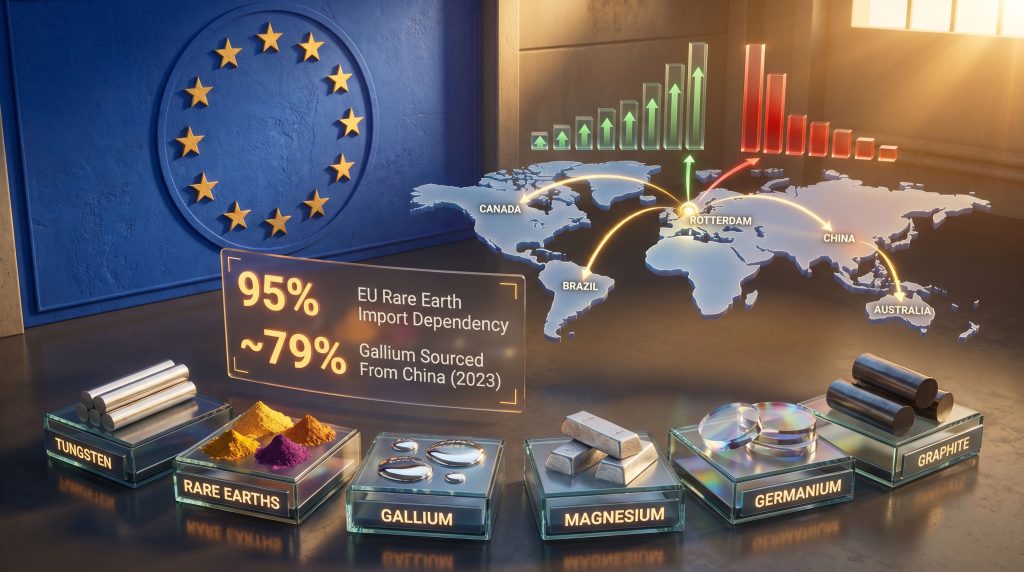

The selection of tungsten, rare earth elements, and gallium as the initial focus of the EU's stockpiling programme is not arbitrary. Each of these materials occupies a structurally irreplaceable position across defence and high-technology manufacturing, while simultaneously exhibiting extreme supply concentration in jurisdictions that have demonstrated both the willingness and the capability to use resource access as a geopolitical instrument.

Tungsten possesses the highest melting point of any metal at 3,422 degrees Celsius, making it physically irreplaceable in applications ranging from cutting tools and armour-piercing projectiles to radiation shielding and high-performance electronics. Furthermore, tungsten's strategic importance is amplified by China controlling approximately 80% of global tungsten production, with its dominance extending into processing and refining. This is not merely a mining dependency but a full value-chain dependency, a distinction that proves critical when evaluating the true depth of Europe's exposure.

Rare earth elements (REEs) encompass 17 chemically similar metals whose properties are essential to the permanent magnets used in wind turbines, electric vehicle motors, and precision-guided munitions. Europe currently imports approximately 95% of its rare earth requirements, with that dependency concentrated across China, Malaysia, and Russia. The processing bottleneck is particularly severe: even where rare earth ores are mined outside China, the vast majority of separation and refining capacity remains under Chinese control, meaning that geographic diversification of extraction does not automatically translate to supply chain independence.

Gallium, a byproduct of aluminium and zinc smelting, is the foundational material for gallium nitride and gallium arsenide semiconductors. Indeed, gallium in semiconductors underpins 5G infrastructure, military radar, satellite systems, and high-frequency power electronics. Approximately 79% of global gallium supply was sourced from China as of 2023, and the subsequent introduction of Chinese export licensing requirements for gallium and germanium that same year served as a watershed moment, demonstrating precisely how a licensing regime could be deployed to restrict supply with minimal diplomatic forewarning.

Magnesium, Germanium, and Graphite: The Secondary Consideration Tier

Beyond the first-tier priorities, reports indicate that magnesium, germanium, and graphite are under active consideration for inclusion in broader stockpile frameworks.

Magnesium is indispensable in aerospace and automotive manufacturing due to its unique strength-to-weight ratio, yet China accounts for roughly 85–90% of global magnesium production, a figure that left European automotive manufacturers acutely exposed during the 2021 supply crisis triggered by Chinese energy rationing at smelting facilities. Germanium, alongside gallium, became subject to Chinese export controls in 2023, and its applications in fibre optic cables, infrared optics, and satellite imagery systems make it a high-sensitivity material from a defence perspective. Natural graphite, where China controls over 70% of global supply, is the dominant anode material in lithium-ion batteries, making it central to both the European electric vehicle transition and grid-scale energy storage ambitions.

The table below illustrates how each mineral maps to specific end-use sectors and the nature of its supply risk:

| Mineral | Primary End-Use Applications | Key Supply Risk |

|---|---|---|

| Tungsten | Defence armaments, cutting tools, electronics | ~80% China production dominance |

| Rare Earth Elements | EV motors, wind turbines, defence guidance systems | ~95% EU import dependency |

| Gallium | Semiconductors, 5G, military radar | ~79% China-sourced (2023) |

| Magnesium | Aerospace, automotive lightweighting | ~85–90% Chinese production |

| Germanium | Fibre optics, infrared optics, semiconductors | Active Chinese export controls |

| Graphite | EV battery anodes, nuclear applications | China controls >70% of supply |

Why These Minerals Appear on NATO's Critical Materials List

The alignment between NATO's critical materials designations and the EU's stockpile prioritisation is not coincidental. Both frameworks apply a similar criticality assessment methodology that evaluates materials across three primary dimensions: economic importance to strategic industries, supply concentration risk, and the absence of technically and economically viable substitutes at industrial scale.

Materials that score highly across all three dimensions, as tungsten, REEs, and gallium unambiguously do, become candidates for the most urgent policy intervention. The defence dimension is particularly salient: modern weapons platforms, electronic warfare systems, and communications infrastructure all incorporate REE-based permanent magnets and gallium-based semiconductors in configurations where substitution would require fundamental redesign rather than incremental material replacement.

How Exposed Is Europe? A Data-Driven Assessment

Mapping the 95% Rare Earth Import Concentration Problem

The scale of Europe's rare earth dependency becomes most apparent when examined at the processing level rather than the extraction level. While there are rare earth deposits in countries across Europe, Scandinavia, and allied nations, the absence of domestic separation and refining infrastructure means that even domestically mined ores would typically require export for processing before returning as usable materials.

This creates a structural vulnerability that mining activity alone cannot resolve without parallel investment in downstream processing, an infrastructure gap that the EU has only recently begun to address in earnest. Consequently, initiatives such as the critical raw materials facility have become central to the broader policy response, bridging the gap between extraction ambition and processing reality.

European manufacturers in sectors ranging from wind energy to defence electronics operate with virtually no diversified fallback in the event of coordinated rare earth export restrictions, a vulnerability that supply chain modelling consistently identifies as one of the continent's highest-magnitude strategic risks.

In 2024, available data suggested that 95% of EU rare earth element imports originated from just three countries: China, Malaysia, and Russia, leaving the European industrial base with a dependency profile that most risk frameworks would characterise as dangerously concentrated. The Malaysia component of this dependency is itself partly an artefact of Chinese processing capacity that has been geographically relocated, meaning the true effective concentration of Chinese influence over Europe's rare earth supply chains is arguably even higher than the headline figure suggests.

Gallium Supply Chains: What the 79% China Dependency Figure Really Means

Gallium's dependency profile carries particular significance because of its invisibility within conventional trade data. As a byproduct of aluminium and zinc smelting, gallium does not appear in standard commodity classifications with the same prominence as bulk metals, meaning its supply chain vulnerabilities were historically underweighted in strategic assessments.

China's ability to produce gallium at scale is a direct function of its dominance in aluminium production, which processes bauxite containing trace concentrations of gallium that are recovered during the Bayer process. The 79% supply concentration figure therefore reflects not merely a market share statistic but a structural reality rooted in the economics of coproduction: unless primary metal production scales up in alternative jurisdictions, gallium supply cannot easily migrate away from its current geographic concentration.

This characteristic, known in mineral economics as byproduct dependency, represents one of the most underappreciated dimensions of critical mineral vulnerability because it cannot be resolved purely through investment in dedicated gallium mining, as no economically viable primary gallium ore deposit has yet been identified.

Comparing EU Mineral Dependency to the United States and Japan

Europe's exposure, while severe, exists within a broader pattern of Western vulnerability to critical mineral supply concentration that makes coordinated allied responses both more urgent and more viable. The United States imports approximately 80% of its rare earth requirements, with significant processing dependency on China despite recent domestic mine restarts.

Japan, which lacks significant domestic mineral resources, has historically been the most aggressive among major economies in developing formal stockpile programmes and strategic sourcing partnerships. Indeed, Japan established REE reserve programmes following the 2010 China-Japan territorial dispute that triggered a temporary Chinese rare earth export restriction, causing prices to spike by several hundred percent within months. These comparative profiles reinforce the case for allied coordination, helping explain why the EU's stockpiling initiative is being developed with explicit consideration of how it aligns with parallel initiatives undertaken by Washington and Tokyo.

Who Is Leading the EU Stockpiling Initiative?

Italy, France, and Germany as Founding Coordination Leaders

The political architecture of the EU's stockpiling initiative reflects the broader power dynamics of European industrial policy, with Italy, France, and Germany emerging as the primary coordination leaders among the ten member states currently participating in the planning process. Each of these nations brings distinct strategic interests to the initiative.

France's nuclear energy sector creates specific demand for materials including graphite and certain REEs; Germany's automotive and engineering industries generate acute exposure to tungsten and magnesium supply disruptions; and Italy's defence industrial base, alongside its significant manufacturing sector, creates comprehensive exposure across multiple mineral categories.

The participation of ten member states in coordinated planning represents a significant multilateral commitment, though it also means that seventeen EU member states remain outside the current coordination framework, raising questions about whether the initiative can achieve the scale necessary to function as a genuine strategic reserve rather than a collection of national buffers dressed in European institutional clothing.

France's Push for a Permanent Stockpile Secretariat

Among the most consequential governance debates currently underway is France's advocacy for the establishment of a permanent EU stockpile secretariat with dedicated administrative capacity, technical expertise, and coordination authority. This proposal represents a fundamental philosophical commitment to institutional depth over bureaucratic minimalism, recognising that the complexity of managing multi-mineral reserves across 27 member states cannot be adequately handled through rotating national presidencies.

Whether the EU establishes a permanent secretariat or persists with rotating coordination responsibilities will likely determine whether this initiative achieves durable strategic coherence or fragments into a collection of loosely aligned national programmes with insufficient collective impact.

The secretariat debate also touches upon the fundamental tension within European integration between supranational authority and national sovereignty in areas traditionally considered matters of economic security, with smaller member states potentially concerned about ceding control over strategic material decisions to an institution dominated by the preferences of larger industrial economies.

Why Rotating Presidencies Are Considered an Inadequate Governance Model

The structural limitations of rotating presidency coordination models in managing strategic mineral reserves extend beyond institutional memory to encompass technical expertise, market knowledge, and diplomatic relationships with supplier nations. Effective stockpile management requires continuous monitoring of global supply conditions, ongoing engagement with mining companies and processing facilities, and the technical capacity to assess material quality, storage conditions, and inventory management.

These functions require persistent institutional capability that cannot be credibly maintained through a coordination model that changes leadership every six months and relies on seconded national civil servants without dedicated mineral expertise. Japan's experience with its REE reserve programme, managed through dedicated institutional structures with established industry relationships, provides a useful comparison point illustrating how institutional continuity contributes to programme effectiveness.

Where Will Europe Store Its Strategic Mineral Reserves?

The Port of Rotterdam as a Leading Candidate

The Port of Rotterdam has emerged as a prominent candidate for hosting European strategic mineral reserves due to a combination of physical infrastructure advantages, established logistics networks, and geographic accessibility. As Europe's critical minerals supply chain continues to develop, Rotterdam's position as the continent's largest port by cargo volume makes it an obvious hub, with existing warehousing infrastructure, chemical handling facilities, and deep-water berths capable of accommodating the diverse vessel types involved in global mineral trade.

Its established position within European bulk commodity logistics also means that the institutional knowledge, customs frameworks, and supply chain relationships necessary for effective stockpile management already exist in concentrated form within the port's operational ecosystem.

Infrastructure Requirements for Safe Mineral Storage

The technical requirements for storing critical minerals are considerably more demanding than those for conventional commodity reserves such as grain or petroleum. Rare earth elements in oxide or carbonate form require controlled humidity storage environments to prevent degradation and clumping; gallium, which is a liquid metal at slightly above room temperature, requires specific temperature-controlled containment; and certain graphite forms require segregated storage to prevent cross-contamination.

The infrastructure investment required to establish standards-compliant storage for a multi-mineral strategic reserve represents a non-trivial capital commitment, and decisions about storage specification will have significant implications for both the cost of the programme and the usable quality of reserves when they are eventually drawn down.

Comparing EU Plans to Established National Stockpile Programs

The EU's emerging approach can be contextualised against the longer-established strategic reserve programmes operated by allied nations:

| Country/Bloc | Stockpile Program | Key Materials Held | Governance Model |

|---|---|---|---|

| United States | National Defense Stockpile | ~50 strategic materials | DoD-managed, congressionally funded |

| Japan | Rare Earth Reserve Program | REEs, lithium, others | Government-industry co-financing |

| South Korea | Resource Security Program | Lithium, nickel, cobalt | State enterprise-led |

| European Union | Proposed CRM Stockpile | Tungsten, REEs, gallium + | Multi-member coordination (emerging) |

A critical observation from this comparison is that all mature national stockpile programmes have dedicated institutional structures with clear legislative mandates, defined funding mechanisms, and unambiguous accountability frameworks. The EU's initiative currently lacks these structural foundations, making the governance debate not merely procedural but foundational to whether the programme achieves meaningful strategic impact.

How Does This Relate to the EU's Critical Raw Materials Act?

CRMA Benchmarks and Their Connection to Stockpile Prioritisation

The Critical Raw Materials Act, which entered into force in 2024, established quantitative benchmarks for reducing European dependency on single-source suppliers: by 2030, no more than 65% of EU consumption of any strategic raw material should originate from a single third country, and the EU should domestically extract at least 10% of its annual consumption of strategic materials. These benchmarks provide the regulatory framework within which the stockpiling initiative operates.

The CRMA Round Two selection process, which is due to conclude in Autumn 2026 according to industry reporting, will expand the list of materials designated as strategic raw materials under the Act. The alignment between this selection process and stockpile prioritisation decisions is significant: materials elevated to strategic status under CRMA Round Two are likely candidates for subsequent inclusion in the stockpile framework.

Domestic Extraction Versus Strategic Reserves as Complementary Pillars

A critical conceptual distinction that is sometimes obscured in public commentary is that domestic extraction and strategic stockpiling are complementary rather than competing policy instruments. Domestic mining development addresses structural supply chain vulnerability over decade-scale timeframes, requiring environmental assessment, permitting, infrastructure development, and operational ramp-up that cannot be compressed below multi-year horizons regardless of political urgency.

Strategic stockpiles, by contrast, provide immediate buffer capacity that can be deployed within days or weeks of a supply disruption, buying time for market alternatives to emerge and diplomatic solutions to be pursued. The EU's two-track approach, combining CRMA-driven domestic production growth with stockpile-based emergency reserve capacity, reflects a sophisticated understanding of this temporal complementarity.

The next major ASX story will hit our subscribers first

China's Export Control Strategy and European Urgency

The Gallium and Germanium Restriction Timeline

China's introduction of export licensing requirements for gallium and germanium in August 2023 represented a watershed moment in the geopolitics of critical mineral supply chains. The restrictions did not constitute an outright export ban but instead created a licensing and approval process that introduced timing uncertainty, administrative friction, and implicit conditionality into supply relationships that had previously operated on purely commercial terms.

China subsequently expanded its export control framework in 2024 to include additional materials including certain rare earth processing technologies, reinforcing the pattern and providing European policymakers with a concrete and recent case study in how resource dependency translates into geopolitical leverage. As analysts have noted, the speed with which these controls were implemented highlighted the inadequacy of relying on historical commercial relationships as a proxy for supply security.

The Semiconductor Supply Chain at Particular Risk

The intersection of gallium dependency and semiconductor supply chain vulnerability deserves particular analytical attention because it illustrates a compounding risk dynamic that extends well beyond the immediate material in question. Modern compound semiconductors based on gallium nitride and gallium arsenide are not interchangeable with silicon-based alternatives for high-frequency, high-power, and high-temperature applications.

The 5G radio access networks being deployed across Europe rely on gallium nitride power amplifiers; military radar and electronic warfare systems depend on gallium arsenide monolithic microwave integrated circuits; and next-generation power electronics for electric vehicle charging infrastructure increasingly incorporate gallium nitride switching devices. A sustained gallium supply disruption would therefore simultaneously affect civilian telecommunications infrastructure, defence electronics manufacturing, and green technology deployment, creating a multi-sector cascade that no single ministry could contain within its own policy remit.

Rare Earth Processing Bottlenecks Beyond Mining

One of the most technically important and least publicly understood dimensions of the rare earth supply challenge is that mining is the relatively straightforward part of the problem. Rare earth elements occur together in ore bodies and must be separated from each other through a complex solvent extraction process that requires sophisticated chemical engineering expertise, significant capital investment in processing infrastructure, and the management of radioactive byproducts including thorium and uranium.

China's dominance in this processing capacity, developed over three decades through deliberate industrial policy, cannot be replicated quickly elsewhere regardless of how much investment is directed toward it. This reality substantially elevates the strategic value of stockpiles that hold processed materials rather than ores, as the former represent immediately deployable supply rather than raw inputs requiring further transformation.

Broader Geopolitical Implications

Friend-Shoring and the Architecture of Allied Mineral Security

The EU's stockpiling initiative exists within a broader Western strategic framework that has come to be described as friend-shoring: the deliberate reorientation of supply chains toward politically aligned nations with compatible governance standards, transparent rule of law, and reduced risk of weaponised supply restriction. This framework explicitly acknowledges that full supply chain independence is neither achievable nor necessarily desirable, but that the specific risk of dependency on strategically adversarial suppliers can be mitigated through coordinated sourcing from allies.

Brazil, Canada, and Australia represent the most significant potential alternative supply partners for multiple categories of critical minerals. Australia possesses significant tungsten, rare earth, and lithium resources; Canada offers titanium, cobalt, and REE deposits; and Brazil holds the world's largest niobium reserves alongside significant REE and graphite resources.

Could EU Stockpiling Trigger Retaliatory Trade Measures?

A speculative but analytically legitimate concern is that large-scale EU government purchasing of minerals currently dominated by Chinese production could accelerate Beijing's consideration of further export restrictions, as stockpiling programmes explicitly signal that importers are preparing to operate without Chinese supply. This dynamic introduces a first-mover risk calculation into the timing and communication of stockpile acquisition strategies.

Purchasing too visibly and too rapidly may precipitate the very supply restriction the stockpile is designed to hedge against, while purchasing too slowly may leave reserves insufficiently established when restrictions are eventually imposed. The management of this signalling challenge represents one of the most diplomatically sophisticated aspects of the stockpile programme's implementation and will require close coordination between trade policy ministries and the initiative's operational leadership.

Challenges That Could Derail the Program

Financing Gaps and Cost Estimation

Estimating the cost of a comprehensive multi-mineral strategic reserve for a bloc of 27 member states with diverse industrial profiles is inherently complex, but preliminary assessments suggest the figure could reach into the tens of billions of euros depending on the scope of materials covered, target inventory levels measured in weeks or months of consumption, and the market conditions prevailing during acquisition.

The financing question intersects with fundamental issues of EU institutional architecture: whether funding should come from the EU budget, from member state contributions on a formula basis, from debt instruments issued through the European Investment Bank, or from some combination of public and private capital through co-investment structures. Each funding model carries different implications for governance, accountability, and the balance of power between member states with large industrial sectors and those with smaller material requirements.

The Risk of Market Distortion Through Government Procurement

Large-scale government purchasing of critical minerals carries a genuine risk of generating artificial price spikes that disadvantage the downstream manufacturers the stockpile is designed to protect. Without carefully sequenced acquisition strategies that avoid telegraphing purchasing intentions to commodity markets, the cure may intensify the very vulnerability it targets.

This market distortion risk is particularly acute for smaller, more illiquid mineral markets such as gallium and germanium, where annual global production volumes are measured in hundreds of tonnes rather than millions. The US National Defense Stockpile has historically grappled with analogous distortion effects, particularly during drawdown phases where government sales suppressed prices and discouraged private sector investment in domestic production, a dynamic that European programme designers would be wise to study carefully.

Political Fragmentation Across 27 Member States

The structural diversity of the EU membership creates genuine coordination challenges that extend beyond differences in industrial profiles to encompass divergent strategic cultures, varied relationships with China as a trading partner, and different domestic political pressures regarding resource security spending. Member states with significant existing trade relationships with China may resist aspects of the stockpiling framework that could be interpreted as provocative, while those with closer geopolitical alignment to US positions on China policy may favour more aggressive approaches.

Achieving the consensus necessary to establish a well-resourced, credibly governed reserve programme across this political spectrum represents one of the initiative's most significant non-technical challenges.

Frequently Asked Questions: EU Critical Mineral Stockpiling

What is the EU's critical mineral stockpiling program?

The EU's critical mineral stockpiling programme is an initiative coordinated among a group of member states, with Italy, France, and Germany as leading participants, to establish physical reserves of strategic minerals whose supply is concentrated in potentially adversarial or geopolitically fragile jurisdictions. The programme focuses initially on EU stockpiling of tungsten, rare earths, and gallium, with magnesium, germanium, and graphite under active consideration for inclusion.

Why is tungsten a priority for European strategic reserves?

Tungsten's irreplaceability in defence applications, including armour-piercing ammunition and high-performance industrial cutting tools, combined with China's approximately 80% share of global production, makes it a first-tier strategic priority. Its extreme melting point means no currently available material performs comparably across its key applications, making substitution technically impractical at the timescales relevant to supply disruption scenarios.

How does gallium dependency affect European semiconductor manufacturing?

Gallium-based compound semiconductors are essential components in 5G infrastructure, military radar, satellite communications, and high-power electronics. With approximately 79% of global gallium supply originating from China as of 2023, and Chinese export licensing controls now operational, European manufacturers of these systems face material supply uncertainty that cannot be resolved through short-term market alternatives due to gallium's unique status as an aluminium smelting byproduct without viable primary ore sources.

Which EU member states are leading the stockpile coordination effort?

Italy, France, and Germany are identified as the founding coordination leaders, with ten member states total currently participating in the planning architecture. The governance structure remains under development, with France advocating for a permanent secretariat while the debate over institutional design continues.

How does the EU stockpile initiative differ from the US National Defense Stockpile?

The US National Defense Stockpile is managed by the Department of Defense with a congressionally mandated and funded structure covering approximately 50 strategic materials, representing decades of institutional development. The EU's initiative is at an earlier stage with a less formalised governance architecture, a more limited number of participating states, and an unresolved debate over permanent versus rotating coordination structures. However, the EU programme explicitly targets materials of joint civilian and defence relevance, reflecting Europe's integrated approach to industrial and security policy.

When is the EU expected to finalise its stockpile list and governance structure?

A definitive timeline has not been publicly confirmed. The CRMA Round Two selection process, expected to conclude in Autumn 2026, is likely to inform further prioritisation decisions. Governance structure finalisation will depend on the outcome of ongoing negotiations between member states regarding the proposed permanent secretariat model.

What impact could EU stockpiling have on global rare earth prices?

Large-scale government procurement in illiquid mineral markets carries genuine price distortion risk. For rare earths, where individual element markets can be relatively thin, concentrated purchasing by a major importer could create temporary price spikes. However, well-managed phased acquisition strategies that avoid telegraphing procurement intentions to commodity markets can substantially mitigate this effect. Longer term, the initiative may create positive demand signals for non-Chinese producers, potentially incentivising new project development in allied nations.

Investment and Industry Implications

Upstream Beneficiaries and Long-Term Demand Signals

For mining companies operating in tungsten, REE, and gallium value chains outside China, the EU stockpiling of tungsten, rare earths, and gallium represents a structural demand catalyst of potentially significant magnitude. The programme creates guaranteed offtake demand independent of cyclical industrial consumption, a fundamentally different demand driver than conventional market forces and one that may justify investment in projects whose economics would be marginal purely on commercial grounds.

Tungsten mining operations in Europe, including the Hemerdon deposit in the United Kingdom and the Mittersill mine in Austria, alongside REE exploration projects in Scandinavia and the Iberian Peninsula, stand to benefit from both the direct procurement demand generated by stockpile building and the broader policy signal that European authorities are prepared to support domestic and allied-nation production.

The byproduct dimension of gallium supply, however, means that investors seeking exposure to gallium supply chain development should be looking at aluminium and zinc producers in non-Chinese jurisdictions rather than dedicated gallium mining companies. Understanding this byproduct dynamic is one of those areas of mineral market knowledge that separates sophisticated sector investors from those who approach critical mineral themes through conventional mining investment frameworks.

Downstream Exposure Among European Manufacturers

European manufacturers most exposed to the supply vulnerabilities the stockpile is designed to address include defence electronics producers, wind turbine manufacturers, electric vehicle component suppliers, and telecommunications equipment manufacturers. These companies collectively represent some of the continent's most economically significant industrial sectors, and their continued competitiveness is directly contingent on reliable access to REEs, gallium, and tungsten at commercially sustainable prices.

The stockpile programme's success would provide these manufacturers with a degree of supply security that currently forces them to maintain expensive private inventory buffers or accept supply chain risk that is not fully reflected in their cost structures.

The Case for Investment in European Domestic Mining Projects

The policy environment created by the combination of the CRMA and the stockpiling initiative generates meaningful long-term demand signals for domestic European mineral projects. While permitting timelines remain lengthy and social licence challenges persist across multiple European jurisdictions, the direction of policy travel clearly favours investment in domestic extraction and processing capacity.

Projects that can demonstrate alignment with both CRMA strategic material designations and stockpile priority categories occupy an increasingly attractive position within the European industrial policy landscape, with multiple funding mechanisms potentially available to support development. Investors with sufficient sector expertise to distinguish between projects with genuine geological merit and those whose appeal is primarily driven by policy momentum will be positioned to identify opportunities in this space before broader market recognition elevates valuations.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts, projections, and assessments of policy outcomes involve inherent uncertainty and should not be relied upon as the basis for investment decisions. Readers should conduct independent research and seek professional advice appropriate to their specific circumstances before making any investment decisions related to the critical minerals sector or the companies and initiatives discussed herein.

Want to Capitalise on the Next Major Critical Minerals Discovery Before the Market Catches On?

The accelerating demand for tungsten, rare earth elements, and gallium driven by European strategic stockpiling is creating significant opportunities in ASX-listed exploration and mining companies — and Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly alerting subscribers to significant mineral discoveries across these and 30+ other commodities before the broader market reacts. Explore historic examples of major mineral discoveries and their market returns, then begin your 14-day free trial to position yourself ahead of the next transformative find.