July 23, 2026

The Supply Chain Fault Line That Western Industry Can No Longer Ignore

For decades, the global rare earth industry operated under a quiet assumption: that Chinese processing dominance was simply a cost-of-doing-business reality, not a strategic vulnerability. That assumption has been systematically dismantled over the past five years. Today, as Western governments and defence contractors confront the hard arithmetic of supply chain exposure, the race to establish non-Chinese rare earth pipelines has moved from policy discussion to commercial urgency. The Critical Metals REalloys Tanbreez rare earth deal, formalised in May 2026, represents one of the most structurally significant steps yet taken in that race.

When big ASX news breaks, our subscribers know first

China's Processing Grip and the Heavy Rare Earth Problem

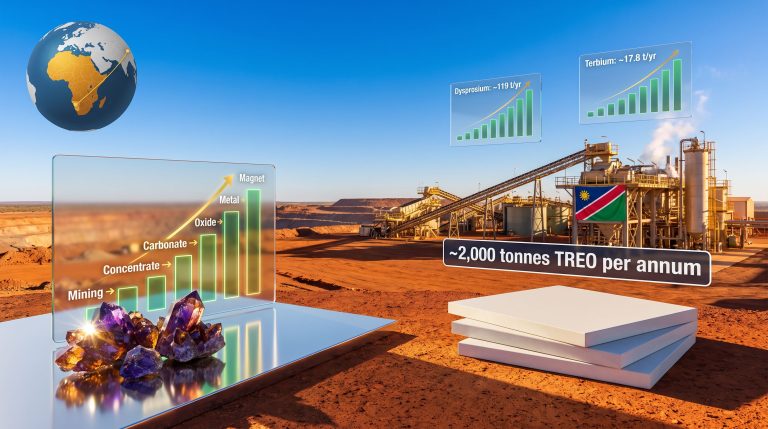

China controls an estimated 85 to 90 percent of global rare earth processing capacity, but the leverage is even more concentrated when it comes to heavy rare earth elements (HREEs). Unlike light rare earths such as cerium and lanthanum, which are relatively abundant and processed in several countries, HREEs like dysprosium and terbium are extracted from a far narrower range of deposits globally, with Chinese ionic clay deposits in provinces such as Jiangxi historically accounting for the dominant share of global supply.

This concentration creates a strategic chokepoint. The permanent magnets used in electric vehicle motors, wind turbine generators, missile guidance systems, and advanced robotics depend on dysprosium and terbium to maintain magnetic performance at elevated operating temperatures. Without these elements, next-generation defence and clean energy systems simply cannot be built to specification. Consequently, understanding rare earth supply chains has become essential for policymakers and investors alike.

Why Dysprosium, Terbium, and Yttrium Sit at the Centre of a New Resource Race

The criticality of individual rare earth elements is often misunderstood by investors and policymakers alike. Not all rare earths carry equal strategic weight. The following elements represent the highest-priority targets for Western supply chain development:

| Element | Primary Application | Why It's Strategically Critical |

|---|---|---|

| Dysprosium (Dy) | EV motors, wind turbines, defence magnets | Maintains magnet strength at high temperatures |

| Terbium (Tb) | Permanent magnets, solid-state lighting | Extremely limited non-Chinese supply |

| Yttrium (Y) | Electronics, high-performance alloys, medical lasers | Broad defence and industrial applications |

| Hafnium (Hf) | Nuclear reactors, semiconductor fabrication | Among the world's most constrained strategic metals |

| Niobium (Nb) | High-strength steel, superconductors | Critical for aerospace and energy infrastructure |

| Zirconium (Zr) | Nuclear fuel cladding, advanced ceramics | Strategic defence and industrial utility |

What makes the Tanbreez deposit in Southern Greenland exceptional is that it hosts meaningful concentrations of all six of these elements within a single geological system, a characteristic that is genuinely rare among known global deposits.

The Tanbreez Project: Scale, Geology, and Strategic Positioning

Location and Deposit Characteristics

The Tanbreez REE deposit is situated in Southern Greenland, a jurisdiction that has attracted intensifying international interest for its mineral endowment. The deposit is hosted within an alkaline igneous complex, a geological setting associated with enrichment in rare earth elements, zirconium, hafnium, and niobium. Alkaline complexes of this type tend to produce large-tonnage, lower-grade deposits rather than the narrow high-grade veins more common in other mineral systems, which has important implications for mining economics and production continuity.

Critically, the HREE fraction at Tanbreez is weighted toward the elements carrying the highest strategic premiums. This is a non-trivial distinction. Many rare earth deposits globally are dominated by light rare earth elements such as cerium and lanthanum, which are abundant and carry relatively low prices. A deposit with genuine HREE enrichment, particularly in dysprosium and terbium, represents a fundamentally different value proposition.

The Tanbreez deposit in Southern Greenland is regarded as one of the world's largest heavy rare earth deposits, hosting significant concentrations of dysprosium, terbium, yttrium, hafnium, niobium, zirconium, cerium, and lanthanum. These are minerals critical to defence applications, clean energy infrastructure, and advanced manufacturing systems.

How Critical Metals Corp Secured Majority Ownership

The path from initial engagement to binding commercial agreement followed a structured escalation over roughly seven months:

| Milestone | Date | Detail |

|---|---|---|

| Initial Letter of Intent with REalloys | October 2025 | 10-year non-binding LOI for 15% of projected output |

| Greenland Government Ownership Approval | April 2026 | Critical Metals permitted to raise its stake to 92.5% |

| Binding 15-Year Offtake Agreement with REalloys | May 2026 | Formalised supply deal with priority HREE access |

| Ucore Rare Metals Offtake (10% of output) | Prior to May 2026 | Second committed U.S. customer secured |

| Total Committed U.S. Offtake | As of May 2026 | 25% of projected Tanbreez annual production |

The Greenland government's approval in April 2026 permitting Critical Metals to raise its ownership stake to 92.5 percent was a pivotal moment. Greenland critical minerals governance has historically maintained sovereignty-conscious oversight of its mineral estate, and government approval for foreign majority ownership at this scale reflects both the project's economic significance and the regulatory confidence built over years of engagement.

Unpacking the Critical Metals REalloys Offtake Agreement

What a 15-Year Rare Earth Supply Deal Actually Represents

Offtake agreements in the mining sector serve as bankable instruments. They provide revenue certainty that supports project financing, underpin feasibility assumptions, and signal market confidence to institutional investors. In the rare earth sector specifically, long-duration offtake agreements are exceptionally uncommon outside of Chinese domestic supply chains, precisely because Western demand has historically been fragmented and project development timelines uncertain.

A 15-year binding agreement therefore carries structural significance beyond its headline commercial terms. It represents a mutual commitment to capital deployment, supply chain planning, and long-term production continuity that short-term agreements cannot replicate. Critical Metals Corp's acquisition of the Tanbreez project underscores just how seriously Western players are taking these long-term supply chain commitments.

Key Commercial Terms of the REalloys Deal

The agreement allocates 15 percent of Tanbreez's annual rare earth concentrate production to REalloys, with several commercially sophisticated provisions embedded within the structure:

-

Priority access to HREE-enriched fractions: REalloys does not simply receive a proportional share of all concentrate. The agreement prioritises heavy rare earth element volumes, ensuring access to the highest-value material streams including dysprosium and terbium.

-

Right of First Refusal (ROFR): REalloys retains the contractual right to acquire additional material beyond its base allocation before it is offered to other buyers. This effectively positions REalloys to scale its Tanbreez feedstock position as production ramps.

-

Two optional five-year extensions: The base 15-year term can be extended by up to a decade, providing REalloys with long-term supply visibility that aligns with its manufacturing investment horizons.

-

Benchmark-linked pricing: Commercial pricing will be calculated against global rare earth oxide benchmarks on an element-specific basis, ensuring both parties are exposed to market price discovery rather than fixed-price arrangements that could become commercially unworkable over a 15-year horizon.

Offtake agreements of this duration, particularly those incorporating priority access to heavy rare earth fractions and Right of First Refusal provisions, are structurally uncommon in the Western rare earth landscape. Their inclusion signals a genuine intent by REalloys to build Tanbreez into a cornerstone feedstock position within its North American supply chain architecture.

REalloys and the Mine-to-Magnet Supply Chain Vision

Understanding the Mine-to-Magnet Model

The term mine-to-magnet describes a vertically integrated rare earth supply chain that connects upstream ore extraction directly to downstream magnet manufacturing, bypassing the Chinese processing and separation intermediaries that currently control the middle stages of the global value chain. Achieving genuine mine-to-magnet capability requires simultaneous execution across multiple complex disciplines: mining, chemical separation, alloying, and precision manufacturing.

REalloys is pursuing this model through a two-pronged feedstock strategy. Its Hoidas Lake rare earth project in Saskatchewan, Canada, provides a domestic North American ore source, while the Critical Metals REalloys Tanbreez rare earth deal adds an internationally diversified HREE supply layer. Combined, these feedstock arrangements are designed to underpin REalloys' Ohio-based manufacturing operations, which supply end-users including the U.S. Department of Defense, the Department of Energy, and NASA.

Why Secure Feedstock Is the Prerequisite for Everything Downstream

A magnet manufacturing facility operating without a secured rare earth feedstock pipeline is structurally vulnerable. Spot market purchases expose manufacturers to price volatility, supply interruption risk, and geopolitical leverage, all of which are materially heightened in the current environment given China's demonstrated willingness to restrict rare earth exports as a trade policy instrument. Long-term agreements like the Tanbreez offtake are not merely procurement conveniences; they are the foundational conditions that make downstream manufacturing investment viable.

The Regulatory Catalyst: U.S. Defence Procurement Rules from 2027

The Policy Deadline Reshaping Western Supply Chain Strategy

The United States is in the process of tightening defence procurement standards in a manner that will, from 2027 onwards, effectively prohibit Chinese-origin rare earth materials from entering strategic military and industrial supply chains. This regulatory transition is creating a hard deadline for Western rare earth projects seeking to qualify as compliant feedstock sources. Furthermore, America's rare earth supply chain development is now being treated as a matter of national security rather than simply industrial policy.

The United States is moving to tighten defence procurement standards from 2027, effectively prohibiting Chinese-origin rare earth materials from entering strategic military and industrial supply chains. Commercial agreements structured around non-Chinese rare earth sources are being developed in direct anticipation of these procurement restrictions.

For Critical Metals and REalloys, the timing of the Critical Metals REalloys Tanbreez rare earth deal is not incidental. Establishing binding commercial relationships now, while Tanbreez advances toward production, positions both parties to be procurement-compliant before the regulatory clock runs out. Projects that fail to establish Western-aligned supply agreements ahead of the 2027 threshold face the prospect of being excluded from the most lucrative segment of the rare earth demand curve.

Greenland's Geopolitical Dimension

Greenland's mineral estate has become a focal point of geopolitical interest that extends well beyond commercial mining. Its Arctic geography, substantial critical mineral endowments, and complex sovereignty relationship with Denmark have made it a territory of strategic significance to multiple Western nations. The broader context of rare earth geopolitics is reshaping how Western governments view Arctic mineral assets. However, investors should be careful to distinguish between policy-level interest in the region and project-specific commercial or regulatory support, which must be evaluated on its own merits.

Where Tanbreez Sits Among Western HREE Development Efforts

| Project | Location | Key HREEs | Status | Western Offtake |

|---|---|---|---|---|

| Tanbreez | Southern Greenland | Dy, Tb, Y, Hf, Nb, Zr | Permitted, pre-production | REalloys (15%), Ucore (10%) |

| Hoidas Lake | Saskatchewan, Canada | Mixed REE | Development stage | REalloys (internal) |

| Other Western HREE Projects | Various | Variable | Various stages | Limited committed offtake |

The combination of deposit scale, HREE weighting, majority ownership structure, and 25 percent committed offtake from two independent U.S. customers distinguishes Tanbreez from most Western alternatives at a comparable stage of development.

The next major ASX story will hit our subscribers first

Market Reaction: What the Share Price Movements Reveal

Critical Metals Corp (NASDAQ: CRML) and REalloys: Reading the Rally

Critical Metals Corp shares surged approximately 10 percent following the announcement, while REalloys shares climbed 7 percent. The symmetry of the rally is instructive. In most supply agreements, value creation is perceived as flowing primarily to one party, typically the buyer securing supply certainty. Here, both parties experienced meaningful market re-rating, reflecting investor recognition that the deal creates strategic value on both sides of the transaction. Industry coverage of this offtake milestone further underscores the deal's significance within the sector.

For Critical Metals, the market signal was a validation of the commercialisation thesis: that Tanbreez's HREE endowment can be converted into durable, bankable revenue agreements with qualified Western buyers. For REalloys, the share price response reflected market confidence in the company's ability to secure the upstream feedstock necessary to credibly execute its mine-to-magnet strategy.

Is the Rally Sustainable? Key Milestones That Will Drive Future Valuation

Investors should note that announcement-day share price movements reflect sentiment, not delivery. The milestones that will determine whether current valuations are justified include:

-

Commencement of commercial production at Tanbreez and first FOB shipments from Southern Greenland's port facilities.

-

Additional offtake agreements for the remaining 75 percent of Tanbreez's projected annual output, which remains uncommitted as of the announcement date.

-

Successful separation and processing of HREE concentrate into individual oxide streams at commercially viable recovery rates.

-

REalloys' progression of its Ohio manufacturing operations toward full-scale production serving DoD and other strategic customers.

-

Regulatory confirmation that Tanbreez-sourced material qualifies under forthcoming U.S. defence procurement sourcing requirements.

Disclaimer: Share price movements discussed in this article reflect historical market data at the time of announcement. Past performance is not indicative of future results. This article does not constitute financial advice. Investors should conduct their own due diligence before making investment decisions.

The Strategic Architecture of the Tanbreez Deal

From Letter of Intent to Binding Contract: The Commercialisation Arc

The progression from the October 2025 Letter of Intent to a binding 15-year agreement in May 2026 illustrates a commercialisation discipline that is worth examining. Many rare earth development projects accumulate non-binding memoranda of understanding without converting them into contractual commitments. The Tanbreez timeline, moving from LOI to Greenland government ownership approval to binding offtake within approximately seven months, demonstrates an execution velocity that distinguishes it from slower-moving peers.

The Remaining 75 Percent: The Deal's Most Consequential Open Question

With 25 percent of projected annual output now committed to two U.S. buyers, the commercial trajectory of Tanbreez will ultimately be determined by what happens to the remaining three-quarters of production. Several scenarios are plausible:

-

Additional long-term offtake agreements with European or Japanese buyers seeking to diversify rare earth supply away from Chinese sources.

-

Spot market sales during early production phases, carrying higher price realisation potential but lower revenue certainty.

-

Vertical integration moves by Critical Metals itself into separation or downstream processing, capturing additional margin within the value chain.

-

Strategic partnerships with allied-nation governments or sovereign wealth vehicles seeking to secure rare earth supply access.

Each pathway carries distinct risk and return profiles, and the eventual configuration of the remaining offtake will be a primary driver of long-term project valuation.

Three Factors That Will Determine Whether This Deal Delivers on Its Promise

-

Production execution: Tanbreez's geological endowment is well-established, but converting a large-scale alkaline complex deposit into a reliable concentrate stream requires metallurgical process development, capital deployment, and operational discipline that remain to be demonstrated at commercial scale.

-

Pricing environment: The deal's benchmark-linked pricing structure means that revenue realisation will track global HREE oxide markets. Dysprosium and terbium prices are subject to significant volatility, influenced by Chinese export policy, EV demand trajectories, and wind energy installation rates.

-

Regulatory compliance qualification: Formal confirmation that Tanbreez material satisfies U.S. defence procurement sourcing requirements will be a critical de-risking event. Until that confirmation is obtained, the policy tailwind remains a potential rather than a guaranteed commercial advantage.

Frequently Asked Questions

What is the Tanbreez rare earth project?

Tanbreez is a large-scale rare earth deposit located in Southern Greenland, hosted within an alkaline igneous complex. It is considered one of the world's largest heavy rare earth deposits, with significant concentrations of dysprosium, terbium, yttrium, hafnium, niobium, zirconium, cerium, and lanthanum. Critical Metals Corp holds a 92.5 percent ownership stake following Greenland government approval in April 2026.

What percentage of Tanbreez output is now committed under offtake agreements?

As of May 2026, 25 percent of projected annual production is covered by binding agreements: 15 percent allocated to REalloys under the newly announced 15-year deal, and 10 percent previously committed to Ucore Rare Metals.

What is a Right of First Refusal in a rare earth offtake agreement?

A Right of First Refusal grants the holder, in this case REalloys, the contractual right to purchase additional material beyond its base allocation before the seller can offer that material to third parties. In practice, it functions as an option to scale feedstock access as production ramps, without requiring an immediate financial commitment to volumes beyond the contracted base.

When will commercial shipments from Tanbreez begin?

Deliveries are planned on a Free on Board basis from Tanbreez's Southern Greenland port facilities once production commences. A specific production commencement date has not been publicly confirmed as of the May 2026 announcement. Investors should monitor project development updates from Critical Metals Corp for timeline guidance.

How does the Tanbreez deal reduce Western dependence on Chinese rare earths?

By establishing a binding, long-term supply agreement between a Greenlandic HREE deposit and a North American mine-to-magnet manufacturer, the deal creates a verified non-Chinese feedstock pathway for the most strategically sensitive rare earth elements. This is particularly relevant for dysprosium and terbium, where Chinese processing dominance has historically left Western defence and clean energy manufacturers with virtually no alternative supply options.

Readers seeking additional context on Western rare earth supply chain development and critical minerals strategy may find value in exploring related industry reporting available at AL Circle, which covers critical minerals, supply chain developments, and strategic resource news across global markets.

Want to Track the Next Major Critical Minerals Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including the critical and heavy rare earth elements driving Western supply chain transformation — so subscribers can identify actionable opportunities the moment they emerge. Explore Discovery Alert's discoveries page to understand how historic ASX mineral discoveries have generated substantial returns, and begin a 14-day free trial today to position yourself ahead of the market.