June 30, 2026

The Architecture of Scarcity: How the DRC Is Engineering a Cobalt Price Floor

Critical minerals markets have long operated under a fundamental tension: the countries richest in resources are rarely the ones capturing the most value from them. For decades, the Democratic Republic of Congo sat at the centre of global cobalt supply while downstream processors, refiners, and battery manufacturers in Asia and Europe captured the majority of economic returns. That dynamic is now being deliberately dismantled, one quota deadline at a time, as Congo withdraws unused cobalt export quotas with increasing regulatory confidence.

The DRC's evolution from a passive raw material exporter to an active supply architect represents one of the most consequential shifts in battery metals geopolitics of the past decade. Understanding how this system actually functions, and what it means for global supply chains, requires moving beyond headline price figures and examining the structural mechanics underneath.

When big ASX news breaks, our subscribers know first

Why the DRC's Position in Cobalt Is Unlike Any Other Critical Mineral Chokepoint

No single country dominates any major industrial commodity the way the DRC dominates cobalt. The country holds in excess of 70% of the world's known cobalt reserves, a geological reality that gives Kinshasa a degree of market leverage with no real parallel among battery-critical minerals. For comparison, Saudi Arabia's share of global oil reserves, while substantial, sits closer to 17%.

This concentration has always given the DRC theoretical pricing power. What changed in 2024 and 2025 was the institutional willingness to actually exercise it. The DRC cobalt export ban that preceded the current framework demonstrated Kinshasa's readiness to absorb short-term commercial disruption in pursuit of longer-term market influence.

The regulator at the centre of this transformation is ARECOMS, the DRC's strategic minerals authority, which has progressively moved from a licensing and compliance body toward an active market management role. Its recent actions are not incidental policy adjustments; they reflect a coherent and sustained strategy to transition the DRC from price-taker to price-maker in global cobalt markets.

From Moratorium to Quota Architecture: The Policy Timeline

The current quota system did not emerge in isolation. It is the successor to a blunter instrument: a full cobalt export moratorium that ran for approximately seven to ten months beginning in late 2024. That ban was effective in squeezing supply but carried significant diplomatic and commercial costs, creating uncertainty for long-term mining investment and drawing pressure from the major Chinese operators who dominate DRC cobalt production.

The cobalt export suspension impact on downstream battery manufacturers was considerable, with procurement teams scrambling to locate alternative sources or draw down existing stockpiles. The shift to a quota-based framework, consequently, reflects a more sophisticated approach to resource governance. Rather than a blanket prohibition, the quota system allows the DRC to:

- Maintain a legal export market that preserves commercial relationships

- Set a defined annual ceiling that anchors supply expectations

- Create compliance obligations that give the regulator ongoing leverage over individual operators

- Redirect unused or forfeited volumes toward domestically aligned projects

This transition from blunt restriction to structured scarcity management is precisely what separates the DRC's current approach from earlier resource nationalism experiments elsewhere on the continent.

How the Forfeiture Mechanism Actually Works

The operational core of the new system is a forfeiture-and-reallocation mechanism that many market participants have underestimated in its implications. The process functions as follows:

- Export quotas are allocated to licensed mining operators on a quarterly basis by ARECOMS.

- Operators must declare their shipments through the customs system before specified cut-off dates.

- Any quota volume that remains unused at the deadline is automatically forfeited, with no carryforward provision.

- Forfeited volumes are transferred into ARECOMS's centrally managed strategic quota reserve.

- Volumes within the strategic reserve are redirected toward projects aligned with national industrial priorities, including domestic processing and value-addition initiatives.

This mechanism is significant because it converts operational delays and logistics friction into permanent quota loss. Under the previous moratorium, the question was simply whether exports could occur at all. Under the quota system, the question becomes whether exports occur on schedule, with failure carrying an immediate and irreversible penalty.

Key Compliance Deadlines Under the 2025-2026 Framework

| Quota Period | Shipment Deadline | Consequence of Non-Compliance |

|---|---|---|

| Q4 2025 (unused volumes) | April 30, 2026 | Forfeited to strategic reserve |

| Q1 2026 (unused volumes) | June 30, 2026 | Forfeited to strategic reserve |

| H1 2026 (customs declaration) | July 5, 2026 | Ineligible for first-half quota |

| Full enforcement commencement | July 1, 2026 | All new rules apply in full |

According to reporting on quota deadlines, Congo gave cobalt miners until end-April to utilise their 2025 export quotas, a deadline that caught several operators off guard. Beyond missed deadlines, ARECOMS has indicated it may withdraw quotas entirely from operators engaged in any of the following:

- Failing to export within the designated compliance window

- Transferring quota entitlements to third parties without authorisation

- Processing artisanal or third-party cobalt material without regulatory approval

- Any breach of ARECOMS compliance standards more broadly defined

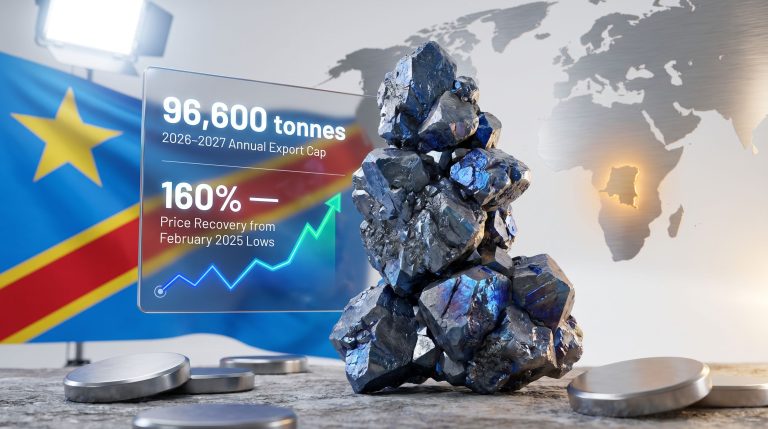

The 96,600-Tonne Cap: Supply Mathematics and Market Consequences

The 2026 annual export ceiling tells a striking story when set against recent production figures. The permitted export volume is structured as follows:

| Quota Category | Annual Volume (Tonnes) |

|---|---|

| Standard miner allocations | 87,000 |

| Strategic national reserve | 9,600 |

| Total permitted exports | 96,600 |

| Estimated DRC production in 2024 | ~204,000 |

| Implied export reduction vs. prior output | ~53% |

The arithmetic is stark. At the 2026 cap, permitted cobalt exports from the world's dominant producer are running at roughly half the volume that reached global markets in 2024. Furthermore, even accounting for existing stockpiles held by producers and traders, this represents a structural rather than temporary supply constraint.

The 10% strategic reserve carve-out (9,600 of the 96,600 total tonnes) deserves particular attention. This is not merely a buffer; it is the instrument through which ARECOMS retains discretionary control over a meaningful slice of export volume. Projects deemed of national interest, particularly those involving domestic processing and local beneficiation, have preferential access to these volumes. This design feature directly incentivises miners to invest in in-country value addition if they want to access the full quota pool.

The Under-Utilisation Problem That Triggered the Forfeiture Rules

One of the less widely understood drivers of the forfeiture policy is the pattern of quota under-utilisation that emerged during the initial export restriction period. During Q4 2025, actual shipment volumes from major operators reportedly reached only 30 to 50% of allocated quota entitlements.

The gap between what was permitted and what was shipped was not primarily a matter of market reluctance. Structural friction across DRC logistics infrastructure, including customs processing bottlenecks, paperwork delays, and port-side capacity constraints, meant that operators simply could not move allocated volumes within compliance windows. The DRC's response was revealing: rather than treating this as an operational problem requiring infrastructure solutions, ARECOMS framed it as a compliance failure requiring regulatory consequences.

This reframing fundamentally changes the risk calculus for every operator in the basin. Logistics delays, which were previously a cost and scheduling inconvenience, have consequently been reclassified as a compliance liability with direct quota consequences. Operators must now build logistics redundancy and customs processing lead times into their shipment planning in ways they did not previously need to.

"Treating operational friction as a compliance failure is a deliberate regulatory choice. It places the burden of infrastructure and logistics adequacy squarely on the private operator, rather than on the state, and creates a permanent ratchet through which the strategic reserve can grow over time at operators' expense."

The next major ASX story will hit our subscribers first

How Major Producers Are Adapting

The four dominant operators in DRC cobalt production face meaningfully different strategic exposures under the new framework:

| Company | Nationality | Strategic Position |

|---|---|---|

| CMOC | Chinese | World's largest cobalt producer; quota compliance is existential |

| Glencore | Swiss-British | Actively pivoting toward copper; using stockpiles to manage quota |

| Eurasian Resources Group | Kazakhstani | Multi-commodity exposure limits cobalt dependency |

| Huayou Cobalt | Chinese | Vertically integrated into battery supply chains; strategic quota access critical |

Glencore's copper pivot is particularly instructive. The company has been deliberately moderating cobalt output in favour of copper production at its Congolese operations, a response to both price signals and quota management considerations. This behaviour illustrates how quota systems can reshape mine-level production decisions in ways that extend well beyond simple export logistics.

Some operators are also engaging in deliberate quota conservation, holding back shipments strategically to maintain optionality rather than simply failing to meet deadlines. This behaviour, however, risks triggering exactly the forfeiture consequences ARECOMS has designed the system to enforce.

Cobalt's 160% Price Recovery: Supply Mechanics Versus Demand Signals

Cobalt prices have risen approximately 160% from their February 2025 lows, reaching around $26 per pound ($57,320 per metric tonne) by mid-2026. Understanding the structural basis of this recovery matters enormously for assessing its durability. The Congo cobalt price impacts have reverberated through battery supply chains globally, forcing procurement teams to fundamentally reassess sourcing strategies.

| Metal | Price Movement (2025-2026) | Primary Driver |

|---|---|---|

| Cobalt | +160% | DRC supply restriction and quota architecture |

| Lithium | Variable | Demand recovery offset by new supply |

| Nickel | Moderate recovery | Indonesian supply dynamics |

| Manganese | Broadly stable | Diversified global supply base |

Crucially, cobalt's recovery is almost entirely supply-driven. Global electric vehicle demand, while growing, has not accelerated sharply enough in 2025-2026 to independently justify a 160% price move. The price signal is a direct product of the DRC's export management decisions, which means its sustainability is tied to political continuity in Kinshasa rather than to demand fundamentals alone.

This distinction matters enormously for investors and procurement strategists. A demand-driven price recovery tends to be self-sustaining as long as underlying growth continues. A supply-restriction-driven recovery is inherently fragile, contingent on regulatory consistency, enforcement capacity, and geopolitical stability in a country with a complex governance history.

Some analysts project a 24% increase in export value by 2027, even within the constrained volume ceiling, on the assumption that price gains more than offset volume reductions. Whether that projection holds depends heavily on whether ARECOMS can maintain enforcement discipline across an industry where workarounds, including artisanal channel diversion, present a structural leak in the quota framework.

The Artisanal Mining Wildcard

Any assessment of the DRC's quota architecture must grapple with the scale of artisanal and small-scale mining (ASM) activity in the Congolese cobalt sector. Artisanal cobalt production, which is not subject to the same quota obligations as large-scale licensed miners, represents a meaningful share of total output and a potential bypass route for material that would otherwise be constrained by the formal quota system.

ARECOMS has specifically prohibited licensed operators from processing artisanal or third-party material without authorisation, suggesting the regulator is alert to this risk. However, enforcement across the DRC's vast and often remote mining provinces remains a formidable practical challenge. The gap between regulatory design and on-the-ground enforcement capacity is one of the most significant uncertainties in the cobalt supply outlook.

How Does the Quota System Affect Global Cobalt Production?

The constraints placed on the DRC necessarily shape global cobalt production trajectories in profound ways. With permitted volumes capped at roughly half of recent output levels, the downstream implications for battery manufacturers and EV producers are considerable, particularly given the absence of immediately scalable alternative supply sources.

Battery Chemistry Substitution: The Unintended Consequence Risk

There is a deeper strategic risk embedded in the DRC's supply management approach that receives insufficient attention: the possibility that sustained cobalt price elevation accelerates the shift toward cobalt-free battery chemistries faster than Kinshasa's planners anticipate.

Lithium iron phosphate (LFP) batteries, which contain no cobalt, have already gained significant market share in entry-level and mid-range electric vehicles, particularly in China. Nickel-manganese-cobalt (NMC) chemistries, while still dominant in higher-energy-density applications, are under competitive pressure from both LFP improvements and next-generation solid-state technologies.

If cobalt prices remain elevated for an extended period due to DRC supply management, the economic incentive for battery manufacturers to complete the transition toward cobalt-minimised or cobalt-free chemistries intensifies considerably. The DRC's strategy could, paradoxically, accelerate the very demand destruction it is trying to monetise before it occurs.

This is not a near-term risk — cobalt remains essential in high-performance cathode chemistries for the foreseeable future — but it is a medium-term strategic consideration that adds complexity to any multi-year price forecast.

The Broader African Resource Sovereignty Context

The DRC's quota architecture does not exist in isolation. It is part of a continental shift toward resource sovereignty that has seen Zimbabwe impose export restrictions on raw lithium, Namibia move to limit unprocessed mineral exports, and multiple West African states renegotiate mining fiscal terms. In addition, the intensifying US-China cobalt rivalry adds a further geopolitical dimension to every regulatory decision ARECOMS makes.

What distinguishes the DRC's approach is its sophistication. The quota system, with its forfeiture mechanics, strategic reserve carve-out, and domestic processing incentives, is a materially more nuanced instrument than the blunt export bans employed elsewhere. It attempts to manage price floors, incentivise local industrialisation, and preserve commercial relationships simultaneously.

Whether it succeeds depends on factors that extend well beyond regulatory design, including Chinese geopolitical pressure — China's refining industry processes the vast majority of DRC cobalt — infrastructure development timelines, and the DRC's internal governance capacity. These are not minor uncertainties. Independent analysis from the IEA's assessment of the temporary suspension of cobalt exports highlights how structurally significant the DRC's decisions are for global energy transition supply chains.

Frequently Asked Questions: Congo's Cobalt Export Quota Reallocation

What does it mean when Congo withdraws unused cobalt export quotas?

Unused quota volumes are forfeited at the end of each compliance window and transferred into a centrally managed strategic reserve controlled by ARECOMS. These volumes cannot be recovered or carried forward by the original quota holder.

How much cobalt can the DRC legally export in 2026?

The total permitted export volume is capped at 96,600 tonnes, comprising 87,000 tonnes in standard miner allocations and a 9,600-tonne strategic reserve carve-out.

Why did cobalt prices rise 160% since February 2025?

The DRC's progressive tightening of export controls, beginning with a multi-month moratorium and transitioning into a structured quota regime, dramatically reduced global cobalt supply and triggered a significant price recovery from multi-year lows.

Which companies carry the greatest exposure to the new quota rules?

CMOC and Glencore, as the world's largest and second-largest cobalt producers operating in the DRC, carry the most direct operational exposure. Huayou Cobalt and Eurasian Resources Group also face material compliance obligations.

Could the quota system create a structural cobalt deficit?

With permitted exports capped at roughly half of 2024 production levels, a sustained supply deficit is a credible scenario, particularly if EV demand growth continues through 2027 and cobalt-free chemistry substitution remains a medium-term rather than near-term development.

What happens to forfeited quota volumes?

Forfeited volumes are absorbed into ARECOMS's strategic quota pool and redirected toward projects supporting domestic cobalt processing, value-addition initiatives, and national economic development priorities as defined by the regulator.

What Investors and Supply Chain Strategists Should Watch

The DRC's quota reallocation policy introduces a new category of risk for cobalt-exposed investors and downstream battery manufacturers: regulatory cadence risk. Under the old moratorium model, the binary question was simply whether exports were permitted. Under the quota model, risk is distributed across quarterly deadlines, compliance windows, enforcement decisions, and strategic reserve reallocation choices.

Key indicators worth monitoring through the second half of 2026 include:

- Actual quota utilisation rates reported by major operators versus allocated volumes

- The scale of forfeiture into the strategic reserve at each deadline

- Whether ARECOMS exercises full quota withdrawal against any operator, which would signal maximum enforcement intent

- Progress on domestic processing investments that could access the strategic reserve carve-out

- Any signs of Chinese diplomatic or commercial pressure on the quota framework

- LFP market share gains in key EV markets as a proxy for cobalt demand durability

The DRC's experiment in sovereign supply management is still in its early stages. The quota architecture is coherent in design, but its real-world effectiveness depends on enforcement capacity, geopolitical resilience, and whether the price signals it generates are sufficient to fund the domestic processing ambitions that underpin the entire strategy. Those are significant open questions, and the answers will shape cobalt markets for years to come.

This article is strictly for informational purposes only and does not constitute financial or investment advice. Commodity price forecasts and supply projections involve significant uncertainty and should not be relied upon as the basis for investment decisions.

Want to Track the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly converting complex mineral data — across more than 30 commodities, including battery metals — into actionable investment insights, so subscribers are positioned ahead of the market the moment a significant discovery is made. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to experience the service firsthand.